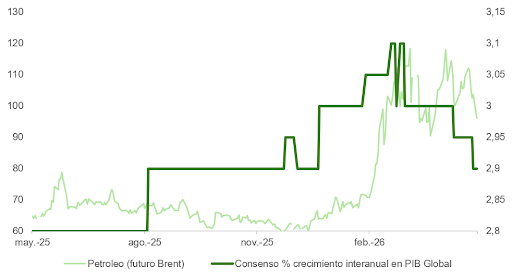

Markets had chosen to ignore the latest U.S. military strikes against Iran, anchored to the narrative of an imminent agreement that would reopen the Strait of Hormuz. Brent crude fell from $104 per barrel on Friday to $93.7 per barrel, while equity markets consolidated gains, with the S&P 500 reaching a new high during Tuesday’s session.

The problem is that market optimism far exceeds the available evidence. A preliminary agreement—featuring a 60-day ceasefire, the lifting of the naval blockade, and the start of nuclear negotiations—faces difficult obstacles, including frozen Iranian assets, Israel’s position, demands regarding the nuclear program, and the fragility of any lasting regional peace framework.

The agreement reported by Axios on Thursday, which would extend the truce for an additional 60 days, would require Iran to remove mines from the Strait in order to restore normal maritime traffic. However, the probability that such an arrangement will lead to lasting peace is not particularly high. In our view, the market is pricing in an excessively benign scenario relative to the actual balance of risks.

The S&P 500 responded to the Axios report with a modest gain of 0.58%, while the Bloomberg Global Equity Index rose 0.41%. Since the ceasefire announcement at the end of February, global equities have gained 7%, led by cyclical stocks and technology. Is it possible that the market has already priced in the good news?

This assessment has also been shared by prominent European Central Bank officials, including Philip Lane, Olli Rehn, and Luis de Guindos.

The Cumulative Cost of Three Months of Closure

We have now spent nearly three months with the Strait of Hormuz effectively closed, and the cumulative impact on the global economy is becoming increasingly difficult to ignore. Crude oil remains above $90 per barrel, while gasoline prices in the United States are approaching the record highs seen after the 2022 invasion of Ukraine.

The impact, however, extends well beyond the energy sector. It affects fertilizers, petrochemicals, sulfur, and helium, disrupting supply chains whose consequences are only beginning to appear in macroeconomic data.

U.S. GDP, released on Thursday and weighed down by net exports, is growing at an annualized rate below the economy’s long-term potential (1.6% versus 1.8%) and below consensus expectations (2%). Consumer spending is also beginning to show signs of strain, as household income lags expenditure (personal income was flat compared with March, while nominal spending rose 0.05%). The gap is being financed through savings, which at 2.6% are starting to run thin.

Possible Scenarios and Positioning

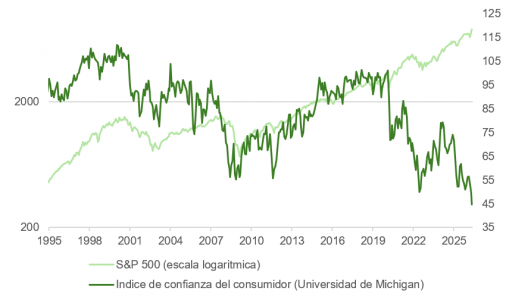

The situation is extremely difficult to manage. If the memorandum referenced by Axios does not materialize, another two or three months of closure would exhaust available reserves, force refinery cutbacks, and ultimately lead to demand destruction and a global recession. The political incentive to resolve the situation is clear: with the midterm elections on the horizon, the Trump administration cannot afford to let energy prices continue to erode consumer confidence, which, according to the latest University of Michigan survey, is at historic lows. In light of recent developments, the possibility of an “escalate to de-escalate” strategy cannot be ruled out—briefly resuming attacks in order to force Tehran back to the negotiating table. If that tactic were to succeed and the Strait of Hormuz were reopened, the decline in oil prices could be just as dramatic as the previous surge.

Our six- and twelve-month outlook is that both oil prices and bond yields will be lower than current levels. The key positioning question lies in the path we will have to travel to get there.

The Federal Reserve at a Historic Crossroads

These uncertainties do not affect only investors. The inflationary environment has created one of the most challenging monetary policy situations in years for central banks, and particularly for the Federal Reserve.

Core inflation has rebounded sharply: the Final Demand Producer Price Index, excluding food and energy, currently stands at 5.25%. At the same time, the yield on the two-year Treasury note has risen above the federal funds rate, a signal that has historically preceded interest-rate increases over the past thirty years.

The Taylor Rule also suggests room for a 25-basis-point rate hike in December, a move to which the market currently assigns a 72% probability.

The Federal Reserve finds itself at a crossroads. If it raises interest rates, it will put pressure on equity valuations and weigh on economic growth. If it refrains from doing so, the bond market could conclude—as it did in 2022–2023—that the central bank has fallen behind the curve. In either scenario, equities would likely react negatively.

That said, there are important nuances. Core inflation excluding housing has remained close to the Fed’s 2% target for nearly three years. The recent increase in the housing component reflects a statistical effect linked to the government shutdown the previous year and should reverse in the coming months.

At the same time, unemployment continues to rise across most G10 economies, reducing the risk of a wage-price spiral.

And although household spending-intention surveys indicate caution in response to persistently higher fuel prices, tax refunds associated with the OBBA plan have so far offset that effect, according to estimates from Brown University.

According to the Tax Foundation, as of April 3, 2026, the cumulative value of refunds issued by the IRS totaled 241.7 billion dollars, 30.7 billion more than during the same period in 2025. The agency processed 69.8 million tax returns, compared with 67.7 million the previous year, and nearly 70% of filed returns resulted in refunds.

Taken together, these refunds amount to approximately 1.7% of U.S. GDP, compared with an estimated negative impact of 0.7% from higher fuel prices.