BBVA Compass announced thatGabriel SanchezIniesta has been named its new chief information officer following Sergio Fidalgo’s appointment as Spain-based head of Applications & Architecture for BBVA Group.

Until now, Sanchez Iniesta served as BBVA Group’s Multichannel Technologies director. A native of Madrid, he was responsible for developing the multichannel architecture BBVA developed in many countries across its global footprint and the core banking platform it currently uses in Spain. He came to BBVA Group in 1997 following several years with Accenture.

Fidalgo, who was in charge of BBVA Compass’ Technology and Support Services unit for five years, successfully led a major transformation of the bank’s legacy technology into a core banking platform that enables real-time transactions. American Banker called it an “epic” project and “one of the largest bank core overhauls in the U.S.,” while one analyst told the Houston Business Journal it had the makings of a “game changer” for the banking industry.

Sanchez Iniesta inherits that ground-breaking platform and is well-positioned to lead the next phase of the bank’s technology growth, which will focus on multichannel banking, said BBVA Compass President and CEO Manolo Sanchez.

Wikimedia Commons. James Boyne deja su puesto de COO en Calamos Investments por la filantropía

Calamos Investments, announced the planned departure of James Boyne, President and Chief Operating Officer, effective September 30, 2013. Until that time, Mr. Boyne will act in an advisory role and assist the company in the orderly transition of his duties and responsibilities.

Boyne joined Calamos Investments in April 2008 and served in a number of executive positions since then. He has decided to pursue a leadership position in the non-profit sector, focusing on the betterment of children and young adults. Boyne and his family will be relocating to Steamboat Springs, Colorado.

“I appreciate Jim’s leadership during his tenure at the firm and wish the best to him and his family,” said John P. Calamos Sr., Chairman, Chief Executive Officer and Global Co-Chief Investment Officer.

The firm does not plan to replace the role of President and COO, and Boyne’s responsibilities will be assumed by other senior leaders at Calamos, including the firm’s Executive and Operating Committees.

Vincent Oswald, cofundador de Azure Partners. (Foto cedida por Azure. Los fondos de fondos de microfinanzas, “una inversión de atractivos retornos”

Azure Partners’ team offers one of the longest track record investing in microfinance and combines a total of 24 years of direct microfinance field experience combined with solid entrepreneurial background. For the co-founders of Azure Partners, Jack Lowe and Vincent Oswald, launching funds of funds was a natural step after managing the largest microfinance debt fund at BlueOrchard Finance from 2004 to 2008.

As explained byOswald, in an interview with Funds Society, microfinance provide an excellent investment case:

De-correlated investment

Stable returns and low volatility

Fast growing markets

Access to the real and informal economy

Vast social impact

Azure Partners, a swiss based investment advisor specialized in microfinance, advises two microfinance funds of funds:

– Azure Global Microfinance Fund (AGMF) is the first fund of funds managed by professional from the microfinance investment industry. It offers a diversified exposure to different investment funds with specific microfinance strategies, from traditional debt funds, to balanced debt and private equity funds, to Private Equity funds.

– Azure Microfinance Private Equity Fund (AMPEF) which aims to focus on investing in strong locally managed microfinance Private Equity funds focused on specific countries or regions with a hands on approach. The fund will combine 20% co-investments with 30% secondary purchases and 50% primary funds to deliver strong returns to our investors.

Respect to its investment process, Oswald said that they have a 5 steps investment process. “In comparison to more traditional fund of funds, we also conduct Due Diligence of underlying Microfinance Institutions in our portfolio, especially for Private Equity funds. This is a key part of our analysis and a clear added value to the decision process”.

Asked if the fund has a charitable side, the co-founder of Azure reply that investing in microfinance has a vast impact. “By its activity and type of clients, Microfinance generates an impact for millions of micro-entrepreneurs in the countries where we invest in”.

“We do not see the fund as charitable, as it delivers a credible financial return to its investors. However, we pay high attention to our investments social impact. Therefore, we developed our own Social Performance rating to analyze the funds we invest in and include it in our investment decision process”.

He also explained that they have atop-down / bottom-up approach in selecting their investment opportunities. “Usually, debt funds offer a worldwide exposure to microfinance markets and we focus in choosing the best one for the fund”.

He added that regarding the regional and private equity funds, they perform region and country analysis in order to chose the country, which will fit the investment allocation and diversification requirement of the funds. “We will then look for opportunities in these regions/countries. The fund managers looking for investors in their funds also directly contact us”.

Oswald explained that their fund is focus on microfinance activity only and in that sense, is very sector focus. Each product they advise has its own specific regional, country and single fund exposure limits.

At the end of June, AGMF had 6 investments positions, presenting indirect access to 169 Microfinance Institutions in 48 countries, providing financial services to more than 670.000 micro-entrepreneurs in the world. “For AMPEF, we are in fund raising mode and we plan to make 10 to 15 investments”.

In terms of sales policy, “for AGMF we use a combination of banking platforms (large banks promoting our fund to their clientele) and fundraising companies with a geographic focus. For AMPEF, we have signed a number of fundraising agreements also with geographical focus. We obviously also use our personal networks acquired through our years of activity in the investment world but we do not internalize investor relations or fundraising”.

AGMF has currently more than $6M of AuM and is expected to reach over $20 million by the end of the year. For AMPEF they are looking to raise $100 million in the course of two years.

Oswald believes that compared to other similar funds, “the funds of funds in microfinance offers a differentiated investment strategy to deliver attractive returns while managing the risk efficiently. It provides an active regional and country allocation, an exclusive access to secondary opportunities, access to smaller more innovative funds, access to regional funds, access to opportunities dedicated only to microfinance investors. In that sense, it’s an ideal product for an investor seeking a global exposure to the microfinance investment universe”.

They invest only in funds, holdings or SPVs. They do not do direct investments into Microfinance Institutions except co-investments. The YTD performance of AGMF is 0.92%, which represents 2.21% annualized. The back tested performance presents a 5% – 6% net return in USD once the fund will reach its target size. For AMPEF they are targeting a relatively net return to investors.

Despite the crisis, international fund management companies have grown almost continuously within the Spanish market in recent years. With the exception of some periods in which their assets have fallen (as was the case in early 2012), collective investment institutions of foreign companies which are available for sale in Spain have doubled their assets under management in a period of three years. As Inverco’s latest estimates indicate, the assets of foreign CIIs in Spain would be around Euro 60 billion ($80 billion) as at the end of June. This figure doubles the Euro 30 billion estimated by Inverco in late 2009.

Inverco, which performs its estimates with the data from the CII’s from which it receives information (in this case, extrapolating data from 24 fund management companies with Euro 45.5 billion in assets under management, which are approximately 75% of the total), estimates that figure as the amount traded in assets amongst all domestic customers, both retail and institutional. The data shows an increase of 13.2%, a total of Euro 7 billion, in the first half of the year. The capital gain is comparable to that managed by national fund managers, which, according to Inverco and Ahorro Corporación, during the first half of the year saw asset gains of almost Euro 10.6 billion, i.e. around an 8.5% growth.

A 30% share

Inverco estimates that the total CII assets marketed in Spain, both national and international, would be close to Euro 200 billion (137.5 billion managed by domestic companies, and 60 billion by foreign ones, according to data as at the end of July). According to this information, foreign managers have achieved close to a 30% share of the Spanish market, the highest in history. That figure would be lower when using data from the CNMV ( National Securities Market Commission), which takes into account all fund management companies; according to its latest available data, as at the end of March 2013, the securities supervisor estimates the assets managed by international asset management companies at 44.5 billion. Even so, foreign CIIs would have a weight in the industry of around 20%, which is four times higher than the March 2009 share (7%). And the money keeps rolling into them: in total, the amount of net subscriptions to foreign collective investment schemes which facilitate their data to Inverco stood at Euro 2.9 billion in the second quarter of 2013.

Diversification and product offers

According to experts, this trend of capital raising and growth is due to several factors, including the smaller business volume of international institutions in Spain, which allows them greater potential for growth, and the strong commitment which private banks have made since last year to international funds domiciled in for example, Luxembourg, as a way of diversifying against the risk of peripheral countries.

The gradual return of investors to mutual funds, encouraged by the improvement of the economic situation but also by the decision by the Bank of Spain of penalizing “extratipados” (extra high interest rate) deposits earlier this year, also explains the positive dynamics of international, as well as of the domestic CIIs. The fund management companies surveyed also point out the innovative supply of products, which is in line with market developments. By type of products, the fall of extratipos on deposits and on the Spanish risk premium has led investors towards absolute return funds or actively managed fixed income as the great alternative, as well as towards those which distribute income and dividends. Those institutions which are active in such funds, such as Deutsche Asset & Wealth Management, JP Morgan AM or Swiss & Global AM, are amongst those which are attracting more deposits (see table).

The leading management company in terms of new deposits was BlackRock, with Euro 885 million. “These results demonstrate the strength of our global platform which allows us to offer innovative solutions in any asset class, in any investment style or in any geographical region. Such flows also reflect greater investor confidence in the recovery of the global economy”, says Armando Senra, CEO of the aforementioned management company in Latin America and the Iberian Peninsula.

Trend Continuity

The question which follows the semester’s figures is whether this rate of growth in foreign CIIs marketed in Spain can be maintained. Some market sources believe that it will not remain the same in the coming months, due to the mark left by the falls in emerging market bond funds which had been set up as an alternative to conservative funds, and which will cause further rejection by investors in the coming months. Thus, some experts talk of a slowdown in inflows from here to the end of year, but are more optimistic regarding their evolution in the long term. “It is important for the industry to grow as a whole, both the domestic and international fund management companies, to avoid cannibalization preventing the sustainable growth of companies,” says an expert.

INTERNATIONAL ASSET MANAGERS WITH MORE INFLOWS IN SPAIN. Second Quarter 2013

Asset Manager

Net inflows (Euro million)

BlackRock Investment

885

Franklin Templeton Investments

716

JP Morgan AM

422

Swiss & Global AM

257

Deutsche Asset & Wealth Management

239

Source: Inverco. Estimates for June 30th, with data from 24 asset managers with Euro 45.5 billion in AUMs.

Wikimedia CommonsPhoto: Ikiwaner. The Effects of Rising Bond Yields on Markets

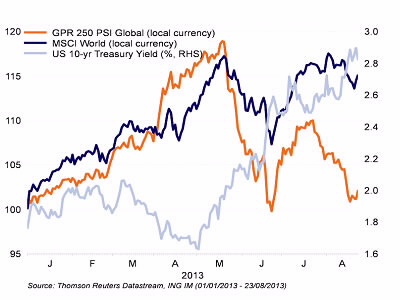

Investor risk appetite is getting depressed by the renewed rise in treasury yields in developed markets. In contrast to the correction in May/June, credit and commodity markets are holding up well. Real estate equities are having a hard time, while emerging market assets continue to struggle.

In this enviroment, ING Invesment Management scaled back their position in global real estate to neutral. Rising (real) interest rates in developed markets weigh relatively heavily on real estate equities as funding costs increase for this more leveraged asset class.

Real estate is very sensitive to the rise in treasury yields

Correction in equities, real estate and emerging markets

The renewed rise in government bond yields of developed markets has clearly started to weigh on investor risk appetite. With 10-year treasury yields in the US, UK and Germany increasing by 20 to 30 basis points in the past two weeks, especially equity and real estate markets have started to correct. The most probable reasons behind this are fears of an erosion of growth prospects and higher funding costs.

Also, emerging market (EM) assets have seen another round of downward pressure as higher US treasury yields further increased the risk of intensifying capital outflows. Especially emerging market currencies suffered last week, but also EM debt and equity markets underperformed their global peers.

Notable differences compared to last correction

At first sight, these dynamics look similar to the market evolution that occurred in late May and June. Some interesting differences are also visible below the surface, however. Most notable is the substantially higher resilience that is seen in credit and commodity markets. Both have hardly lost performance over the past two weeks, while they fell significantly during the May-June correction. Also, cyclical equity sectors are holding up quite well, while a notoriously “high beta” region like Europe is outperforming in equity space.

To view the complete story, click the attacehd document.

Foto: Mar del Este. ING vende su filial de seguros surcoreana por 1.650 millones de dólares a MBK Partners

ING announced this Monday that it has reached an agreement to sell ING Life Korea, its wholly owned life insurance business in South Korea, to MBK Partners for a total purchase price of approximately KRW 1.84 trillion (1.6 billion USD at current exchange rates). Under the terms of the agreement, ING will hold an indirect stake of approximately 10% in ING Life Korea for an amount of KRW 120 billion (106 million USD at current exchange rates).

ING has also reached a licensing agreement that will allow ING Life Korea to continue to operate under the ING brand for a maximum period of five years. In addition, over the course of one year, ING will continue to provide technical support and advice to ING Life Korea.

ING has made great strides in delivering on its programme to divest its insurance businesses as announced in 2009. Since then, ING has sold its insurance and investment management operations in Canada, Australia & New Zealand and Latin America, and a large portion of its insurance and investment management activities in Asia. In May 2013, ING’s U.S.-based retirement, investment and insurance business was successfully listed on the New York Stock Exchange, reducing ING’s stake to approximately 71%.

ING has accelerated preparations for the IPO of its European insurance and investment management businesses to be ready to go to market in 2014. The process to divest the remaining insurance and investment management businesses is on-going and any further announcements will be made if and when appropriate.

Transactions Details

MBK Partners is executing the transaction announced today through Life Investment, a private equity fund and will manage the investment in ING Life Korea for MBK Partners as well as for other investors in the fund. As part of the transaction, ING will hold an indirect stake of approximately 10% in ING Life Korea for an amount of KRW 120 billion (EUR 80 million at current exchange rates) which will be held by ING Insurance (ING Verzekeringen N.V.). As previously announced, the proceeds of the transaction will be used to further reduce the debt of ING Insurance.

The transaction announced today is subject to regulatory approvals and is expected to close in the fourth quarter of 2013. It does not impact ING’s Commercial Banking activities in South Korea.

Jeff Talpas. (Foto cedida por BBVA Compass). BBVA Compass pone a Jeff Talpas al frente de la nueva división de Wealth & Retail

BBVA Compass announced that William C. Helmshas been appointed vice chairman of the BBVA Compass board of directors.

Until now, Helms has led the bank’s Wealth Management business, overseeing private banking, asset management, international wealth management, broker-dealer activities and registered investment advisors.

“Bill brings a deep understanding of our strategic direction and will greatly enrich our board,” said Manolo Sanchez, BBVA U.S. country manager and president and CEO of BBVA Compass. “His leadership has helped us successfully implement our innovative, customer-focused business model across our growing U.S. footprint. We are fortunate to have his counsel.”

In addition to serving on the bank’s board of directors, Helms joins the board of BBVA Compass Bancshares, the bank’s holding company. He will be active in business development and in supporting the bank’s growth as directed by executive management. He also will oversee BBVA Compass’ national and local advisory boards and be involved in the bank’s government relations efforts.

Jeff Talpas, a member of the bank’s Management Committee who has overseen the bank’s Retail line of business, will lead the new combined Wealth & Retail Banking group. The move brings together all of the bank’s consumer segments in a single area led by Talpas, who has more than 25 years of experience in the financial services industry.

Helms joined Compass Bank in 2003 after serving in various leadership roles in the financial industry, including as co-president of Bank of America’s private bank. He serves on the Chancellor’s Council for the University of Texas System and as an advisory director for the McCombs School of Business at the University of Texas. He also serves on the board for the McGovern Museum of Health and Medical Science, and recently served on the boards of the Greater Houston Partnership, the Houston Grand Opera and the Museum of Fine Arts, Houston.

Wikimedia CommonsFoto: Dan SmithRdsmith4. Los grandes bancos centrales no tienen prisa por retirar los estímulos

The timeline set by the US Federal Reserve to reduce its monetary stimulus seems to be gradual enough and calls for the economy to grow strongly before exceptionally loose conditions are over. Nevertheless, the prospect of an end to such a liquidity boost as QE may increase volatility in financial markets until the first interest rate rise actually happens, probably next year, according to Pioneer Investments’ last Global Markets Strategy Report, published last Friday.

“We do not believe that the Fed will be forced to hurry up the process amid evidence of inflation in an uphill battle against the bond market vigilantes”, highlights the report. Pioneer Investment explains that in their strategy, they listened to central banks’ invitation to buy risky assets but have always given priority to risk control and their first assessment in this new scenario was to evaluate which markets stand to lose ground in the run-up to a normalized policy, which eventually includes higher interest rates

Most credit markets were strongly supported by QE-like policies which prompted a global search for additional yields. Although credit spreads did not fall as low as before the last recession, Pioneer has argued that many yield- seeking investors scooped up newly-issued bonds with scant concerns about the issuers’ credit standings. Downside risks in a post-QE world may also affect Emerging-Market bonds, not because of a lesser commitment to good fiscal policies but rather for the negative impact of dwindling investor flows(a concern shared by EM equities).

Equity prices are likely to be more resilient in the more challenging scenario, as valuations look overall cheap and dividend yields remain attractive, especially in Europe. Pioneer Investments’ upbeat view is conditional to a moderate rise in bond yields, which have risen quickly but from near-record lows. Emerging-market equities are another asset class whose performance may be undermined by the changed scenario, according to the report. Unlike high-yield corporate bonds, most emerging equity markets were not overly expensive in their view, but Pioneer Investment believes that most flows into them were spurred to a large extent by QE-like policies and may retreat somewhat. “Moreover, China has often been key for these markets’ overall performance and the uncertainty over the government’s policy action, namely, to curb excess bank lending, may keep concerns over an economic hard landing alive”.

Developed-market equities appear to be less affected by policy uncertainties and provide fair alternatives to Emerging Markets. “Japan has cheapened somewhat after the latest sell-off, whereas US equities may be prone to sharp corrections when bond yields rise significantly but tend to resume the uptrend when the bond market settles down”.

Foto: Martin St-Amant. El mercado laboral sigue mejorando en Wall Street, según una encuesta

A survey of MBA students and graduates from Training The Street(TTS), a leading corporate training provider for Wall Street firms and top-tier business schools, suggests that MBA candidates are receiving multiple offers as the banking industry continues to search for top talent. Offers are coming from the large bulge bracket banks as well as non-investment banking financial firms, such as consulting and private equity shops.

The fourth annual MBA employment survey from TTS also found that candidates are going on multiple interviews and receiving competitive job offers. Forty percent of those surveyed conducted between four and seven first-round interviews, 23% participated in one to three first-round interviews, 12% in eight to ten, and a surprising 19% participated in more than ten interviews. When asked about their satisfaction with their employment offers, 45% of respondents said they were “very satisfied,” with 32% answering “satisfied,” 15% “neutral,” and only 8% “dissatisfied.”

“The Wall Street hiring environment continues to improve, and investment banks in particular are willing to invest in top talent,” said Scott Rostan, Founder and CEO of TTS. “What’s also clear is that other financial and professional firms now feel the need to hire as well, and strong candidates have their choice of where they’d like to work. All of this suggests a significant shift from just a few years ago.”

The most aggressive recruiting came from large bulge bracket banks and consulting firms, with 48% and 35% of survey respondents stating those firms have been actively recruiting them, respectively. Boutique advisory firms/middle market banks were also heavily recruiting, with 27% of survey respondents stating such institutions have actively recruited them. Twenty-two percent said they had been approached by startups.

In terms of candidate sentiment, 22% of respondents said that large banks would be their top employment choice, while 19% would choose a consulting firm. Only 9% of those surveyed chose boutique advisory firms/middle market banks as their top choice, and just 5% selected startups as their top employment choice.

“Our results suggest what we’ve known anecdotally for a while, that not only has the Wall Street job market improved, but it continues to improve regularly,” added Mr. Rostan. “We know from our conversations with recruiting departments that many investment banks are now actively looking to hire more junior professionals as they see the need to expand their talent pools.”

Other findings from the survey include:

Optimism among candidates is high, with 48% reported feeling “very optimistic” about their job prospects after school and 41% as “somewhat optimistic.” Only 5% and 1% responded that they were “somewhat pessimistic” or “very pessimistic,” respectively.

On-campus recruiting was the most successful way for finding a job. Forty-eight percent found their job through on-campus interviews, while 22% found their job independently. 18% utilized personal references.

Forty-seven percent of respondents said they will be receiving a starting annualized base salary between $100,000-$125,000, 21% between $76,000-$99,000, and 22% between $50,000-$75,000.

Seventy-five percent of the survey respondents were male, and 78% were between the ages of 26 and 34.

Wikimedia CommonsPhoto: NASA. Modification: Eric Gaba. AXA Outlines Asian Ambitions and Changes Within Equity Teams

AXA Framlington, the fundamental equity business within AXA Investment Managers, announced its intention to grow its business in Asia and that senior portfolio manager Mark Tinker will relocate to Hong Kong as Head of AXA Framlington Asia.

Mark Tinker will move to Hong Kong in September to support the expansion of the AXA Framlington franchise in Asia. He will be working closely with the distribution teams in Asia to develop business in the region and will support the development of Asian equity capability.

As a result of the move, Mark Tinker will no longer manage the AXA Framlington Global Opportunities and its clone fund AXA WF Framlington Global Opportunities. The funds will be managed by the global sector team, led by Mark Hargraves and will be managed in line with the existing AXA WF Framlington Global. The fund drives returns through fundamental stock selection by sector from recommendations by the global sector team of 7 specialist fund managers with average experience of 18 years. The deputy manager on all three funds will be Susan Sternglass Noble.

The AXA WF Framlington Global High Income is now managed by William Howard. William has over 26 years’ experience in asset management and joined AXA Framlington in September 2012. Prior to this, William was Managing Director and Portfolio Manager at Goldman Sachs and an Executive Vice President at Templeton Investment. The deputy manager is Anne Tolmunen.