BBVA Global Wealth Advisors (GWA) Announces the Addition of Roberta Fernandes as Investment Counselor in Its Houston, Texas Office

“We are thrilled to warmly welcome Roberta Fernandes, who joins our BBVA Global Wealth Advisors team in the Houston office as our new Investment Counselor,” the firm posted on the social media platform LinkedIn.

Fernandes shared the post on her personal profile on the same platform, thanking the team for the welcome. She added that she already feels “part of the BBVA family.”

According to the official announcement, “Roberta’s experience significantly enhances our service capabilities in Houston. She brings over 16 years of experience in private banking and cross-border wealth management.” The bank also highlighted Fernandes’ “relationship leadership: her career has focused on building strategic relationships with high-net-worth (HNW) and ultra-high-net-worth (UHNW) clients in Latin America and the U.S.”

They also emphasized her “technical knowledge: her expertise spans financial markets, asset allocation, and advisory frameworks.” In addition, the statement noted her client-centered approach: “Roberta specializes in delivering wealth solutions well-aligned with clients’ evolving objectives, with a focus on regulatory alignment and risk mitigation.”

According to her profile on the professional network LinkedIn, Roberta Fernandes served as Director at BTG Pactual for nearly three years. Previously, she was Associate VP International Client Advisor (ICA) at Morgan Stanley, and also worked in Miami at Santander Private Banking (as Client Relationship Manager) and at Merrill Lynch in New York (as Registered Client Associate), among other professional roles.

She holds a Bachelor’s Degree in International Business from Trinity University in San Antonio, Texas, a Master’s in Finance from the University of Chile, and an MBA from Babson College. She also holds FINRA Series 66 and 7 licenses.

The “One Big Beautiful” Law Remains a Source of Endless News and Updates in 2026. One of Them, Affecting Mutual Funds and ETFs, Will Be the Launch of the “Trump Accounts” for Newborn American Citizens

All babies born in the United States between January 1, 2025, and December 31, 2028, will have an account automatically opened when they receive their Social Security number, without parents having to take any action. The government deposits an initial $1,000, and from there, parents, relatives, guardians, employers, or organizations can make additional contributions, although these private contributions are not tax-deductible.

The operation is estimated to cost $15 billion through 2034.

The accounts are designed as long-term savings instruments, as the funds remain locked until the beneficiary turns 18.

A New Business for Funds and ETFs Investing in the U.S. Stock Market

The “Trump Accounts” can only invest in the U.S. stock market. Their growth will depend on market performance, and there is no guarantee of returns.

Why are safer assets like Treasury bonds excluded? Only Trump has the answer.

The capital is channeled into diversified funds that track the overall performance of the U.S. stock market, avoiding sector concentrations or investments in assets considered risky or too specific. The law also sets strict limits on fees, allowing only low-cost products.

When the beneficiary reaches adulthood, the account receives tax treatment similar to a retirement account, maintaining usage rules aligned with that type of vehicle.

Since it is a new program, regulators still need to determine which funds or managers will administer the actual accounts.

Funds That Could Be Selected

It is possible to identify U.S. broad-market equity funds and ETFs that, while not guaranteed to be officially chosen, do meet commonly accepted criteria: they replicate broad indexes, have low fees, and are diversified.

Vanguard S&P 500 ETF (VOO) — A very popular ETF that tracks the S&P 500 index, with very low fees.

iShares Core S&P 500 ETF — Another ETF indexed to the S&P 500, with good diversification and low cost.

Vanguard Total Stock Market Index Fund — An equity index fund that covers a broad universe of the U.S. market; it offers diversification beyond the large companies of the S&P 500.

iShares Core U.S. Total Stock Market ETF (for example, in its ETF version tracking a broad index of the entire U.S. market) — An equally diversified and low-cost option.

All Eyes on Birth Rates

Official U.S. birth data for 2025 has not been consolidated yet, but according to the National Center for Health Statistics of the United States, 3,628,934 births were recorded in 2024, representing a 1% increase compared to 2023. The fertility rate (births per 1,000 women aged 15 to 44) was 53.8 per 1,000 in 2024.

The asset management industry faces two challenges: clients demand greater personalization and efficiency, while profit margins are tightening. PwC’s Asset & Wealth Management Revolution study reports 89% of asset managers feel pressure to deliver profitability, with nearly half describing this pressure as high or very high.

At the same time, artificial intelligence (AI) has become the main technological lever in the sector. This is no coincidence: the global AI market surpassed USD 244 billion in 2025, an increase of almost USD 50 billion in just two years. Projections are even more compelling: the industry is set to surpass the trillion-dollar mark by 2031, consolidating itself as a transformative axis for multiple sectors, including financial services.

PwC notes that 80% of asset and wealth managers believe disruptive technologies, including AI, are driving revenue growth. McKinsey, on the other hand, estimates that a mid-sized asset manager can capture between 25% and 40% of their cost base through well-executed AI initiatives, provided that end-to-end workflows are reimagined, not just isolated tasks.

Meanwhile, the McKinsey Global Institute’s Agents, Robots, and Us report highlights that AI is redefining the way organizations operate: machines take on routine tasks, while people focus on interpretation, decision-making, and solution design.

In this context, securitization appears as the “structural bridge” that allows AI capabilities to be transformed into concrete, scalable, and globally distributable investment products.

Why are AI and securitization connected now?

1.- Pressure on margins + need for efficiency

AI reduces operational costs, and securitization allows this efficiency to be packaged into lighter and more cost-effective vehicles, helping managers survive and grow in an environment with increasingly tight margins.

2.- Increasing adoption of AI in front, middle, and back offices

PwC highlights that managers are integrating AI in portfolio personalization, task automation, and generating insights for clients.

However, many of these capabilities remain “locked” within the organization unless they are translated into investable products.

3.- Transformation of the investment leader’s role

McKinsey emphasizes that business leaders must become “tech-savvy leaders,” capable of linking AI strategy with financial outcomes and business models.

Securitization provides a framework for monetizing these technological capabilities in the form of structured series or notes.

How can portfolio managers combine AI + securitization?

a) Turning AI-driven strategies into securitized vehicles

AI models generate increasingly sophisticated investment signals, rebalancing, and portfolio construction. Rather than limiting these strategies to internal balance sheets or segregated mandates, managers can:

Replicate the systematic strategy in a securitized vehicle (e.g., a series issued through an SPV).

Offer it to institutional and professional investors as a product with an ISIN, international custody, and standardized operational flow.

In this way, AI becomes an alpha engine, and securitization is the vehicle that takes it to market.

b) Packaging infrastructures and AI-linked flows

Adopting AI involves investments in data, models, and technology infrastructure. McKinsey emphasizes that the true economic impact is achieved when AI is integrated into full processes and operational models, not just isolated pilots.

Through securitization, portfolio managers can structure:

Thematic notes linked to AI-intensive company or sector strategies.

Vehicles that expose the investor to flows generated by assets or contracts tied to AI (e.g., digital ecosystems, data, or technological services), when eligible as underlying assets.

c) Accelerating time-to-market and customization

PwC’s reports on the asset and wealth management revolution highlight that managers who combine technology and the redesign of operational models are more likely to capture growth in a highly competitive environment.

Securitization allows:

Launching AI-based products in shorter timeframes than a conventional fund.

Creating tailored solutions for specific customer segments (e.g., AI-driven strategies with specific ESG or liquidity restrictions).

Evidence from PwC and McKinsey shows that AI is already a critical factor for future profitability for managers, but its real impact depends on the ability to turn it into tangible investment solutions.

Securitization programs provide portfolio managers with a flexible infrastructure to transform AI capabilities into products ready for global distribution, aligning technological innovation, cost efficiency, and growth in assets under management. In this context, specialized companies like FlexFunds demonstrate how agile, global solutions can facilitate this transformation, turning advanced strategies into cost-efficient, scalable vehicles without the need for complex conventional structures.

To learn more about how FlexFunds uses advanced technologies for its asset securitization program, please contact our experts at contact@flexfunds.com

A global passion for soccer in motion will drive an increase in tourism revenue across 16 U.S. cities, which will welcome 1.24 million international visitors. This is the projected impact of the 2026 FIFA World Cup, according to a report by Tourism Economics, a company under Oxford Economics.

This World Cup will be the largest in history, featuring 48 teams, 104 matches, and 16 host cities across the United States, Canada, and Mexico. A total of 78 matches will be played in the U.S. alone, with stadiums averaging nearly 70,000 in seating capacity. The U.S. match schedule begins on June 12 in Los Angeles, California, and concludes with the final on July 19 in East Rutherford, New Jersey.

Inbound Tourism Demand

The company projects that the United States will receive 1.24 million international visitors for the World Cup, of which 742,000 (60%) will be additional—trips that would not have occurred otherwise. After a challenging 2025 for international overnight travel to the U.S. (with a decline of 6.3%), inbound tourism is expected to rebound by 3.7% in 2026, with nearly one-third of this growth linked to the tournament.

The peak of arrivals is expected in June, when 57 of the 78 U.S. matches will take place, representing a 10% increase in international arrivals compared to the previous year. July will bring in an additional 200,000 visitors, accounting for a 3.2% increase.

The unique passion of the soccer fan base underpins this surge: international spectators are estimated to represent approximately 40% of stadium attendance, typically attending two matches each, with 15 companions per 100 ticketed attendees.

“Mega-events concentrate demand, and the global reach of the World Cup is unmatched,” said Aran Ryan, Director of Industry Studies at Tourism Economics. “We expect a strong increase in hotel occupancy across U.S. host markets, along with a broader tourism boost as fans visit multiple cities and extend their stays,” he added.

“Soccer fans plan to follow their teams for years and may even organize once-in-a-lifetime trips around the World Cup,” he added.

Peak Nights and Premium Rates

In North American host markets, additional hotel room revenue related to the World Cup is expected to rise between 7% and 25% in June 2026, according to Ryan, with the most pronounced increases occurring on match days.

“Factoring in July matches, some cities could see year-over-year growth in additional room revenue between 1% and 5%,” he noted.

Nationally, the event will add approximately 0.4% to total hotel room revenue for 2026—a seemingly modest figure, but substantial in absolute terms, considering host cities only account for about 16% of the U.S. hotel room supply and the increase is concentrated in June and July.

Match significance is key. History shows that final rounds significantly drive up rates. In Germany 2006, the average daily monthly rate increased by 7.6% for each match in June, 14.4% for each match in July, and soared by 46.9% for the final—a pattern that serves as the foundation for the 2026 projections.

Cities such as New York, Dallas, and Miami—hosts of final-round or high-profile matches—are expected to experience significant increases.

Team fan bases also play a role. Fan-favorite teams like England, Brazil, Argentina, and France have an above-average impact wherever they play, amplifying hotel demand. Even smaller nations can generate unexpected impacts when qualification becomes a national milestone, mobilizing passionate fans who travel in surprising numbers.

Seeding allocations are not yet finalized. The December 5 group draw and subsequent schedule will clarify which cities will host teams with the largest fan bases—and therefore the greatest potential.

Legacy and Opportunity for Destinations

The World Cup enhances the branding of host cities through global broadcasts, fan-generated content, and first-hand experiences that elevate each city’s profile and encourage repeat visits. Many fans combine multi-city itineraries, discovering new places they often return to later.

“Destinations have a unique opportunity to capitalize on an active, local audience and will play a key role in spreading demand across neighborhoods, leaving an indelible mark on visitors for decades to come,” added Ryan.

The research findings are based on two reports by Tourism Economics:

FIFA World Cup 26 Host Cities Prepared: Analysis of Expected Hotel Sector Trends in RevPAR, ADR, and Occupancy

FIFA World Cup 2026: Increase in International Visitors to the U.S.: Quantifying Tourist Volume, Spending Impact, and Incremental Travel Effects

The results incorporate match schedules, hotel market capacity, air travel forecasts, and historical mega-event data, as well as behavioral factors tied to global fan bases and diaspora-driven travel.

Tourism Economics, a firm within Oxford Economics, is a global leader in travel forecasting and economic impact analysis, helping destinations and hotel brands turn data into actionable insights.

Women in ETFs held the third edition of its regional meeting WE South | Offshore 360: The Macro View in Miami, a live event aimed at connecting professionals from the ETF universe and the offshore business around the big questions of the economic cycle. It was an intimate day featuring prominent voices in economics, strategy, and innovation in exchange-traded funds.

Sponsored by StoneX, the event took place on November 19 at the JW Marriott Marquis in Miami, with an agenda focused on the macro pulse and its direct impact on portfolio construction. Representing the South Chapter of Women in ETFs were Jan Fredericks, Co-Head of Membership, and Estefanía Gorman, Secretary and Co-Head of Mentorship. Kathryn Rooney Vera, Chief Market Strategist at StoneX, served as Master of Ceremonies and was joined by Christian Prugue, Managing Director and Co-Head of LatAm Securities.

During the first panel, “The Economy Unfiltered: A Debate on the Global Forces Shaping the Markets,”Kathryn Rooney Vera and Jonathan Levin, Markets Columnist at Bloomberg, discussed the outlook for global interest rates, the trajectory of the U.S. labor market, and the impact of rising retail trading on market dynamics.

The experts also analyzed the key drivers reshaping the global market: views on inflation and growth, the expected path of interest rates in the U.S., and how these factors are shifting investors’ risk preferences.

Artificial intelligence and its effects on the economy and asset markets were a key focus of the event. The experts also offered strategic considerations for holding gold in portfolios, in light of opportunities looking ahead to 2026.

The second panel, titled “Market Pulse: Trends, Perception, and Strategic Alignment,” featured April Reppy Suydam, Head of Latin America Distribution at First Trust, and Brad Smith, CFA Analyst & Head of ETF Strategy Americas at Invesco. The panel was moderated by Estefanía Gorman, who also serves as Director of Client Success at Scala Capital.

Guided by Gorman, the experts discussed the “Magnificent 7” and the emerging trends and themes gaining traction.

The session placed special emphasis on the “very promising” opportunities in AI and cryptocurrencies within the ETF landscape. The second panel also covered evidence pointing to a shift from passive to active ETFs, as well as approaches to help advisors and clients become more comfortable with derivatives and options within ETF strategies.

The evening concluded with a memorable sensory experience: a chocolate and wine pairing led by Ricardo Trillo of Cao Chocolates, where attendees enjoyed a curated selection of chocolates, exploring their South American origins, unique flavors, and ideal wine pairings.

For distributors and advisors based in Miami—a city that is becoming an increasingly important hub for Latin America—the conversation delivered a common message: the need to combine macro conviction with agility in implementation amid a backdrop of intermittent volatility.

The South Chapter of Women in ETFs covers the states of Texas, Oklahoma, Arkansas, Louisiana, Mississippi, Alabama, Tennessee, Georgia, Florida, South Carolina, and North Carolina. Beyond market analysis, the gathering reinforced the mission of Women in ETFs to connect, support, and inspire the industry community, providing a space for networking and professional development for all professionals in the sector.

The introduction of digital assets into investment portfolios crossed a new threshold with the approval of Bank of America. The firm recommends a 1% to 4% allocation to crypto assets for clients of its Merrill, Bank of America Private Bank, and Merrill Edge platforms.

The investment strategists of the American bank will begin covering four bitcoin ETFs in January 2026, according to press sources.

“For investors with a strong interest in thematic innovation and who are comfortable with high volatility, a modest allocation of 1% to 4% in digital assets could be appropriate,” said Chris Hyzy, Chief Investment Officer of Bank of America Private Bank, in a statement.

“Our guidelines focus on regulated vehicles, a thoughtful allocation, and a clear understanding of both the opportunities and the risks,” he added.

Starting January 5, 2026, the bitcoin ETFs covered by the firm’s Chief Investment Officer will include the Bitwise Bitcoin ETF (BITB), Fidelity’s Wise Origin Bitcoin Fund (FBTC), Grayscale’s Bitcoin Mini Trust (BTC), and BlackRock’s iShares Bitcoin Trust (IBIT).

“The lower end of this range may be more appropriate for those with a conservative risk profile, while the upper end may be suitable for investors with greater tolerance for overall portfolio risk,” noted Hyzy.

Previously, wealthy Bank of America clients only had access to the products upon request, which meant that the bank’s network of more than 15,000 wealth advisors could not recommend exposure to cryptocurrencies, and many retail investors were forced to seek access through other sources.

“This update reflects the growing demand for access to digital assets from clients,” added Nancy Fahmy, Head of the Investment Solutions Group at Bank of America.

Photo courtesySamantha Ricciardi, until now, CEO of Santander AM

New Changes at Santander. At the top of Santander AM, Samantha Ricciardi has announced her departure from the asset manager, according to an internal statement from the firm, “to pursue new professional opportunities abroad.” She had been the top executive of the asset manager since 2022, a position she assumed following the departure of Mariano Belinky. The firm will launch a process to decide her replacement.

According to her LinkedIn profile, Ricciardi worked at BlackRock for 11 years in various roles, the last of which was as Head of Strategy and Business Development for EMEA. She also spent seven years at Schroders, where she served as Head of the asset manager in Mexico. She began her professional career at Citi in the year 2000.

The bank has just completed the integration of its two asset managers, Santander Asset Management and Santander Private Banking Gestión, to form an entity with approximately 127 billion euros under management.

Meanwhile, Ana Hernández del Castillo will lead the alternatives area at Beyond Wealth. Hernández del Castillo comes from Crescenta, where she joined in January 2024 as Investment Manager. Previously, she held various roles at MdF and Banque Havilland.

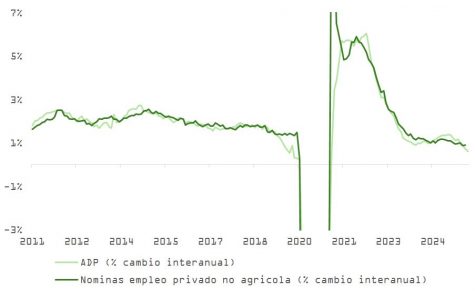

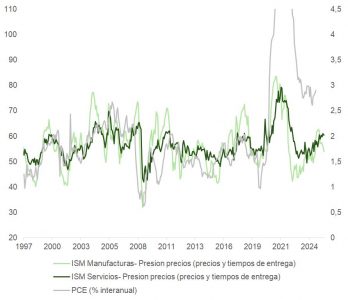

The November ISM manufacturing index fell to 48.2 (from 48.7), marking its ninth consecutive month in contraction. The new orders sub-index remains below that of inventories, signaling further weakness ahead. The employment component also declined (from 46 to 44), reinforcing the narrative of a still-weak industrial sector.

On the other hand, the ADP employment report shows a reduction of 32,000 jobs, while the Challenger report reflected a year-over-year increase in layoffs of 23.5%, though well below October’s 175%. Even so, limited hiring and low turnover continue to characterize the labor market, with no signs of collapse.

Consumption: Dynamic on the Surface, Fragile at the Core

During Black Friday, consumers spent a record $11.8 billion online, with holiday spending projected to exceed one trillion dollars. However, the momentum was driven by aggressive promotions, value-seeking behavior, and the use of “buy now, pay later” schemes—pointing to defensive strategies by the average consumer. This same pattern was evident, for example, in Walmart’s quarterly results, which showed higher-income families switching brands or slightly adjusting purchase quality to cut spending.

The stability of consumption now depends on political stimulus, such as the possible $2,000 check that Trump could distribute, and the expectation of declining financing costs. The “K-shaped” economy is becoming more apparent: high-income households continue spending, while middle-income ones are forced to seek liquidity.

The Fed: Cut in Sight, but With a Hawkish Stamp

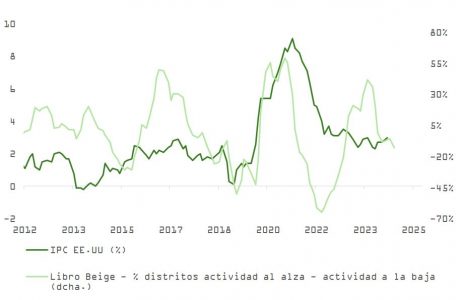

Given the lack of complete data due to the shutdown, the Fed will pay close attention to the Beige Book, which shows a nearly -20% gap between expanding and contracting districts, and a clear moderation in price indices.

Amid the absence of consensus within the Fed, a hawkish cut is shaping up for the December 10 meeting, with a cautious message aimed at containing expectations. This move could strengthen the dollar (DXY), which is threatening to break above its 200-day moving average. In that case, EURUSD would target the 1.14–1.12 range. While it is important to monitor the technical evolution of the exchange rate—which has briefly recovered its 50-day moving average—productivity gains, more evident in the U.S., are translating into increases in real incomes that should, in the short term, support U.S. asset prices and, consequently, international flows into its currency. The DXY dollar index (mostly reflecting the dollar’s crosses with the euro, Canadian dollar, and Japanese yen) is attempting to break above its 200-day moving average. If Powell ends up casting doubt on the integrity of the three cuts currently priced into the 2026 curve, a recovery of this reference level would boost the greenback’s exchange rate.

The Nasdaq Rebounds, but Sentiment Remains Mixed

The Nasdaq has recovered nearly 80% of the decline suffered in November, while the S&P 500 has corrected its overbought condition. However, investor sentiment remains cautious. The market has priced in the rate cut scenario, but is beginning to question the sustainability of the rally if data do not improve uniformly.

2026: When the Rest of the “K” Comes Into Play

U.S. macroeconomic data shows signs that justify rate cuts:

Stagnant private consumption: Real retail sales have been flat since December, and credit card delinquencies remain high, though stabilizing.

Weak housing: Residential investment has declined for two consecutive quarters, and over 60% of counties are seeing price drops (Zillow).

Soft labor market: So far, job growth is slowing and real income growth is below its historical pace.

But a shift on the horizon is beginning to take shape:

Tariff uncertainty is starting to fade, and Trump is closing off geopolitical stress points (Israel, Ukraine, China).

Tax exemptions from the OBBA plan will take effect in 2026.

AI-related productivity is showing results that are starting to extend beyond the technology and communications services sectors.

Financing costs have dropped substantially, with rates similar to 2018 levels, and the balance sheets of households and businesses remain healthy, leaving room for increased borrowing to boost investment and spending.

Credit Demand and Positive Releveraging

With a still-weak but stable labor market and a more optimistic view of the economic outlook, credit demand is beginning to pick up among both households and businesses. Leverage, measured against GDP and historical levels, remains low, creating room for positive releveraging.

In addition, leading employment indicators are showing signs of improvement:

The index from the American Staffing Association has risen for 10 consecutive weeks, suggesting a recovery in temporary employment demand.

Employment sub-indices from regional surveys indicate stabilization of manufacturing payrolls for 2026.

Capital expenditure intentions are rebounding after the tariff-driven slowdown.

Fiscal Risk and Shift in Republican Strategy

With debt levels at 120% of GDP, the fiscal lever is running out. Starting in the second half of 2026, fiscal stimulus could turn negative, even though the OBBA plan may still contribute 0.4% to GDP.

This alters the political approach: Trump and the Republicans will aim to sustain consumption without additional public spending. This implies reducing tariffs on consumer goods, reinstating direct transfers (such as the $2,000 check), and — critically — ensuring low interest rates to reduce financing costs.

Starting in May 2026, Trump is expected to take control of the Fed, which would reinforce this growth strategy through the cost of money rather than public spending.

Conclusion: A Reactive Fed, a Selective Market

The current environment gives the Fed room to continue cutting, but with measured communication. The market has priced in the cuts but needs evidence that the lower part of the “K” is picking up in order to sustain the rally.

The greatest risk is no longer inflation or recession, but rather a combination of uneven growth, instrumentalized monetary policy, and excessive optimism in tech segments that have yet to deliver clear profitability.

It makes sense, for now, to maintain positions in sectors most linked to the AI boom, but also to begin balancing with others that may benefit from the abandonment of the “K” theory.

Over 100 financial advisors from the United States and Latin America gathered at Insigneo’s Summit Sevilla 2025: Navigating Wealth Beyond Borders to explore the forces redefining global wealth management. One of the event’s most anticipated discussions, “Trends Reshaping Wealth Management,” brought together a distinguished panel moderated by Javier Rivero, COO & President of Insigneo, and featuring Ben Harrison, Global Head of Client Coverage and Managing Director at BNY Pershing; Ahmed Riesgo, Chief Investment Officer for Insigneo; and Marc Butler, Founder and CEO of Marc Butler and Wealth Management Chat GPT.

Against a backdrop of rapid technological progress, shifting demographics, and evolving client expectations, the panelists provided a clear roadmap for advisors seeking to remain competitive in a fast-changing landscape.

AI’s Transformative Role in Wealth Management

A central theme of the conversation was the accelerating integration of artificial intelligence into advisory practices. Rivero highlighted Insigneo’s own innovation in this space with Agent Neo, the firm’s proprietary AI-driven daily commentary tool.

“In January, many of you are in the pilot group of our Agent Neo daily commentary, and pretty soon, all of you are going to start receiving a daily piece that’s fully generated by Agent Neo… It’s a model we train on the right data,” Rivero explained.

The consensus across the panel: AI is no longer optional. It has become a critical enhancer of productivity, decision-making, and personalization—allowing advisors to scale insights and deepen client engagement.

Harrison encouraged advisors to proactively immerse themselves in these tools:

“Be curious and educate yourself, especially about new technologies like AI. If you’re not a paying subscriber to the premium ChatGPT, come on—pay the 20 bucks per month and access the research on these new things we’ve been talking about.”

Understanding Digital Assets: Closing the Knowledge Gap

As client curiosity—and allocation—towards digital assets grows, Rivero emphasized the importance of advisor education in cryptocurrencies and tokenized assets.

“I hear this a lot from advisors: How do I learn about crypto?… Unless you have a younger advisor embedded into it, how can they connect and learn? That’s the biggest challenge. I think everybody here wants to learn about it,” he said.

This knowledge gap represents both a risk and an opportunity. Advisors prepared to guide conversations around digital assets will be better positioned to serve younger, digitally native investors.

Reaching the Next Generation: A Strategic Imperative

Demographic shifts appeared repeatedly throughout the discussion. Butler underscored that preparing for wealth transfer is perhaps the most urgent priority for advisors.

“The biggest threat to your business is not AI or digitalization… it’s the beneficiary you haven’t met with,” he warned.

He advocated for bringing heirs into family meetings early and incorporating younger professionals into advisory teams.

“Someone younger that operates as your succession plan is going to create comfort with your clients and their kids… Those ‘HENRYs’—high earners, not rich yet—will be rich in 10 years. Embrace them now.”

Alternatives Take Center Stage in Portfolio Construction

Riesgo provided a forward-looking perspective on portfolio strategy, emphasizing the growing importance of alternatives not only as diversifiers but as potential growth engines.

“When growth is down, you need the diversifiers doing the opposite… You’ve got to have hedge funds, digital assets, gold, commodities,” he noted.

He highlighted that alternative allocations could account for 25% to 50% of portfolios, depending on the market environment and investor risk profiles—reflecting industry-wide momentum toward private equity, private credit, venture capital, and real-asset strategies.

Digital Platforms and Interoperability: The Client Experience Frontier

The panel also discussed the urgent need to create more seamless, intuitive digital experiences. Advisors and clients increasingly demand streamlined platforms, enhanced data connectivity, and user-centric interfaces.

Interoperability, they emphasized, is no longer a luxury but a core component of modern advisory ecosystems—particularly as workflows become more distributed and cross-border.

A New Era for Cross-Border Wealth Management

The panel closed on a unifying message: advisors who remain curious, adaptable, and tech-forward will lead the industry’s next chapter. As the wealth management landscape becomes increasingly global and digital, the insights shared at Summit Sevilla 2025 offer a powerful blueprint for advisors seeking to grow, innovate, and better serve clients across generations and geographies.

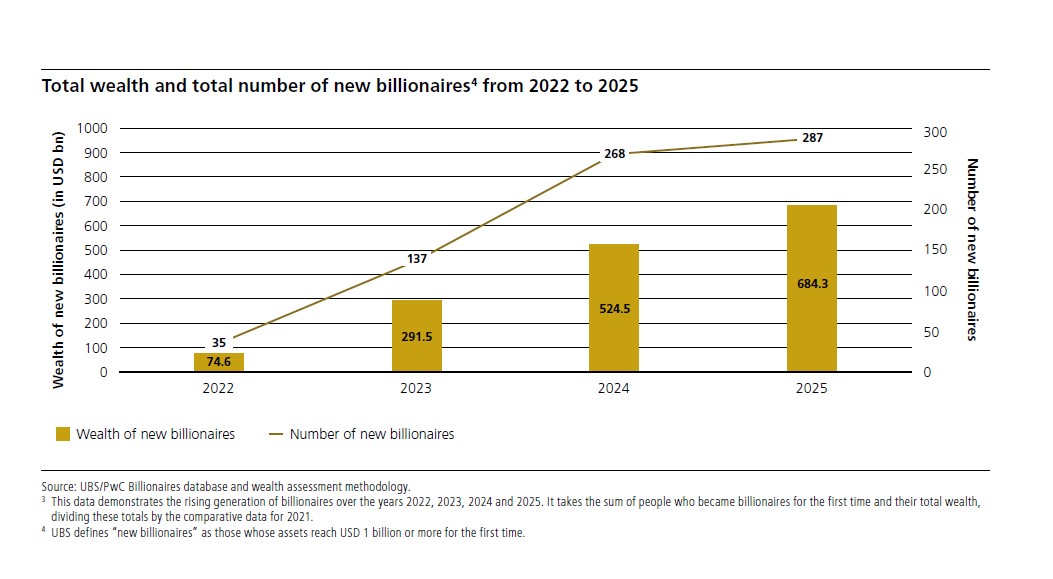

In 2025, 196 self-made billionaires drove global wealth to a record high of $15.8 trillion, a 13% increase over 12 months and the second-largest annual gain after 2021. According to the latest UBS report, titled Billionaire Ambitions Report 2025, we are witnessing a new wave of billionaires, fueled by business innovation and a rise in inheritances.

The report highlights that these new billionaires include both entrepreneurs successfully building businesses in today’s uncertain environment and heirs participating in a multi-year, accelerated wealth transfer. In 2025, the second-highest number of self-made individuals in the history of the report became billionaires.

“Our report shows how the rise of a new generation of wealth creators and heirs is transforming the global landscape. As families become more international and the great wealth transfer accelerates, the focus is shifting from simply preserving wealth to empowering the next generation to succeed independently and responsibly. This is influencing not only succession planning, but also philanthropic priorities and long-term investment decisions,” notes Benjamin Cavalli, Head of Strategic Clients and Global Family and Institutional Wealth Connectivity at UBS Global Wealth Management and Co-Head of EMEA One UBS.

In Cavalli’s view, we are seeing a billionaire community that is more diverse, mobile, and forward-looking than ever before. “The combination of entrepreneurial drive and the largest intergenerational wealth transfer in history is creating new opportunities and challenges for both families and wealth managers,” he adds.

Regarding investment priorities, despite market volatility in 2025, North America remains the top investment destination (63%), followed by Western Europe (40%) and Greater China (34%). Some 42% of billionaires plan to increase their exposure to emerging market equities, while more than four in ten (43%) are considering increasing their exposure in developed markets.

Self-Made Billionaires

According to the report’s data, in 2025, these 196 self-made billionaires added $386.5 billion to global wealth, pushing total wealth to a record $15.8 trillion. This marks the second-largest annual increase recorded in the history of the report. As a result, the number of billionaires rose by 8.8%, from 2,682 to nearly 3,000.

The report explains that, unlike the boom driven by asset revaluation after the pandemic in 2021, “this growth was marked by strong business dynamics and intense company creation.” From marketing software and genetics to liquefied natural gas and infrastructure, these innovators are reshaping large-scale demand, with billionaires from the United States and Asia-Pacific leading the way.

While billionaires investing in the tech sector saw their wealth grow by 23.8%, consumer and retail slowed to 5.3%, as the European luxury industry lost momentum to Chinese brands. Despite this, the consumer and retail sector remains the largest, totaling $3.1 trillion.

Industrial wealth experienced the fastest growth, rising 27.1% to reach $1.7 trillion, with more than a quarter coming from new billionaires. Meanwhile, wealth originating from the financial services sector increased by 17% to $2.3 trillion, driven by strong markets and a rebound in cryptocurrencies. Self-made billionaires now represent 80% of total wealth.

Billionaires by Inheritance

When it comes to wealth transfer, it is clear that the pace is accelerating. Looking ahead, billionaires are expected to transfer around $6.9 trillion globally by 2040, with at least $5.9 trillion going to their children.

Regarding this year’s developments, the report reveals that 91 individuals (64 men and 27 women) became billionaires through inheritance, receiving a combined $297.8 billion—more than one-third above the $218.9 billion in 2024. Additionally, according to calculations, at least $5.9 trillion will be inherited by the children of billionaires over the next 15 years.

Globally, inheritances have contributed to a rise in the number of multigenerational billionaires, now totaling nearly 860 and managing a combined $4.7 trillion in wealth, compared to 805 who controlled $4.2 trillion in 2024. Notably, the average wealth of women continued to rise in 2025, increasing by 8.4% to $5.2 billion—more than double the growth rate of men, which was 3.2%, reaching $5.4 billion.

“Although the transfer of wealth will likely be concentrated in a limited number of markets, high levels of migration could shift this landscape. Most wealth transfers will take place in the U.S. and in certain markets, but 36% of surveyed billionaires report having moved at least once, while another 9% are considering it,” the report notes.

Moreover, billionaires expect their children to succeed independently despite the influence of inheritance: 82% of surveyed billionaires with children want them to follow their own path and say they aspire to instill the skills and values necessary to thrive on their own, rather than relying solely on inherited wealth.

“In an era in which entrepreneurs often appoint professional managers or sell their businesses instead of passing them down to the next generation, 43% still hope their children will continue and grow the family business, brand, or assets,” the report adds.