Navegar el miedo, las narrativas y la ilusión de seguridad

Los periodos de tensión en los mercados suelen describirse como momentos de mayor riesgo. En realidad, con la misma frecuencia son momentos de mayor atención al riesgo.

Durante gran parte de la era financiera moderna, las incertidumbres de mercado llegaban a los inversores de forma episódica: a través de los periódicos diarios, los informativos de la noche o actualizaciones financieras periódicas. Hoy, en cambio, los inversores se enfrentan de manera continua a posibles fuentes de riesgo. Tienen una exposición casi constante a noticias de última hora, opiniones y comentarios en una amplia variedad de plataformas digitales. Las estimaciones sugieren que el consumidor medio dedica actualmente aproximadamente seis horas al día al consumo de medios digitales, gran parte de ellos vinculados, directa o indirectamente, a la información. En este entorno, las personas reciben recordatorios constantes de una lista cada vez mayor de focos de preocupación potencial: el conflicto en Oriente Medio, la guerra entre Rusia y Ucrania, las tensiones en torno a China y Taiwán, el aumento de la polarización, los crecientes niveles de deuda soberana, etc. Para agravar la situación, la investigación muestra que los medios de comunicación dependen cada vez más de contenidos orientados a captar la atención y a maximizar los clics para impulsar la interacción, especialmente en las plataformas sociales, donde los titulares dramáticos generan más participación que la información neutral.

Ante este flujo constante de información, los inversores buscan de forma natural maneras de recuperar una sensación de control. En lugar de abordar cada foco de preocupación por separado, muchos se inclinan por grandes narrativas que ofrecen una sensación de protección frente a un amplio abanico de escenarios, creando así el terreno propicio para la aparición de una sensación de seguridad.

Cuando el “refugio seguro” se convierte en consenso

El aumento de la ansiedad suele dirigir a los inversores hacia activos percibidos como refugio, como la deuda soberana, las divisas de reserva y los metales preciosos, con el oro a la cabeza. Tradicionalmente considerado una cobertura frente a la inflación, la depreciación de las divisas y la inestabilidad política, el oro puede desempeñar un papel legítimo en carteras diversificadas. El problema surge cuando la protección se convierte en consenso, cuando la diversificación da paso a un posicionamiento masificado como respuesta a la incertidumbre.

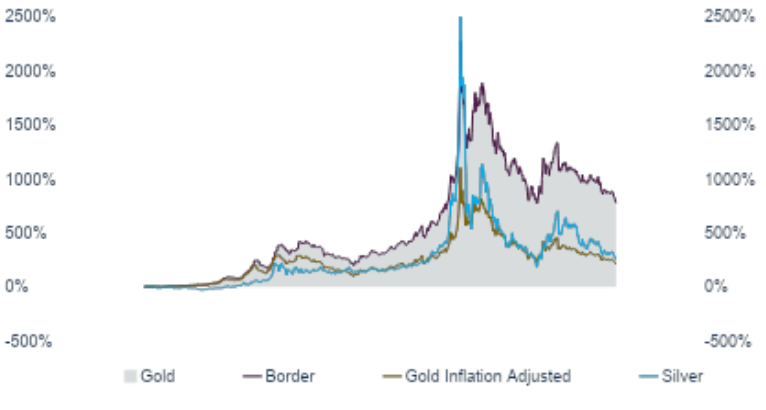

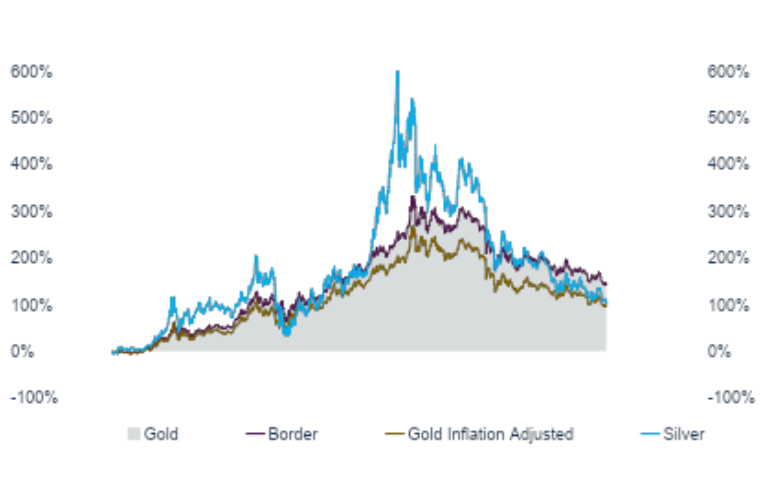

La historia ofrece ejemplos reiterados. En la década de 1970, el oro se revalorizó casi 24 veces a medida que la inflación, la inestabilidad monetaria y las tensiones geopolíticas transformaban el comportamiento de los inversores, para después caer aproximadamente un 65 % en los cuatro años siguientes, una vez que la inflación fue controlada y se restauró la credibilidad de la política monetaria. La magnitud de aquella subida superó ampliamente lo que podía explicarse únicamente por la inflación, reflejando un periodo en el que la demanda de protección llevó los precios muy por encima de su justificación fundamental. Tras la crisis financiera global, se produjo una dinámica similar: el oro avanzó en torno a un 170 % entre 2008 y su máximo de 2011, a medida que se intensificaban los temores sobre la fragilidad del sistema y la depreciación monetaria, seguido de una caída de alrededor del 45 % durante los cuatro años posteriores, cuando el crecimiento se estabilizó y regresó el apetito por el riesgo. En ambos episodios, el papel del oro pasó de ser una cobertura de cartera a convertirse en una expresión ampliamente compartida del miedo macroeconómico.

Cuando un activo se etiqueta de manera universal como refugio, su comportamiento cambia. La evolución de su precio refleja cada vez más el posicionamiento de los inversores en lugar de los fundamentales, y esta dinámica suele trasladarse a activos relacionados. La plata, por ejemplo, ha sido arrastrada repetidamente por los rallies impulsados por el oro, a pesar de que sus fundamentos de oferta y demanda eran más débiles, solo para sufrir caídas mucho más profundas cuando el sentimiento cambió. Lo que comienza como una medida de protección puede transformarse silenciosamente en una operación basada en momentum.

Cómo se ve una defensa real

La verdadera defensa de una cartera rara vez se logra mediante la concentración en un solo activo, sin importar lo convincente que sea la narrativa. Se alcanza a través del equilibrio y anclando las carteras en los fundamentales en lugar del miedo.

Mientras que las operaciones basadas en el miedo se centran en lo que podría salir mal, los resultados corporativos reflejan lo que sigue funcionando bien. A pesar de guerras, recesiones y convulsiones políticas, los beneficios agregados han demostrado una capacidad persistente de recuperación y acumulación, impulsados por la capacidad de las empresas para reestructurar precios, reasignar capital, innovar y controlar costes. Datos recientes refuerzan esta resiliencia: el S&P 500 ha registrado múltiples trimestres consecutivos de crecimiento interanual de beneficios de dos dígitos, con estimaciones futuras que apuntan a un crecimiento continuo de un dígito alto a bajo doble dígito. Este impulso existe junto a una economía estadounidense que ahora es aproximadamente un 40 % más grande en términos nominales que al inicio de la pandemia, lo que subraya la durabilidad de la expansión.

Una cartera bien construida refleja esta realidad. La renta fija proporciona ingresos y estabilidad relativa, las alternativas ofrecen diversificación, y la renta variable brinda exposición a empresas con flujos de caja duraderos y capacidad de fijación de precios. Este enfoque no elimina las caídas, pero reduce la dependencia de un solo resultado y evita pagar precios máximos por una comodidad psicológica. La defensa, en este sentido, no es retirada; es composición.

La disciplina de ver con claridad

Los errores de inversión más significativos rara vez se cometen durante periodos de crisis real; suelen ocurrir cuando el miedo lleva a los inversores a tratar el entorno actual como excepcionalmente amenazante. La historia demuestra que los mercados han operado repetidamente a través de guerras, divisiones políticas, inflación y aumento de la deuda, incluso cuando las narrativas predominantes aumentaban la incertidumbre y acortaban los horizontes de decisión. En estos periodos, el desafío no es la presencia del riesgo en sí, sino la tendencia a confundir la tranquilidad con una gestión de riesgo sólida. La disciplina, la diversificación y el énfasis en los fundamentales siguen siendo las formas más fiables de navegar la incertidumbre, no evitando la volatilidad, sino evitando la sobrerreacción.

Tribuna de opinión firmada por Juan Carlos Guerra, CFA® and CAIA charterholder de Boreal Capital Management.

Legal Disclaimer Boreal Capital Management AG

Investment advisory products and financial services are provided by Boreal Capital Management Ltd (“Boreal”), a Swiss external asset manager regulated by the SRO AOOS.

Boreal Capital Management Ltd is not permitted to give legal or tax advice. Only an attorney can draft legal documents and provide legal services and advice. Clients of Boreal should consult with their legal and tax advisors prior to entering into any financial transaction or estate plan.

The opinions and information contained herein have been obtained or derived from sources believed to be reliable, but Boreal makes no representation or guarantee as to their timeliness, accuracy or completeness or for their fitness for any particular purpose. The information contained herein does not purport to be a complete analysis of any security, company, or industry involved. Opinions and information expressed herein are subject to change without notice. Boreal and/or its affiliates may have issued materials that are inconsistent with or may reach different conclusions than those represented in this document, and all opinions and information are believed to be reflective of judgments and opinions as of the date that material was originally published. Boreal is under no obligation to ensure that other materials are brought to the attention of any recipient of this document. Boreal accepts no liability whatsoever and makes no representation, warranty or undertaking, express or implied, for any information, projections or any of the opinions contained herein or for any errors, omissions or misstatements in the document. Boreal does not undertake to update this document or to correct any inaccuracies which may have become apparent after its publication.

This material is not to be construed as an offer to sell or a solicitation of an offer to buy any security nor a solicitation to buy, subscribe or sell any currency or product or financial instrument, make any investment or participate in any particular trading strategy in any jurisdiction where such an offer or solicitation would not be authorized or to any person to whom it would be unlawful to make such an offer or invitation. The information and material presented herein are for general information only and do not specifically address individual investment objectives, financial situations or the particular needs of any specific person who may receive this presentation. It does not replace a prospectus or any other legal document relating to any specific financial instrument which may be obtained upon request from the issuer of the financial product. In this document Boreal makes no representation as to the suitability or appropriateness of the described financial instruments or services for any recipient of this document nor to their future performance. Each investor must make their own independent decision regarding any securities or financial instruments mentioned in this document and should independently determine the merits or suitability of any investment. Before entering into any transaction, investors are invited to read carefully the risk warnings and the regulations set out in the prospectus or other legal documents and are urged to seek professional advice from their financial, legal, accounting and tax advisors with regard to their investment objectives, financial situation and specific needs. The tax treatment of any investment depends on your individual circumstances and may be subject to change in the future. Boreal does not provide any tax advice within this document and the investor’s individual circumstances were not taken into account when providing this document.

Investing in any security or investment strategies discussed herein may not be suitable for you, and you may want to consult a financial advisor. Nothing in this material constitutes individual investment, legal or tax advice. Investments involve risk and any investment may incur either profits or losses. The investments mentioned herein may be subject to risks that are difficult to quantify and to integrate into the valuation of investments. In general, products with a high degree of risk such as derivatives, structured products or alternative/non-traditional investments (such as hedge funds, private equity, real estate funds etc.) are suitable only for investors who are capable of understanding and assuming the risks involved. The value of any capital investment may be at risk and some or all of the original capital may be lost. The investments are exposed

to currency fluctuations and may increase or decrease in value. Fluctuations in exchange rates may cause increases or decreases in your returns and/or in the value of the portfolio. The investments may be exposed to currency risks because a financial instrument or the underlying investment of a financial instrument is dominated in a currency different from the reference currency from the portfolio or other than the one of the investor’s country of residence.

This document may refer to the past performance of financial instruments. Past performance does not guarantee future results. The value of financial instruments may fall or rise. All statements in this document other than statements of past performances and historical facts are “forward-looking statements” which do not guarantee the future performance. Financial projections included in this document do not represent forecasts or budgets but are purely illustrative examples based on series of current expectations and assumptions which may not eventuate. The actual performance, results, market value and prospects of a financial instrument may differ materially from those expressed or implied by the forward-looking statements in this document. Boreal disclaims any obligation to update any forward-looking statement as a result of new information, future events or otherwise. The information contained in this document is neither the result of financial analysis within the meaning of the Swiss Banking Association “Directive on the Independence of Financial Research” nor of independent investment research as per EU regulation on MiFID provisions.

Unless otherwise stated, the portfolios and its performances herein do not account for costs, fees, commissions, expenses charged on issuance and redemption of securities or other, nor any taxes that may be levied and / or charges, have no track record and have not been independently audited. Boreal shall accept no liability for any loss arising from the use of this material, nor shall Boreal treat any recipient of this material as a customer or client simply by virtue of its receipt. The information herein is not intended for any person residing in any jurisdiction in which it is unlawful to distribute this material.

This document is confidential and is intended only for the use of the person to whom it was delivered. This document may not be reproduced in whole or in part or delivered to any other person without the prior written approval of Boreal.