For much of the past two decades, asset management was governed by a relatively simple logic: generating consistent returns attracted capital. Alpha was the primary competitive differentiator, and distribution capacity was, in many cases, a natural byproduct of performance.

That model began to change.

Today, even managers with strong track records, sophisticated investment processes, and differentiated strategies are struggling to scale their businesses. The problem is no longer exclusively financial- it is structural.

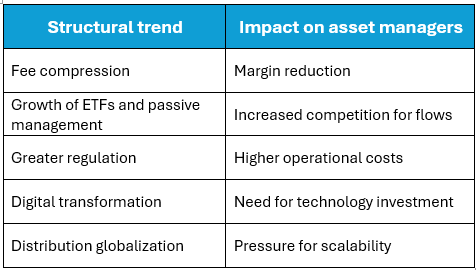

Margin pressure, the concentration of flows in large platforms, the growth of passive management, rising regulatory costs, and operational fragmentation are redefining the economics of asset management.

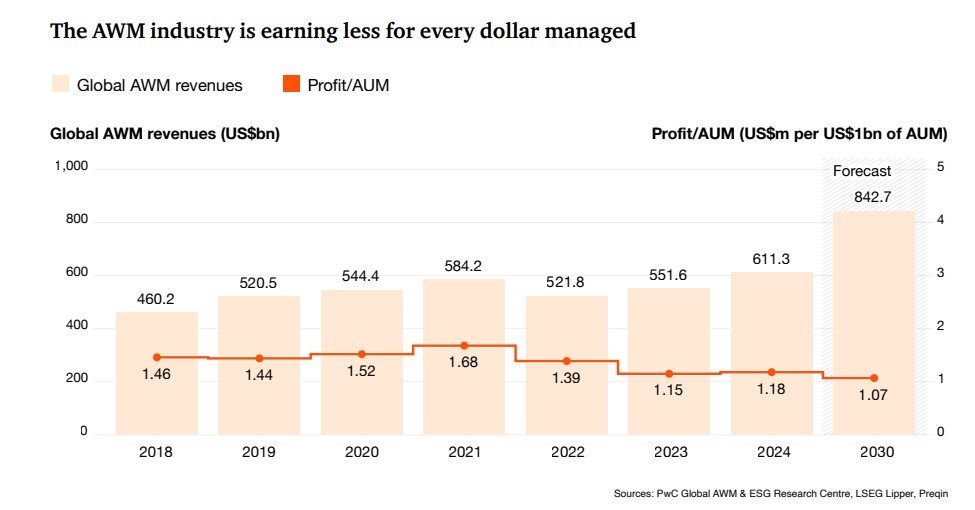

According to PwC, the industry’s profit per AUM has fallen approximately 19% since 2018, while more than two-thirds of many firms’ revenues are already consumed by operational, technology, and compliance costs.

At the same time, McKinsey & Company describes a “great convergence” among wealth management, technology, alternative assets, and global distribution, where operational scale and financial infrastructure are becoming as relevant as investment capability itself.

In other words: asset management is no longer purely a business of asset selection; it is becoming a business of infrastructure, distribution, and efficiency.

And that fundamentally changes how many managers will need to compete over the next decade.

The structural pressure on the conventional model

Asset management is undergoing a structural transformation. Fee compression, the growth of passive management, rising regulatory requirements, and technological pressure are forcing many firms to rethink how to scale their investment strategies.

At the same time, the globalization of distribution is favoring platforms with greater operational capacity, institutional integration, and international reach.

The new economics of asset management

Source: Own elaboration based on data from PwC, McKinsey, Deloitte, and ETFGI

In this environment, many managers are finding that the challenge is no longer solely about generating performance, but about enabling their strategies to grow, operate efficiently, and reach new global distribution channels.

The great migration toward scalable infrastructure

The transformation of asset management is also reflected in the evolution of investment vehicles used to distribute strategies globally.

The industry is rapidly migrating toward more liquid, efficient structures compatible with international institutional platforms. ETFs, ETPs, SMAs, and hybrid vehicles are no longer simply financial products; they are becoming distribution infrastructure.

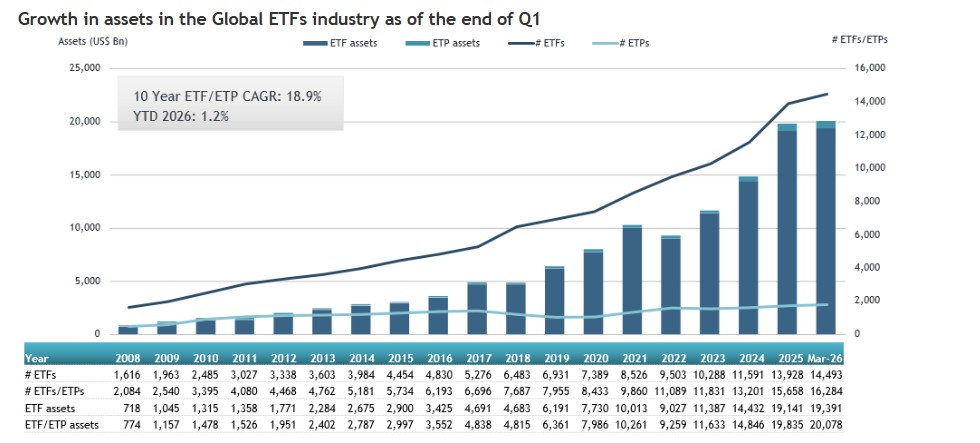

According to ETFGI, the global ETF and ETP industry recorded record flows during the first quarter of 2026, driven by growing demand for efficient, transparent, and globally distributable vehicles.

Source: ETFGI data sourced from ETF/ETP sponsors, exchanges, regulatory filings, Thomson Reuters/Lipper, Bloomberg, publicly available sources and data generated in-house. Note: “ETFs” are typically open-end index funds that provide daily portfolio transparency, are listed and traded on exchanges like stocks on a secondary basis as well as utilizing a unique creation and redemption process for primary transactions. “ETPs” refers to other products that have similarities to ETFs in the way they trade and settle but they do not use a mutual fund structure. The use of other structures including grantor trusts, partnerships, notes and depositary receipts by ETPs can create different tax and regulatory implications for investors when compared to ETFs which are funds.

The phenomenon runs far deeper than a simple shift in product preferences.

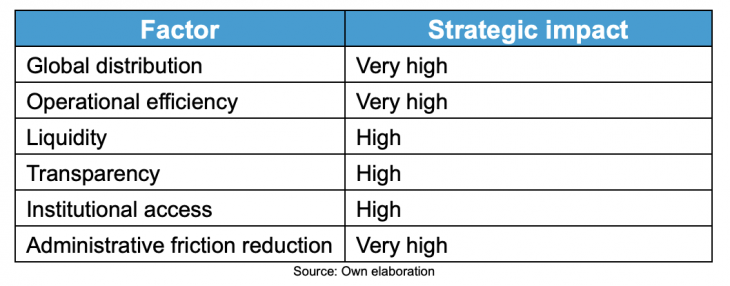

Institutional investors, offshore platforms, and private banking networks are prioritizing structures capable of combining:

- Liquidity,

- Operational efficiency,

- Transparency,

- Ease of integration,

- Compatibility with global custody and distribution infrastructures.

This explains why the growth of ETPs, ETFs, and securitized structures has accelerated in recent years. The industry is evolving toward models where distribution capacity is as important as investment capability.

What drives the growth of ETFs and ETPs

The real bottleneck is no longer performance: it is distribution

Having a strong strategy no longer guarantees AUM growth. For many managers, the challenge lies in enabling that strategy to scale, operate efficiently, and reach new international distribution channels.

The ability to access banking platforms, global custodians, and vehicles compatible with international financial infrastructure is becoming an increasingly significant differentiator within the industry.

This is especially visible in LATAM and US Offshore, where independent managers, RIAs, multifamily offices, and investment boutiques seek more flexible structures to compete globally without taking on the operational complexity of building conventional vehicles from scratch.

The III Annual Report of the Asset Securitization Sector, authorized by FlexFunds and Funds Society, reflects this evolution: securitization is consolidating as a pathway for creating customized investment vehicles, enhancing global distribution, and facilitating capital raising through international banking platforms.

The next competitive advantage will be financial infrastructure

The asset management industry is entering a phase where generating strong returns remains essential but is no longer always sufficient to drive business growth.

More managers are discovering that distribution capacity, operational efficiency, and access to global financial infrastructure are beginning to play a role as important as the investment strategy itself.

And that explains the growth of more flexible and scalable models within the industry, as well as the growing interest in structures that provide more efficient access to new international distribution channels.

In that context, specialized platforms like FlexFunds are part of an evolution that is helping managers, advisors, and family offices transform investment strategies into solutions ready to compete in global markets.

Because, ultimately, the future of asset management will likely belong not only to those who generate the greatest alpha, but to those who manage to scale it.

By Funds Society

By Funds Society