Photo courtesyEduardo Ferrín and Miguel Ángel Fernández, Founders of Wealnest

The Wealnest Wealth Well-Being Platform, designed to help users organize, visualize, and manage all their assets in a simple and intuitive way, is now active. This pioneering initiative has been developed technologically by a Spanish team with an international vision, and it relies on specialized partners for functions such as valuation, security, and open banking.

The project is led by Eduardo Ferrín and Miguel Ángel Fernández, two executives with extensive experience in management, strategy, and technological development. It is aimed at individuals with medium to high net worth who currently manage their wealth manually or in a fragmented way. It is also designed for professionals, entrepreneurs, families, or emerging family offices seeking uncomplicated control over their assets.

With over 250 subscribers from 15 different countries, who have registered assets worth more than €300 million, Wealnest is redefining what it means to manage wealth in order to live with peace of mind. The project is currently undergoing rapid international expansion across Europe—Germany, France, and the United Kingdom—and the Americas—the United States, Mexico, Colombia, Argentina, Chile, and Peru—through a network of partners. It aspires to become the global reference marketplace for managing wealth well-being.

The concept of “wealth well-being” is at the core of Wealnest’s offering. It goes beyond simply having a solid financial situation; it’s about living with clarity, balance, and oversight over everything a person has built. The goal is to achieve the peace of mind that comes from knowing that both liquidity and owned assets are under control, without losing sight of the future, by planning for both retirement and legacy with foresight.

Miguel Ángel Fernández emphasizes that “currently, around 15% of global wealth is trapped in assets that don’t outpace inflation, so understanding and managing your wealth with the right tools can improve that return. True wealth management shouldn’t be exclusive to the ultra-wealthy, everyone should be able to understand, control, and manage their assets using the best tools available to them.”

Eduardo Ferrín, in turn, states that “the wealth management sector is undergoing a revolution, with €450 billion in annual inheritance transfers from baby boomers to younger generations, and Wealnest meets a need the market currently does not fulfill. Our system goes beyond simply optimizing financial positions. It offers the peace of mind that your wealth is working for you in the right way and adapted to current market conditions.”

Wealnest leverages the capabilities of artificial intelligence to democratize tools that until now have only been available to large fortunes. Through a subscription model, it offers various services based on the selected tier. Even in its free version, limited to three assets, it provides real-time property valuations in major European markets and the United States. The premium version includes additional tools such as succession and retirement planning.

The platform goes beyond showing a snapshot of your wealth: it helps you understand its real value, make your assets more profitable, and plan your future with intelligence and peace of mind, in a way that is simple, intuitive, and accessible, regardless of the size of your portfolio. It combines three key differentiators: ease of use and an onboarding process designed for any user, not just financial experts; affordable pricing, well below that of other professional platforms offering similar services; and smart AI-powered assistance to improve decision-making and optimize wealth management.

The FII Institute has announced the return of the FII PRIORITY Miami Summit, which will be held from March 25to 27, 2026. The event will bring together global leaders to address a central question: how should capital move, adapt, and lead in an increasingly fragmented world.

Under the theme “Capital in Motion,” the 2026 summit will gather policymakers, investors, innovators, and decision-makers to explore how capital, technology, and policies can drive sustainable and inclusive growth, with the Americas at the heart of global transformation.

In its fourth edition, the gathering reaffirms Miami’s strategic role as a bridge between North and South America and as a gateway to international markets. Following the recent success of the FII PRIORITY Asia Summit in Tokyo, Miami will offer a cross-sectional perspective on investment flows, economic resilience, and opportunity generation.

“Miami is not just a place, it is a symbol. At a time when capital is being reassigned, revalued, and reinvented, FII PRIORITY Miami will go beyond dialogue to generate action, shaping impactful partnerships, strategies, and decisions,” stated Richard Attias, Chairman of the Executive Committee and Acting CEO of the FII Institute.

Highlights of the summit’s key content include:

High-level dialogues with global leaders, policymakers, investors, and CEOs on capital deployment, emerging technologies, and growth focused on the Americas.

Strategic closed-door roundtables aimed at influencing investment priorities and delivering concrete outcomes.

Thought leadership and exclusive analysis, co-created with global partners and presented during the event.

The 2026 edition will also mark the beginning of a key year for the institute, leading up to the tenth edition of the Future Investment Initiative (FII 10) in Riyadh at the end of October, consolidating the FII Institute as the global platform where investment, innovation, and policy converge to define the future.

Registration is now open for FII Institute members, partners, media, and invited delegates. For more information and to register, visit the FII PRIORITY Miami 2026 page. More details about the program and speakers will be announced soon.

Photo courtesyStanding: Carlos Torres Vila, Chairman of BBVA, and H.E. Dr. Sultan Al Jaber, Chairman of Altérra. Seated: Javier Rodríguez Soler, Global Head of Sustainability and CIB at BBVA, and H.E. Majid Al Suwaidi, CEO of Altérra (JPG)

BBVA and Altérra, one of the world’s largest private investment vehicles in climate finance, have announced a partnership through which BBVA commits to invest $250 million as a strategic investor in a climate co-investment vehicle that Altérra plans to launch, subject to the necessary regulatory approvals. This alliance reflects BBVA’s recognition of, and interest in, Altérra’s distinctive strategy and capabilities, and supports the bank’s ambition to advance its sustainable finance strategy and growing interest in the Middle East.

Once launched and approved, the fund will be domiciled in the ADGM² and will consolidate Altérra Acceleration³’s existing co-investments into a dedicated structure managed by Altérra, marking a decisive step in its transition to the next phase of growth.

The fund, called Altérra Opportunity, will pursue a globally diversified investment strategy in climate-aligned infrastructure through private equity and private credit. The strategy reflects an investment approach focused on delivering superior risk-adjusted returns and positive climate impact across both developed and emerging markets. The fund will target climate-related investments ranging from energy transition and industrial decarbonization to climate technology and sustainable lifestyles. Its geographic scope will include North America, Latin America, and Europe, in addition to high-growth markets.

H.E. Dr. Sultan Al Jaber, Chairman of Altérra, and Carlos Torres Vila, Chairman of BBVA, announced the strategic alliance during Abu Dhabi Sustainability Week, which concludes today, January 15, in the capital of the United Arab Emirates.

“This fund marks a new chapter for Altérra as we move into our next phase of growth and deepen our ability to mobilize and deploy global capital into high-impact investments. Our alliance with BBVA represents a major step forward in strengthening global collaboration on clean energy, sustainable infrastructure, and technology investments, enabling us to continue supporting high-quality opportunities and delivering long-term value,” said Al Jaber.

“This alliance is fully aligned with BBVA’s strategy of making sustainability a key driver of differentiated global growth and of expanding our presence in fast-growing climate finance hubs like Abu Dhabi. We see Altérra as a long-term partner in mobilizing large-scale capital, and this alliance reflects our confidence in their track record and climate-focused strategy,” added Torres Vila.

BBVA has maintained a longstanding presence in Abu Dhabi through its representative office, established in 2013, demonstrating the bank’s interest in the Middle East as a strategic region for its corporate and investment banking activities. The region’s growing role in global markets and its economic transformation make it a key area for BBVA, which aims to support institutional and corporate clients with an international footprint. This interest has advanced significantly with the recent initial approval granted by the ADGM Financial Services Regulatory Authority to open a new BBVA branch in Abu Dhabi. This will allow the bank to expand its wholesale banking offering in the region and enhance its service to local corporate and institutional clients, while connecting them to BBVA’s global network.

By becoming a strategic investor in Altérra’s new climate fund, BBVA strengthens its relationship with one of the Middle East’s most influential investors, supporting the bank’s strategy to expand its presence and visibility in the region and fulfill its sustainability goals. In addition to this $250 million (€213 million) investment in Altérra, the bank has already invested approximately €300 million in climate funds focused on decarbonization, as part of its broader global climate strategy.

BBVA has set a target to mobilize €700 billion in sustainable business between 2025 and 2029, after having reached its previous goal of €300 billion one year ahead of schedule.

The news broke in the final week of 2025 and sent shockwaves through the industry:Trian Fund Management and General Catalyst announced the acquisition of Janus Henderson for $7.4 billion. At the time, company spokespeople issued a message of reassurance that, from Spain, the firm’s Head of Sales for Iberia, Martina Álvarez, fully endorsed: “The acquisition by Trian and Catalyst puts us in a very privileged position for the strategy we were already implementing,” she stated during a recent press breakfast held in Madrid.

Both Trian and Catalyst bring “a strong focus on growth,” which in the expert’s words translates into “high demands,” but also a commitment to continue investing in “the business, in clients, and in employees.”

Álvarez took the opportunity to reiterate that the vision Janus Henderson has been developing in recent years, and which remains fully in force, is to “invest in a better future together,” structured around three pillars: protect and grow, product innovation, and diversification.

A strategy based on three pillars.

On the first pillar, the Head of Sales referred to the company’s ambitious growth targets focused exclusively on its asset management business, and added: “We have the right to be ambitious: the firm already manages nearly $500 billion in assets globally and close to $5 billion in Spain.” The areas where they are targeting the most growth, the expert explained, include thematic investing (with the Global Life Sciences and Global Technology Leaders strategies as flagships), small caps, European and U.S. equities, and absolute return.

In terms of product innovation, Álvarez specifically highlighted the company’s strong commitment to active ETFs, a segment where it is already a leader in the U.S. and one it has been rapidly expanding in Europe since last year. The firm has already registered 8 active ETFs in the region, collectively managing $1 billion in assets.

A standout among them is the firm’s active ETF focused on AAA-rated CLOs (JAAA), which has ranked among the top 5 fastest-growing active ETFs in Europe. Remarkably, it is the only one among the five that has been on the market for less than a year, during which it has attracted $350 million in inflows. Álvarez described this active ETF push as a way to “broaden our strengths,” while noting it is “where we see the greatest demand from our clients.”

Finally, under the diversification pillar, the Sales Head spoke specifically about “diversifying where clients give us the right to do so.” The firm has been highly active in corporate transactions; Álvarez noted that more than 70 potential deals were evaluated last year alone, though only two acquisitions materialized: one of a private debt specialist in Chicago, and another in the Middle East. The expert added that the asset manager is preparing to register its private debt strategies in Luxembourg soon.

Secondly, the firm has also been active in signing strategic agreements with insurance companies, an area where Álvarez anticipates “strong growth in the U.S. and Europe.”

Thirdly, the firm is focused on developing and launching products specifically designed for distribution through private banks, such as the recently launched Janus Henderson Global IG CLO Active Core UCITS, a fund managed by John Kerschner, the firm’s Global Head of Securitized Products. This product offers exposure to U.S. and European CLOs with investment-grade ratings, focusing particularly on BBB-rated securities to enhance income potential. Martina Álvarez emphasized this shift toward the wealth channel as a sign of Janus Henderson’s growth and evolution: “Ten years ago, it would have been unthinkable for a private bank to choose us as a partner.”

The expert added that the firm expects to further innovate in products “if we receive requests from private banks and it makes sense for us.” Along these lines, she also highlighted Janus Henderson’s long-running training initiatives; for example, she mentioned the firm has signed an agreement to train 350 private bankers in CLOs by 2026.

“We want to understand our clients much better, and that leads us to greater personalization,” the expert concluded.

Lastly, looking ahead to 2026 and anticipating a macroeconomic scenario of persistent inflation, the Head of Sales explained that the asset manager is recommending clients definitively exit cash products and rotate toward investment solutions that provide a higher level of income. She specifically mentioned the Multisector Income strategy, as well as the firm’s short-term fixed income offering with a global approach.

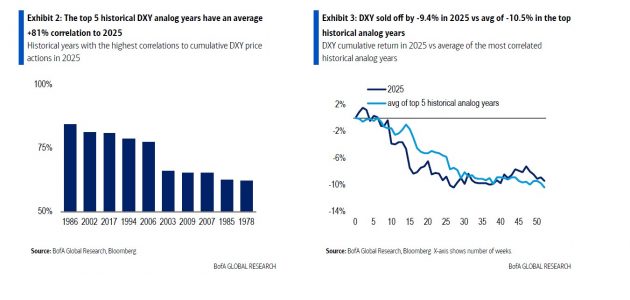

History suggests major dollar sell-offs tend to occur in consecutive years. This is the conclusion reached by Bank of America after analyzing the behavior of the U.S. dollar since the 1980s. Looking ahead to this year, the institution argues that the closest historical analogues point to an additional 8% decline in the Dollar Index (DXY Index) in 2026.

“2018 was the exception, but it coincided with Fed rate hikes, the trade war, and weak European growth. For now, the dollar remains in broad downward trends against G10 currencies. The fact that global equities are outperforming U.S. equities at the start of 2026 warrants attention,” they argue.

Reference to 1995

Focusing on the dollar’s decline in 2025, the institution explains that in the main historical analogues with the highest correlation to last year’s dollar movements, the dollar’s weakness continued the following year in four out of five cases. “The average of the five best analogues would imply an additional -8% drop in the dollar in 2026. Among these analogues, 1995 may be the most relevant for 2026, as it also featured a soft landing of the U.S. economy driven by technology and Fed rate cuts in the second half of the year. The dollar weakened by -4.2% in 1995, close to our forecast that the DXY index will fall toward the 95 level in 2026,” the report notes.

They also highlight that 2018 was an unusual year in which the dollar reversed its 2017 losses and rose by 4.7% due to Fed rate hikes, headlines surrounding the U.S., China trade war, and a weak eurozone economy. According to their analysis, despite a moderate rebound toward the end of 2025, the dollar remains in broad downward trends against G10 currencies. “Global equity markets also began 2026 outperforming the U.S. This factor deserves attention, as equity flows and hedging could become a clearly bearish trigger for the dollar in 2026,” they add.

Years “Similar” to 2025

The dollar fell by 9.4% in 2025 against G10 currencies, according to the DXY index, making it the second-largest annual dollar decline in the past two decades. In identifying the historical years most closely correlated with the dollar’s performance in 2025 and drawing possible implications for 2026, the institution highlights 2005, 1995, and 1975.

Since 1975, the five closest historical analogues have shown an average correlation of 81% with the dollar’s performance in 2025, the report states.

In those five years, the dollar weakened by an average of 10.5%, with most of the decline concentrated in the first half of the year, similar to what occurred in 2025. And in all five historical analogues, the dollar continued to fall the following year, with the sole exception of 2018. On average, the dollar recorded a further 8.3% drop in the subsequent year.

The report also argues that 1995 may be the most relevant analogue for 2026 among the DXY’s imperfect historical comparisons. According to the bank’s analysis, tech-driven growth helped the U.S. economy achieve a soft landing instead of a recession. Additionally, the Fed began cutting rates in the second half of 1995, even though inflation was closer to 3% than 2%.

In light of these findings, the conclusion is that large dollar sell-offs rarely happen in isolation: “This bearish quantitative outcome supports our base case for currencies in 2026, where we expect further dollar weakness due to interest rate convergence between the U.S. and the rest of the world post-Powell, stimulus in the eurozone and China, and increased currency hedging on dollar-denominated assets.”

Outlook for 2026

Looking ahead, Bank of America expects the U.S. economy to struggle after a temporary setback in Q4 2025 caused by the government shutdown, and sees the Fed continuing to cut rates after midyear. Under this scenario, the 1995 analogue alone would imply a further 4.2% decline in the dollar, closely in line with the bank’s forecast for the DXY to fall toward the 95 level in 2026.

Another key observation is that divergence in equity markets could prolong the dollar’s downward trend in 2026. “Although U.S. stock markets reached new all-time highs at the start of 2026, their performance has lagged most global equity markets. With global central bank easing cycles nearing their end, the FX regime is gradually shifting from being almost entirely rate-driven, as it was between 2022 and 2024, to being more influenced by equities. The relative performance of equity markets across countries should be watched closely, as continued divergence like we’ve seen so far in 2026 could become a major bearish driver for the dollar,” the Bank of America report concludes.

A new analysis by Ocorian, specialists in asset services for private markets and corporate and fiduciary administration, reveals that assets in infrastructure funds have reached a record high of $1.35 billion. Their value has more than doubled since 2020, when it stood at $652 billion, and has grown 10% since December 2024, according to the latest Global Asset Monitor from Ocorian.

The firm projects a further 70% increase by 2030, which would bring total assets in global infrastructure funds to $2.3 trillion.

The analysis shows that nearly half (47%) of the underlying assets in infrastructure funds are located in North America, while two-fifths are in Europe. Europe is nearing North America in terms of fund domicile, and Asia-based funds represent about one-sixth of the total.

“Infrastructure investment AUM has grown 10% this year, reaching $1.35 trillion. AI infrastructure, the energy transition, and decarbonization are key drivers of this growth, showing that investors are committing long-term capital to critical sectors and assets that support real economic resilience and sustained returns,” says Yegor Lanovenko, Global Co-Head of Fund Services at Ocorian.

“At Ocorian, we support alternative asset managers in navigating operational and regulatory complexity across the entire investment lifecycle, especially where operational scale makes a difference and investor needs and profiles are rapidly evolving across asset classes,” Lanovenko concludes.

It seems the Trump administration intends to make the final months of Jerome Powell’s tenure at the Federal Reserve more difficult. Over the weekend, the Department of Justice launched a criminal investigation into the Federal Reserve (Fed) over the renovation of the central bank’s headquarters. Jerome Powell, its chairman, views this as a pretext to escalate pressure on the Fed, as President Trump remains dissatisfied with monetary policy, putting the central bank’s independence at risk.

How Have Markets Responded to This Latest Episode?

According to experts, as in previous cases, the Fed’s lack of independence doesn’t go unnoticed, and markets don’t like it. “The global financial ecosystem has entered a phase of systemic volatility and power realignment reminiscent of periods of intense geopolitical friction in the 20th century. The convergence of an institutional crisis at the heart of the Federal Reserve, an aggressive resource-grabbing policy in the Southern Hemisphere, and escalating tensions in the Arctic and Middle East has fractured the stability narrative that dominated the end of last year,” says Felipe Mendoza, CEO of IMB Capital Quants.

Jon Butcher, Senior U.S. Economist at Aberdeen, notes that the initial market reaction appears negative, with rising risks that a devaluation could weigh on the U.S. dollar, equities, and bonds. In particular, he warns, “the long end of the curve could see an increase in term premiums.” In his view, this also raises questions about the composition of the Fed’s Board of Governors. “A new chair is expected to be appointed this month, likely filling the seat of Stephen Miran, whose term ends on January 31. However, Republican Senator Thom Tillis has stated he will oppose any Fed nomination until this legal matter is fully resolved,” Butcher explains.

Powell’s term as a governor runs through 2028, and he had been expected to step down once his term as chair ends in May. However, his recent statement raises questions about whether he will remain on the Board to defend the Fed’s independence despite legal risks. “Regardless of whether this legal action has merit, it signals the administration’s willingness to continue pressuring the Fed to adopt a more accommodative monetary policy. Given that President Donald Trump is also considering fiscal measures that would widen the deficit, we expect growing concerns over fiscal dominance and the external risk of yield curve control,” Butcher adds.

The Question of Independence

Paul Donovan, Chief Economist at UBS Global Wealth Management, believes that if the move is aimed at weakening the Fed’s independence, it could backfire on the administration. He speculates that Powell now has “less incentive to resign as a Fed governor, given the publicly defiant stance he has taken against this criminal investigation.”

“Trump doesn’t directly appoint the next Fed chair—he only nominates the candidate,” he continues. “That candidate must either be a sitting governor or fill a board vacancy. The Senate must confirm the next Fed chair, and that process could become more complicated if this situation is seen as a direct attack on the central bank’s independence.”

Donovan outlines a more extreme scenario, suggesting that if a future interest rate decision is particularly close, “these explicit attacks on central bank independence could push FOMC members toward a more hawkish stance as a show of autonomy.” In fact, he argues, based on market reactions, that may be the safest response from a bond market perspective. “The need to underline independence could become a key factor in rate-setting, both institutionally and in terms of market consequences,” he emphasizes.

The Gold Market Narrative

For Carsten Menke, Head of Next Generation Research at Julius Baer, it’s clear that concerns over the Fed’s independence are being reflected in the commodities market. “Gold and silver reacted positively to the news, rising 1.5% and 5% respectively in early Monday trading. We see increased interference in the Fed as a clearly bullish wildcard for precious metals in 2026. While silver is expected to respond more strongly to such concerns, we still believe its outperformance relative to gold has become excessive,” says Menke.

He concludes that, although the U.S. dollar is also weakening, the reaction in precious metals markets, especially silver, seems somewhat disproportionate. For Menke, growing interference with the Fed and doubts about its independence are among the main bullish wildcards for precious metals in 2026. “With Powell’s expected departure in May, the future of the Fed’s independence will hinge on whether his successor acts independently or aligns closely with the administration. Ongoing concerns over the Fed’s independence and the U.S. dollar’s status as the world’s reserve currency could drive more safe-haven investment into gold and silver, pushing prices even higher than current levels,” he adds.

Powell Defends the Fed

In a rare statement from a central bank chair, Powell said the move represents “an unprecedented action” that should be understood “in the broader context of the administration’s threats and continued pressure.” He stated:

“This new threat has nothing to do with my June testimony or the renovation of the Federal Reserve buildings. Nor does it relate to the Congressional oversight function; the Fed, through testimony and other public disclosures, has made every effort to keep Congress informed about the renovation project. These are pretexts. The threat of criminal charges stems from the Federal Reserve setting interest rates based on our best judgment of what serves the public interest, rather than following the President’s preferences. The real issue is whether the Fed will continue to set interest rates based on evidence and economic conditions, or whether monetary policy will be dictated by political pressure or intimidation.”

To help restore confidence in the monetary institution, he added that throughout his service under four different administrations, he has performed his duties without fear or political favoritism, focusing solely on the Fed’s dual mandate of price stability and maximum employment.

“Public service sometimes requires standing firm in the face of threats. I will continue to do the job the Senate confirmed me to do, with integrity and a commitment to serve the American people,” Powell concluded in his statement.

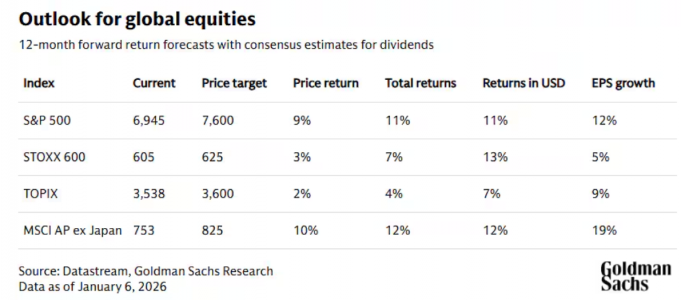

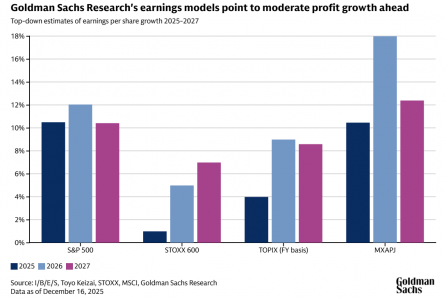

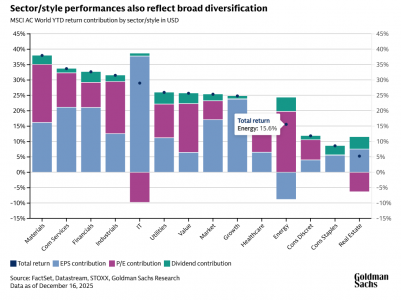

The global bull market could continue in 2026, supported by growth in corporate earnings and resilient economic activity, although equity gains are unlikely to match the strong advance seen in 2025, according to Goldman Sachs Research. The firm expects continued global economic expansion across all regions and further moderate rate cuts by the U.S. Federal Reserve.

“Given this macroeconomic backdrop, it would be unusual to see a significant equity pullback or a bear market without a recession, even starting from elevated valuations,” writes Peter Oppenheimer, Chief Global Equity Strategist at Goldman Sachs Research, in the report Global Equity Strategy 2026 Outlook: Tech Tonic—A Broadening Bull Market.

Looking back, diversification was a central theme for Goldman Sachs Research last year. “Investors who diversified across regions in 2025 were rewarded for the first time in many years, and analysts expect diversification to continue in 2026, extending to investment factors such as growth and value, as well as across different sectors,” they explain.

Outlook for Global Equities in 2026

“We believe that returns in 2026 will be driven more by earnings growth than by rising valuations,” says Oppenheimer. The 12-month global forecast suggests that stock prices, weighted by regional market capitalization, could rise by 9% and deliver a total return of 11% including dividends, in U.S. dollars. “Most of these returns are driven by earnings,” he adds. Commodity indexes could also advance this year, with gains in precious metals once again offsetting declines in energy, as was the case in 2025, according to Goldman Sachs.

Diversification and Market Cycle

Oppenheimer’s team analyzes the typical phases of market cycles: despair during bear markets, a brief phase of hope after the initial rebound, a longer period of growth driven by rising earnings, and finally, a phase of optimism as investor confidence builds.

According to this analysis, equities are currently in the optimism phase of a cycle that began with the 2020 bear market during the pandemic. This stage is typically accompanied by rising valuations, suggesting some upside risks to baseline forecasts.

Should Investors Diversify in 2026?

Geographic diversification benefited investors in 2025, an unusual outcome, as the United States underperformed other major markets for the first time in nearly 15 years. Equity returns in Europe, China, and Asia were nearly double those of the S&P 500 in dollar terms, supported by the weakness of the U.S. currency.

While U.S. equities were driven primarily by earnings growth, especially among large tech companies, markets outside the U.S. showed a more balanced mix of improving corporate results and rising valuations. The growth-adjusted valuation gap between the U.S. and the rest of the world narrowed last year.

“We expect this convergence in growth-adjusted valuation ratios to continue in 2026, even though absolute valuations in the U.S. are likely to remain higher,” notes Oppenheimer’s team.

Diversification is expected to continue offering potential to enhance risk-adjusted returns in 2026. Investors may consider broad geographic exposure, including a greater focus on emerging markets, while combining growth and value stocks and diversifying across sectors.

Elevated Valuations and Sector Opportunities

Although equities performed strongly in 2025, outperforming both commodities and bonds, gains were not linear. The S&P 500 saw a nearly 20% correction between mid-February and April before rebounding. The sharp recovery that followed has left valuations at historically high levels across all regions, including Japan, Europe, and emerging markets.

Oppenheimer notes that non-technology sectors could perform well this year, and investors may benefit from companies that indirectly gain from capital investment by tech firms. Interest is also expected to grow in companies outside the tech sector as new capabilities related to artificial intelligence begin to materialize.

Is There a Bubble in Artificial Intelligence?

Market interest in artificial intelligence remains intense, though this does not necessarily signal a bubble. The dominance of the tech sector began after the financial crisis and has been supported by stronger-than-average earnings growth.

While the share prices of major tech companies have risen sharply, valuations are not as extreme as in past cycles, such as the peak of the tech bubble in 2000.

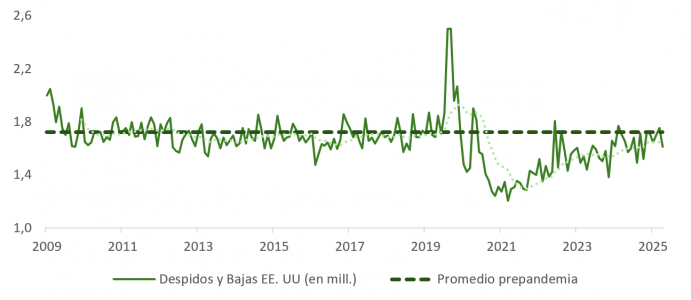

The year begins with few surprises on the macroeconomic front. The U.S. labor market remains in a gray area: hiring appears sluggish, yet there are no significant increases in layoffs. The December ADP private employment report came in below expectations (41,000 vs. the expected 50,000), although it confirms a trend of stability since mid-2025. For Friday’s payroll report, an increase of around 60,000 jobs is anticipated, along with a slight improvement in the unemployment rate from 4.6% to 4.5%.

The November JOLTS survey reinforced this mixed picture: job openings declined from 7.67 to 7.15 million, but voluntary quits rose, typically a sign of worker confidence. Layoffs remain stable. The message? A fragile balance, with no clear signs of acceleration or systemic deterioration. Even so, the divergence between public and private employment could distort the broader interpretation. The BLS’s upcoming methodological revision in February could mark a turning point in how labor data is assessed.

In this context, the Fed maintains its “wait and see” approach, with growing attention on employment trends as a key variable for adjusting monetary policy. The possibility of an additional rate cut by mid-2026 will largely depend on how the labor market evolves in the second quarter.

Growth, CAPEX, and Focus on the Tech Sector

The Atlanta Fed’s GDP model projects above-potential growth. The recovery remains concentrated in specific sectors, such as technology, which generate little direct employment. Focus will turn to fourth-quarter results from hyperscalers to assess whether investment momentum is holding. However, BEA data shows that tech CAPEX has lost traction in recent months.

The potential slowdown in tech investment comes at a time when the market is beginning to demand concrete results. Investors are no longer rewarding narratives alone, they are starting to penalize models without clear profitability. This could lead to a rotation toward sectors with more visible fundamentals.

ISM Services and Favorable Signals for Risk Assets

The ISM services index exceeded expectations (54.4) and showed improvements in the new orders and employment components (the latter rising to 52, entering expansion territory), while the prices subindex declined. This combination of easing inflationary pressure and modest gains in activity and employment is favorable for risk assets, helping to keep the 10-year Treasury yield below 4.2%. That, in turn, supports equity valuations and strengthens expectations that the Fed could cut rates more than markets had anticipated after its last meeting.

The composite ISM and JOLTS indicators support the case for wage moderation. Layoffs are at a six-month low, and the Challenger index fell from +23.5% to -8.3% in December. This environment reinforces the post-pandemic normalization narrative, with a soft landing increasingly gaining traction as the baseline scenario.

AI, Productivity, and Pressure on Wages

The accelerated adoption of AI tools is beginning to show effects on productivity and labor structure. While it enhances efficiency, it also reduces employees’ bargaining power, contributing to further moderation of real wages in 2026.

Although large-scale AI investment began in 2024, its impact on productivity remains uneven. Some major companies have achieved tangible improvements, while others are still in the exploratory phase. The market is beginning to differentiate between those with a clear monetization strategy and those without.

This shift in focus will also have implications for the labor market. Sectors such as financial services, marketing, and administrative technology could see workforce adjustments in favor of leaner structures.

Energy, Housing, and the Electoral Agenda

On the geopolitical front, U.S. control of Venezuela’s oil sector, with a projected release of 30 to 50 million barrels, could stabilize crude prices between $50 and $60. This aligns with Trump’s goals of protecting the purchasing power of his electoral base.

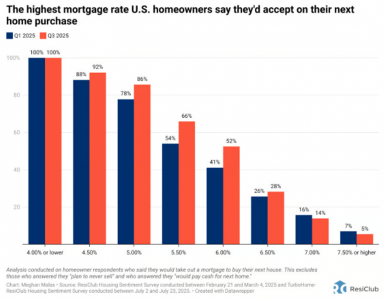

President Trump is also seeking to improve housing access. His proposals include limiting the role of institutional investors in the residential market, allowing retirement savings to be used for home purchases, and promoting mortgage portability. In addition, he is pressuring Fannie Mae and Freddie Mac to acquire up to $200 billion in MBS, which would lower real estate financing costs. If fully implemented, the 30-year mortgage rate could fall below 6%, compared to the historical average spread of 1.76% over the 10-year Treasury (currently at 2.03%).

These measures carry a strong electoral component. The early 2025 ResiClub survey suggests they could help revive the housing market. Understanding the behavior of the “lower leg” of the K-shaped economy will be key to sector allocation in portfolios.

Political Stimulus and Inflation Expectations

With limited fiscal space (debt-to-GDP above 120%), Republicans may intensify the use of alternative policies: deregulation, tax cuts, selective tariff reductions, and access to cheaper financing. The OBBBA plan will play a key role in catalyzing investment during the first half of the year.

At the same time, inflation could ease more than expected in the second half of 2026. The impact of tariffs is likely to fade, and productivity gains from AI may have a meaningful disinflationary effect. Trump may also choose to ease certain trade sanctions (including those on China), aiming to support growth and broaden his electoral base.

In addition, private consumption could rebound if direct transfer mechanisms, such as checks or temporary subsidies, are activated. The conditions for a more expansive second half in terms of consumption are in place, as long as external shocks do not materialize.

Sector Rotation and a Rally Beyond Technology

While AI-related CAPEX and productivity gains are expected to remain in the spotlight, the rally could extend to previously lagging sectors such as industrials and consumer goods. Active sector selection will be key in 2026 to capture shifts in the composition of growth. Valuations continue to show exploitable dispersion.

In this environment, maintaining a balanced exposure across technology, advanced manufacturing, and services could be a prudent strategy. Additionally, cyclical sectors may benefit from an extended economic cycle if consumption holds and inflation continues to ease.

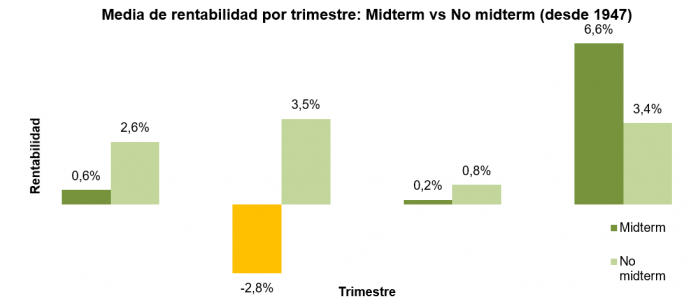

Tactically, the combination of contained interest rates, disinflationary pressure, and active policy measures could create a favorable backdrop for maintaining exposure to risk assets during the first half of the year. However, we anticipate increased volatility and will be monitoring historical parallels with U.S. midterm election periods.

Photo courtesyFrom left to right: Michael Averett, Chief Revenue Officer for Insigneo; Mariano Huidobro, SVP Financial Advisor at Insigneo; Edward Varona, Insigneo advisor; Juan Carlos Amado, Financial Advisor at Insigneo; and Andres Brik, Senior Vice President at Insigneo.

During Insigneo’s triennial event held in Seville in November 2025, several of the firm’s financial advisors shared their vision on how they are guiding their clients through the transition toward advisory services, moving away from the more traditional transactional model common among broker-dealers in the region. Far from framing it as a simple “account change,” the panelists agreed that the shift to the advisory model is driven by a combination of good timing, financial education, transparency, and client connection. Above all, they recognize that this change stems from the advisor’s ability to deliver excellence to their clients.

“For me, in a broad sense, excellence is about giving more of yourself—something similar to what happens in sports. For example, Kobe Bryant used to do something different; he didn’t have extraordinary talent. His team was willing to give more, just like we want to give more to our clients every day, and that’s why I believe excellence is built when no one is watching. Working late nights, training hard, improving 1% in every small thing 1,000 times, it’s a process of hard work, not a single performance. We aspire to excellence as a team, and I believe we have the best team,” said Juan Carlos Amado, Financial Advisor at Insigneo.

In the view of Edward Varona, Insigneo advisor, excellence is achieved by adopting a different mindset. “If we analyze a problem, for example, how to manage volatility, we need to step back and figure out where we might fail so we can avoid it. The key is, if we can prevent volatility by explaining to clients that it’s not about constantly watching the screen, then that kind of proposal and way of thinking will add value,” Varona explained during the panel discussion.

A Transition Built on Experience

Advisors are confident in their ability to provide excellence and added value to clients; now comes the more complex part: transitioning to a model of explicitly paid advisory services. Along this path, one of the concepts most often mentioned by advisors was the use of so-called “natural transition moments.” Situations such as a platform shutting down or structural changes in a firm, for example, the closure of Wells Fargo Advisors, force clients to move their assets. Rather than replicating the old setup, advisors use this moment to reframe the relationship and focus on becoming more efficient and improving client service.

That was the case in the experience shared by Varona, a former Wells Fargo advisor, during the panel. “In my case, I was quite lucky, it was like being in the right place at the right time. We built our business from our branch with a synergy-focused approach and a solid team. So, when the shutdown happened, I almost saw it as my own ‘Liberation Day,’ because I was able to continue working within a model where advisory is a key and integral part of the business and your frontline operations,” Varona recalled.

For Andres Brik, Senior Vice President at Insigneo, the journey was a mix of conviction and passion, culminating in a single proposition: the advisory model. “We like to take the reins of investment, even in more complex assets like alternatives and private markets. I do believe that, as markets evolve, clients need to understand that financial education is extremely important, especially for private assets. This is work we do by combining education, the technology from various providers, and quarterly reviews. The result is that when something happens in the market, like last year’s ‘Liberation Day’, we don’t get calls from clients asking what’s going on, because they know exactly what they have in their portfolios and how those assets behave. They’re fully aware of what they hold,” he explained.

Making the Case to Clients and the Next Generation

When it comes to knowledge, advisors aren’t just referring to how assets or portfolios work, but also to the cost of investment, of advisory services, and the margins involved. As Varona acknowledged, that was one of his strongest arguments when guiding clients through this transition. “I showed clients, openly and transparently, the fees—so they could decide for themselves. We were also lucky because, right in the middle of the transition, we saw that Insigneo’s IMAPS program was available. The other thing we did was, for every new client opening an account, I’d set up a dual scheme: a transactional account and an advisory account. And I’d explain: ‘Look, we have these mutual funds. And math doesn’t lie; it comes down to that, math doesn’t lie. There’s an internal expense ratio. These firms need to keep the lights on, you know. So, if we move from here to here, from this share class to that one, you’re going to save money.’ That’s basically it,” Varona recalled during the event.

Beyond transparency with the client, advisors emphasized that the advisory model is better aligned with today’s expectations, and especially with those of the next generation. “One of the common and key factors is listening to what your client has to say. We have two ears, two eyes, and only one mouth, there’s a reason for that. To connect with the client and understand their needs, you have to listen: what is their body language telling you, what is their attitude saying? It’s essential to earning their trust. And having younger professionals on the team also helps improve that empathy, especially with younger generations,” noted Mariano Huidobro, SVP Financial Advisor at Insigneo, who shared his experience on the panel.

Among other conclusions presented by the advisors regarding the advisory model were the importance of professional and ongoing management, consistency with goals and risk profile, long-term planning, and a clear fee structure, all of which are increasingly valued by heirs and younger clients. These elements become especially relevant when navigating uncertain cycles and environments, as in 2025. In this regard, Amado emphasized that advisors must prepare clients for volatility. “Volatility is the price you pay to stay in the game. But then comes the question of how you can reduce volatility with the range of products we have. And I firmly believe that Insigneo has a platform that gives clients access to an unmatched range of products. For me, private infrastructure plays a very important role in reducing volatility without sacrificing returns, taking fees into account. When you go through those storms with the client, explaining why something is happening now and how their portfolio is positioned for it, and show them that every time we’ve been through this before, the market recovered and so did the portfolio, then the transition becomes much more manageable,” he pointed out.

The Value of Advisory

Up to this point, Insigneo’s advisors are clear on the value they deliver, but as they themselves admit, it’s difficult to price their service. “The transactional part of the business is like a commodity: it’s very hard to prove your value if you’re not adding any. That’s why, among brokers, we do a lot of non-discretionary advisory. But I also think it’s important to move forward and start developing the advisory business. IMAPS is a very good solution because you have the entire senior team, strong performance, and it’s a way to start building an advisory business. Another path is through the technology we have, Orion, which integrates accounts and lets you access other parts of the client’s wealth held on other platforms. That way, you can provide real advisory on their true asset allocation,” concluded Huidobro.