During the first six months of the year, gold’s performance has been remarkable, delivering a year-to-date return of 5%. After decisively breaking through previous psychological barriers, gold reached an all-time high on January 29, 2026, touching $5,595.42 per ounce. In the months that followed, the market began to stabilize and gradually correct as central banks maintained—or even increased—interest rates to contain inflation.

“The precious metal became, to some extent, a victim of its own success: significant profit-taking emerged, particularly in U.S. ETFs, while some central banks—such as Turkey’s—had to draw on their reserves to support their currencies,” acknowledges Diego Franzin, Portfolio Manager of Strategies at Plenisfer Investments (part of Generali Investments). However, he notes that the asset is still widely perceived as the “ultimate solution” for diversifying and protecting portfolios against market risks.

Price Dynamics

In Franzin’s view, gold price dynamics remain closely linked to developments in the Middle East and the trajectory of black gold.

“Any stabilization of the geopolitical landscape could ease the economic pressure stemming from energy costs and moderate expectations of further rate hikes, a scenario that would likely reduce gold’s short-term appeal, given that it does not generate income. Beyond short-term volatility, we believe gold will continue to play a structural role in portfolios thanks to its function as a store of value and a tool for financial independence in an increasingly complex geopolitical environment,” he argues.

However, Charlotte Peuron, Precious Metals Portfolio Manager at Crédit Mutuel Asset Management, believes that gold prices are influenced more by monetary policy than by geopolitical risks.

“Currently, gold prices are being driven more by changes in real interest rates and monetary policy than by geopolitical risks. The oil supply crisis, together with its potential economic and inflationary consequences, has effectively eliminated expectations of further rate cuts by the Federal Reserve, which is also weighing on precious metals prices. Given the current situation, this volatility is likely to persist until these uncertainties are resolved,” she says.

This view is also shared by UBS Global Wealth Management. Its experts note that while gold has historically benefited from safe-haven demand during periods of heightened geopolitical tension, this time the precious metal has come under pressure due to concerns that elevated energy prices could prompt a more restrictive monetary policy stance from the Fed and other central banks, thereby increasing the opportunity cost of holding gold.

Nevertheless, they acknowledge that although headwinds for gold have intensified recently, the metal could regain momentum as concerns about future Fed rate hikes begin to fade.

“We remain positive on the outlook for gold and continue to view the precious metal as a source of diversification within portfolios. While short-term performance may remain sensitive to headlines related to the United States and Iran, energy prices, U.S. bond yields, and the dollar, the medium-term bullish thesis continues to be supported by central bank demand, reserve diversification, elevated global debt levels, and the prospect of a more accommodative Fed later this year,” says Mark Haefele, Chief Investment Officer at UBS Global Wealth Management.

Gold in Portfolios

Both experts agree that gold is becoming increasingly entrenched in investor portfolios.

“If inflation becomes entrenched, gold is likely to regain its role as a safe-haven asset following the new cycle of rate hikes. Conversely, if the conflict with Iran ends quickly without triggering a surge in inflation, the Federal Reserve could seek to stimulate the economy by resuming its rate-cutting cycle. Both scenarios are favorable for gold. Finally, currency weakness driven by fiscal deficits and rising public debt has supported gold prices in recent years. In the current environment, some governments may expand deficits even further, which would likely be positive for gold,” adds the Crédit Mutuel AM specialist.

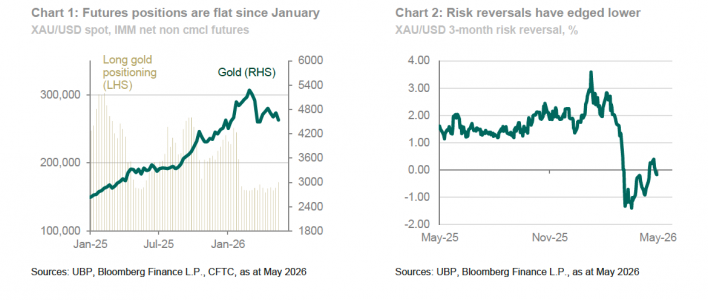

Meanwhile, UBP notes that investor activity in gold and the broader precious metals complex has stalled since the end of February.

“IMM futures data remain virtually unchanged, indicating that institutional investor interest in gold has leveled off. Open interest has also remained flat. ETFs experienced significant outflows in March—the largest monthly decline since 2021—and since then, inflows have slowed to a trickle. Retail interest in gold has also declined substantially overall,” the firm states in its latest report.

For the experts at UBP, the data and overall market sentiment point to a substantial decline in short-term appetite for long positions in gold. “However, the longer-term outlook for gold remains constructive, suggesting that the recent weakness is best viewed as a pause within gold’s broader upward trend,” they note.