Pixabay CC0 Public Domain. Volatilidad, el elemento olvidado al que hay que volver a costumbrarse

¿Recuerdan cuando los analistas advertían de que los niveles de volatilidad eran extremadamente bajos? Pues bien, la volatilidad ha vuelto. Los dos shocks que ha sufrido el mercado en este primer semestre del año, la crisis sanitaria del coronavirus y las tensiones geopolíticas en torno al petróleo, ha dejado a su paso un importante crash bursátil y una crisis de confianza, pese al esfuerzo de los bancos centrales y gobiernos por enviar señales de calma

“Existen demasiados temores en los mercados y la volatilidad ha llegado para quedarse. En marzo, los mercados de renta variable cayeron con fuerza. Los riesgos a la baja persisten ya que desconocemos la extensión del impacto del virus en el crecimiento. Como tal, probablemente no hemos visto todavía el final del ajuste”, señala Esty Dwek, jefa de estrategia global de mercados de Natixis IM.

En opinión de Dwek, los mercados han intentado considerar los resultados para varios impactos, y el temor es el principal factor. “Como tal, los riesgos a la baja van a persistir por un tiempo. Al mismo tiempo, debido a los movimientos del mercado y otros eventos, esperamos ver más estímulos anunciados, tanto monetarios como fiscales. A medida que lleguen, ayudarán a estabilizar los ánimos, aunque pensamos que el temor y la volatilidad seguirán elevados por un tiempo”, apunta en su análisis sobre la situación actual.

En opinión de la firma ClearBridge Investments, filial de renta variable de Legg Mason, ha sido la “guerra del petróleo” lo que ha acentuado la volatilidad durante el primer trimestre del año. “En el peor de los supuestos, Libia y la OPEP incrementan su producción y la demanda tarda en recuperarse, las reservas alcanzan máximos recientes y ello conlleva drásticos recortes de producción por parte de los productores de esquisto estadounidenses. Y en el mejor de los casos contempla una disipación de las repercusiones del coronavirus, lo que se traduciría en una recuperación de la demanda mundial durante el segundo semestre del año”, explica sobre la situación del petróleo.

Desde Fidelity International recuerdan que la volatilidad es algo normal dentro de la inversión a largo plazo y que, sin embargo, los mercados tienden a reaccionar en exceso ante los acontecimientos que nublan las perspectivas a corto plazo. “Como inversor, es importante tomar distancia en estos momentos y afrontarlos con amplitud de miras. Cuando estamos preparados desde el comienzo para sufrir episodios de volatilidad en la evolución de nuestras inversiones, menos probabilidades tenemos de vernos sorprendidos cuando ocurren y más probabilidades tenemos de reaccionar racionalmente. Con amplitud de miras y una perspectiva de inversión a largo plazo que acepte la volatilidad a corto plazo, los inversores pueden empezar a adoptar una visión más cerebral. Eso no solo contribuye a no perder de vista los objetivos de inversión a largo plazo; también ayuda a los inversores a aprovechar los precios bajos, en lugar de anotarse pérdidas vendiendo a precios bajos movidos por las emociones”, explican de cara a los inversores.

Respecto a los bruscos movimientos de subidas y bajadas que ha sufrido el mercado durante este mes, Simon Aninat, gestor de Seeyond (gestora de Natixis Investment Managers), advierte de la posibilidad de nuevas caídas en los mercados. «Los Gobiernos y los bancos centrales parecen haber tomado la medida del problema del coronavirus, pero es difícil saber si el mercado ha medido correctamente el precio de las consecuencias de un período prolongado de incertidumbre/cuarentena/viajes reducidos, etc. sobre el consumo, las inversiones y los márgenes corporativos. En ese contexto, podríamos ver otro nuevo episodio de caídas en los mercados a medida que tenemos una mejor idea del impacto del virus en la economía global, antes de que la volatilidad pueda normalizarse”, argumenta.

Foto cedidaJuan Alcaraz, CEO de Allfunds.. Allfunds lanza una nueva plataforma de sub-advisory B2B, y amplía sus soluciones de outsourcing de inversión

Allfunds ha anunciado el lanzamiento de una nueva plataforma de sub-advisory B2B, así como nuevas soluciones de outsourcing de inversión para bancos, wealth managers e inversores institucionales. Según explica la firma “se trata de la nueva propuesta en el área de inversiones, tras la incorporación de, Stéphane Corsaletti como CIO en el mes de marzo”.

Esta nueva plataforma, Allfunds Investment Solutions, estará disponible a partir del tercer trimestre del año. La gestora señala que estos nuevos servicios proporcionará a los clientes de Allfunds una “solución única y completa para acceder a la industria de gestión de activos”. Esto les permitirá una mayor flexibilidad en la selección de gestores, más transparencia y mejor monitorización de los datos.

La compañía da respuesta así a las necesidades de sus clientes para optimizar sus programas de arquitectura abierta y externalizar parte de su cadena de valor de inversión, desde la construcción de sus carteras hasta su plena implementación, en el actual contexto normativo y de mercado. Desde la perspectiva de las gestoras, estos nuevos servicios facilitarán aún más la distribución de sus capacidades de gestión de activos.

Stéphane Corsaletti, que se incorporó a Allfunds como CIO el pasado mes de marzo, está trabajando junto al actual equipo de Investment Solutions, en el lanzamiento al mercado de esta revolucionaria oferta. El equipo, que cuenta con más de 30 profesionales con experiencia y presencia internacional, será reforzado con nuevos perfiles que aporten conocimientos en la gestión de estos nuevos servicios.

“En nuestros 20 años de historia siempre hemos buscado aportar valor tanto a distribuidores como a gestoras. En un primer momento, haciendo más eficiente la intermediación de fondos y después con la digitalización de la mayoría de nuestros servicios y productos. Ahora, gracias a la nueva plataforma B2B de mandatos, aportaremos valor a nuestros clientes aumentando la eficiencia y complementando sus programas de arquitectura abierta. Estas nuevas soluciones de inversión maximizarán la rentabilidad de los productos al menor coste posible y ofrecerán a las gestoras nuevos canales y oportunidades de aumentar sus activos bajo gestión”, ha explicado Juan Alcaraz, CEO de Allfunds.

La firma explica que Allfunds Investment Solutions es “la evolución natural del modelo de negocio de la compañía tras la inversión realizada en los últimos años orientada a ofrecer soluciones digitales punteras”. Gracias a esta nueva oferta de servicios, los clientes podrán aprovechar al máximo las herramientas digitales disponibles en Allfunds Connect, principalmente Nextportfolio como sistema de gestión de carteras completo, con contenidos procedentes de Digital Selector.

Este nuevo servicio operará como una unidad de negocio separada y contará con una Sociedad Gestora en Luxemburgo. La oferta inicial de fondos de mandatos se lanzará a través de una SICAV luxemburguesa e incluirá hasta 20 estrategias, gestionadas por las mayores gestoras de fondos del mundo seleccionadas por Allfunds. Los clientes, bancos, wealth managers e inversores institucionales podrán invertir en las estrategias de la SICAV como solución de referencia para sus respectivas necesidades y al mismo tiempo ofrecerá a los gestores de fondos un canal adicional para reunir sus estrategias. Las ofertas alternativas estarán disponibles en 2021.

Pixabay CC0 Public Domain. Los fondos a vencimiento, ¿una oportunidad en el entorno post-COVID?

Muchas empresas se verán perjudicadas por el periodo de confinamiento. Algunas no se recuperarán, otras lo harán más o menos rápido, mientras que otras destacarán como ganadoras en el mundo posterior al COVID-19. A pesar de que los bancos centrales y los gobiernos de todo el mundo están haciendo todo lo posible para proporcionar liquidez suficiente para contener el aumento de los impagos, quiebras y tasas de desempleo, habrá algunas bajas, ya que liquidez no equivale a solvencia.

Esto es exactamente por lo que, en este entorno, es esencial confiar en el análisis de fundamentales del mercado y la capacidad de selección de bonos al invertir en los mercados de crédito. Tikehau Capital ha estado implementando este enfoque de inversión durante muchos años. Así, los gestores de carteras están trabajando en estrecha colaboración con un equipo de 15 analistas que cubren aproximadamente 450 emisores, abordando los antecedentes de crédito individualmente desde un punto de vista ascendente.

En el contexto actual, lo primero es identificar los emisores con una posición de liquidez sólida (en el balance general, a través de facilidades bancarias comprometidas o capacidad para acceder a programas de préstamos gubernamentales) que les permita capear la tormenta. Tras este primer pilar viene el análisis del modelo de negocio: cómo se ve afectado por la crisis sanitaria y cómo le irá en el corto plazo, junto con la sostenibilidad de la estructura de capital (apalancamiento, vencimientos). Así, podemos determinar el grado de apoyo del accionista/sponsor en caso de que la empresa necesite una nueva inyección de liquidez. Finalmente, se debe evaluar cómo le irá después de la crisis, cómo se adaptará y cuánto tiempo tardará a volver a sus niveles anteriores.

Una vez realizada esta evaluación, el equipo de gestión de la cartera aplica su enfoque “value” para seleccionar e invertir en sus mejores opciones y construir una cartera resistente que muestre lo que consideramos un perfil atractivo de retorno/riesgo, tal y como se muestra en el fondo de reciente lanzamiento Tikehau 2027.

Un fondo con un proceso similar y un universo de inversión parecido es el Tikehau 2022. Cuando se lanzó, Tikehau Capital quería traer algo nuevo a la mesa. La idea era destacar tanto en contenido como en estructura cuando se comparase con fondos de vencimiento tradicionales. En primer lugar, se diferencia en estructura al ser un fondo abierto (sin período de suscripción) y sin comisiones de entrada o salida (solo un swing price). En segundo lugar, invierte en el mercado crediticio europeo y mantiene un estilo de gestión muy activo.

El enfoque de inversión activa de Tikehau IM permite optimizar diariamente el perfil de riesgo/rendimiento de cada posición del fondo, asegurando así que los riesgos subyacentes se compensen, además de gestionar de forma eficiente las suscripciones/reembolsos dentro del fondo. Dependiendo del mercado, eso podría evitar una dilución del rendimiento general de la cartera en caso de una suscripción.

Por ejemplo, el fondo ha registrado importantes entradas desde las fuertes ventas experimentadas a finales de febrero/marzo de este año por el mercado, lo que dio al equipo de gestión de la cartera la flexibilidad necesaria para identificar e invertir en créditos resistentes, mostrando un punto de entrada atractivo según nuestro análisis. Las suscripciones en este contexto son beneficiosas tanto para los inversores actuales como para los nuevos, ya que aportan liquidez que permite al equipo de gestión de la cartera aprovechar oportunidades en un mercado donde los precios se dislocaron a niveles extremos, y que no reflejan los fundamentales de mercado.

En un entorno sometido a un alto nivel de estrés como el que vivimos, el enfoque de inversión de Tikehau Capital, basado en un análisis fundamental en profundidad, es primordial para mantener la cabeza fría y beneficiarse de los puntos de entrada que consideramos atractivos.

Tribuna de Laurent Calvet, gestor de renta fija en Tikehau Investment Management y a cargo de los fondos Tikehau 2022 y Tikehau 2027

Foto cedidaJessica Ground, directora global de ESG de Capital Group.. Capital Group ficha y nombra a Jessica Ground para el cargo de directora global de ESG

Capital Group ha anunciado el nombramiento de Jessica Ground como directora global de ESG, puesto al que se incorporará en septiembre y que estará ubicado en Londres. Desde este cargo, será responsable de avanzar en la integración del enfoque ESG de Capital Group en el proceso de inversión global.

Según ha explicado la gestora, trabajará con equipos de los grupos de inversión, distribución, marketing y tecnología para avanzar en materia de criterios ESG. Asimismo, representará a Capital Group como participante activo en organizaciones que fomentan la aplicación de dichos criterios en el sector empresarial.

Jessica Ground tiene más de 20 años de experiencia en el sector, todos ellos en Schroders. Su último cargo en la gestora ha sido el de directora global de Stewardship, responsable de un equipo de analistas de factores ESG y especialistas en gobierno corporativo con la función de integrar los factores ESG en las distintas regiones y clases de activo. Jessica se incorporó a Schroders en 1997 como analista de los sectores financiero y de suministros públicos y trabajó posteriormente como gestora de fondos del equipo británico de renta variable. También preside el Comité de Stewardship de The Investment Association y es miembro del Consejo de Investor Forum.

“En Capital Group, contamos con una larga trayectoria de análisis fundamental y de diálogo activo con las empresas en materia de cuestiones ESG. Nos complace enormemente incorporar a nuestro equipo a alguien con la experiencia y el calibre de Jessica para avanzar en la integración de los factores ESG en Capital Group. Se trata de un área de gran importancia estratégica para nosotros y nuestros clientes, y continuaremos invirtiendo recursos en ella”, ha señalado Rob Lovelace, vicepresidente de Capital Group.

Por su parte, Ground ha declarado: “Estoy encantada de entrar a formar parte de una gestora con un proceso de inversión único y una larga y sólida trayectoria. Los inversores otorgan una importancia cada vez mayor a las cuestiones ESG a la hora de tomar sus decisiones de inversión. Estaré encantada de trabajar con el experimentado equipo de Capital Group para avanzar aún más en la integración de los factores ESG en el proceso de inversión de la gestora y ofrecer servicios que estén en línea con las crecientes expectativas de los clientes”.

Pixabay CC0 Public Domain. ETC Group lanza el primer ETC de bitcoin, que estará disponible en XETRA

ETC Group lista el primer ETC de bitcoin en la bolsa alemana. Se trata del BTCetc Bitcoin Exchange Traded Crypto – (BTCE) y estará disponible a finales de este mes en XETRA, la plataforma electrónica de negociación de la Bolsa Alemana. Además, estará accesible en la plataforma de HANetf, plataforma independiente de inversión en ETFs de Europa.

Según explican desde la firma, se trata de un producto de inversión que permite a los inversores exponerse de forma segura y transparente al bitcoin. Aprobado por la BaFin, el regulador financiero alemán, el producto tiene una estructura similar a los ETC de materias primas que se negocian en la bolsa con un soporte físico como, por ejemplo, el caso del oro. “Toda la estructura del ETC se basa en un proceso transparente y verificable para asegurar que la procedencia del 100% del bitcoin en custodia ha sido estrictamente investigada”, aclaran desde la ETC Group.

La compañía defiende que esta estructura de ETC tiene grandes beneficios para aquellos que quieran invertir de forma directa en bitcoin. Entre estas ventajas señalan que la negociación se realiza en mercado regulados, que los inversores pueden comprar y vender el ETC de la misma forma que lo harían al negociar acciones convencionales o ETPs, contando con las mismas protecciones regulatorias. “La compensación de CCP es una característica que los inversores esperan cuando negocian en una bolsa regulada y BTCE trae este estándar a las inversiones de bitcoin y al comercio de criptodivisas por primera vez. La compensación a través de un CCP reduce en gran medida el riesgo de contraparte cuando se negocia en BTCE”, añaden.

A raíz de esta lanzamiento, Bradley Duke, CEO del ETC Group, ha declarado: «BTCE aporta al mundo del bitcoin la transparencia y la protección al inversor que los reguladores e inversores institucionales requieren. El sector de los criptoactivos se ha visto frenado por las preocupaciones sobre la complejidad, la accesibilidad y la gobernanza. Con el BTCE, estamos transportando al bitcoin al redil de los principales mercados financieros regulados. Los inversores obtienen los beneficios de negociar y poseer bitcoin a través de un valor regulado, mientras que tienen la opción de vender su posición si lo desean. Además de la emisión de la criptodivisa comercializada en el mercado, también estamos muy contentos de asociarnos con HANetf para ayudarnos a democratizar la inversión en criptografía a través de un mayor contenido y educación»

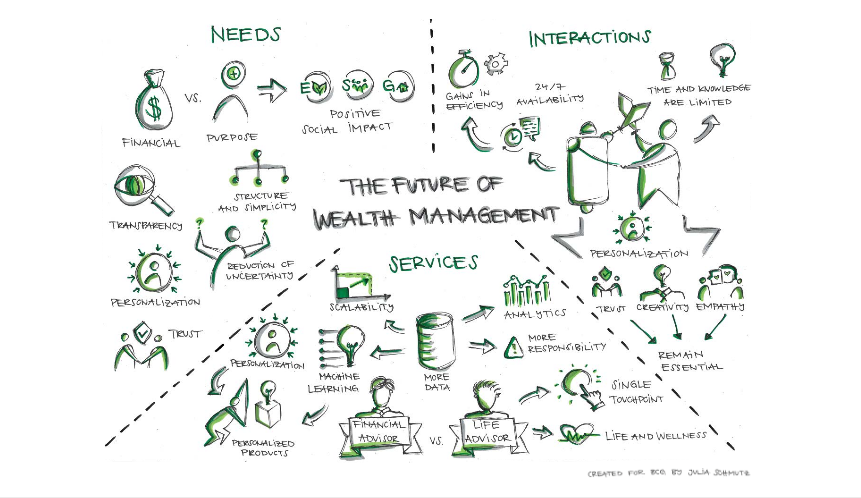

Para el Boston Consulting Group (BCG), «la industria de gestión de patrimonio tiene más de 200 años. Sin embargo, durante la mayor parte de esa historia, los proveedores han operado de acuerdo con el mismo libro de jugadas en general. Tomó la interrupción masiva digital y regulatoria de los últimos 20 años para comenzar a sacudir los modelos comerciales de la industria, y la evidencia sugiere que la mayoría de los proveedores se han movido lentamente, y muchos aún se adhieren a las formas tradicionales de banca privada».

Según un nuevo informe de BCG, titulado Global Wealth 2020: The Future of Wealth Management—A CEO Agenda, los gestores de patrimonio deben tomar medidas en múltiples frentes para navegar por la volatilidad actual del mercado y desarrollar nuevas capacidades que les permitan crear una ventaja competitiva sostenible durante la próxima década y llegar al 2040 con éxito.

Anna Zakrzewski, directora ejecutiva de BCG y coautora del informe, dice: “A medida que la demografía de la riqueza cambie, también lo harán las necesidades y expectativas de los clientes. Con todas las opciones disponibles, los clientes no necesariamente quieren más, quieren algo mejor. Además, las fuerzas disruptivas que surgieron a principios de siglo se están acelerando. Y a medida que la digitalización disminuya las barreras de entrada al negocio de gestión del patrimonio, la competencia se intensificará y las ofertas que una vez proporcionaron la diferenciación enfrentarán la mercantilización”.

Además, en el informe, BCG describe tres escenarios potenciales para el crecimiento posterior a COVID-19: que incluyen un rebote rápido, una recuperación lenta y un daño duradero. «Independientemente del escenario que surja, es probable que los proveedores de administración de patrimonio enfrenten más presión, y muchos de ellos ya estaban en posiciones desafiantes antes del COVID-19. Las necesidades y expectativas de los clientes están cambiando a un ritmo acelerado, la competencia se intensifica y el ratio de costo a ingresos ha sido significativamente más alto que antes de la crisis financiera anterior (77% en 2018 en comparación con 60% en 2007)», mencionan.

BCG cree que los CEOs deben tratar al 2020 como un punto crucial. Su agenda recomendada para los directores ejecutivos de gestión patrimonial presenta tres imperativos clave:

Proteger el resultado final, mediante la mejora inteligente de los ingresos, optimizando la configuración de la oficina principal, optimizando los procesos de cumplimiento y gestión de riesgos, y mejorando la eficiencia estructural.

Ganar al futuro, desarrollando propuestas de valor más personalizadas, mejorando las ofertas de ESG y de inversión de impacto, diseñando juegos retadores y aprovechando los ecosistemas y las fusiones y adquisiciones.

Desarrollar capacidades obteniendo una mejor comprensión del cliente, atrayendo a los mejores talentos, invirtiendo en datos digitales y diseñando una plataforma tecnológica de vanguardia.

«Los últimos veinte años han sido testigos de muchos picos y valles», dijo Anna Zakrzewski de BCG, «y los próximos veinte probablemente traerán lo mismo. Aunque algunas de las iniciativas necesarias pueden no ser nuevas, hay mucho más progreso por hacer. Al actuar con decisión ahora, los gestores de patrimonio tienen la oportunidad de aprovechar su impulso actual y posicionarse de manera óptima para el futuro».

En opinión de BCG, la fusión de la tecnología y las capacidades humanas permitirá niveles de personalización para los clientes que anteriormente habrían sido demasiado costosos, y el modelo de gestión de patrimonio se expandirá y reenfocará durante las próximas dos décadas a medida que la división entre personas y máquinas se desvanezca.

Sin embargo, esto también ejercerá más presión sobre los márgenes. «Además, las generaciones más jóvenes, acostumbradas a la transparencia de los precios en otras partes de sus vidas profesionales y personales, insistirán en una mayor transparencia de los honorarios de sus asesores de patrimonio», dice el informe. “Las herramientas de comparación en línea les facilitarán la búsqueda de las ofertas más competitivas. Juntas, estas presiones podrían reducir los márgenes de los servicios de inversión a la mitad, con el resultado de que los proveedores de gestión de patrimonio tendrán que satisfacer las crecientes demandas de los clientes y encontrar nuevas formas de generar valor con solo una fracción de los recursos actuales».

Para contrarrestar eso, BCG considera que las empresas de gestión de patrimonio deberían cambiar a precios dinámicos basados en el valor, no necesariamente vinculados a los activos bajo gestión.

Por otra parte, BCG dijo que la necesidad de escala, especialización y diversidad de opciones podría hacer que la industria de gestión patrimonial se rehaga en torno a cuatro modelos: Consolidación a gran escala, Jugadas de nicho, Expansión de bancos minoristas y gestión de activos, y la entrada de Big Tech.

Pixabay CC0 Public Domain. Franklin Templeton, Fidelity International y HSBC: líderes en la distribución de fondos transfronterizos a nivel global

Franklin Templeton es la gestora de fondos más relevante en la distribución de fondos transfronterizos. Esta es una de las conclusiones que arroja el informe Annual Global Fund Distribution (GFD), elaborado por PwC, que muestra el crecimiento de los fondos transfronterizos y su distribución en 2019.

Según el informe, las cinco principales gestoras que dominan la distribución de fondos transfronterizos son: Franklin Templeton, Fidelity International, HSBC, BlackRock e Invesco, cuatro de ellas con sedes Estados Unidos y una con sede en el Reino Unido. En concreto, el informe destaca la posición de Franklin Templeton, que está por encima del resto con sus competidores en la distribución de fondos transfronterizos. La gestora distribuye en 10 países más que el siguiente en el ranking, es decir, que Fidelity International.

Observando los primeros puestos de esta clasificación, todas las gestoras tienen en común que buscan países estratégicos en cada una de las regiones, donde además la industria tiene potencial de crecimiento. Como por ejemplo en Chile, Hong Kong, Singapur o Sudáfrica. Otra tendencia clara es que todas las gestoras apuestan por distribuir fondos en Europa, en especial en Reino Unido, Alemania, España, Suiza, Suecia, Noruega, Francia, Irlanda e Italia, lo que coincide con los mercados más maduros del Viejo Continente.

Este documento, que analiza los principales 40 mercados de la industria, refleja el continuo crecimiento de los fondos transfronterizos. A finales de 2019, había registrados 121.458 fondos en todo el mundo, de los cuales 14.031 eran fondos de inversión transfronterizos, lo que supone un crecimiento del 7,02% y del 2,65%, respectivamente, en comparación con el año anterior.

En este sentido, Noruega fue el país en el que se registró el mayor número de nuevos fondos, en concreto 939. Y, en el mercado de oriente medio, los Emiratos Árabes Unidos fue el país donde se realizaron más nuevos registros, mientras que en América fue México el mercado más activo y donde hubo el mayor número de nuevos registros de fondos.

En Asia-Pacífico, uno de los mercados con mayor potencial de crecimiento para la industria, destacó Singapore, donde se registraron 329 nuevos fondos. También el balance es positivo en mercados más maduros como el caso de Europa, donde la mayoría de los países lograron un crecimiento positivo en la distribución de fondos, excepto Estonia, Grecia, Letonia, Lituania y Polonia, que fueron los países con peores resultados.

Entre las conclusiones del informe, se destaca que los ETFs están impulsando la demanda y eso está provocando que crezca el número de fondos transfronterizos. Según los datos del documento, los ETFs transfronterizos crecieron un 7,8% en 2019 respecto al año anterior, lo que supone 4.780 nuevos fondos. En cambio, el número de fondos de inversión transfronterizos solo aumentó un 0,2%, de 9.234 a 9.251 de 2018 a 2019. “Si el mercado alcista de los últimos 10 años ha sido un elemento impulsor clave para los ETFs, el entorno actual podría hacer que los fondos de inversión activos vuelvan a ocupar un lugar destacado”, advierte en sus conclusiones.

Foto cedidaAlison Porter, Graeme Clark y Richard Clode, gestores del fondo Global Technology Leaders en Janus Henderson Investors. Alison Porter, Graeme Clark y Richard Clode, gestores del fondo Global Technology Leaders en Janus Henderson Investors

Alison Porter, Graeme Clark y Richard Clode, gestores de tecnología global de Janus Henderson Investors, ofrecen su visión sobre las últimas restricciones impuestas por Estados Unidos a Huawei y sus consecuencias para los mayores clientes de la compañía y el sector de los semiconductores en general.

Un año después de las primeras restricciones de EE.UU. al gigante tecnológico multinacional chino Huawei y sus filiales, el Departamento de Comercio de EE.UU. anunció el pasado 15 de mayo nuevas medidas que afectan al sector de los semiconductores y tienen consecuencias importantes para los principales proveedores de Huawei, como Taiwan Semiconductor Manufacturing Co. (TSMC), y posiblemente también para la industria tecnológica general y la supremacía de la superpotencia global.

¿Guerra comercial y/o seguridad nacional?

Aunque general los inversores han considerado estas restricciones en el marco de la guerra comercial, en Janus Henderson siempre lo han visto como una cuestión de seguridad nacional. En el comunicado de prensa en el que se anunciaban las nuevas restricciones, el secretario de comercio estadounidense, Wilbur Ross, afirmaba: “Hemos de cambiar nuestras normas que están siendo aprovechadas por Huawei y HiSilicon, e impedir que tecnologías estadounidenses hagan posibles actividades maliciosas contrarias a la seguridad nacional y los intereses políticos extranjeros de Estados Unidos”. Además, en la sesión informativa especial que acompañaba al anuncio de las nuevas restricciones, el subsecretario de crecimiento económico, energía y medioambiente señaló: “Huawei es una compañía con apoyo estatal de la República Popular China que sirve de herramienta al Partido Comunista de China”.

Tras prohibir el uso de equipos de telecomunicaciones de Huawei en Estados Unidos, cuando las intervenciones diplomáticas contundentes resultaron ineficaces para impedir que Huawei fuese incluida en los planes de implantación de la red 5G de los aliados, EE.UU. pasó a una estrategia consistente en eliminar a Huawei de la tecnología y la propiedad intelectual estadounidense. En mayo de 2019, Huawei y sus filiales fueron incluidas en la Lista de entidades de EE.UU. que requieren licencia para cualquier producto cuyo 25% o más de la propiedad intelectual sea de origen estadounidense. Sin embargo, la internalización por parte de Huawei de los componentes en su división interna de semiconductores, HiSilicon, y la elusión por parte de los proveedores de semiconductores globales de la denominada regla de minimis(1) argumentando que no llegaban al umbral del 25% permitieron a Huawei seguir operando con un impacto limitado para el despliegue de sus equipos de telecomunicaciones en China o el resto del mundo. En respuesta a eso y tras la presión ejercida por la US Semiconductor Industry Association (SIA) al alertar del impacto negativo de cualquier restricción general, las nuevas medidas anunciadas parecen directamente específicas para Huawei y sus filiales, enfocadas concretamente en los propios diseños de chips de Huawei y su fabricación, sustituyendo el umbral del 25% de minimis por un nuevo marco directo de concesión de licencias de productos.

Consecuencias para Huawei y TSMC

Con una ventas anuales por un valor de 120.000 millones de dólares, casi 240 millones de smartphones vendidos el año pasado y como mayor compañía de equipos de telecomunicaciones del mundo, Huawei es una de las compañías tecnológicas más grandes e importantes y el mayor comprador de semiconductores del planeta. Tras el impacto de las restricciones de 2019, el efecto directo de estas nuevas restricciones probablemente será más limitado, ya que la mayoría de las compañías de semiconductores globales ya habían reducido considerablemente su exposición a Huawei. Pero hay nuevas áreas bajo amenaza.

TSMC es el mayor fabricante del mundo y Huawei es uno de sus principales clientes, habiendo contribuido de forma importante a la estrategia de internalización de Huawei. Las restricciones de 2019 no afectaron a TSMC, al no llegar al umbral del 25% de la regla de minimis, a consecuencia de lo cual Huawei creció hasta convertirse en uno de los mayores clientes de TSMC. Sin embargo, las nuevas restricciones están pensadas deliberadamente para poner fin a esta laguna. La esperanza de que el compromiso de TSMC por construir una primera fundición de semiconductores en EE.UU. servía para compensar la desescalada se desvaneció con el anuncio de las nuevas restricciones.

Las nuevas normas incluyen también por primera vez los equipos de semiconductores y las herramientas de automatización del diseño electrónico. Un chip diseñado por Huawei o sus filiales no podrá enviarse sin licencia si utiliza software estadounidense para su diseño o equipos estadounidenses para su fabricación. Dado el predominio de EE.UU. en ambos sectores, en la práctica esto supone eliminar la capacidad de diseño de chips de Huawei, puesto que cualquier solicitud de licencia comienza con la presunción de denegación.

Consecuencias también para China

Las nuevas normas entraron en vigor el 15 de mayo y, aunque existe un periodo de gracia para los chips en producción, las fundiciones tienen prohibido aceptar nuevos pedidos de Huawei. Los medios de comunicación informaron de que TSMC ya ha cumplido la norma, a pesar de los intentos declarados de Huawei de solicitar un pedido urgente por valor de 700 millones de dólares. Huawei es uno de los mayores clientes de TSMC, por lo que esta situación tendrá un fuerte impacto en esta última.

Las nuevas restricciones incluyen los equipos de semiconductores en el ámbito de las licencias de EE.UU. y pueden afectar también al gasto en equipos de semiconductores de China, que ha sido muy elevado ante la previsión de nuevas restricciones. La mayor fundición nacional, Semiconductor Manufacturing International Corporation (SMIC), anunció recientemente un fuerte aumento de los planes de gasto en bienes de equipo, hasta los 4.300 millones de dólares, mientras que China Integrated Circuit Industry Investment Fund y Shanghai Integrated Circuit Industry Investment Fund (ambos fondos con respaldo estatal) habían anunciado una inyección de capital de más de 2.000 millones de dólares en la fábrica avanzada de SMIC en Shanghái. Ambos planes parecen ahora bastante inciertos, debido a su fuerte dependencia de los equipos de semiconductores estadounidenses y de Huawei. En caso de desafiar las nuevas normas, tanto TSMC como SMIC correrían el riesgo de ser incluidos en la Lista de entidades de EE.UU. En las carteras de Janus Henderson, llevan un tiempo optando por la prudencia en el sector de los semiconductores y empezamos a reducir su infraponderación a TSMC el año pasado, liquidando la posición a principios de este año; la decisión se debió a la gran exposición de la compañía a los smartphones y las posibles reducciones de pedidos como resultado de las restricciones comerciales impuestas por EE.UU. a Huawei.

¿Qué supone esto para el sector tecnológico global en general?

Estas nuevas normas son muy selectivas y específicas para los diseños de chips de Huawei y sus filiales, por lo que en teoría afectan menos a los semiconductores de otros proveedores. Huawei podría sustituir los chips diseñados internamente de sus smartphones por silicio comercial de otros proveedores, como MediaTek o Samsung. O bien otras marcas de smartphones podrían intervenir y arrancar cuota de mercado a Huawei, ya se trate de Vivo, OPPO y Xiaomi en China o Apple y Samsung a escala mundial.

Por consiguiente, el impacto en los smartphones probablemente será relativamente limitado. En cambio, Huawei tiene entre el 30% y el 40% del total de los ingresos globales del mercado de diferentes equipos de telecomunicaciones inalámbricas y se ha adjudicado casi el 60% de las licitaciones de 5G de China Mobile, lo que implica que el despliegue de la red de 5G depende en gran medida de Huawei. Existe un periodo de gracia de 180 días y Huawei ha acumulado existencias estratégicas. Pero hay alternativas más limitadas para los chips internos de Huawei utilizados en la red que para los smartphones (el foco de las restricciones de EE.UU.), por lo que la disrupción podría ser mucho mayor para el despliegue del 5G en China.

¿Qué va a pasar ahora?

Más allá de los riesgos directos, la principal preocupación será la escalada y la respuesta de China. Las restricciones originales a Huawei provocaron una dura reprimenda por parte de China y la amenaza de una “lista de entidades poco fiables”. Sin embargo, la amenaza no se cumplió y está por ver a quién se incluiría en la lista y qué impacto tendría. Las nuevas normas han suscitado una respuesta similar. Las industrias tecnológicas de EE.UU. y China están cada vez más localizadas, y son pocas las grandes compañías tecnológicas estadounidenses o globales con fuerte exposición a China. Las excepciones evidentes son Apple y Qualcomm. En Janus Henderson siguen siendo conscientes del riesgo de que estas compañías se utilicen como “peones” en este conflicto.

Esta disputa sobre tecnología y seguridad nacional sigue estando muy relacionada con la guerra comercial y ahora con la atribución de culpas por la COVID-19, antes de las elecciones presidenciales estadounidenses. Cualquier desescalada probablemente afecte a los tres factores: la tecnología, la COVID-19 y el comercio. Esto complica una solución, principalmente porque Trump desea enfocar el relato en China antes de las elecciones, dada la debilidad de la economía y las críticas a la gestión de la pandemia, mientras que China podría beneficiarse manteniéndose a la espera para ver quién ocupa la Casa Blanca el año que viene.

Anotaciones:

(1) Regla de minimis: estipula la cantidad de contenido estadounidense en un producto de fabricación en el extranjero, permitiendo a las autoridades públicas de EE.UU. regular la exportación.

Información importante:

Este [documento] está destinado únicamente para ser utilizado por profesionales, definidos como contrapartes elegibles o clientes profesionales, y no está dirigido al público en general. Las llamadas telefónicas pueden ser grabadas para protección mutua, para mejorar el servicio al cliente y para mantener registros con fines regulatorios.

Emitido por Janus Henderson Investors. Janus Henderson Investors es el nombre bajo el cual se proporcionan los productos y servicios de inversión por parte de Janus Capital International Limited (reg. n.º 3594615), Henderson Global Investors Limited (reg. n.º 906355), Henderson Investment Funds Limited (reg. n.º 2678531), AlphaGen Capital Limited (reg. n.º 962757), Henderson Equity Partners Limited (reg. n.º 2606646), (cada uno registrado en Inglaterra y Gales en 201 Bishopsgate, Londres EC2M 3AE y regulado por la Financial Conduct Authority) y Henderson Management S.A. (reg n.º B22848 en 2 Rue de Bitbourg, L-1273, Luxemburgo, y regulado por la Commission de Surveillance du Secteur Financier).

Foto cedidaDesiree Fixler, Group Sustainability Officer de DWS. . DWS nombra a Desiree Fixler para el cargo de Group Sustainability Officer

DWS ha nombrado a Desiree Fixler para el cargo de Group Sustainability Officer (GSO, por sus siglas en inglés), que pasará a ocupar a partir de agosto de 2020. La gestora explica que este puesto, de reciente creación, está diseñado para asegurar la implementación coherente y coordinada de su estrategia ESG en toda la gestora, y que forma parte de su apuesta por la sostenibilidad.

En este sentido, la firma señala que su objetivo es que la estrategia de ESG sea consistente a través de todas las regiones y que esté completamente alineada con sus compromisos tanto como fiduciarios como corporativos. Por ello, entre sus responsabilidad, Fixler coordinará todos los esfuerzos de sostenibilidad de DWS a nivel mundial a través de toda la cadena de valor, vinculándose a todos los equipos que trabajan en temas de sostenibilidad en la gestora.

Fixler trabajará desde la sede de Londres y reportará directamente al CEO de la gestora, Asoka Woehrmann. Se incorpora desde la firma especialista en inversiones alternativas de EE.UU. ZAIS, donde desempeñó como gestora y directora de Impact Investing. A lo largo de su carrera profesional, también ha ocupado cargos directivos en JP Morgan, Deutsche Bank y Merrill Lynch.

Por su parte, la gestora explica que el nombramiento de Fixler complementa los recientes cambios organizativos realizados para intensificar el enfoque en la ejecución de los profesionales clave de la empresa, incluida la sostenibilidad.

«El nombramiento de nuestro GSO es un gran paso para nosotros en la creación de un enfoque holístico para la plataforma ESG en DWS. Estamos encantados de tener a Desiree a bordo para impulsar nuestra estrategia de sostenibilidad. Tiene un fantástico historial en inversiones responsables, así como una valiosa experiencia en los mercados globales y en la innovación de productos. Su capacidad para desarrollar la gestión de riesgos de ESG, las políticas y los marcos de información también la convierten en la candidata perfecta para elevar el estatus de DWS para convertirse en un gestor de activos de ESG líder a nivel mundial», ha señalado Asoka Woehrmann, CEO de DWS.

Por su parte Fixler ha destaca sus entusiasmo por unirse al proyecto de DWS. “Convertirme en GSO también me permite avanzar en un objetivo común que tengo con DWS: incorporar la integración ESG y el impacto de la inversión en toda la cadena de valor de la gestión de activos», ha afirmado.

Pixabay CC0 Public Domain. Los activos netos en UCITS y AIFs cayeron un 11,6% durante el primer trimestre del año

Durante el primer trimestre de 2020, los activos netos en fondos UCITS y AIFs cayeron un 11,6%, hasta los 15,68 billones de euros, según los datos que ha publicado la asociación europea de la gestión de activos (Efama). Solo un tipo de fondo fue capaz de atraer importantes flujos, los fondos alternativos.

Desde Efama explica que la acentuada caída que han vivido los mercados financieros a raíz de la crisis sanitaria del COVID-19 explica el 94% de la pérdida de los activos bajo gestión. En cambio, tan solo un 6% de la caída de los activos bajo gestión corresponde a salidas netas de dinero de los fondos. Un dato que consideran muy significativo, ya que muestra que los inversores no han “huído” de los productos de inversión tras las caídas del mercado.

En este sentido, los activos netos que más cayeron fueron los de los fondos UCITS, un 14,5%, frente a los fondos alternativos, donde la reducción fue de 7,5%. Hablando en términos de flujos, los UCITS y AIFs registraron en conjunto salidas netas por valor de 125.000 millones de euros, un nivel no visto desde la crisis financiera mundial.

En el caso de los UCITS, las salidas de dinero afectó tanto a los fondos de renta fija como de renta variable. Las mayores salidas netas se registraron en Luxemburgo (85.600 millones de euros), seguido de Irlanda (41.200 millones de euros) y Francia (26.000 millones de euros). Mientras que, de nuevo, los fondos monetarios fueron los que menos sufrieron, registrando unas salidas netas de 100 millones de euros. Según matizan desde Efama, el buen comportamiento de los monetarios se debe a “las grandes entradas netas de enero”.

Lo más destacado del primer trimestre ha sido el comportamiento de los fondos alternativos, que experimentaron entradas netas de 51.000 millones de euros. En opinión de Efama, estos datos indican que “algunos inversores institucionales, los principales compradores de fondos alternativos, no dudan en aumentar su asignación a este tipo de fondos cuando el mercado está tensionado”.