Investors saved nearly 6.8 billion dollars in fund-related expenses last year, according to an estimate in Morningstar’s 2026 US Fund Fee Study report, which analyzes data from 2025. “Any reduction in fees represents a major advantage for investors, as fees compound over time and drag down returns,” the study explains.

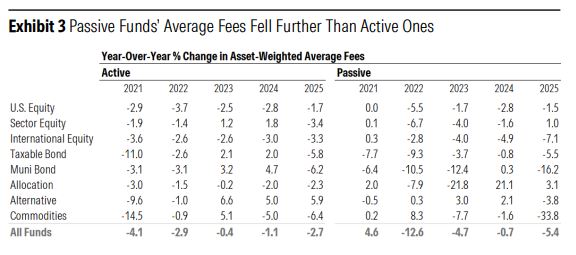

All broad indicators for US fund fees declined once again. Morningstar’s database on US open-end mutual funds and ETFs reveals that the asset-weighted average expense ratio was 0.32% in 2025, representing a 5.6% decline compared to 2024.

Among other conclusions, the report highlights that ETFs are considerably cheaper than mutual funds—both the equal-weighted and asset-weighted average fees for ETFs stood at around half of the fees charged by mutual funds, respectively—and that the fee gap between new mutual funds and new ETFs had been narrowing for years, but it widened in 2025. “The launch of a few high-cost mutual funds pushed the average cost of new mutual funds back above 1% for the first time since 2015. Recently launched ETFs are also more expensive than they used to be, reflecting the proliferation of complex and high-cost strategies being incorporated into the ETF structure,” the report notes.

The asset-weighted average represents a more accurate picture of the costs borne by fund investors, as it approximates what investors actually paid, on average, in fees for the funds they invested in. For instance, the asset-weighted average expense ratio for active US equity funds was 0.58% in 2025, compared to the 1% obtained when calculating an equal-weighted average for this group. Funds with expense ratios above 1% accounted for a small portion of the assets invested in active US equity funds at the end of 2025, according to the study.

When analyzing new fund launches and their costs, the report outlines two trends:

ETFs remain the preferred vehicle for both investors and providers.

Relatively expensive launches offer better business opportunities than cheaper funds.

Active ETFs Set the Trend

The combination of these two trends results in the proliferation of actively managed ETFs. In 2025, there was a surge in active ETF launches: out of the 1,131 exchange-traded funds created last year, 950 were actively managed. However, many of them do not entirely fit the traditional characteristics of active ETFs, according to the study. While there were some new low-cost ETFs managed by fundamental active managers, the vast majority of new launches “venture into territory that traditional major players do not typically explore.”

Smaller ETF providers, backed by white-label ETF firms, have flooded the market with a wide range of niche products. These ETFs feature novel risk/return profiles and generally do not face competition from the largest ETF managers. Vanguard, iShares, and State Street do not offer funds in the “leveraged equity” category. State Street and iShares do offer derivative income ETFs, but their presence in that category is limited.

Funds in these categories usually charge higher fees than those in more traditional categories, such as equities or bonds. Given that fees are a major source of revenue for asset managers, it is easy to understand why some firms are leaning into these higher-cost segments. Success in ETFs is difficult to achieve, but managing to do so with relatively expensive ETFs can yield substantial windfalls for their sponsors. These categories have not experienced the fee competition that has long been seen in other areas.

Which Active ETFs Will Succeed?

Active ETFs face an uphill battle. Although they could throw a lifeline to mutual fund managers suffering from asset outflows, it is impossible to fight against broad trends. Investors have overwhelmingly preferred cheap and predominantly passive funds.

Moving a mutual fund strategy into an ETF or adding an ETF share class may drum up interest for a while. However, based on the report’s data, in the long run, “other factors will determine a fund’s staying power,” notes Zachary Evens, Manager Research Analyst at Morningstar. Performance matters, but trends show that for active funds to succeed, they must be cheap. Consequently, it remains to be seen whether the emergence of novel and relatively expensive ETFs will be enough to reverse the long-term trend of investors paying less and less for their funds year after year, according to the expert.