There is a rare but highly damaging phenomenon for portfolios called “Triple Red,” which consists of a simultaneous decline in U.S. equities, U.S. Treasuries, and the dollar. A note from MSCI analyzes the phenomenon and argues that a similar configuration could exist today: political uncertainty that deteriorates institutional confidence, price pressures linked to tariffs that complicate potential monetary easing, and the possibility of coordinated retaliation acting as an external shock channel.

A “Triple Red” episode breaks “classic” diversification and, for non-U.S. investors, adds a second blow: in addition to losing from the decline in assets, they also lose due to currency depreciation. For this reason, MSCI recommends subjecting portfolios to stress tests based on scenarios already known in history.

The Risk of a Persistent Pattern and a Bit of Historical Perspective

MSCI emphasizes that “Triple-Red” episodes were more common before 2000 and almost disappeared for nearly two decades, which led many investors to take favorable correlations (equities vs. bonds) and the role of the dollar as a safe haven for granted. The key risk, according to the text, is not only that a one-off episode occurs, but that it transforms into a regime (a persistent pattern lasting months or years), because in that case diversification becomes structurally eroded.

To understand when and how a Triple-Red regime can last, MSCI analysts look to history and highlight two precedents where the dynamic was not a simple market “scare.” The first is the stagflation of the 1970s (1973–74): a context of external shocks (then, the oil embargo), high inflation, and authorities caught between fighting inflation or supporting growth, which weakened the credibility of economic policy and favored simultaneous sell-offs across multiple asset classes.

The second precedent is the period following the Plaza Accord in the late 1980s, when coordinated efforts to weaken the dollar coincided with equity market tensions (including the 1987 crash) and upward pressure on bond yields.

Based on this framework, the report highlights that the worst historical episode for a foreign investor in a typical 60/40 portfolio occurred in 1987, with an approximate cumulative drawdown of 31% over four months.

Seeking a Predictive “Stress Testing” Framework

To quantify impacts, MSCI uses its predictive “stress testing” framework and applies the shocks to a diversified global portfolio combining global equities, bonds (mainly U.S.), and real estate, among other components.

The report notes that for a dollar-based investor there may be some relative “relief” from certain European assets, because euro appreciation would increase the dollar returns of European bonds. However, the impact changes drastically for European investors: when translating results into local currency, the estimated decline of the “composite” rises to around 19% in euros and 20% in Swiss francs, precisely because dollar depreciation amplifies losses in U.S. assets.

The final message is one of risk management: MSCI suggests that, instead of treating recent episodes as transitory anomalies, investors could benefit from stress-testing their portfolios against sustained correlation breakdowns, reviewing currency exposures (and the implicit reliance on the dollar as “insurance”), and identifying allocations more resilient to a stagflation-type environment.

Despite the growing use of digital investment tools, investors continue to rely on human financial advice, according to the latest edition of Cerulli Edge – U.S. Advisor Edition. Even among younger, tech-savvy investors, demand for formal advice remains firm.

Online tools make it easier to track budgets and manage investments, but investors are still reluctant to fully delegate their financial decisions to these platforms. Cerulli’s research indicates that only 25% of investors in their 50s, and just 9% of those aged 70, prefer an exclusively online advisor.

Although younger households are more inclined to opt for digital interaction, only 36% of those who consider online tools essential for tracking their financial goals also prefer exclusively digital advice. By contrast, 46% state that they prefer to have a human advisor as part of their financial relationship.

“Affluent investors continue to value having a trained financial professional by their side with whom they can discuss their plans and goals. In addition, retail investors place great importance on their financial provider having a robust website that allows them to easily access and view their entire financial situation,” commented John McKenna, senior analyst at the consulting firm.

Among the most valued tools, account aggregation stands out as key. This resource, fundamental in financial planning programs for integrating external assets, is considered important by 72% of affluent investors. It is not only perceived as essential to the advisor relationship but is also actively used: 63% of these investors report having used online tools to better understand their financial situation.

Financial advisors who effectively integrate these digital tools, commonly used by their clients, will be better positioned to retain them and strengthen their relationships. “It is essential for advisors to ensure that their technology is comprehensive and easy to use, enabling in-depth conversations with clients and generating actionable and trackable insights,” concluded McKenna.

China begins the Lunar Cycle with the arrival of the Year of the Horse. In its culture, this animal is associated with dynamism, drive, and movement, three concepts that very well define the vision that international investment firms have of the Asian giant. Its starting point for this new year comes after having managed to close 2025 with 5% growth, although it shows some weakness in its domestic demand.

Its economic policy aims to sustain without unleashing excesses, while attempting to reorient toward consumption and technology/clean energy sectors. In addition, this year the 15th Five-Year Plan will also be launched, an essential roadmap that sets out the policies and direction of the country’s next stage of development. According to Fidelity International, “with greater clarity in strategic priorities, investors can expect more attention to be paid to execution, as policies translate into tangible actions in key sectors over the coming months.”

According to the asset manager’s view, although controlled stabilization remains the working hypothesis for China’s macroeconomic environment, the initial signs of supportive policies for domestic demand increase the probability that reflation will prevail in 2026. “An important aspect is that the risk of a severe slowdown appears limited, as the external environment remains generally favorable, and the real estate sector is showing new signs of stabilization. Deflationary pressures are expected to persist in the short term, as a lasting recovery in domestic consumption has yet to take hold. For now, we believe that the main driver of real growth continues to be supply,” they explain in their latest report.

Fiscal Policy, Monetary Policy, and Currency

In the opinion of Norman Villamin, chief strategist at UBP, China could surprise to the upside thanks to greater fiscal stimulus. “In addition, the progressive internationalization of the renminbi is emerging as a relevant structural element, reinforcing its role in trade and global financial flows. If the 2026 rate cut is added to this environment, the market would have an additional tailwind, in a context of more flexible monetary and fiscal policy, comparable (though not identical) to the period following the pandemic,” explains Villamin.

His view is that the country could benefit from two combined factors: greater dynamism in China’s trade and structural weakness of the dollar. “This dollar trend, together with inflation divergence, more contained in China and more persistent in the U.S., supports the appreciation of the CNY (Chinese yuan). Within this universe, emerging debt offers attractive opportunities, especially in countries integrated into China’s economic orbit. However, the central axis goes beyond the economic cycle. Global competition is no longer limited to the commercial or political sphere, but is shifting toward control of strategic resources. Beyond the AI narrative, the true investment driver will be the physical assets that make it possible: metals, energy, and infrastructure,” adds the UBP expert.

The Trade Issue

The country’s reality is that, despite rising tariffs and the uncertainty generated by the Liberation Day shock, the composition of Chinese growth is increasingly tilting toward trade. In fact, the share of net trade in GDP growth rose to nearly 33%. In addition, a greater proportion of growth was attributable to consumption, which contrasts with weak retail sales, as spending on services came to the rescue.

“In 2025, for the second consecutive year, the net trade balance was the main engine of growth, helping to offset the lower contribution of investment to GDP. While companies cut prices to support exports, household spending on services was the forgotten hero. Increased government transfers have provided a small offset, but wage and salary growth and substantial savings largely explain spending,” says Robert Gilhooly, senior economist specializing in emerging markets at Aberdeen Investments.

Indeed, growth in disposable income continues to outpace nominal GDP growth, thanks to increased government transfers and despite the sharp moderation in real estate income. The strength of equity markets may also be helping to lift sentiment, although household exposure to equities remains low.

As Gilhooly points out, the record trade surplus of $1.2 trillion has made the People’s Bank of China (PBOC) more comfortable with a stronger currency. “However, in addition to doubts about the rest of the world’s tolerance for further expansion of China’s share in global trade, there is a risk that this could trigger deflation, especially while excess capacity persists. Accepting a stronger currency could boost foreign investor enthusiasm for Chinese assets. It remains to be seen whether the continued fall in housing prices and lower-yield term deposits will encourage households to reallocate their investments toward the stock market,” adds the Aberdeen Investments expert.

Chinese Equities

For investors, Chinese equities remain an attractive asset. The MSCI China index rose 31.4% in 2025, outperforming both the U.S. stock market and developed markets. Innovation-driven themes, especially technology and AI, fueled this rebound following the announcement of the DeepSeek AI model at the beginning of 2025. The positive momentum continued, reflected in the IPOs of Chinese AI and technology companies in Hong Kong at the end of 2025, which attracted strong investor interest.

According to Isaac Thong, senior investment director for Asian equities at Aberdeen Investments, now that China’s economic growth is stabilizing at a long-term rate of 5%, companies are shifting their priorities and seeking a better balance between increasing profits and distributing them to shareholders. “This has been supported by government initiatives on corporate governance, which have encouraged higher payouts. Many companies have begun to pay higher dividends, opening up new opportunities for income funds,” notes Thong.

Significantly, according to LSEG data, total cash dividends from the country’s 2,000 mid- and large-cap companies reached a record 3.4 trillion yuan ($468.84 billion) in 2023. This figure increased by 1.2% in 2024 and could grow another 8.6% in 2025. As a result, dividends have become a more important component of shareholder returns, and these initiatives have also helped improve the overall quality of Chinese companies. “We believe companies have the capacity to pay higher dividends, which could attract more innovative Chinese companies into the universe of income-seeking investors. In this way, the opportunities before us continue to expand steadily,” highlights this Aberdeen Investments expert.

Finally, Fidelity emphasizes that growth-oriented sectors will drive the stock market. “As we move into the Year of the Horse, the Chinese market is beginning to show investors renewed dynamism. Liquidity conditions and capital flows remain favorable, both in the domestic A-share market and in China’s external markets, at a time when authorities continue to push a moderate policy agenda focused on supporting consumption, housing market stability, and structural reforms,” argues Stuart Rumble, Head of Investment Directing for Asia-Pacific at Fidelity International.

For Rumble, technology and innovation continue to present attractive opportunities, but with a view beyond AI and closer to robotics, autonomous driving, future mobility, and advanced manufacturing. “Alongside this, structural reforms, such as capital market liberalization, supply-side modernization, anti-involution measures, and policies to support private enterprise are helping to create a healthier, more innovation-friendly investment environment. These reforms are increasing efficiency in capital allocation and encouraging innovation-driven growth across various sectors,” concludes Rumble.

Multifonds, a global fund management software provider, and Ultumus, a SIX Group company specializing in ETF infrastructure technology, have announced a strategic alliance designed to enable management companies to expand rapidly in the growing ETF market. According to the companies, this collaboration provides Multifonds clients with direct access to Ultumus’ specialized ETF technology platform and its extensive global network of authorized participants and market makers, enabled through a preconfigured standard connector now available on the Multifonds platform.

With ETF assets growing at an unprecedented pace, the companies have identified that asset managers are increasingly seeking efficient ways to launch share classes in ETF format or convert existing mutual fund strategies into ETF vehicles. Therefore, they believe this alliance responds to that demand by combining Multifonds’ market-leading platform for fund administration and investor services, which currently supports more than $10 trillion in assets, across more than 40,000 funds and 35 jurisdictions, with Ultumus’ proven ETF operating infrastructure. “This alliance offers the market an integrated solution that removes the operational burden associated with launching and administering ETFs,” highlighted Oded Weiss, Chief Executive Officer of Multifonds.

Its comprehensive ETF infrastructure solution

According to the companies, the alliance also brings together complementary capabilities. On the one hand, Multifonds contributes its established fund accounting and investor servicing platform, used by 9 of the world’s 15 largest fund administrators; on the other, Ultumus provides specialized ETF infrastructure, including the COSMOS platform for creation and redemption processes, advanced PCF (Portfolio Composition File) calculation capabilities, and a well-established global network of relationships and distribution with authorized participants and market makers.

Together, the combined offering and connectivity enable end-to-end ETF operations, from fund accounting to trading and settlement, all on an integrated technology platform. The companies believe a key differentiating factor of the alliance is Ultumus’ strong network of relationships with European, Asian, and Canadian authorized participants and market makers, essential counterparties in the ETF ecosystem that enable efficient trading and liquidity provision. This network, they note, combined with Multifonds’ experience across more than 35 jurisdictions, provides asset managers and fund administrators with immediate access to the infrastructure needed to successfully launch and operate ETFs in global markets.

“The ETF market is evolving rapidly, and asset managers need partners who understand both the traditional fund administration business and the specific operational requirements of ETFs. Multifonds’ client relationships, combined with our specialized ETF technology and our market maker network, create a robust solution for firms looking to capture the ETF growth opportunity without having to build entirely new infrastructure,” said Bernie Thurston, Chief Executive Officer of Ultumus.

Driving industry transformation

Both firms maintain that this collaboration comes at a crucial moment for the asset management industry, particularly with the transition to the T+1 settlement cycle in Europe. According to them, recent regulatory changes allowing ETF share classes within mutual funds, together with investors’ strong preference for ETF structures due to their tax efficiency and lower costs, have accelerated demand for solutions that connect the mutual fund and ETF worlds.

“We are seeing a fundamental shift in how asset managers and fund administrators think about product structure. It is not just about launching new products, but about equipping existing fund ranges with the tools to evolve alongside market demand. Our collaboration with Ultumus delivers that capability at scale,” concludes Weiss.

State Street Corporation has announced that Mariner, a U.S. private equity-backed financial services firm, will implement the Charles River wealth management solution, a State Street company, to optimize its operations and support its long-term growth strategy, including its goal of expanding to 5,000 advisors.

According to the company, the objective of the implementation is to help Mariner operate more efficiently across its current network of more than 2,080 advisors, while establishing a centralized and scalable technology foundation designed to sustain continued growth without adding operational complexity or disrupting the advisor or client experience.

“Mariner is a rapidly growing wealth management firm and we are delighted to support it with a modern, centralized platform that strengthens the advisor experience. The Charles River platform is designed for firms operating at scale and helps them serve thousands of advisors on a single, flexible foundation built to support disciplined and consistent growth,” said John Plansky, Global Head of State Street Wealth Services.

In this regard, Mariner plans to leverage Charles River’s centralized technology to enhance portfolio management, advisor workflows, trading operations, custody data integration, and enterprise data management. The solution is designed to elevate operational efficiency, reinforce consistency across the firm, and enable advisors to devote more time to client relationships.

According to Marty Bicknell, CEO and President of Mariner, “this partnership reflects how we envision the next chapter of our company. It is designed to support our journey toward 5,000 advisors and beyond, while enabling a more unified and modern experience across the firm as we continue to grow.”

For more than 15 years, Charles River has provided integrated wealth management technology services to large global asset managers, aimed at optimizing operations, managing complexity, and supporting innovation in investment and advisory workflows.

“The centralized Charles River platform provides advisors with the tools they need to manage portfolios, operate efficiently, and work seamlessly across custodians and investment programs, including UMA, SMA, Rep-as-PM, and fund wraps. It is designed to reduce operational friction while giving firms the flexibility to grow on a single integrated platform,” said Swati Verma, Head of Wealth and Advisor Platforms at Charles River.

2026 is shaping up to be a year of balances. Global markets are riding this week between electoral risks, inflation data in the U.S., and geopolitical debates on security, while corporate earnings and signals from central banks add to a horizon filled with focal points.

In the opinion of Christian Gattiker, Head of Research at Julius Baer, markets begin the week managing a dense combination of political events, macroeconomic data, and corporate earnings. Specifically, he believes that investors will be particularly attentive to the evolution of inflation in the U.S. and geopolitical developments: “Macroeconomic attention is focused on Friday’s U.S. CPI report, which will serve as a key indicator to assess whether inflation continues to moderate gradually. Markets remain sensitive to any upside surprise that could call into question expectations of continued monetary easing later this year.”

According to Gattiker, “these releases will help determine whether corporate fundamentals can continue sustaining market sentiment in a context of persistent macroeconomic and geopolitical uncertainties.”

“This week’s January U.S. employment situation report will be important in shaping investors’ views on the trajectory of the labor market in the world’s leading economic power after the data released last week came in weaker than expected. The general expectation is that nonfarm employment will grow by 70,000 jobs, compared to 50,000 in December, that the unemployment rate will remain stable at 4.4%, and that average hourly earnings growth will moderate slightly to 3.7% year-on-year. Markets will be closely watching the nonfarm payroll figures given the weak job creation since May,” acknowledges Ronald Temple, Chief Market Strategist at Lazard.

For Hans-Jörg Naumer, Global Head of Capital Markets & Thematic Research at Allianz Global Investors, although global politics is increasingly defined by shifts in spheres of influence, financial markets are looking beyond the geopolitical risks that dominate headlines, such as the recent turmoil surrounding Iran and Greenland, and are focusing on macroeconomic data, corporate earnings, and the factors driving medium-term returns.

“After the strong results achieved in 2025, equity markets began the year with very positive momentum. Commodities also extended their gains, and gold and silver continued their upward trend for much of January, before greater turbulence emerged in the markets. In contrast, fixed income markets recorded more differentiated performance. European government bonds benefited from falling yields, while U.K. and U.S. sovereign bonds were under pressure,” adds Naumer.

Politics and Geopolitics

Certainly, the political backdrop remains at the forefront, marked by snap elections in Japan, along with general elections in Thailand, whose results could influence the direction of regional policy and investor sentiment in Asia. In the case of Japan, the landslide victory of the Liberal Democratic Party (LDP) of Prime Minister Sanae Takaichi provides her with a firm mandate to assert herself on legislative matters. “In early trading today, the yen appears unchanged from Friday’s close in New York. Investors’ focus will be on the magnitude of fiscal expansion. In particular, close attention will be paid to developments regarding the temporary reduction of the food tax promised during the election campaign,” notes Sree Kochugovindan, Senior Research Economist at Aberdeen Investments.

In addition, looking at the week’s agenda, geopolitics adds another dimension, as the Munich Security Conference is likely to intensify the debate on NATO’s strategic outlook and the war in Ukraine, underscoring the persistent uncertainty surrounding global security.

Central Banks: Focus on the Fed

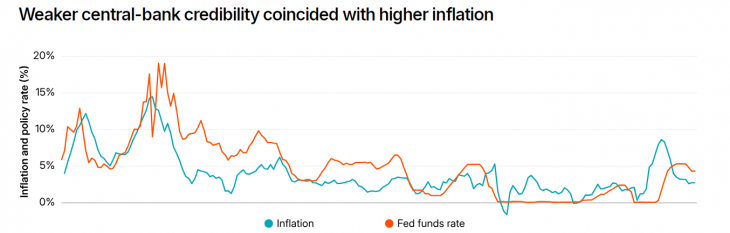

One of the drivers moving the market has to do with central banks. According to MSCI experts, market confidence in the independence of the Federal Reserve could prove decisive in 2026. “With inflation still above target and early signs of a weaker labor market, the pressure to ease policy risks clashing with the Fed’s mandate. Grand jury subpoenas issued to the Chair of the Federal Reserve have further added complexity to an already delicate monetary policy environment. When a central bank’s credibility is eroded, inflation can persist even as growth slows, leading to stagflation, a scenario in which bonds cease to diversify against equities,” they explain.

“Moreover, the Fed kept interest rates unchanged, as expected, at its January monetary policy meeting, with Governors Miran and Waller dissenting in favor of a 25 basis point cut. Uncertainty surrounding the independence of the Federal Reserve intensified at the beginning of the month following news that the Department of Justice subpoenaed the Fed and its Chair, Jerome Powell, in connection with the renovation of the Fed building. The situation has extended to the Senate, where Senator Thom Tillis, a senior member of the Banking Committee, has indicated his intention to block Fed confirmations until the investigation is resolved,” adds Marco Giordano, Investment Director at Wellington Management, regarding the noise surrounding the Fed that continues to hold investors’ attention.

Investment Opportunities

In this context, investment firms are also speaking about opportunities. For example, it is hard to ignore how Japanese equities rose sharply on Monday after Prime Minister Sanae Takaichi’s coalition secured a historic supermajority, unlocking fresh momentum for the so-called “Takaichi trade.”

In this regard, the message is clear: with political stability and reform catalysts in play, investors should be alert to further upside potential, as well as short-term episodes of volatility in bonds and the yen.

“We maintain our attractive rating on Japanese equities and see room for further gains, especially in sectors that benefit from domestic policies (defense, banks, real estate, and IT services) and global themes (energy, data centers, automation, and some auto sector stocks). As for the Japanese dollar/yen, authorities have already signaled a high degree of urgency regarding currency movements, which should help contain pressures,” says Mark Haefele, Chief Investment Officer at UBS Global Wealth Management.

At Capital Group, the focus is on how emerging markets are becoming the engine of industrial transformation on a global scale, thanks to strong investment in electric vehicles (EVs), robotics, and manufacturing related to artificial intelligence, including semiconductors. “The region is expected to account for nearly 65% of global economic growth by 2035. However, the long-term competitive advantage of emerging markets depends not only on excellence in the hardware segment, but also on their ability to advance toward innovation in software and systems,” they argue at the asset manager.

Finally, François Rimeu, Senior Strategist at Crédit Mutuel Asset Management, revisits one of last week’s standout topics: gold. Precious metals have been in the spotlight in recent weeks due to the exceptional movements observed in prices: a 25% increase between the end of the year and January 28, followed by a decline of more than 13% in the case of gold. The situation is even worse for silver, which has lost a third of its value after having risen by more than 60%.

“From our point of view, the rebound in gold (and, to a lesser extent, silver) is driven by several factors, some more relevant than others. The key factor appears to be the continuation of expansionary fiscal policies since the Covid crisis and the war between Russia and Ukraine. On the other hand, current geopolitical instability acts as another supporting factor for gold prices and, once again, recent developments do not point, in our view, to a decline,” explains Rimeu.

His main conclusion is that the catalysts that have been present over the past three years remain in place and that the recent correction is ultimately healthy, as it helps to eliminate more speculative investments.

This week, the dollar extended its losses following disappointing U.S. retail sales data. In the view of experts from investment firms, the weakening of the dollar is likely to continue, especially in a context of further rate cuts by the Federal Reserve (Fed).

Tim Murray, Capital Markets Strategist in the Multi-Asset Division at T. Rowe Price, outlines four reasons why he believes the U.S. currency will likely continue to weaken after nearly 16 years of steady appreciation: “The recent decline reflects a combination of structural and cyclical factors, suggesting that the move may have further room to run rather than representing merely a short-term correction. First, fiscal concerns are increasingly putting pressure on the currency. Second, monetary policy expectations are becoming a clear headwind. Third, political dynamics are influencing foreign demand for dollar-denominated assets. And finally, global capital flows are acting as an additional source of pressure,” Murray notes.

However, from a valuation perspective, this expert believes the dollar remains elevated relative to its own history and against most major currencies. “Even after its recent weakness, it remains expensive by historical standards,” he adds.

The outlook of Axel Botte, Head of Market Strategy at Ostrum AM (an affiliate of Natixis IM), is similar: “The greenback will likely face structural headwinds in the coming years. The dollar’s carry against the euro will fall to around 100 basis points and will turn negative against the pound sterling and the Australian dollar this year.” For Botte, the dollar’s status as a safe-haven asset is being called into question and it may decline at the same time as U.S. equities and bonds.

“This is the phenomenon known as ‘sell America,’ which has shown that the dollar is no longer the ultimate safe-haven currency. U.S. exceptionalism will also be tested as the AI boom comes under greater scrutiny from investors. Dollar hedging flows could increase, and valuation metrics suggest that the greenback has room to adjust downward,” Botte adds.

Investor options

If this outlook materializes, the dollar’s rate advantage over other currencies would consequently erode. In addition, global investors’ efforts to diversify could add further downward pressure and open up tactical opportunities in higher-yielding currencies. “With dollar weakness likely to persist, investors should review their currency allocations and consider the benefits of diversification. For those with an affinity for gold, we consider an allocation of up to a mid-single-digit percentage within a diversified portfolio to be appropriate,” says Mark Haefele, Chief Investment Officer at UBS Global Wealth Management.

In Murray’s view, for investors considering ways to potentially hedge against a weaker dollar, increasing exposure to assets outside the U.S. may offer diversification benefits. “Emerging market and local currency bonds can benefit directly from dollar depreciation, while international equities provide both equity returns and potential currency gains. After years of dollar strength that led some investors to reduce their international exposure, a sustained period of weakness could encourage a reallocation toward global markets.”

Undoubtedly, however, the key task for managers and investors will be to continue monitoring the behavior of the dollar. The U.S. asset manager Muzinich & Co reminds that “in the macroeconomic sphere, the key indicator to watch will be the U.S. dollar, as a sovereign currency is often seen as a barometer of both the health of the economy and confidence in the administration that governs it.”

Fund manager Schroders has announced an agreement with Nuveen under which the U.S. firm will acquire the British company for £9.9 billion ($13.5 billion). The founding family would sell its shares, bringiqng an end to an era for the 222-year-old firm.

Schroders shareholders will receive 590 pence per share in cash, plus dividends of up to 22 pence, valuing the company at 612 pence per share. This represents a 34% premium to Wednesday’s market closing price.

Nuveen stated that the deal would create a leading platform for public and private assets with greater geographic reach across the Americas, Europe, and Asia-Pacific. The firm said it has received irrevocable commitments in support of the deal from Schroders’ largest shareholder group, which controls 41% of the shares through various family trusts.

The offer document states that the businesses of Nuveen and Schroders are highly complementary and that the transaction “represents an opportunity to combine their strengths in order to accelerate growth, better serve clients, and create one of the largest active asset managers globally.” The combined group will have nearly $2.5 trillion in assets under management, balanced evenly between institutional and wealth channels. According to the proposed timetable, the transaction is expected to become effective during the fourth quarter of 2026.

BNP Paribas served as financial adviser to Nuveen, while Wells Fargo and Barclays advised Schroders.

Elizabeth Corley, Chair of Schroders, commented that the Group resulting from the combination of Schroders and Nuveen “will bring together two successful companies with shared values and highly complementary strengths to create a new global leader in public and private investment management. Following Schroders’ tradition, London will remain the center of the new combined entity, and the transaction will provide an attractive cash premium to our shareholders, reflecting the value of our business and its future prospects. The Schroders Board is confident that this is the right step for our shareholders, clients, and employees.”

For his part, Richard Oldfield, Group CEO of Schroders, stated that “in a competitive environment where scale can help deliver benefits, we see in Nuveen a partner that shares our values, respects the culture we have built, and that we believe will create exciting opportunities for our clients and employees.” The executive added that the transaction “will significantly accelerate our growth plans to create a leading public-private platform with broader geographic reach and a strengthened balance sheet. Together, we can create an exceptional opportunity to provide clients with a broad range of high-quality investment solutions that meet their evolving needs.”

Likewise, William Huffman, CEO of Nuveen, stated that through this “exciting transformational step for our two distinguished firms, we look forward to welcoming Schroders to the Nuveen family. By bringing together our platforms, capabilities, distribution networks, and complementary cultures, we will create an extraordinary opportunity to enhance the way we serve our collective clients through access to new markets, a strengthened product offering, and a greater depth of investment talent.” He also said that the transaction “is intended to unlock new growth opportunities for institutional and wealth investors worldwide, equipping our leading and differentiated public-to-private platform with a broader global presence,” according to the transaction statement.

Schroders CEO Richard Oldfield will remain at the helm of the firm following the closing of the deal. London will serve as the headquarters of the combined group outside the United States. Nuveen and Schroders will assess opportunities for collaboration and effective integration during the 12 to 18 months following completion of the transaction. During that period, Schroders is expected to continue operating as an independent company.

Investment managers’ budgets for alternative data will continue to increase this year, consolidating the strong growth of the past two years, according to new research by Exabel and BattleFin, two platforms specializing in alternative data.

Around 85% of the investment managers and analysts surveyed in the global study state that their budgets will increase this year, and 33% foresee substantial growth, according to the report “Alternative Data Buy-side Insights & Trends 2025” by Exabel and BattleFin. This increase adds to the recent expansion of budgets. The study, which included fund managers in the U.S., the U.K., Hong Kong, and Singapore with a total of $820 billion in assets under management, revealed that 43% of respondents reported a budget increase of between 50% and 75%, while 36% indicated that their budgets grew between 25% and 50% during the period analyzed.

The report by Exabel, which was acquired by BattleFin in December of last year, identified that one of the key areas of budget growth is likely to be investment in third-party software systems for data analysis. Currently, 66% of the firms surveyed use third-party software as part of their solutions, compared with 51% that use internally developed systems and 51% that use systems provided by data vendors. However, the research also revealed that 59% of respondents still use basic tools and legacy systems, such as Excel and Tableau, to analyze alternative data.

This landscape appears to be changing: 85% of respondents predict that their use of third-party systems will increase over the next five years, and 15% expect a drastic increase in their adoption for data analysis. The main reason is their greater cost-effectiveness, mentioned by 87% of respondents. In addition, 62% believe that these systems offer a more consistent way of working with different types of data, while 52% consider them more effective than internal systems.

In fact, senior management at the firms surveyed supports the increase in budgets: 98% state that they are very or fairly committed to the use of alternative data for investment research. Likewise, 84% have a head of alternative data on their teams, while only 11% admit not having one.

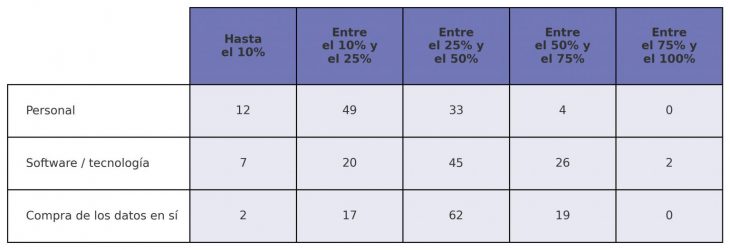

When allocating budgets for the acquisition and management of alternative data, the survey revealed that approximately 62% of firms allocate between 25% and 50% of their resources to purchasing data, while 45% indicate that their firm allocates between 25% and 50% of the budget to technology and software. And 49% indicated that their firms allocate between 10% and 25% of the budget to hiring staff to analyze and manage alternative data.

In light of these results, Tim Harrington, CEO of BattleFin & Exabel, commented: “The demand for alternative data continues to grow globally, with investment managers increasing their budgets year after year both to acquire and to manage a growing variety of datasets. The main challenges include resource allocation, data standardization across different sources, and the use of third-party analytical tools. We are committed to harnessing the power of alternative data to deliver actionable insights and generate value. In today’s dynamic market environment, accessing high-quality data is crucial to gaining a competitive advantage and unlocking alpha.”

Below is a table showing how the firms surveyed distribute their budgets for the acquisition and management of alternative data.

Balanz USA has a new key position: Federico Francia is the new Head of Wealth Management for its Latin America-focused wealth division based in Miami.

“In this role, Mr. Francia will lead the firm’s wealth management strategy across the Latin American region, further strengthening Balanz USA’s commitment to offering personalized investment solutions to its clients,” the Argentine-headquartered firm told Funds Society.

Federico Francia steps into his new role this February 2026, after working for more than eleven years at Puente Servicios Financieros, where he held positions such as Senior Financial Advisor (also in Miami), Team Leader, and Financial Advisor Private Banking.

“With more than 11 years of experience, today it’s time to say goodbye to Puente, a firm that allowed me to learn, grow, and develop in the Wealth Management industry. Thank you to all the colleagues, clients, and friends who accompanied me on this journey, both in Uruguay and the United States. It has been a true pleasure to share this path with you,” Francia shared on LinkedIn.

The new Balanz hire also worked at SURA Uruguay and HSBC, always in the wealth management sector.

The professional holds an MBA from EADA Business School and FINRA Series 66 and 7 licenses.