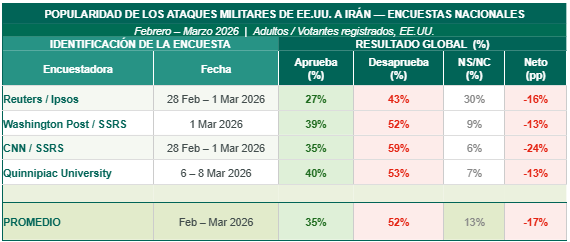

One more week, market attention remains focused on energy prices and fears of a possible stagflation. The verdict remains one of contained concern, without panic, as the conflict in Iran has increased volatility but has not severely damaged the performance of risk assets.

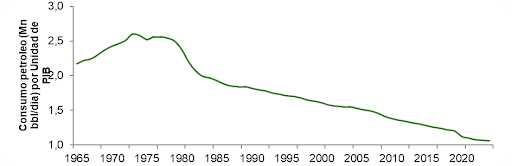

The macroeconomic situation is different from the one that preceded the 2022 energy crisis. In addition, the world is now 60% less dependent on oil than in the 1970s, which mitigates the structural impact.

That said, the historical threshold for real damage is clear: oil needs to more than double to trigger a recession or a bear market. In the case of WTI, that implies sustainably exceeding $140 per barrel, an outcome that is possible but not yet the base case. If energy spending were to double, it would absorb approximately 7% of U.S. disposable income, slowing consumption and weakening the Republican bloc ahead of the midterm elections.

Iran cannot win militarily, but it can keep oil prices elevated long enough to force a shift in Washington’s stance. Trump, under pressure from a largely anti-war public, the proximity of legislative elections, and an affordability crisis directly affecting his electoral base, has strong incentives to resolve the conflict quickly. Markets are pricing in a favorable outcome, but a deterioration in the situation could generate a further correction, not necessarily a bear market, but an episode uncomfortable enough to precipitate a resolution.

In recent days, we have received clear signs of a conciliatory stance from Trump, but Iran continues to play cat and mouse. The new deadline set by the U.S. president to reach a preliminary agreement expires on April 6.

Moreover, the macroeconomic similarity to the First Gulf War discourages abrupt changes in portfolio composition. In 1990–91, the U.S. economy was already losing momentum before Iraq invaded Kuwait on August 2, 1990. In 2026, the pattern is repeating: before the attacks on Iran, the economy was already feeling the impact of intermittent tariffs, weak hiring, and inflationary pressures that, although easing, had not disappeared. In fact, Greenspan had already been cutting rates for a year when Iraq invaded Kuwait, just like Powell, who had also begun easing before the Iranian conflict, reducing rates from 5.25%–5.50% to around 4.25%–4.50% between the second half of 2024 and early 2025.

The rate cuts implemented by the Fed in the second half of 2025 and the fiscal stimulus from the OBBBA plan are acting as buffers against the effects of the war on the economy. If the crisis is resolved within a reasonable timeframe, the boost to equities could be just as strong: from the lows of October 1990, the S&P 500 surged 26% in just three months, quickly recovering pre-conflict levels.

The outlook for the fixed income market points in the same direction. In 1990, Greenspan paused rate cuts when inflation expectations rose due to higher oil prices, and Treasury yields increased accordingly. However, the deterioration in the labor market and the recession forced a resumption of cuts, and by the end of that year, Treasury yields were below pre-conflict levels.

Europe: a less burdensome starting point than in 2022

Although logic suggests comparing the Iranian conflict with the 2022 energy crisis, the starting point is substantially different. When Russia invaded Ukraine, eurozone inflation was already մոտ 6%. Today, with headline inflation at 1.9% and wage growth below 2%, the ECB has insufficient justification to raise rates.

Energy prices should be treated as a temporary supply shock, not as structural inflationary pressure. Tightening monetary policy in this context would repeat Trichet’s 2011 mistake and hinder an economy already hit by gas prices, tariffs, and Germany’s manufacturing crisis. The market is pricing in 76 basis points of hikes in 2026, which may create opportunities in the short and intermediate parts of the curve.

That said, it is worth remembering that, unlike the Federal Reserve’s dual mandate, the ECB’s sole objective is to keep inflation close to 2%. If oil spikes or stabilizes above $100, the memory of Trichet’s mistake may fade among Governing Council members.

The references from the 2022 episode are clear: equities and cyclical currencies do not bottom out until energy prices peak. In the meantime, the energy sector outperforms the market, defensives outperform cyclicals, and the dollar appreciates against major currencies.

The Strait of Hormuz is also the main transit route for helium and fertilizers, among other commodities that are difficult to substitute in production processes, introducing additional risks to food inflation and the global supply chain. This uncertainty particularly penalizes more open economies, such as those in Europe.

Before the subprime crisis, 79% of S&P 500 earnings came from cyclical sectors. Now, 57% comes from growth industries, making the U.S. index more defensive.

Currency markets: dollar strength and gold to the downside

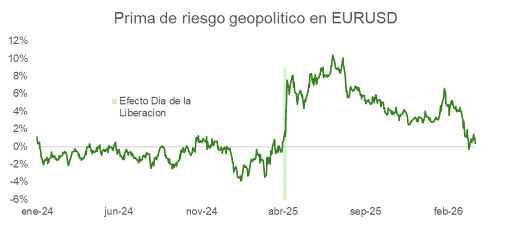

The EUR/USD has corrected since the start of the conflict, confirming that the dollar’s role as a safe-haven asset remains intact despite downgrade concerns. As long as uncertainty persists, the relative strength of the U.S. currency will remain in place. The dollar is also a trending currency, and the breakout above its 200-day moving average provides technical support for this view.

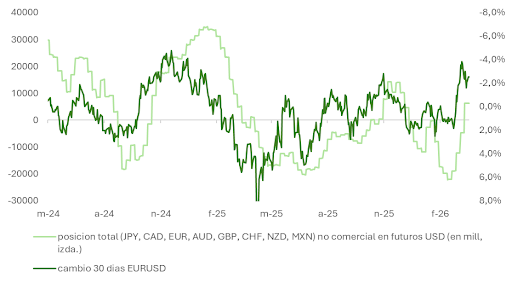

However, the appreciation has fully erased the premium the market had assigned to EUR/USD following the tariff announcements on Liberation Day, although uncertainty around Trump’s trade policy remains high. Long-term models point to a somewhat overvalued dollar, and speculative investors have already closed their short positions on the greenback. Additionally, the market has shifted from expecting fed funds to end 2026 at 3% to seeing them anchored at 3.75%. The announcement of a truce would force a rapid reassessment of these expectations.

Contrary to what might be expected from a safe-haven asset, gold has fallen 14% in the month of March. The strength of the dollar, the sharp rise in real interest rates, and technical overbought conditions explain the move. However, the proximity of a truce (which would entail a reversal of these negative forces), the structural shift toward geopolitical multipolarity, and the procyclical turn toward expansionary fiscal policies maintain gold’s appeal as a diversifying element in multi-asset portfolios.