Pixabay CC0 Public Domain. The Road to an Effective Collateral Management Program

iCapital and Boreal Capital Management AG (Zurich) and Boreal Capital Management LLC (Miami), subsidiaries of the MoraBanc Group, have announced in a statement a global collaboration aimed at expanding cross-border investment solutions. This alliance builds on the successful use of iCapital’s Marketplace by Boreal Miami since 2021 and now includes Boreal Zurich’s access to Luxembourg-domiciled funds for qualified Swiss investors.

This expansion is especially relevant for Latin America, where Boreal Miami serves a growing base of private clients and family offices seeking diversified, institutional-quality investment opportunities. The alliance underscores both firms’ commitment to transparency, innovation, and client-centric wealth management.

We believe this story will resonate with your audience, particularly given the increasing demand for access to sophisticated investments in Latin America. I would be happy to arrange interviews with executives from iCapital or Boreal, or provide additional information.

“This agreement represents a key strategic step in our commitment to offering our clients access to top-tier alternative investment solutions, always with the highest level of transparency and regulatory rigor,” stated Joaquín Francés, CEO of Boreal Capital Management LLC.

“We are pleased to expand our relationship with iCapital, a step that will further strengthen our global offering and enable us to continue providing our clients with access to high-quality investment opportunities,” added Jaime Moreno, CEO of Boreal Capital Management AG.

“We are excited to deepen our relationship with Boreal Capital Management and support their global expansion into alternatives,” stated Wes Sturdevant, Head of International Client Solutions for the Americas at iCapital.

With over $4 billion in assets under management and a team representing fifteen nationalities and ten languages, Boreal offers a unique combination of global reach and local expertise. iCapital, for its part, manages $232 billion in alternative platform assets and provides AI-driven solutions that streamline the investment lifecycle—from onboarding and regulatory compliance to reporting and portfolio integration.

Brazilian investors are no longer asking whether to invest in dollars, according to Fabiano Cintra, Director of Investment Fund Analysis at XP. They have moved past that stage and are now asking how much they should invest and how to allocate those resources.

This statement, made in an interview with Funds Society during XP Expert 2025, reflects the new developments at the renowned Brazilian platform and the growing interest in offshore assets.

According to Cintra, XP is moving aggressively into Miami, seeking new funds and expanding its staff on Brickell Avenue, where a unit of XP International is located.

International Allocation Doubles in Dollars

“We have doubled our allocation to international funds since the beginning of the year,” says Cintra, referring to U.S. operations observed on the company’s platform, which also shows a growing number of openings of XP global accounts that provide access to these assets.

According to Cintra, Brazilians are not just converting their reais to dollars, but also looking to invest in international funds, despite the fact that the local interest rate remains high. “If the CDI is so good, why don’t foreign investors bring their money here and invest in our fixed income? Because they think in dollars. The CDI’s return in dollars over the past 10 years was 40%, which represents less than 4% per year,” he states.

Seeking New Funds

Today, with 10 international asset managers and just over 100 funds, XP continues to look for more players and assets for its clients. “We want to increase the number of funds by at least 30% by the end of this year,” says Cintra.

“We’re exploring all asset classes—not just equities, but also fixed income and the trending topic, structured credit,” says Cintra, who adds that this asset class has seen strong demand both in Brazil and globally. “With Treasury bonds above 4%, there are credit spreads and you can find mandates offering returns of dollar +7%… dollar +8%. Clients are seeking an attractive credit premium in the currency.”

The U.S. Securities and Exchange Commission (SEC) voted in favor of approving orders that allow authorized participants to create and redeem shares of cryptoasset exchange-traded products (ETPs) in kind, according to a statement from the institution.

According to the SEC, this represents a shift from the recently approved spot bitcoin and ether ETPs, which were limited to cash creation and redemption. Now, bitcoin and ether ETPs, like other commodity-based ETPs approved by the Commission, will be able to create and redeem shares in kind.

“It is a new day at the SEC, and a key priority of my chairmanship is to develop an appropriate regulatory framework for the cryptoasset markets,” declared SEC chairman Paul S. Atkins.

“I am pleased that the Commission has approved these orders allowing in-kind creation and redemption of a range of cryptoasset ETPs. Investors will benefit from these approvals, as they will make these products less expensive and more efficient,” he added.

For the SEC, these changes “continue building a rational regulatory framework for cryptocurrencies, leading to a deeper and more dynamic market that will benefit all U.S. investors. This decision aligns with standard practices for similar ETPs.”

Jamie Selway, Director of the Division of Trading and Markets, stated: “Today’s decision by the Commission marks a significant step forward for the growing market of cryptocurrency-based ETPs. In-kind creation and redemption provide flexibility and cost savings to ETP issuers, authorized participants, and investors, resulting in a more efficient market.”

The Commission also voted to approve other orders promoting a merit-neutral approach to cryptocurrency-based products, including exchange applications seeking to list and trade an ETP containing a combination of spot bitcoin and ether, options on certain spot bitcoin ETPs, Flexible Exchange (FLEX) options on shares of certain BTC-based ETPs, and an increase in position limits up to the generic limits for options (up to 250,000 contracts) for listed options on certain BTC ETPs.

In addition, the Commission issued two scheduling orders requesting comments for or against approval by the Division of Trading and Markets, under delegated authority, of proposals by a national securities exchange to list and trade two large-cap cryptocurrency-based ETPs.

Alejandro Gambirazio and Jesús Urrutia, former J.P. Morgan bankers, have officially launched Centrica, a new independent firm registered as an Investment Adviser (RIA). After more than a decade at J.P. Morgan, the founders left the firm in April to pursue a more entrepreneurial and client-centered approach to wealth management.

Centrica already manages approximately $500 million in client assets and offers personalized wealth advisory and investment services to clients in Latin America and the United States. With offices in Miami, the group seeks to expand its presence in Latin America and plans to open offices in Lima and Mexico City. According to the founders, the firm positions itself as a trusted partner for families, entrepreneurs, and institutions seeking personalized financial strategies with global execution capabilities.

The founders bring over 40 years of combined industry experience, with a proven track record of excellence in private banking and global wealth management across different regions. Jesús spent 12 years at J.P. Morgan Private Bank advising high-net-worth families in Switzerland and Miami, while Alejandro brings more than 30 years in the financial industry, including 17 years in leadership roles at Banco Santander, followed by 12 years at J.P. Morgan. Together, they offer specialized capabilities in global investment management, family governance, and cross-border wealth structuring.

According to them, Centrica’s business model is based on independence, alignment, and long-term partnerships, providing clients with access to institution-grade solutions while maintaining the flexibility of an owner-managed firm.

Although no new rate cuts are expected to be announced by the monetary authority, this meeting is marked by somewhat weaker preliminary data, pressure from the Trump administration making headlines, and the market watching closely.

“While no change to the benchmark interest rate is expected, recent comments from some voting members of the Federal Open Market Committee have shown support for a possible cut. Furthermore, the trade agreement between the EU and the U.S. could further reduce the need for short-term stimulus,” note analysts at Muzinich & Co.

The forecast is that the interest rate will remain in the range of 4.25% to 4.5%, as there have been no clear signs either in the last meeting or since then that a rate cut is being considered. Instead, what will matter most are Powell’s remarks, as the goal is to temper market expectations, which currently assign a 60% probability to a rate cut in September.

“The market’s reaction to the press conference will be interesting. A week before the FOMC meeting, the market was pricing in a 65% chance of a cut in September. That probability will approach either 0% or 100% as we get closer to September 17. Will we see signs of such a move after the July meeting?” asks Erik Weisman, Chief Economist at MFS Investment Management.

For Vincent Reinhart, Chief Economist at BNY Investment, Fed officials will have to work hard to do nothing at this FOMC meeting. “This isn’t chess or tic-tac-toe. For the Fed to cut rates, three conditions must align: some concern about employment, signs that inflation will return to target, and enough clarity about the economy to be confident in those two premises. For now, we anticipate a 25-basis-point cut in December, and less than a 50% chance of anything happening before then. Essentially, the Fed would correct course if economic data worsens, acknowledging they may have misjudged the economy’s strength and the impact of tariffs on inflation,” notes Reinhart.

The Data the Fed Watches

Growth and inflation outlooks support the central bank’s more cautious approach. It’s worth recalling that in terms of inflation, the Fed’s preferred indicator (core PCE inflation) remains above target, at 2.7% year-over-year, and there are signs that tariffs are beginning to pass through to core goods prices. “Consumer expectations have declined from multi-decade highs, but remain high enough for the Fed to be hesitant about rate cuts in July,” says Michael Krautzberger, CIO of Public Markets at Allianz Global Investors.

In this context, Kevin Thozet, a member of the investment committee at Carmignac, notes that the Fed does not expect inflation to return to its 2% target before 2027, representing a six-year “deviation.” “And the latest inflation data are not particularly encouraging. We’re starting to see signs of import cost pass-through due to tariffs. Core goods inflation has already ticked up modestly, and the FIFO model that dominates the U.S. retail sector indicates that more price increases will come once tariffs are more broadly applied,” explains Thozet.

According to David Kohl, Chief Economist at Julius Baer, the weakening of the U.S. economic outlook suggests that a more accommodative monetary policy is likely in the second half of the year. However, he warns that “uncertainty around inflation following the rise in tariffs prevents a rate cut in July, as does the political pressure from President Trump to lower rates.”

The Pressure Mounts

Even though the data still support the Fed’s “wait-and-see” stance, the pressure to cut rates is increasing, both from the Trump administration and from within the Fed itself. On the political front, Fed Chair Jerome Powell has faced growing pressure to cut rates immediately, with President Trump even suggesting the possibility of replacing him before his term expires in May 2026. According to Thozet’s analysis, Powell has been under increasing political pressure, but any speculation about his replacement should be treated cautiously. “President Trump has little to gain from reshuffling Fed leadership just six months before Powell’s term ends. Moreover, the risks of undermining the Fed’s credibility on the dollar, inflation expectations, and long-term bond yields are too great. The central bank’s credibility has played a key role in anchoring long-term inflation expectations since their sharp rebound in 2022. Any move toward fiscal dominance or premature easing could jeopardize that hard-won stability, with significant negative ripple effects,” he comments.

The pressure doesn’t come only from the White House—it also comes from within the institution itself. “The minutes from the June meeting showed that most committee members believe monetary policy is ‘well positioned’ as they wait for more clarity on growth and inflation outlooks. However, they also acknowledged the risk that tariffs could have more persistent effects. Still, internal divisions are starting to emerge within the Fed,” comments Krautzberger.

In recent weeks, Governor Waller called for a 25-basis-point cut in July, based on the following rationale: tariffs will cause an exceptional increase in prices; the economy has already been operating below potential during the first half of the year; and labor market risks are increasing. “Other Fed members, however, have expressed a desire not to cut rates preemptively, and Powell himself has suggested that it remains prudent to wait and see how macroeconomic conditions evolve,” adds the Public Markets CIO at Allianz GI.

Beyond July

Looking beyond July, the market anticipates no more than two rate cuts before year-end, depending on upcoming inflation data. However, heading into the Fed’s September meeting, political pressure to reduce rates could intensify, especially if consumer demand and the labor market weaken more than expected. “We believe current data support the Fed maintaining its monetary policy stance in July. However, unless there’s a significant inflation surprise, the September meeting could become an active turning point for resuming cuts, particularly if economic indicators weaken and political pressure reaches a level that forces the Fed to act,” says Krautzberger.

According to Julius Baer’s chief economist, the stagnation of private consumption and lower investment intentions, which point to reduced demand, would justify a less restrictive policy stance, even though inflation rates remain above target. “Political pressure makes it harder for the Fed to communicate rate cuts in upcoming meetings. We expect the Fed to resume its rate-cutting cycle at its September FOMC meeting,” states Kohl.

Experts agree that the overall data suggest the economy remains in good health, and there is a risk of an upward trend in inflation due to tariffs. According to Mauro Valle, Head of Fixed Income at Generali AM (part of Generali Investments), “the market expects the Fed to cut again between September and October, but no longer anticipates two cuts by year-end. Uncertainty about the economic outlook and the impact of tariffs is high, and the Fed will likely continue to take its time.”

In the view of Tiffany Wilding, Economist at PIMCO, interest rates could reach neutral next year. “Many investors are wondering about the direction of Fed policy, particularly in light of public dissatisfaction from Trump with recent decisions under Powell and the expiration next year of key Fed appointments. In our view, economic fundamentals and institutional dynamics point to a baseline policy outlook that is not significantly different from what would be expected under the current composition of FOMC participants—perhaps with a marginally faster return to a more neutral policy stance,” she concludes.

Dynasty Financial Partners announced the appointment of Shawn Shook as Legal Advisor.

Shawn Shook brings over ten years of legal and regulatory experience in the financial services sector, particularly with registered investment advisors, broker-dealers, and professionals transitioning to independence. In his new role, he will oversee Dynasty’s legal strategy across all corporate initiatives and support the network’s 57 partner firms in regulatory, transactional, and compliance matters.

“Shawn brings valuable experience that strengthens our legal team as we continue to grow,” said Shirl Penney, CEO and Founder of Dynasty Financial Partners.

“His judgment and insight will help us continue supporting independent advisors in building their businesses,” she added.

Shook previously worked at Kestra Financial, where he negotiated documentation for several acquisitions and advised on corporate governance, regulatory compliance, and other strategic initiatives. Before Kestra, he served as Associate General Counsel at Edelman Financial Engines, where he worked on matters related to mergers and acquisitions, commercial agreements, advisor onboarding, and risk management.

In his new position at Dynasty Financial Partners, he will report to Shirl Penney, CEO of Dynasty, and work from the firm’s headquarters in St. Petersburg, Florida. Shook succeeds Jonathan Morris, who is taking on a new role as Executive-in-Residence after more than a decade as General Counsel.

“I want to thank Jon Morris for his incredible guidance and contribution as our General Counsel over the past 12 years. Jon has been an exceptional friend, business partner, and trusted advisor to the firm and our entire network. I am very pleased that Jon will remain at Dynasty as an advisor to the firm and as our new Executive-in-Residence,” said Shirl Penney.

Shawn Shook holds a Juris Doctor from George Mason University and a bachelor’s degree in Political Science from the University of North Carolina at Chapel Hill.

The Santander Private Banking International team in Miami has a new member: Alvaro Bueso-Inchausti, the new Director of Alternative Investments, according to an announcement made by the Spanish bank on LinkedIn.

Bueso-Inchausti has been working at the Spanish institution since 2023, and until his appointment in Miami (dated July of this year), he held the position of product specialist at the alternative investment management division of Santander Asset Management.

Bueso-Inchausti comes from A&G, where he was responsible for a new business line dedicated to alternative asset fund-of-funds.

Previously, he served for five years as Executive Director at Altamar Capital Partners, within the Private Debt team, where he worked since the firm launched its first private debt fund-of-funds in 2017. He also spent four years in the infrastructure subsidiary of Grupo ACS, Iridium, on the finance team, and earlier in the Leverage Finance department at CaixaBank Madrid and at Commerzbank in London. He holds a degree from CUNEF.

The U.S. Securities and Exchange Commission (SEC) announced that it will host a roundtable, scheduled for September 18, 2025, to debate the trade-through prohibitions in the equity and listed options markets of the National Market System (NMS).

Specifically, the discussion will focus on the trade-through ban under Rule 611 of Regulation NMS (Reg NMS). “The NMS Rule and its Rule 611 have not been effective for investors or for brokers, given the market distortion and resulting manipulation by those seeking to exploit the structure of the NMS Rule,” stated Chairman Paul S. Atkins, justifying the agency’s decision to hold the roundtable.

“The Commission must provide the public with the opportunity to weigh in on aspects of our regulations that deserve updating, and I look forward to the input we will receive on various aspects of the direct trading prohibition under Rule 611 as it applies to NMS stocks, and the analogous NMS plan prohibition applicable to listed options,” the official explained.

What Does the Trade-Through Ban Under Rule 611 Consist Of?

The trade-through ban under Rule 611 of Regulation NMS (Reg NMS) is a rule by the U.S. Securities and Exchange Commission designed to protect retail investors and promote fair competition among stock markets.

This rule applies to the National Market System (NMS), which includes the major exchanges where stocks are traded in the U.S., such as the NYSE and Nasdaq.

Rule 611, also known as “the Order Protection Rule,” prohibits an exchange or trading center from executing an order at a price worse than the best price available on another exchange. This phenomenon is known as a trade-through.

Rule 611 is intended to ensure that institutions automatically route orders to where the best available price is. This protects the investor from overpaying (or underselling) when a better offer exists on another market.

According to the SEC, the roundtable will be open to the public and will take place at SEC headquarters, located at 100 F Street, N.E., Washington, D.C., on September 18. The discussion will be streamed live on SEC.gov and a recording will be made available afterward. Information about the agenda and roundtable speakers will be published prior to the event.

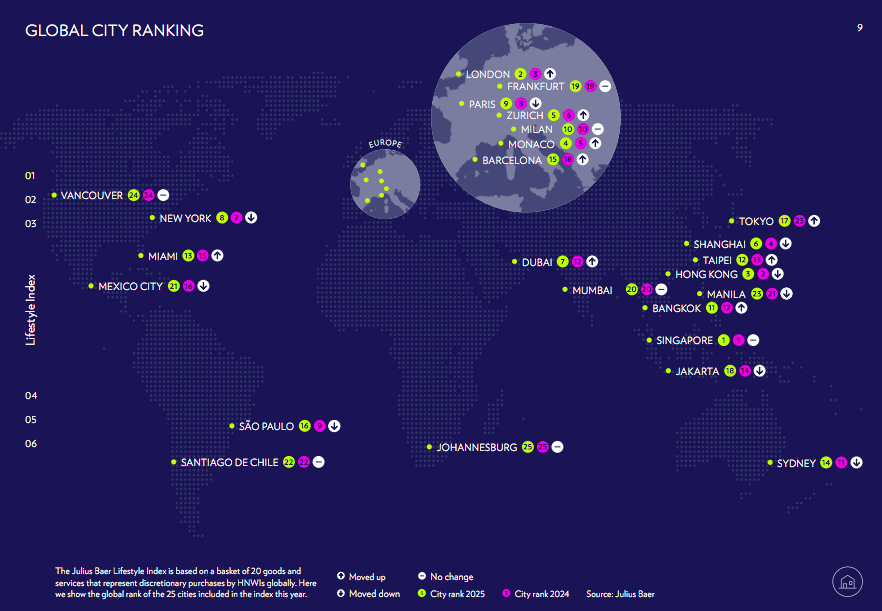

In a context of slowing global consumption, growing geopolitical tensions, and imminent trade disputes, High-Net-Worth Individuals (HNWIs) are adjusting their priorities, according to the new 2025 edition of Julius Baer’s Global Wealth and Lifestyle Report.

“Although data collection concluded before the U.S. announced its new tariffs, our findings still indicate a notable shift,” the report states. One of its main conclusions is that, for the first time since its launch, the report has recorded a 2% decrease, based on measurements in U.S. dollars—a surprising development in a segment that has traditionally outpaced average consumer price growth. “While services declined slightly by 0.2%, goods prices dropped by a significant average of 3.4%,” it clarifies.

As Christian Gattiker, Head of Research at Julius Baer, explains, “In light of current events and the uncertainty brought on by trade tensions and tariff escalations, our findings emerged before the truce declared by the Trump administration expires, so next year’s edition of the Wealth and Lifestyle Report will certainly offer relevant and fascinating data from a retrospective viewpoint.”

One of the report’s findings is that the city rankings remain highly competitive. In this regard, Singapore maintains its position as the most expensive city for HNWIs worldwide, followed by London, which rises to second place. Hong Kong rounds out the top three. However, significant movement is observed elsewhere, with Bangkok and Tokyo each climbing six places, and Dubai continuing its upward trajectory.

The EMEA Region

Focusing on the EMEA region (Europe, the Middle East, and Africa), its cities once again stand out, now representing more than half of the global top 10. London leads the region, rising to second place globally, while Monaco and Zurich each move up one position to fourth and fifth place, respectively. Dubai has climbed five spots to seventh, solidifying its position as a serious contender among traditional wealth hubs. Milan and Frankfurt maintained their positions, while Paris dropped slightly in the ranking. Johannesburg remains at the bottom despite some price increases.

“Price developments in EMEA have been moderate overall, with local currency prices stable or even falling in cities like Zurich. The most notable price increase in the region occurred in Paris, where higher travel and accommodation costs led to a 5% year-over-year rise. Private education costs in London also soared, driven by recent legislative changes,” the report explains.

Other Geographic Regions

The report’s authors note with interest that Singapore remains the most expensive city in the world, underlining the ongoing importance of Asia-Pacific. The region recorded only slight price decreases, averaging 1%, making it the most stable of all regions this year. In terms of rankings, Bangkok and Tokyo saw the greatest progress, each climbing six positions to 11th and 17th place, respectively. In contrast, Shanghai dropped from fourth to sixth place.

In Asia-Pacific, spending on goods remains high, though consumer preferences continue to evolve. Notably, technology prices dropped sharply (by 21.4%), while business class airfares increased by 12.6%. The growing wealth of the Asia-Pacific HNWI population, along with rising interest in health, wellness, and experiences, continues to shape spending patterns across the region.

In the Americas, New York remains the highest-ranked city in the region (eighth globally). Miami moved up two spots to 13th, while São Paulo and Mexico City dropped in the rankings.

Price Trends

Another conclusion from the report is that while average prices of goods in U.S. dollars fell in the Americas, the region recorded some of the largest increases in business class flights (+39.3%) and hotel suites (+17.5%). These increases have significantly raised the cost of travel and hospitality, now 41% higher than the global average. Notably, local currency price increases were much steeper in Latin America, with Mexico City and Santiago experiencing rises of up to 16% and 15%, respectively.

In this sense, the 2025 Index reflects diverging trends across categories. The steepest global price drop was seen in technology (-22.6%), driven by falling prices on items like MacBooks. Conversely, business class flights saw the most significant price hike (+18.2%), fueled by changes in airline business models, limited aircraft supply, and sustained demand for premium travel. The cost of private education also rose considerably (+5.1%), especially in London following the British government’s VAT change on private school tuition. Watches experienced a 5.6% increase, reflecting continued demand for exceptional, high-quality models.

There are just four days left before the tariffs imposed by the U.S. come into effect for countries that have not reached a deal. The most recent to do so are the European Union, which has secured a provisional trade agreement under which most of its exports to the U.S. market will be subject to a 15% tariff, and Japan, which agreed to a flat 15% tariff on all its products. Beginning August 1, however, imports from Canada, Brazil, South Korea, Cambodia, and Bangladesh will face tariffs ranging from 25% to 50%.

Experts expect further announcements in the coming days—particularly regarding the preliminary agreement with China, and the ongoing negotiations with India, which have made progress but remain unresolved. Additionally, Mexico, Brazil, Canada, and South Korea still lack comprehensive agreements and may face further tariffs if negotiations don’t conclude soon.

On the recent deals with the EU and Japan, Philippe Waechter, Chief Economist at Ostrum AM, believes both were fighting the same battle: “The tariff is identical (15%), the exception on steel and aluminum remains at 50%, the market opens further to American companies, and Europe commits to investing $600 billion. Japan agreed to $550 million. So far, we don’t have the details on how the investment benefits will be distributed (in Japan’s case, 90% goes to the U.S.). Europeans will also purchase $750 billion worth of energy over the next three years, moving away from climate targets, and will spend heavily on American military equipment.”

According to Waechter, the EU and Japan agreements show that “to remain dependent on the U.S. market, Europeans and Japanese are willing to pay an exorbitant price, justified only by the risk of isolation.” He adds that these tariffs reflect a global cycle long dominated by U.S. consumers. “Once that situation consolidated, increased tariffs began trapping the rest of the world, which now must pay to maintain cyclical momentum.”

Jared Franz, economist at Capital Group, stresses that not all trade barriers are created equal. In this case, he argues that Trump is using tariffs for multiple purposes—the clearest being negotiation. “The U.S. president has made it clear that some tariffs are meant to pressure countries into helping the U.S. meet its political goals, such as fighting illegal immigration and curbing drug trafficking. These may be temporary,” he notes. In contrast, the cases of Europe, Japan, and Mexico are more about rebalancing. “Reciprocal tariffs are aimed at restoring balance with other trading partners and primarily reducing the U.S. trade deficit,” Franz adds.

He concludes, “These motives will heavily influence the long-term tariff landscape. Tariffs used for negotiation will likely be short-lived, while those tied to broader strategic goals could be more permanent.”

One More Agreement, Less Uncertainty

The terms of the EU–U.S. trade deal include a base tariff of 15% on nearly all EU imports, including key sectors like automobiles (currently taxed at 27.5%). Tariffs on EU steel and aluminum remain at 50% for now, though a quota system may replace them. The agreement also involves major spending commitments: the EU will purchase $750 billion worth of oil, gas, nuclear fuel, military equipment, and semiconductors during Trump’s second term. Meanwhile, European companies are expected to invest $600 billion in the U.S. during the same period.

So far, European equity markets have responded with optimism, as the deal reduces uncertainty. “There’s progress in trade negotiations, but risks remain. Investors are closely watching economic data for signals on tariff impacts and potential policy decisions. With tariff talks ongoing and global monetary policy at a turning point, the coming weeks could be pivotal for shaping investor expectations for the rest of 2025,” say analysts at Muzinich & Co.

From a European perspective, another positive factor is that EU goods are now on equal footing with those from similarly developed competitors like Japan and may receive better treatment than many emerging markets that have signed deals with the U.S. in recent weeks. However, if market optimism drives the euro higher, that could become a headwind for the eurozone, warns Gilles Moëc, Chief Economist at AXA IM.

Avoiding the Worst-Case Scenario

According to Apolline Menut, economist at Carmignac, the agreement prevents the worst-case scenario: Trump’s threatened 30% tariffs, chaotic retaliation, and a full-blown trade war. “Europe lacks the strategic economic and technological leverage that China holds over key industrial supply chains. True, U.S. manufacturers rely more on European suppliers of intermediate goods than vice versa, but in an escalating retaliation cycle, Trump could have expanded the fight to include restrictions on energy and digital services—areas where the EU is fully dependent on the U.S.,” she says.

What the EU Loses

Still, Waechter calls it “a sad day” for Europe: “Europe is so afraid of being isolated from the U.S. that the negotiations focused only on goods—not on the broader spectrum of goods and services, which are more balanced in trade terms. This means Europe has forfeited the chance to pursue technological independence. The imbalance in services is largely due to technology. Draghi’s hope of massive investment to close the tech gap with the U.S. is now just a dream. The ability to generate a strong income dynamic has proven a mirage. Income distribution will become a real power struggle within Europe, as the pie won’t grow significantly. It will have to be split among the active and inactive, and even among the active. Social dynamics will be interesting—but also very dangerous.”

Analysts at Ebury acknowledge the negative economic impact but note that greater harm was avoided: “While many details of the agreement still need to be finalized—and tariffs will likely continue to weigh meaningfully on growth—investors are relieved that the worst-case scenario has been averted.”

Felipe Villarroel, portfolio manager at TwentyFour (Vontobel), sees similarities with the deal struck by the U.K.: “This is a suboptimal outcome for the U.S., the EU, and the global economy—but it’s one the economy can likely withstand without catastrophic macro consequences. Experts have already priced in a 10–15% tariff rate. Markets have had time to absorb what this result means for businesses and growth projections. The conclusion seems to be that certain sectors, such as autos, will take a hard hit, while others will suffer indirectly through slower growth—but can keep going,” he says.

European Equities in Focus

On a more positive note, Villarroel highlights that Europe managed to shield some key sectors from harsher tariffs (ranging from 25% to 50% or more): “The agreement lowers auto tariffs (from the 25% under ‘Section 232’ to 15%) and covers both semiconductors (threatened with a 25% tariff due to a pending BIS investigation) and pharmaceuticals (for which Trump floated potential tariffs of up to 200%). It significantly reduces trade policy uncertainty for European supply chains—though the devil is in the details, especially around ambiguous zero-for-zero tariff provisions.”

Lastly, Johanna Kyrklund, Group Chief Investment Officer at Schroders, continues to emphasize that Europe benefits from global investors’ search for diversification in equity portfolios. “We’ve seen strong demand for European assets—both equities and bonds. European stocks have performed well this year, and we still see value. So, I believe Europe has been the main beneficiary of global investors’ diversification push. There’s also been significant interest in European bonds, showing that investors aren’t cutting exposure but diversifying. Meanwhile, the euro has strengthened against the dollar. In fact, we believe there’s still upside in the euro and remain quite positive on European markets,” Kyrklund concludes.