Commodities: The Market Story Implied by the “El Niño” Phenomenon

| By Amaya Uriarte | 0 Comentarios

After Spain, the new name capturing attention in the markets is El Niño. According to experts, this weather phenomenon—currently in a phase of active strengthening and intensification in the equatorial Pacific Ocean—could complicate the path of inflation, supply chains, and expectations in commodity markets, particularly agricultural ones.

For experts at Lombard Odier, climate volatility is becoming a global phenomenon. “Recurrent phenomena such as the El Niño cycle are displaying unusual intensity and timing, amplifying the frequency and severity of extreme weather events across multiple regions, with potential macroeconomic repercussions,” they argue in their latest report.

It is certainly a risk that, behind the geopolitical headlines, is beginning to gain traction. “The El Niño phenomenon currently constitutes the central scenario through early 2027. While its direct impact on developed economies remains limited, its effects on food supply, hydroelectric generation, and more agriculture-dependent economies represent a genuine supply-side risk that could keep headline inflation elevated for longer and complicate the disinflation process on which equity markets currently rely,” maintains Terry Ewing, Head of Equities at MIFL.

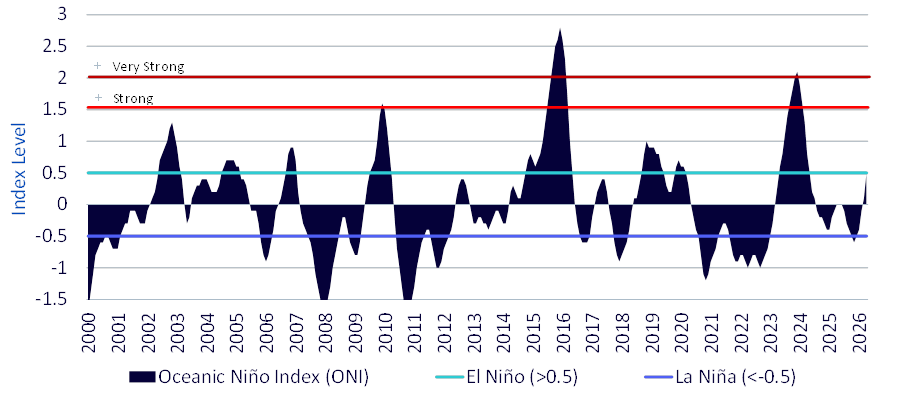

To understand the impact this phenomenon has on commodities, the data speaks for itself: in 2023–2024, cocoa surged 250%, sugar reached its highest price in over a decade, and rice exporters closed their borders. The Oceanic Niño Index, which represents the three-month moving average of sea surface temperatures in the east-central Pacific, points toward what meteorologists describe as a strong or very strong event. “Compounded by disruptions in the Strait of Hormuz—which have slowed the flow of fertilizers from the Middle East precisely when farmers need to secure inputs—this event comes at a time of unusual fragility for global food production,” notes Aneeka Gupta, Director of Macroeconomic Research at WisdomTree.

Commodities and Regions

However, one of the primary considerations experts point out is that not all commodities will be affected equally; rather, it depends on the geographic region in question. As Gupta explains, South and Southeast Asia are the most exposed regions. “Scantier monsoon rains and above-normal temperatures are classic features of El Niño in this region, directly impacting rice, sugar, and coffee crops. Rice production in India and Thailand has dropped sharply during previous severe episodes, and there is a real risk that supply strain could once again trigger export restrictions, further tightening global balances,” she points out.

She adds that the impact in West Africa will center on the cocoa harvest, where production could decline considerably, while in Australia, a sharp drop in wheat acreage is expected, with a potential production decrease of approximately 9 million metric tons in the 2026/27 crop year. “Not all regions face this situation. Argentina is one of the few countries that structurally benefits from El Niño, as above-average rainfall typically favors soybean, corn, and wheat production. Conditions also tend to improve in parts of the southern United States. These are genuine counterweights, but they are unlikely to fully offset what Asia and Africa may lose,” the expert emphasizes.

The Historical Conclusion

Taking a historical perspective, as summarized by Darwei Kung, Co-Head of Commodities at DWS, price spikes in agricultural products tend to be shorter-lived than those seen in metals or energy. “However, when market supply is tight, even small harvest disruptions can cause rapid price movements. Added to this is a long-term structural trend: rising demand for biofuels, driven by governments aiming to reduce their dependence on fossil fuels. We expect to continue seeing upward pressure on food prices over the coming months and years,” Kung explains.

According to his analysis, these effects usually emerge with a lag and vary by crop and region, but they can carry significant consequences for monetary policy. “Food prices significantly influence inflation expectations beyond their actual weight within the consumer basket,” he concludes.

Ultimately, Kung contends that El Niño is not merely a weather story, nor is it exclusively a food story: “For investors, it is also a story of volatility. High fertilizer costs, energy market uncertainty, and fragile food supply chains make agricultural markets more vulnerable today.”