The behavior of the dollar since the beginning of the year and the uncertainty surrounding the market have led investors to analyze how the traditional safe-haven assets they turn to have changed and which is now the best option for their portfolios. Only financial advisors and asset managers can answer the latter question, but for the former we can find an interesting reflection in the Global Investment Returns Yearbook 2026, published by UBS, which analyzes 126 years of market performance.

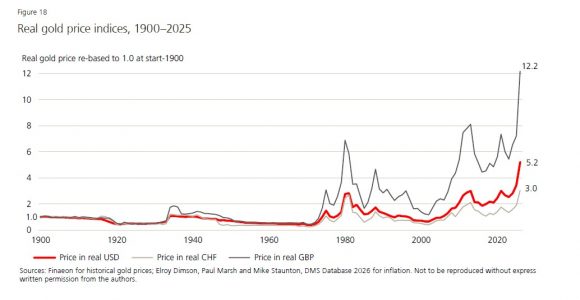

Undoubtedly, when discussing safe-haven assets, gold is first on investors’ list, as it is perceived as a clear hedge against inflation. However, according to the UBS report, the relationship between gold and inflation is weak. “Of the 28 years in which inflation exceeded 3%, we observe that gold returns were negative in 13 of them,” they note.

As shown in the chart above, gold has been more effective at outperforming inflation over the long term. “The red line indicates that, since 1900, the real price of gold in dollars has increased 5.2 times, which is equivalent to an annualized return of 1.3%. In the 54 years following Bretton Woods, gold’s annualized real returns were higher: 4.7% (U.S.), 5.8% (UK), and 4.3% (Switzerland),” the report notes.

Currency Hedging

Regarding currencies, investors have historically considered the U.S. dollar, the Swiss franc, and the Japanese yen to be the most reliable “safe havens.” However, over the past three months, a broad debate has emerged about whether the U.S. currency could lose this status. As a result, investors have paid more attention to how to hedge currencies.

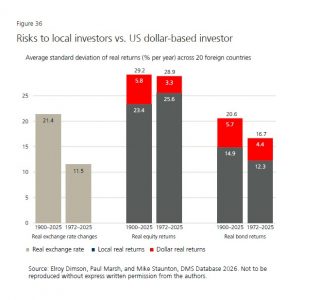

On this point, the UBS report notes that institutional investors tend to hedge at least part of their portfolios. “In general, non-U.S. (non-USD) investors tend to hedge more and with higher hedge ratios, and bond investors hedge more than equity investors,” the report states.

The question is whether such hedging is worthwhile. According to the report’s conclusions, on average, currency risk added around 6% to total risk, whether focusing on equities or bonds, although currency risk contributes proportionally more to the risk of bond portfolios. “This may explain the greater prevalence of hedging in fixed income portfolios,” UBS adds.

Which Risks Dominate?

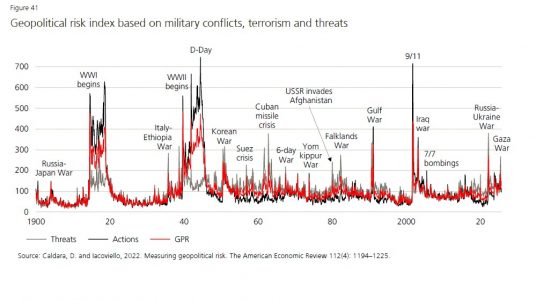

If we think about today’s markets, there is a clear consensus that geopolitics has become the main risk they face, but has this always been the case? According to the UBS report, the reality is that, historically, economic risks have outweighed geopolitical risks. “In many cases, investors would be right to ‘look beyond the noise’ of geopolitics. Using a simple regression of future global equity returns against an index of geopolitical threats, we find no relationship, whether looking one month ahead or one year ahead. However, geopolitical risk, whether related to armed conflicts or trade conflicts, clearly matters when extreme events occur with a significant economic impact on major nations. World War I, World War II, and the 1973–1974 oil shock were geopolitical events that led to three of the six worst episodes for major global equity markets since 1900,” the report concludes.

By Funds Society

By Funds Society