Christopher Shea joins Balanz USA after 16 years at Citi to establish Shea Wealth Advisory.

The 25-year industry veteran, who also previously worked at Morgan Stanley, has decided to leave the large financial firms to focus on delivering clients a more robust product offering and unparalleled client experience, which the large institutions have abandoned.

As stated by Claudio Porcel, Balanz Group President, “there is a drive towards independence, advisors are looking for a culture that is both client and advisor friendly, Balanz aims to provide this culture”. With this, Chris will continue to service high-net-worth clients globally and expand his practice, from Balanz’s new Coral Gables, Miami office.

As one of Citi’s most successful advisors, Chris has spent his entire career developing a substantial wealth management business that encompasses a global footprint that aligns perfectly with our strategy and growth trajectory, said Balanz USA CEO Richard Ganter.

Shea will continue to deliver guidance and advice to his clients, and now, with the resources of the Balanz global brand and independence-driven culture, he will undoubtedly grow his practice to the next level. Is a significant hire for our firm and creates what we consider to be an enormous opportunity for him and his clients, added Ganter.

In the same sense, Balanz USA Managing Director Fred Lucier said, “with his knowledge and expertise, Shea will be an important catalyst for our future growth”.

A graduate of Florida International University’s College of Business, and a recent Barron’s Top advisor, He focuses on comprehensive wealth management for ultra-high-net-worth families and individuals.

“With Balanz’s open architecture platform and superior technology stack I can be far more proactive with clients, provide best in class solutions, and will have access to unique intellectual capital”, said Shea.

Diego Daza will be joining together with Shea, and he will be his second-hand in the process of establishing his wealth advisory practice in Balanz USA. Daza is a highly experienced and accomplished portfolio registered associate, with a proven track record in esteemed financial institutions, including JP Morgan Chase and Citibank.

With 12 years of combined experience, including the last 7 years at Citibank, Daza has established himself as a specialist in servicing high-net-worth clients, the release added.

“His extensive experience and comprehensive knowledge of the industry have enabled him to understand and cater to the unique needs of affluent individuals. Diego’s expertise led him to become a valued member of Citibank’s top producer’s team as a Registered Service Associate, where he efficiently helped manage a book of over $250MM (AUM) in assets”, the firm said.

In addition to his vast industry experience, Daza holds a B.B.A from Towson University.

Shea’s hire is the first of many to come and sets the tone for Balanz USA moving forward: the firm will continue to hire top-tier financial advisors, offering them sophisticated wealth management services and independence, with the goal of helping these advisors grow their practice and give their clients best-in-class plans, strategies, and solutions to achieve their financial goals.

Safra New York Corporation, the holding company of Safra National Bank of New York (“The Bank”), announced the successful completion of its acquisition of Delta North Bankcorp, including its subsidiary Delta National Bank and Trust Company.

This strategic acquisition is a significant milestone for Safra National Bank and underscores the Bank’s continuous expansion in the private banking and wealth management business.

The acquisition strengthens the Bank’s market position among high-net-worth clients in the United States and Latin America, where the Bank has been providing premier private banking and financial services and has a long and successful track record.

Jacob J. Safra, Chairman of Safra National Bank of New York: “We are proud to have completed this acquisition, which represents an excellent strategic fit to our existing business in these markets. Clients will benefit from an organization that is fully dedicated to wealth management, providing the service, products and expertise that best meet their specific needs. We are confident that the Bank has all the attributes required to continue growing and prospering in a sustainable manner.

Simoni Morato, Chief Executive Officer of Safra National Bank of New York: “We very much look forward to working closely with Delta’s clients and employees and developing long term relationships. Together we will build on the strengths of our organization, not only in the United States, but also throughout Latin America.”

Headquartered in New York, with branches in Aventura, Miami and Palm Beach, and offices throughout Latin America, Safra National Bank is a leading private bank with approximately US$ 30 billion in clients’ assets. Safra National Bank of New York is part of the J. Safra Group.

BroadSpan Capital has announced that Mark Rosen has joined the firm as a Senior Advisor and Vice Chairman of the firm’s Advisory Board.

Rosen brings over 30 years of experience in international financial markets including the role of US Executive Director at the International Monetary Fund, a position he held until January 2021.

Prior to his time at the IMF, Rosen held various senior positions in the investment banking industry, including Chairman and CEO of the Latin American Investment Banking Division of Bank of America Merrill Lynch, holding the Chairman position at BAML until August 2018.

BroadSpan CEO Mike Gerrard commented: “We are delighted to have the opportunity to work with Mark. His experience at the IMF is a great asset for our sovereign restructuring group and his deep transaction knowledge will complement our M&A advisory efforts across the region”.

Rosen added: “The BroadSpan team has built a very impressive restructuring and M&A advisory platform. I am delighted to join and help expand the business in Latin America, as well as in other emerging markets around the world”.

About BroadSpan

BroadSpan Capital, founded in 2001, is an independent investment banking firm that provides corporations, partnerships and government institutions with impartial advice related to mergers & acquisitions and financial restructuring in Latin America and the Caribbean. BroadSpan delivers solutions to clients from its offices in Miami, Rio de Janeiro, São Paulo, Mexico City and Medellín and through affiliate offices located in 30 countries around the world.

U.S. stocks were lower in August as the S&P 500 and Nasdaq suffered their first monthly declines since February. One notable challenge that stocks grappled with in August was rates rising again, despite the prevailing narrative of broader disinflation. However, even with this month’s declines, equities are having a great year, with the Nasdaq attaining its best first 8 months to start a year since 2003.

The “Magnificent Seven” mega-cap tech stocks remain at the forefront of news, driving nearly 72% of the S&P 500’s gains this year. Notably, Nvidia Corp. (NVDA), a major player contributing approximately 14% of the S&P 500’s returns for the year, recently reported robust earnings amidst the surging demand for artificial intelligence technology.

On August 25, Fed Chair Jerome Powell spoke at the annual economic symposium hosted by the Federal Reserve Bank of Kansas City in Jackson Hole, Wyoming. Powell noted that the Federal Reserve may need to raise interest rates further to cool still-too-high inflation and noted both the progress made on easing price pressures as well as risks from the surprising strength of the U.S. economy. Although Powell’s stance was notably less hawkish compared to his messaging a year ago, there is a strong likelihood that the Federal Reserve will implement at least one more interest rate hike by year-end.

Small-cap stocks sold off during the month and have underperformed the broader equity market in 2023 thus far. We continue to see abundant opportunities in small to mid-cap stocks, given the compelling valuation of the Russell 2000 Value, which currently trades at only 10-12x earnings. This stands in stark contrast to the broader market, which hovers closer to 20x earnings, representing one of the biggest deltas we have ever witnessed.

Merger Arbitrage performance in August was bolstered by deals that made significant progress in securing U.S. regulatory approvals. Shares of Horizon Therapeutics traded higher after the U.S. FTC indicated it was open to settlement discussions ahead of the September 11th trial date, and the FTC and parties formalized a settlement on September 1st. The deal is expected to close shortly after the October 5th Irish High Court hearing. Spreads firmed on other deals that experienced similar regulatory wins including: VMware being acquired by Broadcom for $85 billion in cash and stock; Black Knight was acquired in September by ICE for $12 billion in cash and stock, ForgeRock was acquired by Thoma Bravo for $2 billion in cash in August, and NuVasive was acquired by Globus Medical in September for $4 billion in stock. Investors are actively deploying capital in newly announced deals like Abcam plc, which is being acquired by Danaher for $6 billion cash, and Capri Holdings, which is being acquired by Tapestry Inc. for $10 billion cash.

August saw a return of volatility, and the convertibles market gave up some of its gains for the year but rebounded slightly as we approached month end. New convertible issuance picked up in August after companies reported earnings. We saw a mix of issuance that included companies that are new to convertibles, along with some that are returning to refinance existing debt. This mix of issuance is good for our market and it has generally been at attractive terms with higher coupons and lower premiums than many existing issues. With equities having moved substantially off the lows this year, we think convertibles offer a compelling value proposition. They allow us to stay invested in the market with an asymmetrical profile that has increasing equity sensitivity while still offering a yield advantage and near term maturities that should limit downside participation.

Opinion article by Michael Gabelli, Managing Director and President of Gabelli & Partners.

CAZ Investments, a Houston-based investment manager, and Palantir Technologies, a builder of operating systems for the modern enterprise, announced a five years partnership for Palantir to provide its Artificial Intelligence Platform (AIP) in support of CAZ’s growth and innovation.

Palantir will provide CAZ with AI-powered solutions to accelerate partner onboarding and augment investment managers’ work with generative AI. The use of Palantir’s software aims to help CAZ automatically scale operations and meet growing demand.

AIP will offer CAZ executives a next-best action system to identify and recommend opportunities or content to improve retention and service to its partners, among other use cases, allowing it to provide differentiated investment services to its partners as it embarks on a crucial expansion period.

“The last few years have marked unprecedented growth for CAZ and a dramatic increase in demand for access to our curated opportunities,” said Christopher Zook, Founder and Chief Investment Officer of CAZ Investments. “We are excited to partner with the talented team at Palantir to ensure that we are able to scale our business for exponential growth, harnessing the power of AI to transform our processes.”

“CAZ is embarking on a remarkably ambitious AI transformation that will put exceptional demands on AIP. These are the partners we are looking for,” said Daniel Wheller, Head of Financial Services at Palantir. “We are proud to deploy Palantir AIP at CAZ, bolstering AI transformation.”

Palantir’s technology is currently deployed to solve some of the world’s most complex challenges in the government, defense, and financial sectors, including banking, asset management, anti-money laundering, and cryptocurrency.

CAZ Investments’ proprietary research process and global network identifies thematic investment opportunities across public and private markets. The CAZ team reviews 1,500 private investments in a typical year, but usually invests in approximately 10-12. Among CAZ Investments’ guiding principles is that it will align its interests with its partners, meaning the firm is the first investor in every opportunity it presents to its network.

This means that individual investors and investment advisors alike can participate knowing that CAZ is directly aligned with their success, or that of their client’s.

Inflation and ongoing market volatility remain the primary concerns of business leaders of mid-sized corporates and organizations surveyed by Citi Commercial Bank (CCB) in its first ‘Global Industry Insights Report’.

Of approximately 500 survey respondents, globally, a majority ranked inflation and market volatility as the two primary factors challenging the wellbeing of their business followed by the regulatory environment and trade.

The recent global business survey offers insights into the prevailing challenges and opportunities facing companies today. At the forefront of concerns is inflation, which emerged as the most ominous factor threatening businesses.

A 72% of respondents identified cost management as their primary obstacle to success, reflecting the pervasive pressure inflation exerts on operations and profitability. This unambiguous sentiment suggests that despite other evolving challenges, cost control remains a critical focal point for businesses in today’s volatile economic landscape.

While inflation worries loom large, the survey shows a relatively optimistic view on supply chain issues, a pain point that has plagued industries in recent years. A surprising 52% of respondents believe that the situation has improved over the last 12 months, with only 13% stating it has worsened.

Additionally, 36% report no change, painting a picture of either actual improvements in supply chain management or a more accustomed adaptation to existing challenges. This optimism may pave the way for companies to focus on other key areas, such as sustainability and international expansion.

Speaking of sustainability, the report shows that companies are taking strides in their commitments to becoming carbon neutral by 2050. With 55% of respondents affirming they are on track, led notably by healthcare companies, the move towards sustainability appears to be gaining momentum.

However, it’s worth noting that only 37% consider net-zero and ESG factors as a primary focus, signaling room for greater emphasis on these crucial issues.

Moreover, international expansion remains a tantalizing prospect for over half of the respondents, with Asia-Pacific markets being particularly attractive. Yet, despite these future-oriented plans, 27% express dissatisfaction with their financial goals for 2023, indicating that while there may be optimism for long-term growth and responsibility, short-term financial objectives remain a point of contention.

For additional information, please visit the website of Citi.

Venture capital firm 500 Global announced the UpNext summit will bring together investors, asset allocators, innovators, and policymakers to discuss a shared future for technology and innovation on October 5, at The Showroom in Washington DC.

The future of venture capital necessitates that stakeholders take a more active role in devising strategies and guidelines that produce social and economic value, according to the company’s announcement.

500 Global will present its new report, the 500 Global Rise Report, which outlines a plan for innovation in both developing and mature markets. “The upcoming ten years of technological progress and venture capital will, above all, be international. We, as investors, policymakers, and thought leaders, must collaborate to promote innovation worldwide and generate a positive and enduring impact,” stated Christine Tsai, CEO and founding partner of 500 Global.

According to the company information, UpNext functions as a platform for these key individuals to address pertinent challenges facing the establishment of a sustainable ecosystem that cultivates innovation and global expansion while enhancing competitiveness and ensuring national security.

Speakers at the event will include Magdalena Coronel, Chief Investment Officer of IDB Lab; Dami Osunsanya, Co-Head of SoftBank Group’s Opportunity Fund; L. Felice Gorordo, Alternate Executive Director of the World Bank; and Areije Al Shakar, Director and Fund Manager of Al Waha, among others.

The topics to be discussed are centered around the rise of the new era of global technology, emerging sectors in technology, next global companies, and global economies.

“Achieving the Silicon Valley dream doesn’t mean following the same playbook,” stated Courtney Powell, COO and Managing Partner of 500 Global, a prominent venture capital firm managing $2.4 billion in assets, dedicated to investing in founders building fast-growing tech firms. 500 Global concentrates on technology-driven markets to generate long-term value and drive economic growth, as stated on its website.

In the dynamic world of finance, asset securitization has emerged as a valuable bridge to multiple private banking platforms, enabling the conversion of underlying assets into what is known as “bankable assets”. “Bankable assets” can be effectively distributed through various private banking platforms. This process has become even more powerful by incorporating exchange-traded products (ETPs) as key tools for transforming underlying assets into bankable assets, the FlexFunds team explains in an analysis:

Securitization: a path to liquidity

Securitization is a financial process that goes beyond merely converting liquid or illiquid assets into securities. It also uses ETPs as instruments for this transformation. This process can become quite complex, but thanks to FlexFunds’ solutions, it can be carried out in an agile, straightforward, and cost-effective manner.

FlexFunds’ securitization program is crucial in facilitating access to multiple private banking platforms by designing and launching investment vehicles, similar to traditional funds, that enable strategy management and global distribution to international investors.

Securitization for multiple asset classes

One of the most notable advantages of securitization is its flexibility. It is not limited to a specific class of asset, which means both liquid and illiquid assets can be securitized. Most importantly, private banking treats these operations as debt, streamlining the process of registering a FlexFunds ETP compared to the complex and lengthy verification procedures associated with traditional funds.

Advantages of the asset securitization process

Asset securitization offers multiple advantages that make it attractive to both financial advisors and investors:

Improved liquidity and access to alternative sources of financing: Securitization converts illiquid assets into tradable securities, providing financial institutions with additional liquidity and access to alternative sources of financing.

Customization of securitized assets: It allows institutions to structure securitized securities according to investors’ preferences and needs.

Diversification of investments: Securitized securities can be backed by various types of assets, enabling investors to diversify their portfolios and reduce exposure to specific risks.

How are assets converted into Bankable Assets?

The process of converting assets into bankable assets through an ETP is relatively straightforward for FlexFunds’ clients. In five simple steps, they can bring their ETP to market, facilitating access to investors in the global capital markets:

Design the investment strategy for your ETP.

Sign the Engagement Letter.

Conduct Due Diligence.

Create the ETP.

Issue the ETP.

Once this process is completed, advisors can market the product, which combines a series of assets into a single investment vehicle, simplifying the investment process for their clients.

The Role of ETPs in Modern Finance

ETPs are exchange-traded products that track the performance of underlying assets, such as indices or other financial instruments. They trade on exchanges similarly to stocks, which means their prices can fluctuate throughout the day. However, these prices fluctuate based on changes in the underlying assets.

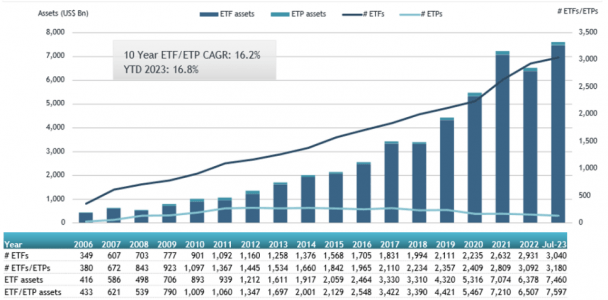

Since the launch of the first ETF in 1993, these funds and other ETPs have grown significantly in size and popularity. According to ETFGI data, as of the end of July 2023, ETFs in the United States reached a record of $7.6 trillion in assets under management (AUM). Their low-cost structure has contributed greatly to their popularity, attracting assets away from actively managed funds, which typically have higher costs.

By the end of July, the U.S. ETF industry had 3,180 products totaling $7.6 trillion in assets, from 289 providers listed on three exchanges.

Trends Toward 2027

According to a report by Oliver Wyman, Exchange-Traded Funds (ETFs) are projected to account for 24% of total fund assets by 2027, up from the current 17%. As of December 2022, total ETF assets under management in the U.S. and Europe reached $6.7 trillion, experiencing steady growth with a compound annual growth rate (CAGR) of approximately 15% since 2010. This growth is nearly three times faster than that observed in traditional mutual funds.

Despite various trends, such as increased demand from retail investors, tax and cost advantages, favorable regulation, growing demand for thematic ETFs, and direct indexing, positively influencing the growth prospects of ETFs, their launches face various challenges. These challenges include the high costs associated with establishing infrastructure and significant risk of failure. These obstacles have given rise to white-label ETF providers, a relatively novel business model that allows fund providers to bring their strategies to market quickly and efficiently.

Additionally, there is anticipated strong focus on technologies like artificial intelligence and autonomous learning to gain competitive advantages and provide greater value to customers. These trends also open up opportunities for wealth managers to expand their business models, especially concerning non-bankable assets, which represent a significant and growing portion of individuals’ total wealth today.

Asset securitization through ETPs offers innovative financial solutions that enhance liquidity, expand financing options, and enable portfolio customization. These strategies align with future trends in the financial sector, which are moving towards personalized solutions and adopting advanced technologies. FlexFunds stands out as a leader in this transformative industry, providing advisors with unique opportunities in modern finance.

If you wish to explore the benefits of asset securitization in greater depth, do not hesitate to contact our experts at info@flexfunds.com

2023 is a year of milestones and celebrations for L. José Corena, Managing Director of MFS Investment Management for the Americas. He will be celebrating 25 years with the firm; MFS will soon celebrate its 100th anniversary; and September 21st has been the official opening of the MFS Miami office, from where Corena and his team will serve MFS clients in Miami, Mexico, the Caribbean, Colombia, and the southwestern United States (Texas, Arizona, and Southern California).

This opening, says Corena, is the culmination of the asset manager’s efforts to strengthen its presence in the Americas, further demonstrating its commitment to collaboration and growth across its distribution footprint. Consider, last year, it opened an office in Montevideo adding to an existing office in Santiago de Chile which opened nearly a decade ago. Additionally, MFS has a representative office in Colombia and an investment office in Sao Paulo, Brazil.

As for Mexico, Corena explains that the company is hard at work and formulating its next steps. However, he hints that there could be more updates “shortly”. “Mexico is a large, unique, and complex market given its idiosyncrasies, but it provides an excellent opportunity for active global managers like MFS.

In relation to the Americas institutional business, the MFS executive clarifies that business emanates primarily from AFPs, AFOREs, insurance and re-insurance cos., family offices and selective local opportunities in key regions. While not currently working with any third-party distributors in the Americas to cover these segments, MFS has had relationships in the past. “We know the institutional segment provides a great opportunity for us to continue to build on our overall competitive market share in the region. We have done a lot of work recently and are evaluating how to best penetrate, service and support these key segments” he notes.

Trends in the Offshore Industry

“Opportunity” is a frequent word in Corena’s conversation with Funds Society. The head of the Americas sees an opportunity in the shift in the way business is done in the Non US Cross Border market, as the number of asset managers continues to proliferate, the distribution model continues to evolve and the independent model gradually takes over: “It’s extremely important for us that the business continues to grow and evolve during this post-Covid world, and that it continues to do so in a diversified way, both from a distribution and product offering perspective”.

Regarding how the distribution model has evolved, Corena says, “It’s definitely more complex right now given how the independent model has taken centre stage. You can imagine, contrary to the past, instead of going to one distributor / company to visit 20 financial advisors, as an example, today it has shifted to having to go to, potentially, to twenty different places and see these same financial advisors (FAs). One can easily see the challenges this poses. That said, the independent model has proven to be dynamic. It provides the financial advisor a great deal of flexibility and ownership of their business. While this can create more distribution challenges, we feel MFS is uniquely qualified to support clients who adopt this model.”

Another trend Corena sees is the general flow of business toward clean asset classes: “The largest distributors are definitely moving the needle towards the ‘fee-based’ business model , which I firmly believe is the right approach long term, as it benefits the overall client/advisor relationship ,” he says.

Corena points out that “transparency is also on the side of the client”, who now has more access than ever to see what they’re paying for an advisor’s services and for their mutual funds, as well as comparing fees and services with the competition and giving them the ability to evaluate the best value proposition for their financial situation. “Looking at big-picture trends today, we are definitely seeing a trend towards fee-based models with an emphasis on institutional share classes combined with retail A shares”, he explains. The MFS executive adds that “as the younger generation of financial advisors continues to grow in the business, they will definitely be more inclined to adopt the fee-based advisory model to their practice,” but he is also witnessing adaptation to this model among advisors who have been in business for a long time. The more experienced cohort is aiming towards building partnerships and teams in order to grow their overall business in a more sustainable, long-term manner. However, Corena concedes that there is a part of the business “that is going to continue to be transactional in nature and will not find its way to an advisory model”.

Another opportunity, he believes, is also changing the distribution model in the industry: “By going independent, we’ve seen many of these FAs joining advisory platforms, retooling their business and approach, and tailoring their practice to fit their client needs. The independent model provides them the freedom to pursue more clients and provide more flexibility. The beauty is that as these teams grow within the independent channel it allows for the creation of specialized sub-teams with part of the team focused on handling the purely transactional needs of clients, while another part of the team focuses on building their business through an intergenerational lenses, where clearly an advisory fee based model is optimal”.

Product Trends

The change in the way the Non-US Cross Border industry does business is, of course, also being driven by the levels in interest rates not seen in the last two decades. “This is an important message to convey to our clients”, Corena says, especially since many have not experienced a period of aggressively rising interest rates like the current one. Corena states that “what worked over the last two decades will definitely not work today or going forward, given this new normal.” Having said that, Corena makes it clear that he believes “it is important and healthy that we get rates back to historically normal levels, because the low-rate environment over the last 10-15 years has been quite atypical.

Another message that Corena believes is important to convey to clients is that while the market selloff last year was historically harsh and has altered the historical performance of many investment products, it is important we accept the fact that volatility will remain for some time. But he notes, “the other side of that coin” is all the repricing has led to an abundance of opportunities that are available to investors now in the fixed income market.

“So far in 2023, we have seen actively managed strategies experience inflows across both its fixed income and equity strategies”, he says.

Corena highlighted the importance of the role active management will have in this new market environment. He makes it clear that he is not against passive management but feels that the current environment will favour experienced and highly skilled active managers: “Looking at where we are and the environment, we’re in, selectivity will be key. At the end of the day, if you are a responsible long-term wealth manager, active management plays a vital part in the overall portfolio and can complement passive exposure.”

Another topic that comes up is investors’ growing interest in alternative investments. “Alts” as an asset class that has attracted a lot of interest and inflows over the past twelve to twenty-four months. But Corena is clear: “MFS has no plans to launch private credit or private equity products. Our responsibility is to create long term value for our clients by allocating capital in a responsible and disciplined manner. We will continue to assess where the best opportunities to fill gaps within our product line and do so thoughtfully and methodically.

While he admits that Alternatives are “an interesting asset class,” he is a bit concerned about their growing ‘commoditized’ popularity: ” Investing in alternatives is not for everyone, given their unique structure and the lack of daily liquidity some of these products have. To that end I feel they have a place as part of a well-diversified portfolio and clients should come prepared to ask really difficult questions to ensure they fully understand the risks associated with alternatives, and really any investment opportunity before them.”

Standard Chartered Americas announced that it has entered a trade finance partnership with Truist Bank that will enhance Truist clients’ ability to conduct global business.

Through this strategic partnership, Truist Bank and Standard Chartered aim to create a seamless and efficient business environment for importers and exporters in the U.S. Standard Chartered will provide centralized processing, analytics and tracking services by leveraging the Bank’s unique network, local expertise, infrastructure, and technology.

Truist’s corporate and commercial clients will benefit from Standard Chartered’s ability to fulfill their trade finance needs in emerging markets in Asia, Africa and the Middle East.

The firms will be expand its trade finance services, specifically in the area of Export and Import Letters of Credit. Through this collaboration, Truist will have access to Standard Chartered’s network and its real-time transaction monitoring capabilities for the entire value chain of documentary trade. This will allow Truist’s clients to confirm, advise, or discount letters of credit through Standard Chartered, especially in markets where the latter has a presence.

The partnership also includes provisions for Standby Letters of Credit (SBLC). Truist clients will be able to execute performance and commercial contracts in markets that require local expertise, facilitated by Standard Chartered’s SBLC delivery capabilities. The partnership enables Truist to process and issue end-to-end SBLCs through Standard Chartered’s network, aiming to improve turnaround times and provide transparency on cost.

“We are proud to have a strong network across the world’s most dynamic emerging economies and regions, which have the U.S. as its major trade partner. This presents immense opportunities for companies looking to expand their reach and tap into these new markets,” said Chris Burtch, Head of Financial Institution Sales at Standard Chartered Americas. “We are thrilled to be partnering with Truist and facilitate its clients’ cross-border trade finance needs across our footprint. With our expertise in navigating the complex landscape of cross-border trade, we are confident that we can support Truist clients, help them achieve their business objectives and unlock new opportunities for growth.”

“Many of Truist’s corporate and commercial clients operate in the global economy and require solutions that allow them to complete transactions effectively across borders and throughout the supply chain,” said Chris Ward, Head of Wholesale Payments at Truist. “This partnership will allow our clients to more efficiently achieve their goals, scale their business, invest in their teams and build their communities.”