Pixabay CC0 Public Domain. Finletic lanza dos nuevos planes de pensiones

Finletic lanza dos nuevos planes de pensiones, uno de renta fija y otro de renta variable, que replican la estrategia de las carteras actuales, que es la inversión a nivel global de manera diversificada y eficiente en costes.

El primer vehículo, el International Equity Markets Plan de Pensiones tiene como objetivo replicar el comportamiento de la bolsa mundial. La comisión de gestión, que incluye la de administración y asesoramiento, es de un 0,45% anual.

Por su parte, el segundo plan, el International Bond Markets Plan de Pensiones, persigue replicar el mercado global de emisiones de renta fija. Su comisión de gestión será del 0,40%.

Ambos planes pueden contratarse de forma digital, ya sea por transferencia o por traspaso a Finletic desde cualquier plan que pueda tener el inversor en otras entidades. Estarán gestionados por Caser Pensiones, asesorados por Finletic y depositados en CecaBank.

Finletic, entidad presidida por Rafael Juan y Seva, es una fintech fundada en 2017 por Borja Durán y Jorge Coca (creadores de Wealth Solutions) junto con Daniel Giménez y Raúl Puente (fundadores de Trovit). Mediante la unión del mundo financiero con el tecnológico, tiene como objetivo ayudar a sus clientes a cumplir con sus objetivos a través de un “asesoramiento sencillo, transparente y de bajo coste”, aseguran desde la compañía.

Estos planes de pensiones son la continuación de su estrategia de servicio de gestión patrimonial combinando la experiencia de Wealth Solutions tras veinte años gestionando grandes familias e instituciones con una plataforma tecnológica pionera.

Pixabay CC0 Public Domain. Y en mitad de esta tormenta, ¿cómo esperan las gestoras que sea la recuperación?

Tras semanas hablando de cuáles han sido las medidas tomadas para frenar la actual crisis, cuáles las consecuencias económicas que dejará a nivel global y cómo será la paulatina vuelta a la normalidad, muchas gestoras comienzan a analizar cómo será también la recuperación cuando todo esto acabe.

Un pensamiento positivo, en parte impulsado por la evolución de la pandemia en Asia y en algunos países europeos, permite a los gestores valorar sus carteras y prepararse para el gestionar un futuro que todavía es incierto. En primero en preguntarse qué forma tendrá la recuperación ha sido Keith Wade, economista jefe de Schroders.

“La economía mundial se encuentra en mitad de un parón repentino. Toda la actividad se ha frenado por las medidas adoptadas por los gobiernos en virtud de contener la expansión del coronavirus. Teniendo en cuenta este contexto, hemos revisado nuestras previsiones y creemos que el PIB mundial experimentará una recesión severa en 2020, especialmente durante el segundo trimestre del año. Según nuestras previsiones, la contracción de la actividad mundial en 2020 de un 3% superará la observada durante el primer año de la crisis financiera de 2008, cuando el PIB mundial se contrajo en un 0,5%”, explica Wade.

Al igual que Wade son muchas las valoraciones que destaca que esta crisis es muy diferente a la de 2008, y por lo tanto la recuperación también lo será. “El fuerte rebote, o la recuperación en forma de V, está en duda. Los países que han adelantado la vuelta al trabajo han visto la aparición de nuevas olas de contagios y están teniendo que buscar un levantamiento gradual de las restricciones. Singapur, por ejemplo, ha registrado un nuevo fuerte aumento de los contagios. la presión para levantar los cierres más rápidamente se intensificará a medida que el daño económico se haga más evidente. Sin embargo, nuestra opinión es que la recuperación en forma de V es demasiado optimista y es probable que en nuestra próxima ronda de previsiones revisemos a la baja nuestras perspectivas de crecimiento mundial para 2020. La recuperación será más débil y se retrasará, adoptando una forma más cercana a la de una U. Sin embargo, la esperanza está en que con un levantamiento más gradual de las restricciones la economía mundial debería ser capaz de evitar una segunda ola significativa de contagios y la recesión de doble caída, o escenario en W», argumenta Wade.

Misma valoración comparte Esty Dwek, Head of Global Market Strategies de Natixis IM Solutions (Natixis Investment Managers), quien también ve una recuperación en forma de U. En este sentido, Dwek explica: “Los primeros datos de PMI de Estados Unidos no han sido tan malos como se esperaba, pero eso parece responder a la fecha en la que se realizó la encuesta y esperamos que los futuros datos reflejen un deterioro mayor de las condiciones económicas en EE.UU. Sabemos que los datos van a ser malos, la cuestión es cuánto de malos y durante cuánto tiempo. No esperamos una recuperación en V, sino en U y solo de manera gradual, por lo tanto, también anticipamos volatilidad y riesgos a la baja en el mercado. De momento, creemos que los bancos centrales han triunfado en mantener bajos los riesgos sistémicos para evitar una crisis de crédito, pero seguimos vigilando cómo podrán contenerse las suspensiones de pagos o quiebras de empresas si éstas se producen”.

Desde AXA IM, apoyan la teoría de la recuperación en forma de V, pero matizan: será una V muy alargada. En opinión de Gilles Moëc, Chief Group Economist AXA Investment Managers, «la recuperación mundial tendrá forma de V muy alargada, como el logotipo de Nike», y siempre «a partir del tercer trimestre». El experto considera que «el rebote será lento» porque, probablemente, «el gasto del consumidor se verá afectado por una mayor propensión a ahorrar y por los posibles frenos a la inversión». Así, señala que «el PIB mundial tendrá la forma del logotipo de Nike», un rebote swoosh que tendría lugar «a partir del tercer trimestre suponiendo siempre que la pandemia no se reactive» y no haya más bloqueos en el resto de trimestres del año.

Primeros rebotes

Ante la mejora que ha experimentado algunos índices bursátil, Stefan Hofrichter, economista global de Allianz Global Investors, es prudente a la hora de hablar de recuperación y prefiere centrarse en identificar los signos de rebote que los inversores deben tener en cuenta. Según Hofrichter, “a medida que continúa la crisis del coronavirus, estamos viendo señales de que este mercado bajista probablemente no ha tocado fondo. Si bien los inversores deben ser cautelosos, también deben buscar activamente evidencia de que podría estar llegando un rebote”.

Según el análisis que hace el experto de Allianz GI, los estímulos fiscales y monetarios masivos se encuentran entre las condiciones necesarias para que el mercado bajista toque fondo, pero no son suficientes. También deben existir otras condiciones, incluida una depresión en la dinámica cíclica y valoraciones atractivas.

“Debido a que los movimientos observados recientemente en los mercados corresponden a ventas rápidas según los estándares históricos, las perspectivas podrían volverse repentinamente más positivas, pero es probable que todavía no estemos ahí. Aunque, la reciente volatilidad ha creado oportunidades de inversión para inversores activos que utilizan un minucioso proceso bottom-up en renta variable o bonos”, apunta Hofrichteren su último informe.

Por este mismo tono de prudencia apuesta Guilhem Savry, Executive Director, Head of Macro and Dynamic Allocation de Unigestion, en su último informe. En él argumenta que apostar por una recuperación rápida de la economía es un peligroso porque se está subestimando dos elementos clave: “efectos indirectos” entre las economías y sus sectores, y la situación real de las pequeñas y medianas empresas.

Los economistas y los mercados esperan en torno a dos trimestres de contracción económica. Una de las razones que sustentan esta tesis tiene que ver con la duración que tendrá en el tiempo la recesión. El consenso y las valoraciones actuales en la renta variable anticipan una crisis breve, cercana a los dos trimestres, con un rápido retorno a la normalidad, durante el cuarto trimestre de 2020. Los estímulos fiscales sin precedentes, cuyos costes ascienden alrededor del 10% del PIB para la mayoría de los países involucrados, planificados para suavizar los efectos negativos, son un elemento importante que podría “apoyar el argumento de que se producirá una recuperación en forma de V o U”, expone Savry.

Con todo, desde Unigestion creen que apostar por una recuperación rápida es “peligroso”. Por un lado, los “efectos indirectos” entre las economías y sus sectores. Si el período mínimo de confinamiento es de seis semanas, pero hay una brecha de ocho semanas entre los primeros países en imponerlo y entre el último país afectado, esto aumenta significativamente el período de ineficiencia en la economía mundial centrada en el comercio y la movilidad de bienes y personas. De igual modo, las pequeñas empresas, la parte oculta dentro del iceberg, no están representadas en los índices globales de capital o crédito. Debido a que no tienen el mismo acceso a la financiación y están menos diversificadas que las grandes firmas, las pymes están más expuestas a la contención económica y al cierre. Así, Savry afirma que creen que “es prematuro anticipar una salida rápida de la crisis y que la economía volverá instantáneamente a su potencial”

Pixabay CC0 Public DomainMark Hargraves, responsable global de Framlington Equities de AXA IM. . AXA IM nombra a Mark Hargraves responsable global de Framlington Equities

AXA Investment Managers ha nombrado a Mark Hargraves responsable global de Framlington Equities y a Isabelle de Gavoty subdirectora de Framlington Equities. Según ha explicado la gestora, el nombramiento de Hargraves tendrá efecto inmediato y sustituirá a Matthew Lovatt, quien ha sido nombrado responsable global de clientes del Grupo.

Hargraves comenzará a trabajar desde este nuevo puesto reportando directamente a Hans Stoter, responsable global de AXA IM Core. Físicamente estará en las oficinas de la gestora en Londres y desde allí liderará el negocio global de Framlington Equities de AXA IM, que cuenta con oficinas en Londres, París, Tokio y Hong Kong. Además de sus nuevas responsabilidades, continuará siendo responsable de la gestión de carteras.

Respecto a Isabelle de Gavoty, también se incorporará a su cargo de subdirectora de Framlington Equities de forma inmediata. Como parte de su nuevo puesto, será la encargada de gestionar sus carteras. Estará ubicada en París y dependerá directamente de Mark Hargraves.

Framlington Equities es el negocio de renta variable activa, con un horizonte de inversión a largo plazo y basada en convicciones de AXA IM. Según recuerda la gestora, el objetivo de esta parte de su negocio es “ofrecer un exceso de rentabilidad consistente a través de una selección de acciones activa, fundamental y bottom-up” en sus carteras.

Pixabay CC0 Public Domain. iShares lanza una nueva gama de ETFs ESG con tres fondos de inversión por factores

iShares, perteneciente a BlackRock, amplía su gama de fondos cotizados (ETFs) con tres nuevos productos que combinan los criterios ambientales, sociales y de gobierno corporativo (ESG) con la creciente demanda de estrategias de mínima volatilidad basadas en factores. Según explican desde la gestora, este lanzamiento supone un hito en su objetivo por convertir la “sostenibilidad en un pilar a la hora de invertir”.

BlackRock considera que la inversión en estrategias basadas en criterios ESG y de mínima volatilidad sigue acelerándose a medida que las turbulencias de los mercados ponen a prueba la resiliencia de las carteras. Los flujos de entrada en ETFs sostenibles a escala mundial alcanzaron por sí solos los 14.800 millones de dólares en el primer trimestre de 2020, cifra que triplica con creces la del mismo periodo en 2019. Los clientes también han recurrido de forma creciente a las estrategias basadas en factores de iShares en busca de determinados catalizadores del riesgo y la rentabilidad en sus carteras. El de mínima volatilidad es un factor de estilo que ha destacado especialmente a la hora de limitar la exposición de los clientes a las caídas del mercado en periodos de volatilidad.

En los tres primeros meses de 2020, los ETFs iShares Edge MSCI Minimum Volatility UCITS han brindado a los clientes una rentabilidad superior media del 4% en comparación con los índices a los que estaban vinculados asumiendo una menor exposición a las caídas y, al mismo tiempo, ayudándoles a captar buena parte del repunte del mercado. Este enfoque defensivo ha contribuido a que el ETF iShares UCITS Minimum Volatility atrajese activos por valor de 800 millones de dólares en el primer trimestre de 2020, que se suman a los 1.300 millones de dólares captados en 2019.

Según explica la gestora, al combinar el liderazgo de BlackRock en la inversión por factores con la creciente demanda de estrategias ESG, los nuevos fondos de iShares están concebidos para brindar un perfil ESG perfeccionado y una exposición reducida al carbono, al tiempo que obtienen unas rentabilidades similares a las del mercado asumiendo menos riesgo. Los tres fondos están indexados a los índices MSCI Minimum Volatility ESG Reduced Carbon Target. Estos lanzamientos amplían la oferta de ETFs y fondos indexados centrados en la sostenibilidad de iShares hasta un total de más de 100 productos

Los tres nuevos productos son:

ETF iShares EDGE MSCI World Minimum Volatility ESG UCITS (MVEW): este fondo brinda una exposición diversificada a una amplia gama de empresas del universo desarrollado con una exposición al mercado internacional y un perfil de volatilidad inferior. Cuenta con una ratio de gastos totales (en inglés, TER) del 0,30% y constituye la alternativa ESG al ETF iShares EDGE MSCI World Minimum Volatility UCITS (MVOL).

ETF iShares EDGE MSCI Europe Minimum Volatility ESG UCITS (MVEE): se trata de la alternativa ESG al ETF iShares EDGE MSCI Europe Minimum Volatility UCITS (MVEU). El fondo se centra en tener una exposición diversificada a empresas europeas con un perfil de volatilidad inferior y una TER del 0,25%.

ETF iShares EDGE MSCI USA Minimum Volatility ESG UCITS (MVEA): brinda una exposición diversificada a empresas estadounidenses con un perfil de volatilidad inferior en comparación con el mercado bursátil estadounidense en su conjunto. Cuenta con una TER del 0,20% y constituye la alternativa ESG al ETF iShares Edge S&P 500 Minimum Volatility UCITS (SPMV).

A raíz de este lanzamiento, Stephen Cohen, responsable de iShares para la región EMEA en BlackRock, ha declarado: “En un momento en que los inversores están haciendo balance de su posicionamiento táctico y estratégico, los ETFs están desempeñando un papel fundamental en unas carteras cada vez más orientadas a los criterios ESG. Hemos observado un crecimiento récord en nuestra gama sostenible y seguimos concentrados en estructurar la oferta más exhaustiva e innovadora de ETFs que siguen criterios ESG para satisfacer las necesidades de los inversores y anticiparnos a estas”.

Por su parte, Philipp Hildebrand, vicepresidente de BlackRock,ha señalado que “la marcada reasignación de activos a estrategias de inversión sostenibles ya ha comenzado y no hará sino acelerarse. La resiliencia que muestran las rentabilidades de las estrategias sostenibles en el actual contexto de turbulencias en los mercados mediante la consecución de mejores resultados en las carteras es destacable e impulsará aún más la demanda de componentes sostenibles. Los productos indexados están permitiendo una integración a gran escala de criterios sostenibles en las carteras de las gestoras patrimoniales e inversores institucionales de todo el mundo, y este es solo el comienzo”

Pixabay CC0 Public DomainMarc Syz, CEO de SYZ Capital.. SYZ Capital fusiona los equipos de SYZ Asset Management Alternatives y SYZ Private Banking Global Investment Solutions

SYZ Capital, boutique de inversión en mercados de capital privado, ha decidido centralizar la experiencia de inversión alternativa de todo el Grupo SYZ. Para ello, ha fusionado los equipos de SYZ Asset Management Alternatives y SYZ Private Banking Global Investment Solutions.

Según ha explicado la firma, con este movimiento pretende ampliar su oferta en inversiones alternativas y convertirse en un “centro global de experiencia”, para crear una “propuesta líder” e “innovadora” para estrategias líquidas e ilíquidas. En cierto modo, la firma se afianza en sus orígenes, ya que fue creada como para invertir en mercados de capital privado, capital riesgo directo, fondos temáticos y fondos multigestor. Y, según explican, para acercar a los inversores, junto con la familia Syz, oportunidades que tradicionalmente solo estaban disponibles para los inversores institucionales.

Desde SYZ Capital explica que, con el objetivo de cumplir las siempre exigencias de los inversores y aprovechar las oportunidades disponibles en los mercados mundiales, incorporará a partir de ahora la experiencia en inversiones alternativas líquidas y hedge funds, anteriormente disponibles en SYZ Private Banking y SYZ Asset Management, y representará un total de 1000 millones de francos suizos de activos bajo gestión.

Sherban Tautu, Head of Global Investment Solutions (GIS), y sus equipos dedicados a la gestión discrecional y asesoramiento de inversión alternativa, que antes formaban parte de SYZ Private Banking, se unirán a SYZ Capital. Según matiza la firma, “la continuidad en las carteras de los clientes estará garantizada, ya que serán gestionadas por el mismo equipo de gestores expertos”.

Por su parte, Cédric Vuignier, responsable de análisis e inversiones alternativos en SYZ Asset Management, y su equipo también se unen a SYZ Capital, donde seguirán gestionando el fondo OYSTER Alternative Uncorrelated y el OYSTER Alternative Multi Strategy, así como la gama UCITS Alternative White Label.

Según explican, esta expansión es fruto del creciente apetito por las inversiones alternativas y la dinámica cambiante de inversión. A raíz de este anuncio, Eric Syz, CEO del Grupo SYZ, ha señalado que “las estrategias long-only están cada vez más estandarizadas, por lo que las inversiones alternativas son el futuro de los gestores activos. En los últimos años, los inversores como nosotros han buscado cada vez más fuentes de diversificación, distintas de las tradicionales renta variable y renta fija, pues los mercados han mostrado una dinámica de fase tardía del ciclo. La fuerte volatilidad de mercado que estamos presenciando como resultado de actual crisis del coronavirus que estamos sufriendo, provocará que estas estrategias sean todavía más populares”.

Respecto a la situación actual, el CEO de la firma considera esta pandemia es un acontecimiento de tipo “cisne negro”, que ha puesto fin de manera abrupta a la direccionalidad del mercado. “El regreso de la volatilidad obligará a los inversores a adoptar estrategias de mitigación de riesgos más sólidas, con una protección frente a caídas, y que aumente la demanda de diversificación a través de activos alternativos. En nuestra opinión, los inversores deberían contar con una exposición del 20%-30% de su cartera a este tipo de activos. Actualmente, estamos totalmente preparados para ayudar a los inversores a conseguir este objetivo en el segmento de la liquidez durante los próximos años”, afirma.

Impacto de la sinergia

Asimismo, el Grupo cree que los países desarrollados se dirigían a una situación parecida a la de Japón, con una ralentización prolongada del crecimiento, lo que ha provocado que muchos inversores busquen fuentes alternativas de rentabilidades sólidas y de riesgo ajustado.

Marc Syz, CEO de SYZ Capital, señala: “La familia de Syz lleva más de 35 años invirtiendo en activos alternativos, por lo que forman parte de nuestro ADN. Nuestro objetivo es democratizar el acceso a este tipo de inversiones y brindar sus beneficios a un universo de inversores mucho mayor, especialmente a nuestros clientes, que comparten los valores del Grupo y el espíritu emprendedor. La fusión de nuestras ofertas líquidas e ilíquidas permitirá a nuestros clientes acceder y beneficiarse de una amplia gama de soluciones de inversión interesantes junto a nuestra familia. Las inversiones alternativas ayudarán a los inversores a capear este difícil entorno con un mercado altamente volátil y, al mismo tiempo, les permitirá descubrir fuentes no correlacionadas de alfa consistente. Los instrumentos alternativos líquidos, como los fondos de inversión libre, son conocidos por su correlación reducida con las clases de activos tradicionales, lo que les permite generar rentabilidades interesantes en los ciclos de mercado con bajos niveles de volatilidad. Gracias a nuestras relaciones y redes históricas, somos capaces de aprovechar las oportunidades de rentabilidad únicas en este segmento”.

Syz explica que la firma está lista para respuesta a las necesidades de los inversores. “En cuanto a la oferta ilíquida, nuestra experiencia nos permite identificar situaciones en las que se pueden generar rentabilidades ajustadas al riesgo considerables mediante los desequilibrios estructurales, la información clave o el acceso único al mercado. Invertimos de manera activa en una amplia gama de estrategias sobresalientes de capital riesgo, situaciones especiales y estrategias no correlacionadas. Al agrupar ambos equipos en una única sociedad de inversión, SYZ Capital, podremos generar más ideas de inversión de calidad y más opciones de gestión de carteras”, sostiene.

Por último apunta que la demanda de activos alternativos está creciendo y quieren formar parte de ello. “Aunar la experiencia y los conocimientos sobre la inversión líquida e ilíquida en un centro de excelencia permitirá al Grupo SYZ seguir innovando y brindando soluciones de inversión seleccionadas durante la próxima década”, concluye

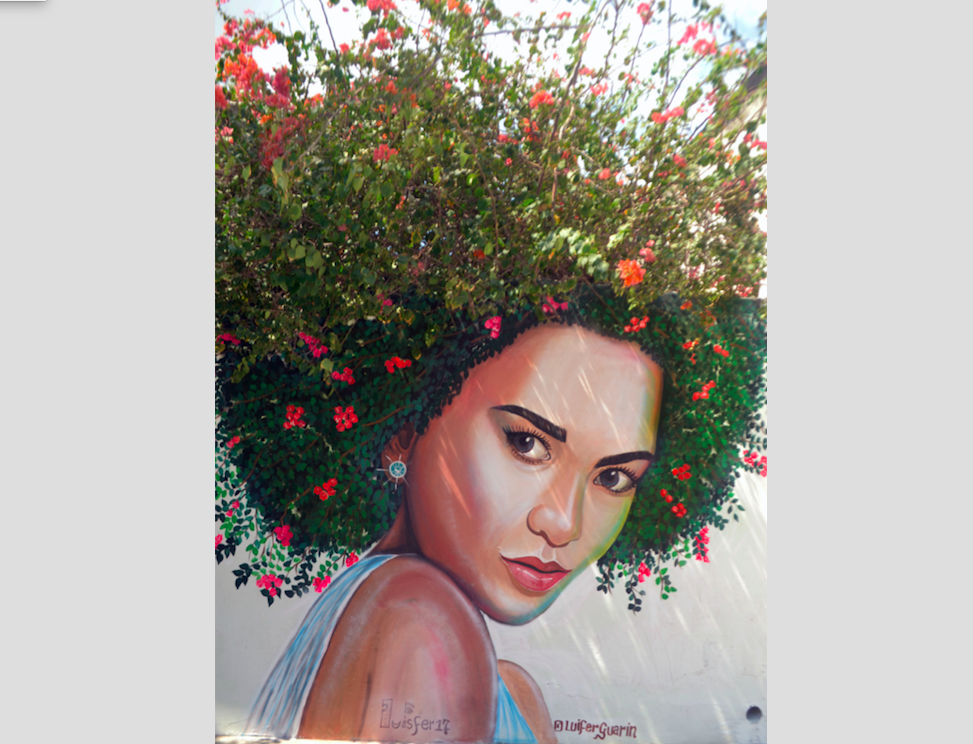

Pixabay CC0 Public Domain. Luis Guarín Molina, ganador del concurso Art on Climate de Allianz Global Investors

Allianz Global Investors ha otorgado el premio del concurso internacional de ilustración Art On Climate al artista colombiano Luis Guarín Molina. Art On Climate es un concurso diseñado para ayudar a crear conciencia sobre la importancia del cambio climático y la necesidad de encontrar soluciones que puedan contribuir a alcanzar un futuro más sostenible.

El concurso Art On Climate es una iniciativa de Allianz Global Investors en España, con el apoyo de Imartgine que ha aportado su experiencia en el ámbito cultural. El concurso fue convocado en 2019 y, desde entonces, 446 artistas de 69 países, incluyendo 155 de España, han contribuido con 920 obras originales. La selección de las obras ha corrido a cargo de un Jurado Calificador, presidido por Beatrix Anton-Groenemeyer, Responsable de Sostenibilidad de Allianz Global Investors, con la participación de Joaquín Garralda, presidente de Spainsif, y de un grupo de expertos de reconocido prestigio en el mundo de la ilustración como Aurora Solano Pérez, Anne Derenne, René León Sánchez y Jean-François Sauré, director de imartgine.com, en calidad de secretario. Además de la obra ganadora, fueron elegidas como finalistas las ilustraciones de Agustín Gagliano (Argentina), Sebastián Govino (Argentina) y Aleksandra Herman (Polonia).

Como gestora activa, Allianz Global Investors busca influir y facilitar el cambio hacia una economía baja en carbono, tanto a través de sus decisiones de inversión como de su comportamiento corporativo. El concurso Art On Climate busca promover, mediante el arte, la reflexión en torno a la necesidad de luchar contra el cambio climático y de impulsar un modelo de desarrollo sostenible.

“En Allianz Global Investors trabajamos para mejorar y aumentar la sostenibilidad de nuestras inversiones, colaborando con empresas para ayudarlas a desarrollar negocios más sostenibles. Creemos en un futuro mejor para todos nosotros y en compartir la responsabilidad de hacerlo realidad. Y esto se conecta con el arte. Encontramos que los artistas tienen una visión muy especial, poco común y única sobre las cosas, el mundo y la sociedad. Tienen la capacidad de aportar una mirada refrescante y, como la mayoría de las obras de arte que participan en este concurso, en su mayoría optimistas, se esfuerzan en promover un mundo mejor”, ha señalado Beatrix Anton-Groenemeyer.

Por su parte, Joaquín Garralda apunta que “en la actual emergencia sanitaria del COVID-19, puede parecer que la pandemia ha quitado relevancia a la preocupación por la ‘emergencia climática’ y que esto seguirá así durante cierto tiempo, aun cuando la situación se normalice. Sin embargo, puede ser un factor que acelere la exigencia social a los líderes políticos para que afronten más coordinadamente los problemas globales. Desde el punto de vista del empleo, la gran preocupación actual, la transición hacia una economía baja en carbono se presenta como una importante fuente de generación de empleo. Por ello no son emergencias que se sustituyen una a la otra, sino que pueden ser muy complementarias. En este sentido, el poder de las imágenes tiene un papel muy relevante y este concurso es una buena muestra de ello. La creatividad y sensibilidad de las imágenes que han concursado hace más difícil no considerar el tema climático con la relevancia y urgencia que se necesita”.

Con el objetivo de compartir cómo los artistas participantes ven y piensan sobre el cambio climático, Allianz Global Investors creará el Museo Virtual “Art On Climate”, donde se podrá disfrutar de una selección de las mejores obras, incluidas las del ganador y los finalistas.

La obra ganadora, del artista colombiano Luis Guarín Molina es un retrato de una mujer en el que su pelo se transforma en una abundante melena de hierba verde salpicada de flores rojas. Sobre ella, el autor comentó: “Con esta obra he querido mostrar que no hay división entre nosotros y la naturaleza, que en realidad estamos mucho más unidos a ella de lo que creemos, y es esta unión la que permitirá que la tierra tenga un mejor futuro. Estoy muy agradecido de haber recibido este premio y de poder contribuir a generar conciencia de la importancia de la sostenibilidad y la conservación de nuestro planeta para futuras generaciones”.

Por su parte, Marisa Aguilar, Directora General para España de Allianz Global Investors, añade: “El arte es una herramienta de comunicación muy poderosa y estamos convencidos de que puede contribuir a amplificar el impacto de la necesaria concienciación sobre el cambio climático. Por ello agradecemos enormemente la participación de tantos artistas en esta iniciativa, y desde Allianz Global Investors nos comprometemos a seguir haciendo esfuerzos por conseguir un crecimiento económico y social más sostenibles, ahora más que nunca».

Foto cedida. Juan Pablo Hernández, socio de HMC Capital: “Esta crisis encontró relativamente bien parado al sector inmobiliario”

Juan Pablo Hernández, socio y gerente Activos Reales de HMC Capital, analizó las consecuencias del Covid-19 y expectativas en el mercado inmobiliario nacional, en una nueva edición del programa live streaming “Visión de Líderes” de Itaú, el cual se transmite a través del canal de YouTube Itaú Chile.

El ejecutivo se refirió a los impactos sucesivos que ha tenido la pandemia en el sector inmobiliario, y el panorama de incertidumbre que enfrenta hoy. Afirmó que “cada subsector de la industria se comportará según su riesgo. La hotelería, sin duda, será la más afectada por sus importantes costos operativos, sumado a que ya venía afectada desde octubre”.

A juicio de Hernández el sector de los centros comerciales también podría verse afectado de manera “significativa”, considerando el efecto que en el largo plazo pueda provocar la presión del e-commerce.

“Las bodegas de logística destinadas al e-commerce serán el subsector más beneficiado en esta crisis y, probablemente en el largo plazo se mantendrá en bonanza, porque se transformará en un hábito”, destacó.

El socio de HMC Capital indicó que lo que menos ha caído ha sido la renta residencial. Respecto al stock, manifestó que esta crisis encontró mejor parado al sector inmobiliario que la de 2008, cuando había 18.000 unidades disponibles en Santiago, y hoy hay 2.000.

Así, Hernández detalló que a la hora de pensar en un portafolio inmobiliario, es importante mantener diversificación geográfica en las inversiones. A su parecer, la deuda inmobiliaria debe ser uno de los componentes importantes dentro del portafolio debido al atractivo componente de riesgo retorno de la inversión. En cuanto a la renta residencial, explicó que prefiere la exposición a Estados Unidos. A esto, el ejecutivo explicó que sería interesante evaluar inversiones más tradicionales para tener exposición a centros comerciales.

El socio de HMC Capital afirmó que la crisis actual será más grande a la de 2008, al afectar de manera transversal a la economía, “pero no debiera haber una presión importante en la baja de los precios de la industria”.

“Visión de líderes” es un programa de conversación en vivo de Banco Itaú, transmitido por el canal de Youtube Itaú Chile, con el fin de proveer de información de valor para la sociedad.

Foto cedida. XP Investimentos: “Tenemos previsto cerrar entre 6 y 10 acuerdos con gestoras internacionales en 2020”

Los inversores brasileños han estado tradicionalmente orientados hacia mercados domésticos, entre otros motivos, por los altos retornos que ofrecían los activos locales de renta fija. La fuerte bajada de los tipos de interés desde el 14,25% en julio 2015 hasta el actual 3,75%, y la evidencia de la necesidad de una mayor diversificación por la frágil situación de la economía brasileña han obligado al inversor local a mirar más allá de sus fronteras.

Así lo confirma Fabiano Cintra, CAIA, International Relationship Manager de XP Investimentos, en una entrevista concedida a Funds Society tras la reciente firma de dos nuevos acuerdo de distribución en exclusiva con las gestoras Wellington Managementy AXA IM. “El inversor local se ha dado cuenta que necesita nuevas fuentes de retornos no correlacionadas entre ellas”, confirma.

Desde que se inició el proceso a la baja de los tipos de interés, el inversor local ha migrado de los mercados de renta fija hacia mercados de renta variable locales y hedge funds (conocidos locamente como multiproducto). Sin embargo, Cintra puntualiza que la poca profundidad de los mercados brasileños hace que la correlación entre empresas brasileñas sea alta y se agudice la necesidad de una mayor diversificación internacional. “Es como pescar desde una misma barca en un rio poco profundo”, señala.

Además, la actual coyuntura macroeconómica tras el COVID-19 hace que lograr una mayor diversificación de cartera apremie. “Hay economías que han sido más resilentes y que saldrán de esta crisis antes que otras y el inversor necesita invertir ahí, ahora, es el momento”, explica Cintra. A modo de oportunidades de inversión cita como ejemplo el reinicio de la actividad en China, Nueva Zelanda o Alemania o sectores como el tecnológico en Estados Unidos y el farmacéutico en Suiza.

Aceleración nuevos acuerdos para 2020: interés por mercados emergentes

Por este motivo, y con el objetivo de actuar como puente entre el inversor brasileño y las mejores gestoras del mundo, desde XP Investimentos están trabajando intensamente para poder ampliar su gama de productos lo más pronto posible.

Así, Cintra confirma que están trabajando en la firma de nuevos acuerdos con gestores internacionales y que esperan cerrar entre 6 y 10 nuevos acuerdos antes de que finalice el año. Aunque no descartan del todo incluir gestoras boutiques, muestran preferencia por gestoras internacionales con suficiente tamaño, track record, expertise en la gestión y procesos de inversión robustos de la talla de Aberdeen Standard, Morgan Stanley, Wellington Management y AXA IM con los que ya trabajan en exclusiva.

“Estamos liderando el proceso de ofrecer productos internacionales en exclusiva a inversores brasileños”, confirma Cintra. Esta iniciativa completa la estrategia de plataforma digital que comenzó ofreciendo fondos locales a través de un modelo de arquitectura abierta y que posteriormente completó con fondos extranjeros de gestoras que ya tenían presencia en el mercado local tales como BlackRock, PIMCO, JP Morgan, Franklin Templeton o Legg Mason.

En cuanto al apetito del inversor brasileño por distintas categorías de activo, el ejecutivo confirma que hay interés por estrategia globales y regionales, muy especialmente en mercados emergentes, que guiaran la firma de sus futuros acuerdos.

Flexibilización en la regulación

Con respecto a cómo la legislación brasileña se está adaptando a esta nueva necesidad de diversificación internacional, Cintra explica que los limites se han suavizado en el último año hasta más de doble. En concreto, el límite para los fondos de pensiones se ha ampliado del 10% a 20%, el aplicable a inversores cualificados del 20 al 40% y se aumentado el limite para la inversión en BRDS (Brazilian Depositary Receipts por sus silgas en inglés) de empresas internacionales que cotizan en la bolsa brasileña. En esta línea, muchos de los fondos de pensiones, fondos de mutuos e inversores cualificados ya han o están modificando sus políticas de inversión para dar cabida a esta mayor exposición internacional.

No obstante, los fondos que invierten más del 67% en activos extranjeros solo pueden ser distribuidos entre inversores cualificados, es decir, personas físicas o jurídicas con más de un millón de reales de patrimonio (180.000 dólares aproximadamente), limitación a los que están sujetos muchos, aunque no todos, los fondos internacionales que ofrece XP Investimentos.

Sin embargo, y en su afán de democratizar la inversión, el ticket mínimo establecido suele ser muy bajo para así facilitar el acceso a los productos internacionales. “Queremos ofrecer a los brasileños lo mejor del mundo” afirma Cintra.

Reciente incorporación de estrategias de Wellington Management y AXA IM

XP Investimentos ha anunciado dos nuevos acuerdos en exclusiva con dos grandes gestoras internacionales, Wellington Management y AXA IM, con muy pocos días de diferencia, lo que demuestra una vez más el aumento de la demanda del inversor brasileño por productos internacionales.

Gracias a su acuerdo con Wellington Management, XP Investimentos comenzará a distribuir el fondo local (feeder funds) Wellington Ventura que invierte en la estrategia global de acciones de Wellington, y que estará disponible tanto en dólares como en reales brasileños, para inversores locales calificados a partir de un importe mínimo 5.000 reales (900 dólares aproximadamente).

Este acuerdo, anunciado a finales del mes de abril, ha tenido excelentes resultados habiendo captado en pocos días cerca de 300 millones de reales (53 millones de dólares) desde su puesta en funcionamiento.

Por otra parte, el acuerdo con AXA IM fue anunciado el pasado 6 de mayo y gracias al cual XP pone a disposición de inversores cualificados e institucionales domiciliados en Brasil estrategias de AXA IM innovadoras de global equity y high yield con foco en la economía digital. En concreto, los fondos feeder invierten en las siguientes estrategias: AXA IM US High Yield Bonds, AXA IM Framlington Digital Economy y AXA IM Framlington Robotechy estarán disponibles en reales brasileños para mitigar los efectos del tipo de cambio.

SURA Asset Management México ha elegido a Emilio Bertrán Rodríguez como director general de Afore SURA, reportando directamente a Enrique Solórzano, CEO de SURA Asset Management México.

De acuerdo con la institución, «el nombramiento será ratificado por el Consejo de Administración próximamente. Esta designación se da en sustitución de Luis Armando Kuri, a quien deseamos el mayor de los éxitos. Entre sus principales responsabilidades, Bertrán, se encargará de continuar entregando el mayor valor al cliente en términos de asesoría pensional, los mejores rendimientos, y seguir desarrollando servicios que han distinguido a SURA como la Afore #1 en servicio en la industria por cuatro años consecutivos, según la Consar».

Sobre el nombramiento, Enrique Solórzano mencionó: “Me complace profundamente que un ejecutivo de nuestra cantera asuma la responsabilidad del negocio más grande de SURA en México; esto reafirma la calidad de nuestro talento y la convicción de nuestra empresa por desarrollarlo”.

Bertrán Rodríguez, con más de 20 años de experiencia en el sector financiero, trabaja en SURA desde hace 10 años y ha desempeñado diferentes responsabilidades clave para el negocio. Fue director de Inversiones y Asset Allocation, dirigió el proyecto para renovar la plataforma de inversión de la Afore, y también fue director de Riesgos. Su más reciente responsabilidad era la Dirección Ejecutiva de Finanzas y Riesgos de la Compañía.

Previamente, la experiencia profesional de Emilio Bertrán incluyó al Banco de México, donde trabajó en Investigación Económica y Operaciones de Banca Central de la institución. También colaboró en Petróleos Mexicanos en temas relacionados con riesgos y finanzas. En Afore XXI fue subdirector de Inversiones.

Bertrán Rodríguez es licenciado en Economía y maestro en Finanzas por el Instituto Tecnológico y de Estudios Superiores de Monterrey. También fue catedrático de Finanzas Internacionales en esa institución durante 6 años.

Foto cedidaFernando de Calzada, banquero senior de Pictet WM.. Pictet WM amplía su equipo de banqueros senior en Madrid con Fernando de Calzada

Pictet WM ha anunciado la incorporación de Fernando de Calzada a su equipo de banqueros senior. Según ha explicado la firma, Calzada cuenta con más de 20 años de experiencia en el sector financiero, que incluyen la gestión de carteras en UBS SGIIC, el análisis de renta variable de compañías europeas en Santander SVB y, desde 2005, el asesoramiento financiero de grandes patrimonios en Credit Suisse.

Para Luis Sánchez de Lamadrid, director general de Pictet WM en España, esta nueva incorporación confirma la estrategia de crecimiento del área de Wealth Management de Pictet en España. El fichaje de Fernando de Calzada se suma a la incorporación de Diego Cavero recientemente, así como a la creación de un Comité Asesor de cuatro expertos con amplia experiencia en el sector empresarial. De hecho, la nueva oficina de Madrid de Pictet & Cie en España se inauguró a comienzos de 2019 en el barrio de Salamanca con mayores prestaciones, tanto para empleados como para clientes. Oficina que se suma a la que ya tiene en Barcelona.

“Las incorporaciones de Fernando de Calzada y Diego Cavero como banqueros senior, complementan nuestro compromiso con la captación de talento para establecer relaciones responsables con nuestros clientes con el fin de proteger, desarrollar y transmitir sus patrimonios”, ha señalado Sánchez de Lamadrid.