Brazilians have increasingly started to invest internationally. In this context, AXA Investment Managers and XP Investments have partnered to bring strategies focusing on technological disruption and sustainable investments. Their collaboration started in 2020 to launch feeder funds in Brazil and today it has grown to exceed 1 billion reals in assets.

“The strategy is at the forefront of where technological innovation and the need for a more sustainable world meet, and it will provide investors in Brazil access to a vast and diverse set of innovative business opportunities that aim to help reduce greenhouse gas emissions from the most polluting and harmful industries”, pointed out AXA IM in a press release.

In this sense, it has identified four key areas that represent the most attractive investment opportunities within the Clean Economy strategy: Low Carbon Transport, Smart Energy, Agriculture & Food and Natural Resources Preservation. “These sectors have the potential for long-term profitability and growth, while making a positive impact on the environment”, they said.

The asset manager believes that its focus on technological disruption was key to bring to Brazil a strategy focusing on companies that allowed our lives to continue during the lockdowns, including companies in fintech, the cloud, remote working, streaming, video games, artificial intelligence, etc. “Investors in Brazil have also become captivated by sustainable and socially responsible investing. We believe we are in front of a multi-decade growth opportunity in areas such as low-carbon transportation, renewable energy, and smart grids. Electric and Hydrogen fuel-cell battery technologies are very exciting. Other areas include Agri-tech, and the development of healthier and organic foods, recycling, and water preservation”, AXA IM commented.

The firm has currently more than $1 trillion in assets under management. Founded in 1997 in Paris, it has grown into a global powerhouse in asset management, with a presence in more than 20 countries and major investment centers in the US, UK, France, and Hong Kong.

Colchester has announced in a press release that its three flagship Irish UCITS funds (Colchester Global Bond Fund, Colchester Global Real Return Bond Fund and Colchester Local Markets Bond Fund) are now being offered to BNY Mellon Pershing’s clients.

The funds will be available to their introducing broker-dealers and registered investment advisors using BNY Mellon Pershing’s NetX360® platform upon the execution of an agreement with Colchester Global Investors’ Fund.

“We’re very pleased with bringing our core strategies to the Latin American and US offshore markets where we have had immense support to make this listing possible. The simplicity of our investment process and the exclusive focus on global sovereign bonds and currencies have resonated with investors in a heavily fixed income biased region”, said Global Head of Marketing and Client Services, Paul Allen.

In his view, their global sovereign bond strategies have experienced strong interest from advisers who are seeking both value and a defensive fixed income alternative for their client portfolios. “With our long track record of displaying negative correlation to risk assets including credit, we are sought out as the anchor in portfolios,” Allen explained.

He revealed that investors have also welcomed their expertise in local currency emerging markets to complement their “aggressive fixed income exposure” through the Colchester Local Markets Bond Fund USD Unhedged Accumulation Class – I Share class (ISIN IE00BQZJ1775), which has received a 5-Star Morningstar RatingTM as of 31/8/20211.

“Nuestro punto de diferencia es que solo invertimos en bonos soberanos físicos en nuestros fondos principales, lo que garantiza la liquidez en todos los mercados y una simplicidad que los clientes pueden comprender. En Colchester, nos enorgullecemos de nuestra alineación con nuestros clientes como inversores a largo plazo en lugar de realizar apuestas a corto plazo “, concluyó Allen.

Los fondos estarán disponibles de inmediato a través de varios acuerdos existentes con corredores de bolsa orientados a la gestión de patrimonios, asesores de inversión registrados (RIA) e instituciones.

Wikimedia CommonsAna Botín, presidenta de Banco Santander durante la celebración de The Global Summit 2015.. Ana Botin

Euromoney has recognized Santander as the world’s best bank for financial inclusion in its “Global Awards for Excellence 2021”, highlighting the group’s efforts to make financial services more accessible.

The magazine has distinguished the company’s efforts to financially empower individuals and entrepreneurs through a range of programs in Latin America, Europe and the US, as well as the work Santander has done more broadly to help people, especially the elderly, adopting digital channels through the pandemic.

“In the last three years we have financially empowered 6 million people, with the goal to empower 10 million by 2025. The impact can be life changing: from supporting entrepreneurs in setting up new businesses through our micro finance programs, to helping individuals who want to build confidence in using digital banking. This is critical to creating inclusive, sustainable growth, and I am delighted that Euromoney has recognized the efforts and innovations of our teams across the world”, said Ana Botín, Santander Group executive chairman.

Different initiatives

In a press release, the bank has informed that its initiative Santander Finance for All seeks to support financial inclusion to help people get access to the financial system, offer them finance to set up and grow micro-businesses, and enhance their resilience through financial education. The strategy “targets the unbanked and underserved”; individuals and SMEs who face difficulties obtaining credit; have limited financial understanding; or are in financial distress.

One of those initiatives is Superdigital, Santander’s flagship 100% digital platform for making payments in Brazil, Mexico, and Chile. It leverages the rapid growth in smartphone adoption and improved network coverage in Latin America to increase financial inclusion in the region. The platform is expanding its services to reach five million active customers by 2023 across seven markets in Latin America.

Besides, Santander has specific microfinance programs to provide financing for micro entrepreneurs. Although named differently (Tuiio in México, Prospera in Brazil, Uruguay and Colombia, and Surgir in Perú), all have same goal: to support microentrepreneurs set up and grow microbusinesses with credit and other products such as microinsurance Thanks to these initiatives, Santander has supported 1.2 million micro-entrepreneurs in Latin America, out of which 70% were women.

The magazine has also recognized that, during the pandemic, the bank has been especially vigilant in supporting elderly or vulnerable customers and ensuring they can access financial services, contacting them proactively to help build confidence in using digital banking services. It also produced simple step-by-step videos and guides for online and mobile banking.

In August, Santander was also recognised as the most innovative bank for its financial inclusion initiatives by The Banker, a Financial Times magazine.

Financial Innovation of the Year

Santander has also won the Financial Innovation of the Year award for its role as joint lead manager advising European Investment Bank in the first-ever digital bond on a public blockchain multi-leader led. It was a 100 million euros and 2-year maturity bond, placed with key market institutional investors.

The transaction used Ethereum, a public blockchain protocol, and it was a milestone for Santander’s CIB Digital Solutions Group (DSG). Santander CIB created the unit at the beginning of 2021 to partner with global coverage and product teams to provide comprehensive support in the digital acceleration of customer’s business. It also produces added-value digital products and financing structures to help Santander’s clients in the digital acceleration of their business.

Euromoney magazine has been a leading publication in international finance for 50 years. Its Awards for Excellence were established in 1992 and are the global benchmark for the banking industry.

Pixabay CC0 Public Domain. Las finanzas se mantienen como una de las opciones profesionales preferidas entre los jóvenes

CFA Institute, the global association of investment professionals, has recently released the results from a survey it conducted on the career outlook of more than 15,000 current university students and recent graduates aged 18-25 from 15 markets. Globally, 58% of respondents still feel confident about their future career prospects in the wake of the COVID-19 pandemic.

“Traditionally stable fields, such as finance, remain attractive for graduates navigating these uncertain times”, the report points out. In fact, respondents across all 15 markets ranked this sector as one of the top five most valuable majors for finding a career. Overall, graduates felt that medicine/science was most stable and attractive, followed by healthcare and then education.

“Students and recent graduates are more flexible and confident about their prospects than ever. The pandemic forced many grads to reassess their expected career paths, and they have displayed remarkable resilience despite the circumstances. It is now incumbent on companies to adapt to the new realities, such as hybrid workplaces, in order to attract and retain the young talent we need to help lead us out of the pandemic”, said Margaret Franklin, CFA, President and CEO at CFA Institute.

She finds “encouraging” to see that many graduates still view finance as a stable and attractive career path; however, they currently don’t see the industry as making a positive social impact. “This issue is only going to increase in importance, and industry leaders need to make sure we are on the front foot in educating students about the positive impact an investment career can have for people and our planet,” Franklin concluded.

The survey shows that a majority of graduates believe their future career will be as good or better than their parents’ generation, despite the pandemic. Findings showed that those studying accounting and finance were particularly confident, with 80% believing their prospects are as good or better than their parents’ generation, compared to three quarters (75%) of respondents overall.

Skills and insecurities

Another primary concern for students is developing work-related skills during degree programs and after graduating. Those surveyed shared personal insecurities about this, with a quarter of respondents saying they feel underqualified for the job they want, and 22% saying they do not feel ready for the working world.

When approaching the current complex job market, students and graduates see value in further education. Nearly nine in 10 respondents feel that upskilling and post-graduate qualifications are important in the current job market, and 57% believe postgraduate qualifications/professional certification will give them an edge when looking for a job.

Working in an industry that makes a positive societal and environmental contribution ranks very important to recent graduates, with nearly nine in 10 respondents saying it’s an important part of their career choice. For CFA Institute, of concern is that only 8% of respondents consider a career in investment management as one in which they could make a positive environmental and societal impact. This finding shows that, to retain talent, the sector must do more to educate students around the positive impact they could have in an investment industry career.

“Graduates may be unaware of the remarkable global trend towards environmental, social and governance (ESG) investing and the career opportunities a specialism in sustainability and ESG could offer them in the investment industry. We need to show them that investment careers can be rewarding well beyond the traditional attraction of higher salaries,” commented Peter Watkins, who leads the University Affiliation Program at CFA Institute in Europe, Middle East and Africa.

Foto cedida. Aegon AM amplía su equipo de Inversión Responsable con tres nuevos especialistas

Aegon Asset Management has announced that Andy Woods, Curtis Zappala and Jamie McAloon will be joining its Responsible Investment team, bringing the number of specialists in this division to 17.

Based in the UK, Andy Woods arrives as a responsible investment manager, supporting the Equities and Multi-Asset investment platforms. His primary responsibility will be the voting activities and related engagements with companies within Aegon AM’s portfolios. Previously, he headed up the Institutional Voting Information Service of the Association of British Insurers.

The firm has also appointed Curtis Zappala as a responsible investment associate. Based in the United States, his focus will be on ESG integration and engagement, supporting the fixed income investment platform. Prior to his new role, Zappala was a member of the sustainability team at United Parcel Service (UPS). He has also held various sustainable-related positions at SunShare and Growth International Volunteer Excursions.

Finally, Jamie McAloon joins as a responsible investment associate, supporting the Equities and Multi-Asset investment platforms. Also based in UK, McAloon will be primarily responsible for supporting the sustainable range of products with analysis of existing and potential holdings, according to Aegon AM’s sustainability research framework. He joins the business from Abrdn, where he was a Private Equity Finance Analyst.

“We have built a comprehensive responsible investment approach, with a 30-year history of investing in this area. The three new appointments allow us to continue our work, broadening our expertise, knowledge and skills base. I’d like to welcome Curtis, Andy and Jamie to the team and look forward to the fresh perspective and enthusiasm they will bring”, commented, Brunno Maradei, head of responsible investment at Aegon AM.

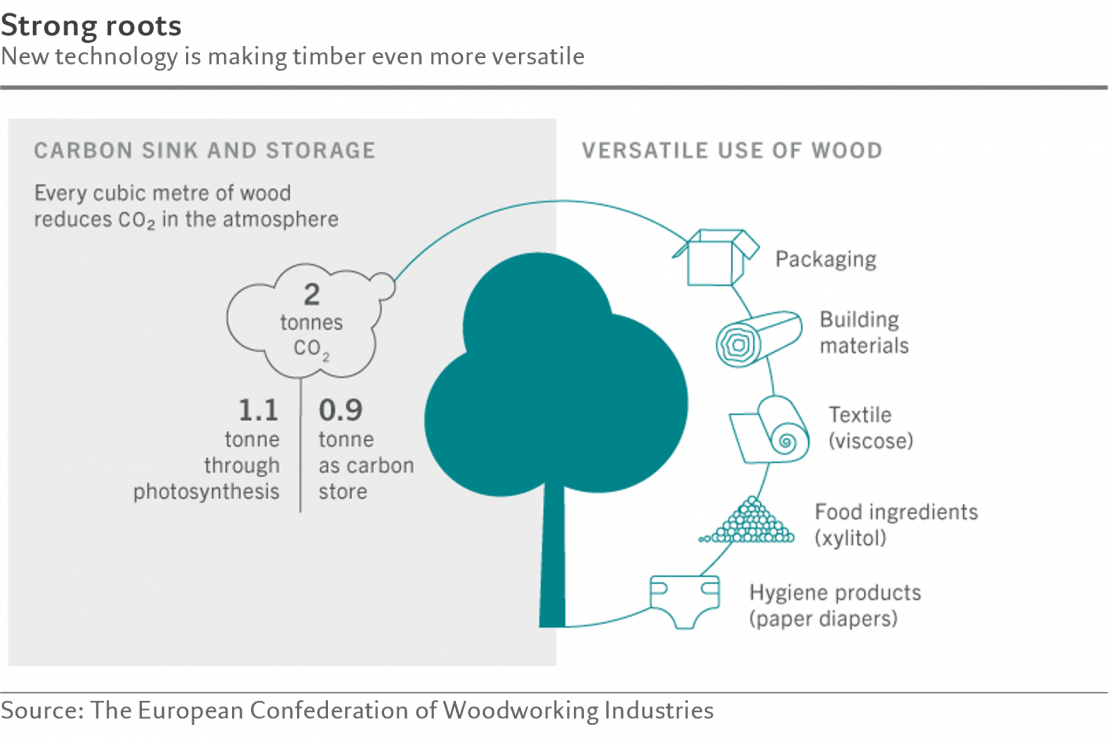

Every day, the world’s urban population swells by 200,000. At that rate, more than two thirds of us will be living in cities by 2050 compared with just over half today1.

That will require a significant expansion of the built environment. It could also mean a significant enlargement of humans’ carbon footprint. Cities already account for around three quarters of global carbon emissions and energy use2. This means using popular construction techniques and planning methods would likely derail efforts to halt climate change.

But it need not be this way. Participants attending The Klosters Forum showcased the ways in which the looming urban expansion could yet be sustainable. Not all the solutions were technologically advanced. The most effective, attendees discussed, literally grows on trees.

Timber has strong credentials as a sustainable building material. Historically, timber has been used in building construction for centuries across Asia, Europe and Americas thanks to its durable and resilient properties and relative ease of construction.

In recent decades however, the material’s share in building has shrunk in the face of concrete and steel which are considered more durable, rot resistant and easy to mass produce.

Wood for good

In a workshop on “how to scale timber buildings that regenerate sustainable forestry and local economies,” The Klosters Forum participants stressed the need to readopt this earliest method of construction en masse, especially if the world were to halt global warming and environmental degradation.

Timber provides an attractive cost-effective means to reduce net carbon emissions, especially the embodied carbon that the building sector badly needs0 to cut.

What’s more, it also acts as carbon sink, can restore biodiversity and improve soil quality.

There’s no shortage of data to support timber’s utility. For example, research shows a young willow tree building up a dry biomass of 75kg in the first five years of growth captures 140kg of CO2,3 which compensates the emission from a typical household’s electricity use for 10 days.4

Wood sequesters carbon even after it is logged. Every cubic metre of wood used as a substitute for steel or aluminium reduces carbon emissions to the atmosphere by an average of 0.9 tonnes.5 Proper forest management ensures timber is sourced sustainably without depleting forests.

Busting the myths

The key challenge, forum participants agreed, lay in formulating strategies that could incentivise the construction of timber-based buildings and regenerate sustainable forestry and local economies.

One of the myths surrounding timber is that it is not fit for tall buildings. However, mass timber is beginning to be used more widely for high-rise buildings, thanks to innovation.

Among the pioneering engineered wood products is cross-laminated timber (CLT) – a building panel made of sawn, glued and layered wood which allows architects to build wooden skyscrapers.

Mjøstårnet, currently the world’s tallest timber building in Norway, which rises to more than 85-metre high, uses CLT. A 100-metre-tall timber residential block is currently planned in Switzerland for completion in 2026.

The market for CLT is expected to grow to a USD2.5 billion globally by 2027 from the current USD1.1 billion, an annual increase of some 15 per cent6.

Another misconception is that timber-based buildings pose a fire hazard. However, wood is inherently fire resistant – when the external layers of a timber beam char, they protect the core from damage for longer periods. What is more, new technologies such as CLT can produce a stronger and fire-resistant weave which can outperform unprotected steel structures in fire safety.

Built by Nature, an Amsterdam-based organisation dedicated to showcasing ground-breaking projects, has been making multi-million euro grants to foster mass timber construction in cities.

“There are a lot of myths about mass timber – whether it’s inflammable or contributes to deforestation for example. There are a lot of research that speak the contrary and it’s important to distribute them and dispel these myths,” its CEO Amanda Sturgeon, a participant, said.

Forum attendees discussed the lack of technical knowledge in the public sector and municipal authorities. To overcome this challenge, forum attendees suggested that the industry should train sustainability facilitators to engage with this tough group of stakeholders.

They added that regulation and tax schemes should also change to reward environmental performance of buildings to induce system-wide change.

Encouragingly, some European governments are pledging a greater use of timber and other sustainable materials to meet national or municipal net zero targets. The city of Amsterdam is mandating that 20 per cent of all new construction projects to use wood or other biobased materials from 2025.

The French government is requiring all new public buildings to be made at least 50 per cent from wood or other sustainable materials from this year.

Typically, residential buildings in Europe use around 20 per cent of timber; this number drops to just 5 per cent for commercial counterparts7.

“Policies and mandates have to come into play to move the sector at speed we need,” Sturgeon said.

Notes

[1] UN World Urbanisation Prospects

[2] Seto et al. 2014; UN-Habitat, 2011

[3] Zuercher, Bern University

[4] US EPA

[5] European Confederation of Woodworking Industries

[6] Markets and Markets

[7] Tomorrow’s Timber

The Klosters Forum is a not-for-profit organisation, offering a neutral platform for disruptive and inspirational minds to tackle some of the world’s most pressing environmental challenges. Its mission is to accelerate positive environmental change by developing and nurturing a growing community of leading thinkers and doers and by fostering cross-disciplinary exchange and collaborations.

Every year, the Forum hosts an environmental annual event connecting high-profile participants from the fields of science, business, politics and industry, as well as NGOs, creative minds and sustainability experts in a neutral and discreet environment. This year, the annual forum took place on 28-30 June 2022 with the theme “The future of the built environment.”

Foto cedidaDe izquierda a derecha: Honor Solomon, nueva responsable del Canal Minorista de EMEA de AB, y Mike Thompson, recién nombrado responsable Global de Desarrollo de Negocio y Estrategia de Renta Fija.. AllianceBernstein refuerza su equipo para EMEA fichando a Honor Solomon y Mike Thompson

AllianceBernstein (AB) has strengthened its EMEA product and client leadership with the appointment of two high-profile industry figures in London. In a press release, the firm revealed that Honor Solomon will join the firm as Head of Retail EMEA and Mike Thompson will lead AB’s global Fixed Income business development strategy.

In her role, Solomon will oversee strategy, management and distribution for AB’s fast-growing EMEA retail business, and will be charged with building on the considerable growth of the retail offering across the region in the last two years. In this sense, the firm has seen the AUM in its EMEA retail business increase by 47% since the start of 2019 – including strong momentum and inflows into its UK-based OEIC range since its launch in March of last year. She will join the firm in Q1 2022, and will report to Onur Erzan, Head of Global Client Group.

Solomon joins from Legal & General Investment Management (LGIM), where she spent seven years as Head of Retail Distribution, helping to build the firm’s retail offering into one of the UK’s largest. Prior to this, she led BlackRock’s London Discretionary Team, with responsibility for the firm’s relationships with banks and intermediaries. She began her career with Merrill Lynch, where she spent four years in its investment banking division across Paris, New York and London

Meanwhile, Thompson will assume the role of Global Head of Fixed Income Business Development & Strategy, and will be responsible for driving growth and brand-building efforts for AB’s high-performing fixed income range worldwide. He joins from ICG, a leading UK-based alternative asset manager, where he was global head of the Financial Institutions Group and European Head of Marketing and Client Relations.

Prior to ICG, Thompson had a 15-year career at PIMCO, where he was head of Asia ex-Japan and previously head of third-party distribution in Europe. His prior experience also includes large fixed-income managers Western Asset Management and Franklin Templeton. Thompson will join AB in December.

“Bringing Honor and Mike aboard is a clear signal of the ambitions we have for both our EMEA business and our global fixed income franchise, and our intent to capitalize on the growth we have seen in both over the last few years”, said Onur Erzan.

In his view, to be able to attract talent “of their calibre” is confirmation of AB’s status as a brand of choice for both clients and leading industry talent. “We are delighted to welcome them both to the firm, and we are confident that they will help to lift our retail and fixed income franchises to new levels”, he concluded.

The first signs of a moderation in global economic growth are on the horizon. According to the latest market report by BLI – Banque de Luxembourg Investments, the moderation in activity seems to be more the result of the ongoing disruptions in supply chains than any major weakening of demand.

“Although most activity indicators are holding up, they appear to be starting to drop back from the very high levels of previous months. In the United States, for example, the manufacturing activity index fell for the second consecutive month after 15 months in a row of almost uninterrupted growth”, points out Guy Wagner, Chief Investment Officer and managing director of the asset management company. Besides, in services, the activity index was also down slightly due to the rise in coronavirus infections, although, in his view, “this should prove temporary.”

The “Highlights” report shows that trends appear similar in Europe, with activity remaining robust but possibly at a turning point.

Moderation in China continues

In China, the pace of growth has continued to moderate in recent months. According to BLI, this is due to the simultaneous effect of strict restrictions to curb the epidemic, tighter regulatory measures in almost all economic sectors, a shortage of electricity, and the financial difficulties of China Evergrande, the country’s second biggest property developer. In Japan, exports continue to be the most dynamic segment, as yet showing no signs of weakening.

Upcoming reduction in asset purchases

The FOMC (the Federal Reserve’s monetary policy committee) left its monetary policy unchanged at its September meeting. Nevertheless, Fed Chair Jerome Powell signaled that it would start tapering asset purchases, from the next meeting in November through to mid-2022. The report reminds that when it comes to the future level of interest rates, Powell reiterated that the end of asset purchases did not mean a simultaneous rise. “Opinion in the FOMC seems to be divided on this subject since half its members are expecting a first interest rate hike in 2022″, it adds.

In Europe, in view of the economic improvement and the surge in prices, the ECB announced a slight readjustment of asset purchases under the pandemic emergency purchase program to a level slightly below that of the previous two quarters. At the December meeting, the monetary authorities expect to give more details on the monetary policy outlook for 2022.

More volatility in equity markets

Lastly, BLI highlights that having risen almost every month since the beginning of the year, equity markets were more volatile in September. “Uncertainty surrounding the financial difficulties of property developer China Evergrande and the rise in long-term interest rates weighed on share prices. In consequence, the major indexes in the United States, Europe, and the MSCI Emerging Markets recorded losses“, says Wagner.

Meanwhile, the Topix in Japan was alone in rising, partially making up for the accumulated lag of previous months. “In terms of sectors, energy stocks stood out with a sharp increase in their share price on the back of rising oil and gas prices”, concludes the Luxembourgish economist.

The global economic outlook is darkening again as tighter monetary policy around the world and surging energy prices continue to undermine consumer confidence and corporate earnings growth.

Major economies are flirting with a recession. Europe is feeling the chill more than most other regions as the soaring cost of living and energy shortages force consumers to tighten their belts, banks to slow lending and companies to delay capital spending plans.

All of thisaugurs badly for corporate earnings in the coming months.

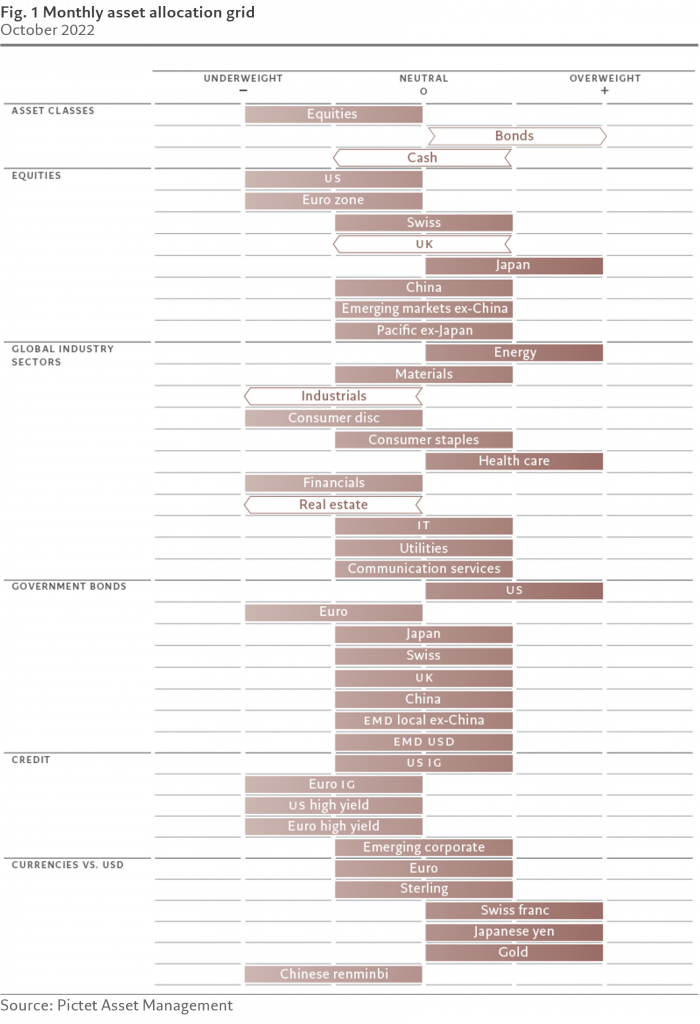

While the equity market sell-off this year has driven investor risk appetite to record lows – a point where stocks and other risky asset classes tend to stage a rebound – we see risks of a further correction. This is why we maintain our underweight position in equities.

We’re unlikely to change this stance until we see stabilisation in corporate earnings revisions, a steeper yield curve and a further cheapening of cyclical stocks.

By comparison, some areas of the bond market are beginning to look attractive, however, as yields are climbing to levels that are increasingly at odds with economic fundamentals. Headline inflation has likely peaked in the US, with inflation expectations also having slipped in recent months. The New York Federal Reserve’s monthly survey shows that consumers in August saw inflation at 5.75 per cent over the next 12 months, the lowest since October 2021. Against this backdrop, we upgrade bonds to overweight, with a preference for US Treasuries – a haven in times of turbulence. We also cut cash to neutral.

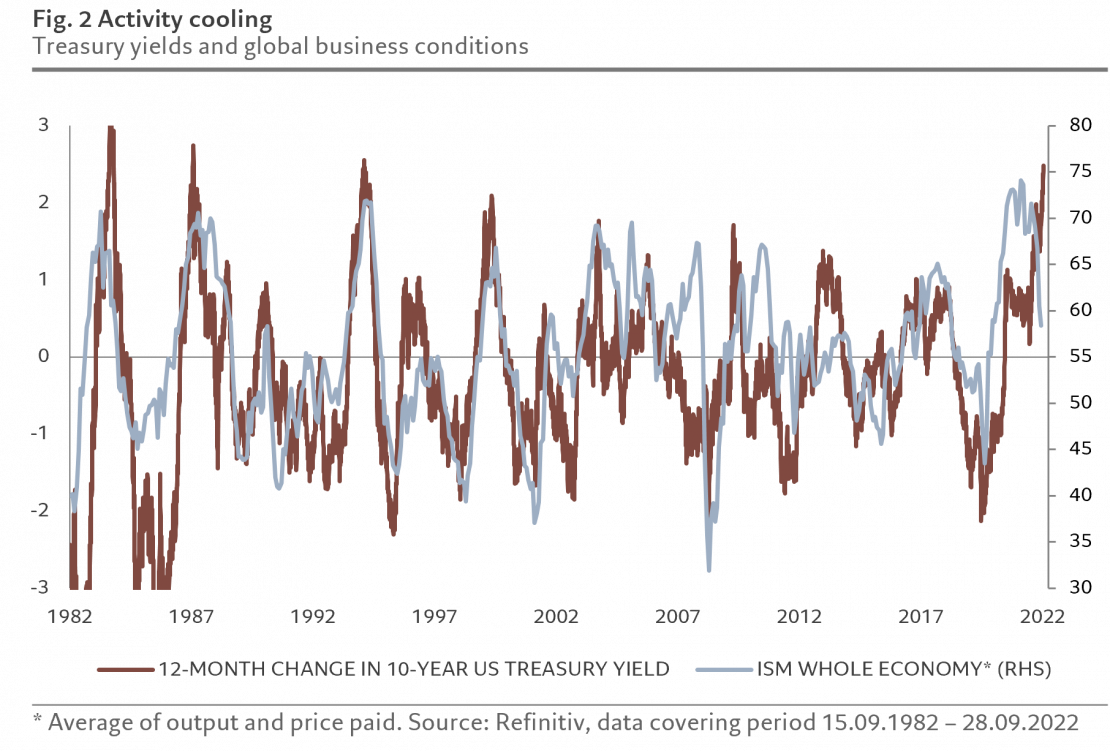

Our business cycle indicators show a clear slowdown in global economic growth. As Fig. 2 shows, rising borrowing costs tend to exact a heavy toll on global business conditions.

The outlook has deteriorated in the euro zone in particular, where consumer confidence has plunged to an all-time low and energy rationing poses further risk to industrial sectors. With the euro zone economy expected to contract towards the end of this year, we have cut our 2023 real GDP forecast to 0.2 per cent from 1 per cent.

The growth outlook is also weak in the US, although there are some positive signs that testify to the resilience of the world’s largest economy. The US labour market remains tight with jobless claims now trending down. Consumer confidence, meanwhile, has improved for the second consecutive month thanks to easing inflation worries.

That said, surveys also show companies remain reluctant to boost their capital spending while the housing market is confronting a slump in construction activity, pointing to a further 10 per cent decline in property prices over the next six months.

What’s more, typical mortgage payments as a proportion of income stand at their highest levels since the 1980s.

We’re becoming cautious on Japan’s economy whose leading indicators have slowed down. Manufacturing activity is contracting and weak global demand is pressuring the export sector.

The prospects for the UK economy remain weak, too.

The government’s plans to deliver the biggest tax cut since 1972 and ramp up borrowing at a time when the country’s consumer price index hovers close to a 40-year high has led investors to question the country’s fiscal credibility, giving rise to a sharp sell-off in sterling and gilts.

Consumer confidence stands at an all-time low with inflation-adjusted wages expected to contract 5 per cent. We expect the UK economy to fall into recession from the fourth quarter of this year with full-year growth to be at zero next year.

Our liquidity indicators show tighter conditions in major economies, especially in the US and UK, as central banks continue to reverse pandemic-era monetary stimulus.

At the same time, bank credit, which has until recently partially offset the effect of central bank tightening, is finally slowing down, in line with leading indications from credit standards.

China is the only country showing easier liquidity. The People’s Bank of China is lowering funding costs and offering targeted easing measures to revive credit demand.

Our valuation model backs up our positive stance on bonds.

Global bond yields are now at the highest since mid-2011 following a recent sell-off.

Equities are on the verge of becoming cheap for the first time since April 2020 after a 9-per cent decline in world stocks in September alone – which was driven entirely by a contraction in earnings multiples.

As a result, the global 12-month price earnings ratio has fallen to 13 times, below the low seen in June.

What is more, the pace of contraction is consistent with a sell-off typically seen during a recession.

Our models suggest a rebound in multiples of 5-10 per cent over the next 12 months, assuming that 10-year yield on US Treasury Inflation Protected Securities (TIPS) falls to 0.75 per cent.

Our 2022 global earnings growth forecast, meanwhile, stands at 2 per cent, significantly below market consensus.

Within equities, we’re becoming more cautious on cyclical sectorsthat are growth-sensitive, such as industrials and real estate.

Our technical indicators show investor risk appetite close to record low levels, with equity funds losing USD25 billion in flows in the past four weeks.

While a technical rebound cannot be ruled out at this depressed sentiment level, our negative trend score suggests taking an underweight equity position over our investment horizon.

Opinion written by Luca Paolini, Pictet Asset Management’s Chief Strategist

La séptima edición del Investments Summit & Golf de Funds Society volverá a reunir a gestores de activos de todo el mundo que compartirán ideas de inversión y estrategias este jueves 14 de octubre.

Además, en el evento, que tendrá cita en el Ritz Carlton Golf Resort de Naples, se disputará un torneo de golf el viernes 15 en el Tiburon Golf Club.

Dentro de los temas que propondrán las gestoras se encuentran los mercados emergentes. En este sentido, John M. Malloy Jr de RWC quien presentará la oferta de la compañía “Emerging and Frontier Markets”.

Janus Henderson también profundizará sobre los emergentes con Daniel J. Graña, CFA, portfolio manager de Mercados Emergentes que estará acompañado por Matthew Culley, assistant portfolio manager.

M&G Investments discutirá los beneficios, las valoraciones de mercado y las oportunidades de los High Yields a tasa flotante con James Tomlins, manager de M&G (Lux) Global Floating Rate High Yield Fund, quien hablará sobre las oportunidades que el alto rendimiento puede ofrecer en un escenario de presiones reflacionarias.

Por otro lado, Thornburg intervendrá con una conferencia sobre inversión en bonos en un entorno de bajo rendimiento a cargo del administrador de la cartera de clientes, Robert Costello, CFA. El técnico hablará tanto del Thornburg Limited Term como del Thornburg Strategic Income en su presentación “Bond Investing in a Low Yield Environment”.

Vontobel, en cambio, centrará su disertación en la importancia de los activos de calidad a la hora de buscar inversiones. Bajo el lema “Quality or Nothing”, Ben Falcone, CFA, Head of Client Portfolio Manager Team Quality Growth Boutique, hará su presentación demostrando la importancia de esta característica al momento de colocar inversiones.

Alec Murray, Senior Vice President Head de Equity Client Portfolio Managers en Amundi, hará su presentación sobre management. El experto dirige un equipo de portfolio managers de clientes que son responsables de representar la filosofía de inversión, el proceso y el desempeño de las estrategias de renta variable de la empresa, y proporcionar actualizaciones sobre las tendencias del mercado financiero y las perspectivas económicas de la empresa a los clientes y sus asesores.

Finalmente también se hablará del futuro. En ese sentido George Saffaye, Managing Director de Global Investment Strategist en BNY Mellon presentará “Mobility Innovation for the future”. En su rol, Saffaye guía el mensaje y el posicionamiento de las estrategias de inversión. Es una interfaz crítica entre el personal de cara al cliente y los equipos de inversión, según la información de la firma.

Por último, Manulife Investment Management también hablará acerca de los desafíos para las nuevas generaciones. Clinton Graham, Vice President and Portfolio Advisor of Wellington Management, hablará sobre su estudio “Next Generation Themes”. La presentación se dividirá en cuatro partes bien definidas: el caso de los temas a largo plazo, la oportunidad FinTech, la inversión temática en atención médica y, finalmente, la evolución de datos 5G.

Si desea obtener más información del evento puede acceder a través del siguiente enlace.