Brown Advisory will showcase its U.S Sustainable Growth Fund strategy during the IV Funds Society Investment Summit& Rodeo in Houston.

The event, set to take place on February 29th at the JW Marriott Houston by The Galleria for professional investors from California and Texas, will be led by Madison Freeze, CIMA, Regional Investment Consultant at Brown Advisory.

The goal of the Brown Advisory U.S. Sustainable Growth Fund “is to achieve capital growth, seeking competitive risk-adjusted returns over a full market cycle, through a concentrated portfolio of companies that we believe offer enduring fundamental strengths, sustainable competitive advantages, and attractive valuations,” according to the company’s information.

Brown looks for companies with specific sustainability factors, referred to as “sustainable business advantages,” that directly benefit financial outcomes by specifically driving revenue growth, cost improvement, and franchise value enhancement, the fund description adds.

About Madison Freeze

She is a member of Brown Advisory’s U.S. institutional sales and client service team, where she focuses on relationships with advisors and distribution with registered investment advisors (RIAs), bank trusts, and other intermediaries.

She joined the firm in 2012 after internships at the office of U.S. Senator Jim DeMint and Merrill Lynch Wealth Management. She holds an MBA from the Johns Hopkins Carey Business School and a bachelor’s degree from the College of Charleston.

AlTi Global announced a strategic investment of up to $450 million by Allianz X and Constellation Wealth Capital (“CWC”).

Allianz X will invest up to $300 million through one of its affiliates and CWC will invest $150 million.

AlTi will use the capital principally to fund its M&As pipeline and organic growth activities. This will expand the scale and reach of AlTi’s global UHNW wealth management and strategic alternatives business in existing and new markets, leveraging the industry expertise and relationships of both Allianz and CWC.

The partnership with Allianz offers opportunities to provide additional solutions to service both companies’ clients more holistically.

Nazim Cetin, Chief Executive Officer of Allianz X, and another Allianz representative will be appointed to AlTi’s Board of Directors, and CWC will have an observer seat on the Board, upon completion of their respective investments.

“Allianz X brings capital and skills to our portfolio companies to foster innovation, fuel growth and realize their ambitions. Our investment in AlTi demonstrates our approach as well as our conviction in wealth management and alternatives, and we believe it will unlock opportunities for scale, new revenue streams and societal impact for the Allianz Group,” Cetin said.

The investment in AlTi, detailing $250 million through a combination of $110 million in newly issued Class A Common Stock and $140 million in newly created Series A Convertible Preferred Stock. Additionally, Allianz X has been granted the option to invest up to an additional $50 million in Series A Convertible Preferred Stock, earmarked for AlTi’s international expansion initiatives.

Warrants for the purchase of 5 million shares of Class A Common Stock are also part of the investment package. These Series A Convertible Preferred Stocks and Warrants will be subjected to certain beneficial ownership limitations, and Allianz will face lock-up restrictions regarding the Class A Common Stock it acquires upon closing.

Furthermore, Allianz X retains the right to nominate two directors to AlTi’s board as long as it holds at least 50% of the Class A Common Stock acquired at closing.

Florida’s real estate market will slowly begin to grow in 2024 as interest rates flatten and consumers begin to realize that what they are seeing is the new normal in prices and interest rates, Florida Realtors® Chief Economist Dr. Brad O’Connor said Friday during the annual Florida Real Estate Trends Summit.

The state of the sun saw almost $200 billion in closed sales in 2023, which wasn’t far below 2022, a super-strong sales year post-pandemic, he told a packed room of Realtors®.

Moreover, that number was substantially higher than in the pre-pandemic year of 2018, according to Florida Realtors data.

“There’s still a lot of money flowing through our industry. We’re not dead,” O’Connor said. “Over the next several months, the market could reignite a little bit. Even though there aren’t as many homes for sale, the ones that are for sale are selling for more.”

The summit was part of this year’s Florida Realtors’ Mid-Winter Business Meetings at the Hyatt Regency Orlando. In addition to O’Connor, the summit featured Dr. Sean Snaith, a nationally recognized economist in the field of business and economic forecasting. Snaith has won multiple awards for the accuracy of his forecasts and research.

Mortgage interest rates have likely peaked, and there’s a good possibility that the Fed could begin cutting rates in the coming months — and that could reinvigorate buyers. O’Connor speculated a cut to below 6% could be in the forecast with the first relief possibly coming by May.

“The psychology of buying or selling a home is closely tied to these rates,” he said.

In addition to interest rates, Florida’s high property insurance prices paired with inflation continue to slow buyer demand, O’Connor said.

“People are still saying the real estate market is going to crash. But that’s just not the case,” he said, explaining that adjustable-rate mortgages, which played a large part in the housing crisis of the aughts, aren’t as widespread. “We have weathered the pandemic with no foreclosure crisis. We are not in a position for a crash to happen.”

Recession on the horizon?

Both O’Connor and Snaith acknowledged that signs point to a slowdown in economic growth at the national level, but that a full-blown recession isn’t likely. Even so, Florida’s strong economy is well-positioned.

“We are forecasting a slowdown, not a downturn at this point,” said Snaith. “I think Florida is prepared to weather any national economic storm. We’re ready.”

Several factors are contributing to the resilience of the Florida real estate market against certain national economic trends, creating a unique landscape for both potential buyers and investors. Firstly, the state’s labor market is robust. Moreover, Florida’s population continues to grow significantly, at a rate of about 1,000 new people each day, a trend that Snaith believes leads to increased economic activity, as “An increase in population means an increase in economic activity.”

This demographic expansion is further bolstered by the state’s appeal to “untethered” remote workers, a group for whom O’Connor has observed, “The workplace will never be what it used to be.”

Finally, retirees with home equity who are looking to relocate appear undeterred by high interest rates, indicating a strong demand within this demographic.

The total M&A market dropped to $3.2 trillion in 2023, leaving a backlog of deals that will shape the 2024 M&A agenda. According to Bain & Company’s sixth annual Global M&A Report, the drop in deal multiples led to a wait-and-see atmosphere in 2023, with many sellers hesitant to come to the table at a market bottom.

However, the landscape is expected to change in 2024 as interest rates stabilize and competition for assets increases.

“The drop in deal multiples led to a wait-and-see atmosphere in 2023, with many sellers hesitant to come to the table at a market bottom,” said Les Baird, partner and head of Bain & Company’s global M&A and Divestitures practice. “This year, buyers have their eyes on a growing backlog of deals. A need for liquidity will motivate some sellers, while others will divest assets while reshaping their portfolios. As interest rates stabilize, we expect the logjam in M&A markets will break. When it does, competition for assets will be significant. Winning buyers will use diligence to uncover a differentiated view on revenue and cost synergies and win the deal.”

Beneath the surface of 2023 dealmaking

Across industries, the collapse of tech M&A has been the biggest drag on strategic M&A. Tech deal values declined by roughly 45% as median valuations tumbled from 2021’s high of 25 times to 13 times in 2023.

At the same time, a healthy dose of big-ticket deals supported a strong M&A year for energy and healthcare, prompted by differing sector dynamics.

Megadeals made a mark in the second half of 2023, a possible signal that dealmakers are ready to look forward. For M&A observers, the timing wasn’t too surprising. Many companies had sustained high levels of proactive deal screening and outside-in due diligence even as deal counts fell.

Finally, the year 2023 showed a widening of the gap between how frequent acquirers and their inactive peers behave in M&A downcycles. Most frequent acquirers never stop doing deals even as the market overall contracts. This is significant as Bain’s long-term research shows frequent acquirers outperform in total shareholder return and that this margin continues to grow.

“History shows that downturns and times of disruption always produce newer, stronger competitors that used the turbulence to make market gains,” said Suzanne Kumar, Bain & Company’s global practice vice president for M&A and Divestitures. “Last year’s downturn will likely be no exception, and we expect to see more deals get done in 2024—if for no other reason than there are a lot of assets that should trade. But it won’t be without headwinds. In today’s regulatory environment, with approval processes for contested deals becoming longer and less predictable, companies contemplating large, game-changing M&A must have conviction and fortitude.”

An evolving regulatory climate

At least $361 billion in announced deals were challenged by regulators around the globe over the past two years. Among the $255 billion of those deals that ultimately closed, nearly all required remedies. While most contested deals do make it to close, new research from Bain shows timelines for scrutinized deals have extended considerably. The pre-close period, that crucial and vulnerable phase between announcement and close, can stretch from quarters to years. Most deals close within about three months. But the average time to reach a regulatory outcome for scrutinized deals is now 12 months.

Meanwhile, the regulatory climate continues to evolve. For example, regulators have differentially focused on deals in technology and healthcare, given wider concerns about competition and consumer well-being in those industries. Even as the rulebook changes, companies looking for growth and transformation are staying in the M&A game. The best-prepared acquirers use extensive diligence to wrestle the deal thesis to the ground, confirming a base case with plenty of upside to withstand the twists and turns of deal approval.

Generative AI in dealmaking

Bain’s survey of more than 300 M&A practitioners shows that while only 16% are currently deploying generative AI for deal processes, 80% expect to do so within the next three years.

Early generative AI users are focused on process efficiencies in the early stages of the M&A process—idea generation in sourcing and reviewing data in diligence. A full 85% of early users report the technology met or exceeded their expectations, and 78% say they achieved productivity gains from reduced manual effort.

Practitioners are quick to point out challenges too, identifying data inaccuracy, privacy, and cybersecurity as the most concerning risks to using generative artificial intelligence for M&A. Companies that get the most out of generative AI will invest early to identify the efficiency gains that could deliver a competitive advantage today. Using it for targeted purposes now is a way of building familiarity and setting the stage for higher-impact uses in the future.

The Securities and Exchange Commission (SEC) has proposed a new rule that would update the dollar threshold for a fund to qualify as a “qualifying venture capital fund” under the Investment Company Act of 1940.

The proposed rule would increase the threshold to $12 million in aggregate capital contributions and unsolicited committed capital, up from the current standard of $10 million.

Qualifying venture capital funds are excluded from the definition of “investment company” under the Act. The Economic Growth, Regulatory Relief, and Consumer Protection Act of 2018 requires the SEC to index the dollar figure for this threshold to inflation once every five years.

The SEC’s proposed new rule is designed to implement this statutory directive and would adjust the dollar amount to $12 million, based on the PCE Index. In addition, the rule would establish a process for future inflation adjustments every five years.

According to the SEC, the proposed rule is intended to provide greater flexibility for venture capital funds and promote capital formation. The rule would also ensure that the definition of a qualifying venture capital fund remains up-to-date and relevant in the face of inflation. By adjusting the dollar threshold to $12 million, the SEC aims to provide greater clarity and certainty for funds seeking to qualify as venture capital funds.

The proposal will be published on the SEC’s website and in the Federal Register, and the comment period will remain open for 30 days after publication in the Federal Register.

Interested parties are encouraged to submit comments on the proposed rule, which will be taken into consideration by the SEC before making a final decision. The SEC’s proposed rule is an important development for the venture capital industry, and stakeholders are encouraged to stay informed and engaged in the rulemaking process, the press released ends.

Registered Investment Advisors (RIAs) managed to post the greatest growth in advisor and firm count over the last decade despite facing a 13% decrease in total channel assets in 2022, according to The Cerulli Report—U.S. RIA Marketplace 2023.

The advisor headcount in the RIA marketplace expanded nearly 8.6% in 2022, which is twice the annualized rate of 4.4% over the past ten years. This growth is attributed to new RIA firms and breakaway teams continuing to tuck into large established RIAs.

According to the research, this trend will continue, but likely at lower annual growth rates as the pent-up pipeline during the COVID-19 pandemic begins to normalize.

The overall total firm count of retail-focused RIAs grew greater than 11% in 2022, mainly supported by a large amount of new independent RIAs (12.3%).

However, the RIA channel remains diverse and fragmented—93% of all RIAs manage less than $1 billion in assets under management (AUM), whereas firms above this threshold manage 71% of channel assets and employ 47% of advisors. Cerulli anticipates that asset growth and market share gains will continue to be concentrated among firms managing more than $1 billion in AUM.

“2022 continued to highlight the obstacles that many smaller firms face due to not having the resources or capacity to differentiate and foster inorganic growth in a challenging market. The largest RIAs will continue to dominate as breakaway teams leave employee-based models to join large established RIAs that offer more autonomy, without advisors needing to sacrifice resources they are accustomed to,” says Stephen Caruso, senior analyst at Cerulli.

The research indicates that future market growth will be supported by continued investments from private equity firms and industry consolidators, allowing these firms to capitalize on acquisition opportunities among growth-challenged firms with complementary processes, talent, and clients.

Pixabay CC0 Public DomainAutor: Alexas_Fotos en Pixabay

Despite predictions by many market participants, including us, that the relative setup for international equities was favorable entering 2023, the U.S. looks set to turn in outperformance versus the majority of other developed and emerging markets. However, we note that many indicators that led us to last year’s prediction remain stretched and that the MSCI EAFE Index has outperformed the S&P 500 since markets began rebounding in October 2022.

The primary driver of U.S. index returns in 2023 was the emergence of AI as a significant market driver and the resulting charge of the Magnificent Seven: Apple, Amazon, Alphabet, NVIDIA, Meta, Microsoft, and Tesla. As of mid-December, the Magnificent Seven had contributed about two-thirds of the S&P 500’s roughly 25% return, and the S&P’s remaining 493 stocks about one-third. As of mid-December, the top 10 stocks in the S&P 500 made up one-third of the index, a new high for the period of U.S. outperformance. The comparable numbers for the MSCI EAFE and ACWI ex USA indices are approximately 15% and 11%, respectively.

The Magnificent Seven began 2023 with a price-to-earnings ratio of about 20x and are wrapping up the year with a PE in line with their long-term average of about 28x. In other words, these companies began 2023 at a steep discount, which has been closed. Of their year-to-date return, more than half derived from the increase in their PE ratio and the remainder from robust earnings growth anchored in the explosion of interest and adoption of AI.

Heading into a new year, we see a disagreement between the U.S. equity and fixed income markets. As of late 2023, U.S. equities are priced at approximately 20 times earnings, which is 33% more expensive than the historical average of about 15 times earnings. Moreover, the financial markets anticipate earnings growth of about 12% this year. In other words, optimistic equity investors are willing to pay above-average valuations in anticipation of above-average growth.

However, the fixed income market is pricing in about 125 basis points of Fed easing in 2024 in anticipation of slower economic growth and perhaps the delayed recession many thought was possible in 2023. Market expectations for rate cuts were boosted in mid-December due to the dovishness surrounding 2023’s final FOMC meeting.

We find it difficult to reconcile these two outcomes: a robust economy supporting solid earnings growth and expensive valuations, but not an easier monetary policy. Or you have a weakening economy and likely recession that supports about 125 bps of Fed rate cuts but not robust earnings growth and historically expensive valuations. You can’t have it both ways.

This dichotomy, equity markets calling for growth and fixed income markets for recession, needs to be resolved, and investors may want to seek active equity returns until this situation settles. Given the mixed messaging from markets, we believe that quality and cash flow will be key for equities, and we favor businesses with durable models and the ability to navigate an environment with elevated levels of uncertainty and recession risk. Additionally, we believe active managers may be more agile in adapting to change through the coming year as financial markets rectify this bifurcation of expectations.

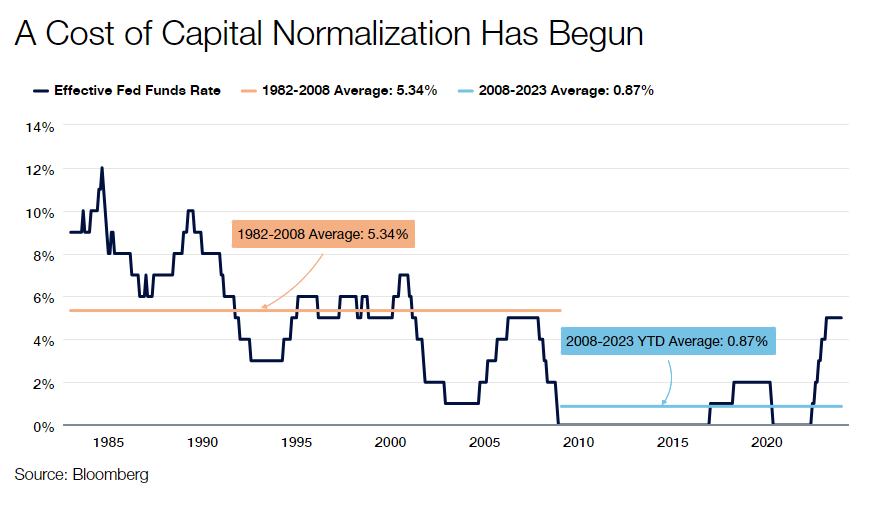

As the growth vs. recession situation resolves, and markets continue to digest a more normalized cost of capital (see the illustration above), we expect more modest returns for equity investors and an environment that may favor steadier income-generating stocks. While inexpensive capital of the past decade was a tailwind for companies with less cash flow today, but higher potential growth rates, the rapid rise in rates that began in March 2022 should support more mature companies with consistent cash flow profiles, strong moats and the ability to self-fund future growth. If this plays out as we expect, income will likely play an even more significant role than usual in total equity returns.

Investors are just emerging from a period of devastating inflation and performance in fixed income, and equity income portfolios that have produced growing income streams may be an excellent hedge against stubborn inflationary pressures in the U.S. and overseas. With fixed income markets still struggling in 2023, equity income has emerged as an attractive opportunity for investors, and we believe it offers attractive relative value and the opportunity to deflect any volatility stemming from the standoff between growth and a slowdown or even recession.

U.S. equities have outperformed international equities for much of the last 15-plus years. But we know from history that relative performance between U.S. and non-U.S. markets is cyclical.

At the end of last year, we noted several factors that in past markets (notably in the early 2000s) had led to a turn in international vs. U.S. performance. While that didn’t happen in 2023 due primarily to the catalyst of AI and the performance of the Magnificent Seven, we note that those factors are still present and at stretched levels:

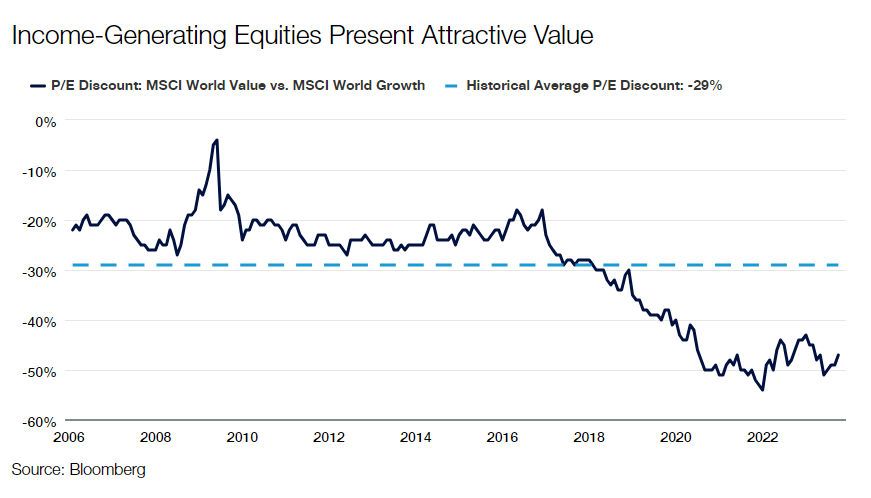

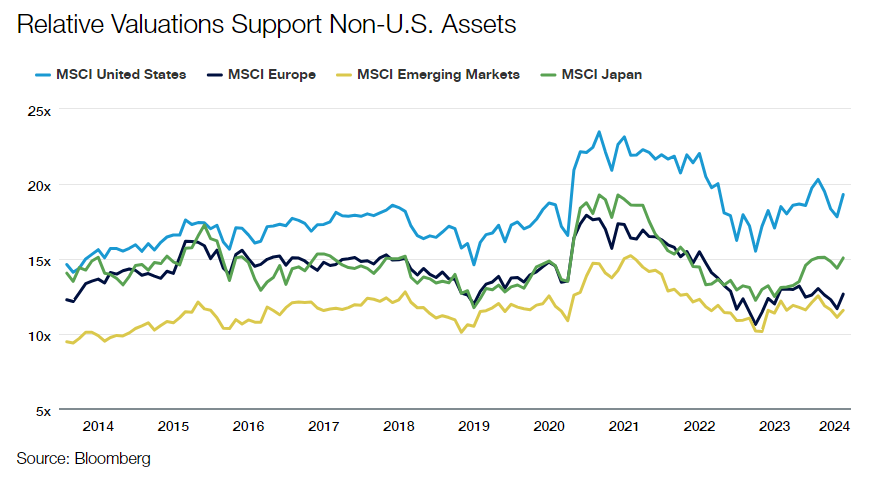

Relative Valuations: The MSCI ACWI ex USA Index trades at a 33% 1-year forward P/E discount to the S&P 500, near the widest levels of more than 15 years of U.S. outperformance. While research has shown that although valuation differentials may have a low correlation to short-term returns, they have an increasing impact the longer the holding period.

The U.S. Dollar: The dollar is a significant factor in the relative performance of international equities, contributing about 40% of international outperformance in 2002-2007 and half of its underperformance since then. The U.S. Dollar Index (DXY) sits at its highest level since late 2002, around the last time international began to outperform the U.S.

Market Concentration and Breadth: As noted above, just seven stocks contributed roughly two-thirds of U.S. performance in 2023, and the top 10 stocks now constitute 32% of the S&P 500. The comparable numbers for the ACWI ex USA Index are about 20% of the total return from the top seven stocks and 11% of the market cap in the top 10 companies.

While we can’t time a turn in relative performance, we think it makes a strong case for rebalancing by U.S. investors who hold roughly 14% of their equity portfolio in international companies versus a 38% weight in the MSCI ACWI Index.

While value has outperformed in international year to date as opposed to the U.S., where growth has outperformed due to AI and the impact of the Magnificent Seven, there is no shortage of interesting Growth and Value investment themes outside the U.S. In AI, many leading “picks and shovels” investments are outside the U.S.—companies such as Taiwan Semiconductor and SK Hynix and semiconductor equipment makers ASML, BE Semiconductor Industries, and Disco. In the booming market for weight loss medications, Ozempic manufacturer Novo Nordisk’s headquarters are located in Denmark.

We like these names because we don’t have to select the “winners” but focus on the firms providing the tools all players need in the AI revolution. We believe many of the best firms and most attractive valuations are outside the U.S.

Opinion piece by Ben Kirby, CFA Co-Head of Investments and Managing Director at Thornburg Investment Management

Insigneo has announced the addition of financial advisors Patricia Holder and Nicole Spirgatis to its network.

Along with Renato Izaguirre as a Client Associate, they form Phoenix Private Client Group, a team dedicated to providing exceptional client service and expertise in Latin American markets, the press released said.

Holder and Spirgatis bring a combined 50 years of experience in financial services, specializing in Latin American markets.

Prior to joining Insigneo, they worked at Morgan Stanley, with Holder spending 25 years at the firm and holding advisory roles at Citi Smith Barney and Merrill Lynch. Spirgatis has a distinguished background at Merrill Lynch, Banco de Crédito del Peru, and Scotiabank.

“We are thrilled to join Insigneo and start this new chapter in our careers,” said Holder, Managing Director. “Our expertise in Latin American markets positions us to contribute significantly to Insigneo’s commitment to excellence. Together, we aim to navigate the complexities of wealth management, build lasting client relationships, and capitalize on opportunities in the dynamic international financial services industry.”

Holder and Spirgatis’ cultural fluency in Latin American markets highlights their ability to deliver tailored wealth management solutions. They recognize the importance of understanding local nuances to provide optimal client service, demonstrating their commitment to building relationships based on trust, expertise, and integrity, the firm added.

“We are excited to welcome Patricia and Nicole to Insigneo. Their experience and success in international markets align perfectly with our growth strategy,” said Jose Salazar, Market Head Miami-US. “Their addition strengthens our commitment to excellence and enhances our ability to serve clients in key markets.”

The addition of Phoenix Private Client Group is another milestone in Insigneo’s expansion efforts, reinforcing its position as a leading wealth management institution in the US and Latin America, the memo ends.

BNY Mellon Investment Management will highlight the virtues of the international context for equity investment at the IV Funds Society Investment Summit & Rodeo in Houston, exclusively for professional investors from Texas and California.

The event, scheduled for February 29th at the JW Marriott Houston by The Galleria, will feature James Lydotes, Head of Equity Income & Deputy CIO at Newton, presenting the BNY Mellon Global Equity Income strategy.

Lydotes will discuss the fund’s features, including “the goal of income and long-term capital growth from a portfolio of high quality global companies, the philosophy that dividend capitalization is the dominant source of long-term returns, and a disciplined and systematic buy/sell investment approach,” according to the information provided by the company.

Moreover, BNY Mellon attributes the strategy’s success to “buying companies with yields greater than 25% BM (FTSE World TR Index) and selling companies with yields below market.”

Additionally, through its boutique Newton, the American bank emphasizes the importance of investing in companies that meet profitability requirements, have sustainable dividends, and are traded at attractive valuations.

After the experts’ presentations, guests will be transported to the NRG Stadium to enjoy the Houston’s Livestock Show and Rodeo from the Funds Society’s private suite.

About James Lydotes

Lydotes is the Head of Equity Income at Newton and the Deputy Chief Investment Officer for Equities. He is also the lead portfolio manager for the Global Equity Income strategy. Additionally, he has been the primary manager for the Global Infrastructure Dividend Focus Equity and Global Healthcare REIT strategies since their inception in 2011 and 2015, respectively. He designed both income-oriented strategies to offer exposure to different themes within a risk-aware framework.

He joined Newton in September 2021, following the integration of Mellon Investments Corporation’s equity and multi-asset capabilities into the Newton Investment Management Group. Prior to joining Newton, he had 22 years of experience across multiple roles at Mellon Investments Corporation and The Boston Company Asset Management (both part of the BNY Mellon group).

J.P. Morgan released its 2024 outlook for the alternative investment landscape.

Uncertainty has remained a central theme in financial markets over the past several years. Surging inflation, rapid interest rate increases, slowing global growth, increased geopolitical risks and elevated stock and bond market volatility have all dramatically shifted the investment landscape, and alternative investments have not been immune.

To help investors take advantage of these market dynamics, J.P. Morgan asked experienced investment leaders from across its $213 billion Global Alternatives platform to share their 12- to 18-month outlooks on several alternative investment markets. Their insights into the trends, risks and opportunities influencing multi-alternatives strategies, core private infrastructure, private equity and commercial real estate are featured in individual papers within the research.

“The case for investing in alternatives remains as strong as ever,” said Anton Pil, Global Head of Alternatives for J.P. Morgan Asset Management. “These assets have historically helped investors diversify traditional portfolios by pursuing investment returns largely independent from publicly traded equity and bond markets, potentially helping to diversify portfolio correlations, lower overall volatility, expand investment income sources, mitigate inflation risk and enhance both absolute and risk-adjusted performance.”

Looking ahead into 2024, the firm expects to see growing demand for alternative investments driven by three broad themes: Displacement, Democratization and Diversification.

Displacement: Much of 2023 saw a slowdown in private market activity, which broadly pressured pricing in many alternative assets. This opened considerable investment value in some segments and could result in a compelling 2024 vintage, especially if the current interest-rate tightening cycle proves to be at or near its peak.

Democratization: Investment innovation continues to expand access to alternative investments through a growing range of strategies and structures available to a much broader number of investors.

Diversification: The investment markets of the past few years have shown the limits of relying solely on traditional stocks and bonds to provide adequate portfolio diversification in the current market cycle. Alternative investments can offer solutions to tap into new, dynamic investment opportunities designed to help better balance portfolio risk/return exposures.

More information about the research and J.P. Morgan’s alternatives offering can be found at the following link.