More than 50% of asset managers continue to bet on the 60/40 model

| Por Romina López | 0 Comentarios

Did the year 2022 destroy the relevance of the 60/40 model? Are portfolio managers willing to implement other options? What alternatives are available in the market for asset managers to facilitate portfolio diversification? According to FlexFunds, a leading company in the design and launch of investment vehicles (ETPs), uncertainty becomes the playing field, and adaptation becomes imperative.

FlexFunds, has taken the initiative to prepare the 1st Report of the Asset Securitization Sector: a study of the main trends of these financial instruments to raise capital in international markets. This report reveals that despite poor results in the last year, more than half of the surveyed asset managers continue to bet on the 60/40 portfolio diversification model (request this full report by sending an email to info@flexfunds.com).

The 60/40 portfolio management model is an asset allocation strategy that involves a 60% weighting of the portfolio in equities and a 40% in fixed-income assets. This approach is commonly used by portfolio managers as a way to diversify risk and ensure a certain level of return in an investment portfolio.

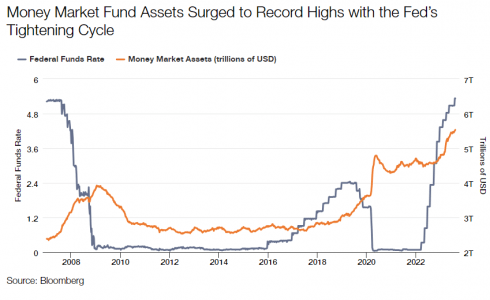

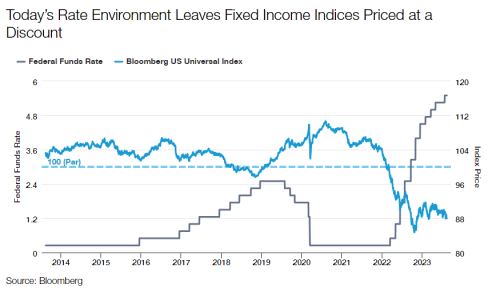

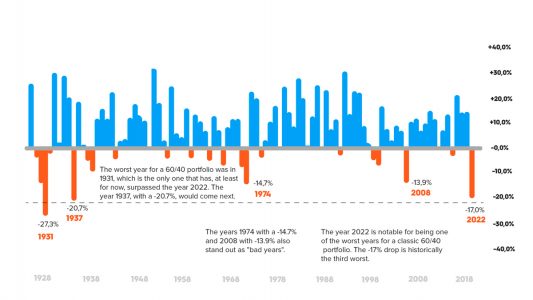

The year 2022 marked a dark milestone for 60/40 portfolios, worsening even the negative returns experienced during the economic crises of 2001 and 2008. Traditional recipes failed, and both the fixed-income and equity markets suffered significant losses. The war in Ukraine and the rapid rise in interest rates in the U.S. and the eurozone created a very complex scenario where the orthodoxy of the price relationship between stocks and bonds was not met.

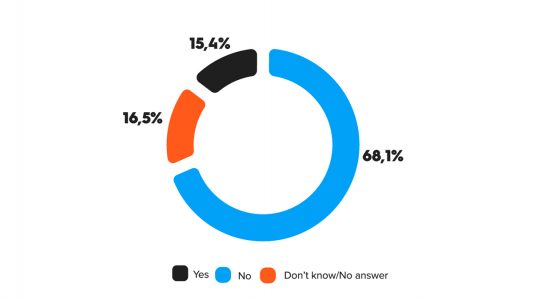

To the question, “Do you think the 60/40 portfolio composition model worked in the last 12 months?” more than 68% of asset managers and investment experts answered that the 60/40 model did not work, while 15.4% believe it did. However, 16.5% of the sample does not have a clear opinion on the matter. It is worth noting that among those who believe it did not work, almost 75% think it was due to the rise in interest rates, while nearly 10% argue that it was due to the decrease in equities.

Amid the uncertainty, portfolio management becomes a delicate art. Diversification, a cornerstone, was challenged by the lack of correlation between fixed income and equities. Traditional strategies, such as the 60/40 model, faltered, revealing their vulnerability to the changing economic and financial paradigm.

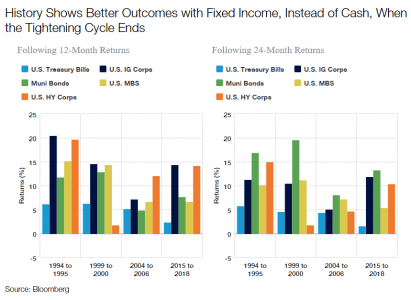

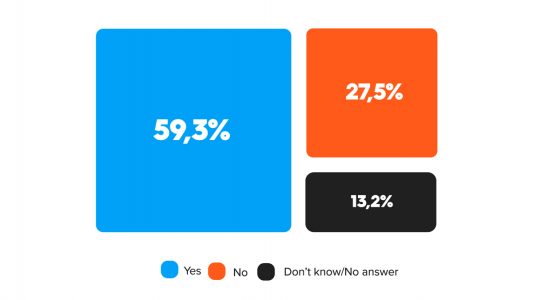

However, despite the majority of respondents agreeing that the 60/40 model did not work, when asked, “Do you think the 60/40 model will remain relevant?” 59% of asset managers and investment experts believe that this strategy will continue to be relevant. This fact highlights two aspects: first, its future application will depend on how the markets and economic conditions evolve, and second, perhaps paradoxically, it contradicts the earlier assertion that most respondents believe it did not work in 2022, yet now there is a majority opinion that it will remain a relevant strategy.

The global trend in portfolio diversification with new asset classes such as real estate, crypto assets, and private equity offers divergent alternatives to the classic 60/40 model in the international market. FlexFunds, through its asset securitization program, provides investment managers with the flexibility to design a portfolio with multiple asset classes and repackage it for distribution through Euroclear to private banking platforms.

How should asset managers adapt? What investment vehicles do investment advisors prefer to diversify their portfolios? What are the industry’s biggest challenges for clients and capital acquisition? Discover all of these key trends and more in the 1st Report of the Asset Securitization Sector by FlexFunds, which gathers the opinions of more than 80 asset managers and investment experts from 15 countries in Latin America, the U.S., and Europe.

Request it by sending an email to: info@flexfunds.com