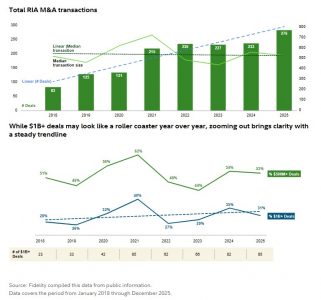

2025 set a new all-time high for M&A activity among RIAs, with 276 completed transactions totaling $796.4 billion in acquired assets. This surpasses the 233 transactions and $669.8 billion in acquired assets recorded in 2024, according to data from the latest report published by Fidelity. “For the first time since we began tracking the market in 2015, acquired assets for the year exceeded three-quarters of a trillion dollars, representing a 19% increase year over year and more than double the total recorded in 2023,” the asset manager highlights.

According to the firm, an analysis of the transactions makes it clear that firm leaders are not growing simply for the sake of growth. Instead, firms are evolving into more sophisticated organizations, as their executives recognize the need to “fish in bigger ponds in order to compete at scale.” “Adjacent acquisitions, such as tax planning, CPA capabilities, and ultra-high-net-worth services, are gaining increasing prominence as firms work to build comprehensive fiduciary platforms. RIAs are shifting from a narrow focus on gathering assets under management to a more strategic view of M&A as a tool to expand and diversify their service models,” the report notes in its conclusions.

Reaching record levels

Since 2020, transaction volume has increased by 111%, while acquired assets have more than quadrupled. According to Fidelity’s report, this momentum is clearly reflected in the activity trend, which mirrors the upward trajectory of U.S. equity markets over the same period. “Despite the increase in overall volume, median deal size has remained notably stable, within a range of $400–600 million. The exception was 2021, when near-zero interest rates drove an accelerated pace of transactions amid strong FOMO (fear of missing out). This stability is reflected in a flat median trend line, with 2025 closing at a median deal size of $508 million,” the document explains.

According to the asset manager, an analysis of transactions exceeding $1.0 billion in acquired assets shows a similar pattern. “While quarterly snapshots may suggest increases or declines in activity around the $1.0 billion threshold, more than a decade of data provides a broader and more reliable perspective. That long-term view makes it clear that the RIA M&A market remains strong and balanced, with steady demand among firms of all sizes, both above and below the $1.0 billion AUM threshold,” they add.

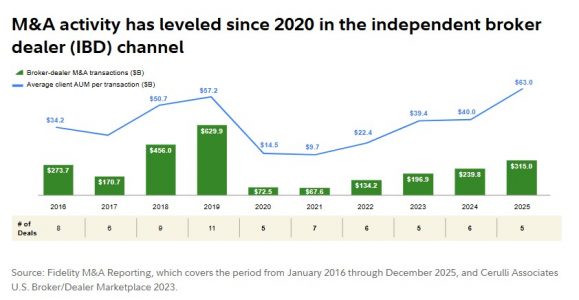

Broker-dealer market

One noteworthy data point is that the broker-dealer sector recorded five M&A transactions totaling $315.0 billion in acquired assets. The report explains that the sector’s more concentrated market structure, stricter capital requirements, and demanding regulatory environment “continue to keep transaction activity relatively contained.”

In light of this data, the report’s authors ask why the broker-dealer M&A market is quieter than that of RIAs. The answer is clear: it is a more concentrated sector, as the number of firms continues to decline. According to FINRA, the 3,378 broker-dealer firms in 2022 decreased to 3,249 in 2024, a 4% drop. Meanwhile, Fidelity’s report recorded 17 broker-dealer acquisitions during that period.

“It is possible that the broker-dealer sector will continue moving toward greater consolidation, as regulatory requirements, technological expectations, and client needs become increasingly difficult for smaller firms to manage on their own,” the report states.