Photo courtesyJohn Cervantes, CFA, new partner and senior investment advisor at Prime Capital Financial

Prime Capital Financial announces the appointment of John Cervantes, CFA, as a partner and senior investment advisor at Crossvault Capital Management in San Antonio, Texas.

Cervantes brings nearly 20 years of experience in financial planning and investment management to the team, according to the firm information.

“With Prime Capital Financial’s extensive resources and the expertise of the Crossvault team, I look forward to providing greater value to my clients, helping them achieve their financial goals,” Cervantes said.

He previously served as executive director and investment advisor at Texas Capital Bank and has held senior roles at Merril Lynch, USAAA, and JPMorgan Chase Bank.

Cervantes holds a Bachelor of Business Administration in Finance from The University of Texas at San Antonio.

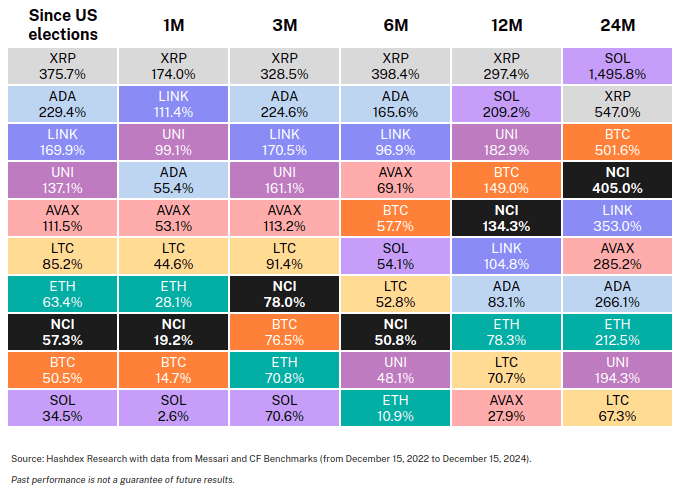

2024 was a year of transition for the cryptocurrency universe. According to Hashdex, this market went through a recovery cycle following a turbulent 2022 marked by bad actors and fraudulent activities. Reflecting on the past year, they believe crypto assets experienced a recovery phase and the beginning of a bull market. A key turning point was the U.S. election results and Donald Trump’s victory. Evidence of this is the Nasdaq Crypto Index, which has risen more than 57% since November 5, 2024, driven by widespread optimism about the future direction of U.S. digital asset policies.

“We believe the current investment case for bitcoin and other crypto assets remains strong. The steady demand from institutional investors, advancements in infrastructure, and a regulatory environment set to improve significantly in 2025 are positioning this asset class for what could be its strongest year on record,” said Samir Kerbage, CIO of Hashdex. In his opinion, crypto assets tend to follow a cycle of four years that includes a bullish phase lasting approximately 12 months, followed by a bear market lasting one year, and then a recovery period spanning two years. In the last two bull markets, altcoins (that is, everything except bitcoin) have significantly outperformed the largest crypto asset, according to Hashdex.

“I believe we have entered a bull market, reinforced by the macroeconomic environment and the U.S. election results. But another indicator of a bull market is the superior performance of the Nasdaq Crypto Index compared to bitcoin. Over the past three months, the index has outperformed bitcoin (78% vs. 76.5%) and, since the elections, the Nasdaq Crypto Index has outpaced bitcoin by 6.8%,” added Kerbage.

2024 was a year of transition for the cryptocurrency universe. According to Hashdex, this market went through a recovery cycle following a turbulent 2022 marked by bad actors and fraudulent activities. Reflecting on the past year, they believe crypto assets experienced a recovery phase and the beginning of a bull market. A key turning point was the U.S. election results and Donald Trump’s victory. Evidence of this is the Nasdaq Crypto Index, which has risen more than 57% since November 5, 2024, driven by widespread optimism about the future direction of U.S. digital asset policies.

“We believe the current investment case for bitcoin and other crypto assets remains strong. The steady demand from institutional investors, advancements in infrastructure, and a regulatory environment set to improve significantly in 2025 are positioning this asset class for what could be its strongest year on record,” said Samir Kerbage, CIO of Hashdex.

A key area, according to the entity, is smart contract projects—platforms that will enable users to conduct transactions involving not only information but also value and ownership. Hashdex estimates that these platforms and applications will outperform bitcoin over the next 12 to 18 months, as they compete for users and lay the foundation for decentralized applications.

“Thanks to the infrastructure developments we have seen in this area in recent years, new applications are emerging in fields such as artificial intelligence, video games, and many others as tokenization continues to expand. We also believe that new regulatory advances in 2025 will be more beneficial to these applications than to bitcoin specifically, given that bitcoin already has regulatory clarity and a well-developed capital market structure, with the growth of ETFs, options, and futures,” Kerbage explained.

In the U.S. and Europe, this legislative and regulatory clarity benefiting altcoins may include market structure legislation, as proposals like FIT21 aim to eliminate ambiguities regarding crypto assets’ status as commodities or securities, while creating registration pathways that could drive adoption in the U.S.

According to the latest report from Sygnum, a global banking group specializing in digital assets, relatively small institutional investor inflows into bitcoin ETFs could have a disproportionate impact on the market due to limited liquid supply. Their analysis of recent ETF flows suggests that every $1 billion inflow (approximately 0.1% of Bitcoin’s market cap) corresponds to price movements of 3-6%, with larger inflows showing greater price sensitivity.

The report predicts that this multiplier effect could be amplified if major institutional investors—including sovereign wealth funds, endowments, and pension funds—begin making allocations. Some U.S. state pension funds have already invested in crypto assets, and several states have introduced bills encouraging pension funds to consider cryptocurrency allocations. With the size of assets managed by these investors, even conservative estimates represent a larger wave of inflows than experienced in 2024 with the launch of spot cryptocurrency ETFs in the U.S.

“Many traditional institutional investors, those with the largest volumes of assets under management, are just beginning their foray into cryptocurrencies. Our analysis shows how even relatively modest allocations from this segment could fundamentally alter the crypto asset ecosystem. With greater regulatory clarity in the U.S. and the potential for Bitcoin to be recognized as a reserve asset for central banks, 2025 could mark a significant acceleration in institutional participation in crypto assets,” said Martin Burgherr, Chief Clients Officer of Sygnum Bank.

Stablecoin legislation, particularly the implementation of MiCA, will also play an important role by driving stablecoin adoption in the U.S. and Europe, expanding their use beyond emerging markets.

The repeal of SAB121, allowing U.S. banks to hold cryptocurrencies for their clients, is expected to enable banks and brokerages to expand their cryptocurrency trading and custody offerings, benefiting altcoins in particular. Additionally, new ETF launches under the new SEC chair are raising hopes for more approvals, including ETFs for indices and individual assets like Solana and XRP. Although uncertainty persists, the availability of new assets with ETFs as access points is highly positive.

Altcoin Use Cases

According to Kerbage, in addition to bitcoin evolving as an emerging digital store of value and smart contract platforms becoming a new way to exchange information, value, and ownership, three other altcoin use cases are expected to benefit over the next year:

DeFi: Projects aimed at creating an internet-based financial system, operating on smart contract platforms, will establish a new global capital markets infrastructure for payments. Stablecoins and tokenized money market funds are the first major use cases.

Web3: A new iteration of the internet that will enable users to own their data and make the web decentralized and more useful for innovations like AI agents and other advancements.

Digital Culture: An emerging digitally native generation will drive greater demand for owning digital assets and collectibles, with video games as the first natural application.

“If we compare cryptocurrencies to the internet, this industry is like the internet in the 1990s, and bitcoin could be compared to email—the only application most people have heard of. However, if we fast-forward 20 years, although email remains very useful, it has not been the internet application that has created the most value for society. We believe this perspective could apply to how bitcoin is currently perceived in relation to cryptocurrencies,” Kerbage concluded.

2024 marks 15 years since Antonio Zegers, Santiago Valdés, and Roberto Loehnert created Venturance Alternative Assets, an asset manager specializing in alternatives that has carved out its space in the Chilean financial ecosystem. Looking ahead, the plan is to leverage the experience their investments have brought them to launch new strategies in venture capital and growth equity, in addition to taking advantage of opportunities from the boom in private debt.

“As a management company, we are advancing in all areas,” describes Zegers, general manager of the investment firm – which has around 350 million dollars in AUM – in an interview with Funds Society. In particular, the areas of greatest interest to the firm are private equity and private debt, with new launches in mind, supported by the good results of two exits made in 2024.

In venture capital – one of Venturance’s flagship areas – they have two funds in operation: FIP Alerce, a private vehicle in the investment process, and Zentynel I, a fund focused on biotechnology and domiciled in the U.S. About this last vehicle in particular, Zegers highlights that “it has advanced very quickly in its placement and is a niche where we have adapted quite well.”

For its part, in growth equity, they have four strategies, according to their online portal. Two are private investment funds (FIP): Endurance I and Venture Equity, and two public funds: Outdoors and SAAS HR. In this area, the firm’s strategy is to take medium-sized companies, in the growth stage, and make them “as professionalized as possible,” describes the CEO of the asset manager.

New Launches

“In 2025, we are going to launch the second Zentynel fund, to continue that strategy,” Zegers anticipates, expecting it to be around 30 million dollars.

Regarding the portfolio, the executive notes that “like any venture capital fund,” the vehicle will be “well atomized,” with around 15 investments in the portfolio. The portfolio’s objective is biotechnology companies and related businesses, such as medical devices.

On the other hand, the firm is preparing to launch its third public growth equity fund. In this asset class, the objective is to strengthen the operation of the companies so that a strategic buyer is willing to pay for that added value and that the companies can move to a new stage of expansion.

“We have a group of base contributors who want to continue doing things with us,” says Zegers, adding that the new fund will replicate the strategy of the previous two iterations. Thus, they will focus on a profile of medium-sized companies, with revenues between 10 million and 50 million dollars, and expect the portfolio to have more than eight assets.

“We have already liquidated four assets, and the idea is to capitalize on our specialization in that area, for the next fund,” he notes. In May 2024, they sold the hamburger chain Streat Burger to the business group Copec, and in September, the mining equipment supplier Ancor Tecmin to the Canadian firm EPCM Group.

Opportunities in Private Debt

Outside of their private equity formulas, private debt – one of the most visible categories in the boom of alternatives in the Chilean fund industry – is a space they are watching closely. “It is the subclass of alternative assets that has been attracting the most attention lately,” says Zegers.

The area manages over 100 million dollars in strategies in dollars, Chilean pesos, and UF (a unit of account indexed to inflation). The hard currency fund, notes the CEO of the asset manager, has seen significant placement.

More recently, the professional also emphasizes that “what is capturing more attention lately is the UF fund,” as the drop in rates has left investors looking for inflation-indexed instruments.

For now, according to their website, the company has three funds: Lennox, which invests in working capital for an exporter, in dollars; FIP Fitz Roy/FI Tronador Deuda Privada, which finances Chilean SMEs via promissory notes with collateral; and FIP Navarino, which invests in short-term debt from a factoring, focused on invoices, leaseback, and loans.

What Lies Ahead

Looking further ahead, Zegers says that at Venturance Alternative Assets, they have “no specific bias.” The key, he explains, is to “stay very attentive” to take advantage of the opportunities offered by the markets in which they participate.

“There are subsectors that are gaining more prominence, such as UF instruments or biotechnology,” but it’s not something they predetermine.

For now, they plan to focus on their business lines: venture capital, growth equity, private debt, and real estate assets, where they manage six development funds.

However, new areas of interest are emerging. “Green infrastructure is a topic we have identified and want to reach, not as a fund directly, but as underlying assets,” he comments, as opportunities for their growth equity strategies. In addition, he notes there are some interesting spaces to explore, such as the world of energy storage.

Regarding more traditional infrastructure, they see less motivation. “We haven’t looked into it. It’s a topic, in our opinion, of greater specialization and size,” says the CEO, adding that while there are local players in that market, “the field is more dominated by foreign infrastructure funds.”

The fintech Fraccional (Fraccional.cl) has taken a step forward in the internationalization of its model, which is based on fractional real estate investment, expanding beyond the borders of Chile. This milestone involves a project in Miami, United States, a market they describe as highly profitable and dynamic.

According to Julián Blas, COO and co-founder of the company, in a press release, this initiative responds to demand for assets in the U.S. market—characterized by its stability and dollar-based denomination—from its users.

Fraccional’s model is anchored in crowdfunding to invest in real estate projects, significantly lowering the entry barrier for this type of asset. For the Miami project—a market historically reserved for high-net-worth individuals—investors can participate with as little as $300.

The system brings together individuals interested in investing in the fintech’s residential real estate development projects. Investors purchase shares through a joint-stock company, becoming partners. From there, in addition to property appreciation, contributors receive rental income from the properties.

A Market of Interest

The first development of the Miami project targets the upper-middle class and will be located in the northern part of the city. It replicates Fraccional.cl’s traditional model, where investors acquire fractions of real estate projects. “We maintain our essence: simple and accessible investment but with a global perspective,” Blas stated in the press release.

For its entry into the U.S. market, Fraccional will work with experienced real estate companies that meet strict requirements, such as having approved building permits. “We have chosen partners with whom we already have experience in Chile, such as Copahue and GFU, linked to successful developments in Ñuñoa, for instance,” Blas detailed.

The fintech emphasizes that Miami has shown sustained growth in housing demand, describing it as a high-appreciation market.

In 2023 alone, the city received over 54,000 migrants, contributing to a market with high turnover and projects that typically sell within one to two months. This dynamism has established Miami as a preferred destination for international investors, including Chileans, the company stated.

Plans for Expansion

The initial Miami project will be followed by a second initiative, focusing on the lower-middle class and located in the southern part of the city.

Looking further ahead, the fintech is also exploring opportunities beyond the U.S. market. It has its sights set on Latin America and Europe, particularly Spain, where it plans to launch coastal projects for residential and vacation purposes.

“With this strategic move, Fraccional.cl aims to establish itself as a key player in the fractional real estate investment market, offering attractive and accessible alternatives for small Chilean investors interested in dollarizing their assets and diversifying risks,” the press release concluded.

North America is undergoing a period of political and economic transition that may generate investment opportunities, especially in the markets of Mexico and the United States, despite the challenges. This is outlined in the Mexico 2025 Strategy report, prepared by the research team at Grupo Bursátil Mexicano (GBM) Casa de Bolsa.

The Latin American country recently experienced a change in government just over two months ago, with its first woman president in history, Claudia Sheinbaum Pardo. Meanwhile, in the United States, Donald Trump will take office for a second term on January 20, following a decisive victory in the election on November 5, 2024.

GBM highlights that a selection of Mexican companies reflects some of their most attractive valuations in decades, driven by a changing social and political landscape across the region. The brokerage firm supports increased portfolio exposure to defensive names, particularly in resilient sectors in such contexts, such as consumer goods and infrastructure.

The specialists behind the report identified three factors that could benefit Mexican equities next year:

Strong domestic consumption dynamics:

Mexico maintains robust internal consumption dynamics, supported by social programs and a rising wage base in recent years. Additionally, the purchasing power of remittances has regained momentum after the dollar strengthened against the peso in the second half of 2024.

Strategic location in North America and a robust manufacturing sector:

The region continues along a path of supply chain integration, facilitated by Mexican corporations with leadership positions not only nationally but also in the United States. GBM also identified investment commitments in the infrastructure sector for the 2020-2029 period that are 43.3% higher in real terms than the previous decade, strengthening the country’s medium- and long-term outlook.

Potential for growth in infrastructure and housing:

With the potential consolidation of nearshoring, the country may be at the beginning of a period of infrastructure growth. Additionally, the positive economic impact of this trend could increase the population’s purchasing power, triggering significant demand for housing.

The GBM analysts further note that the effect of nearshoring could boost exports and foreign direct investment even more, leading to significant economic benefits in the logistics and energy sectors.

Other analysts from investment firms have emphasized in their year-end reports that they continue to favor U.S. equities, at least in the early phase of Trump’s second term.

The investment world is defined by nuances that reflect local preferences, regulations, and the cultural characteristics of each region. Latin America is no exception, and operating in a market with such specific idiosyncrasies often means that clients of asset managers see the coordination between Iberia and Latam as an added value.

This brings significant advantages, as it allows for high-quality service with a strategic focus in the various countries where operations take place. Moreover, we hold a competitive edge over our European neighbors: a common language and a cultural connection that enable us to provide tailored service to meet each client’s needs.

However, when comparing the investment dynamics between Latin America and Iberia, clear differences emerge in both the nature of investors and the regulatory frameworks governing the markets.

Retail Preferences in Mexico, Brazil, and Beyond

In Mexico and Brazil, retail investors—including banks, independent advisors, and platforms—tend to favor local products with a conservative focus. In contrast, elsewhere in the region, as well as in Iberia, such investors predominantly opt for UCITs-compliant funds and ETFs.

Institutional Strength in Latin America

In the institutional segment, which includes insurers, pension plans, and family offices, Latin America stands out as one of the most advanced regions in the world. A prime example is the pension plans in countries like Chile and Mexico, where mandatory worker contributions have created a robust and sophisticated institutional ecosystem. In this ecosystem, pension funds play a fundamental role in asset management.

Regulation and Distribution: A Study in Contrasts

Regarding distribution, Latin America is characterized by the autonomy of its markets. Each country has its own regulations defining how financial products are distributed among investors. This heterogeneity contrasts with the uniformity in Spain and Portugal, where MiFID regulations unify financial market oversight across the European Union. While this facilitates cross-border operations, it may limit the personalization offered by the fragmented markets of Latin America.

Investment Preferences: Diverging Trends

Investor preferences, whether retail or institutional, also reflect these structural differences:

In US Offshore and South America, excluding Brazil, a significant portion of portfolios is allocated to U.S. assets, including fixed income, equities, mixed assets, and alternatives. There is also growing interest in diversifying beyond traditional funds into vehicles like ETFs or separately managed accounts (SMAs).

In Mexico and Brazil, the focus remains on local fixed income, supported by high interest rates, making this asset class a cornerstone of their portfolios.

Iberia’s Changing Landscape

In Iberia, the recent shift in European Central Bank monetary policy has influenced investor behavior. Investors are moving away from money market funds toward options offering greater added value, particularly in European fixed income, which now presents better prospects due to interest rate adjustments and inflation stabilization.

In equities, there is a trend toward diversification to reduce dependence on national indices often dominated by a few large companies. This strategy aims to mitigate risks associated with high concentration and improve returns by targeting sectors or regions less represented in traditional indices.

Investors are increasingly exploring active management strategies that prioritize companies with quality and value profiles. Simultaneously, thematic investments—such as technological transformation driven by digitalization and AI, or energy transition—are gaining traction. Additionally, emerging markets like India, often underrepresented in traditional portfolios, have captured the interest of Iberian investors due to their significant potential.

Shared Pathways and Future Opportunities

Despite their differences, Latin America and Iberia share a common path in fund management, as both regions lean toward products offering risk diversification and new sources of profitability. A shared vision can provide fertile ground for innovative investment strategies, supported by the commitment of global asset managers with strong local components. This approach enables the advancement of each country’s strategic plans.

Adapting to the specific characteristics of each market is crucial. Only in this way can asset managers in Spain deliver tailor-made services suited to the needs of clients on both sides of the Atlantic.

Authored by Javier Villegas, Head of Iberia & Latam at Franklin Templeton.

The U.S. Consumer Confidence Index by The Conference Board dropped 8.1 points in December, reaching 104.7, marking a decline compared to November, when Donald Trump won the elections.

Additionally, the Present Situation Index, based on consumers’ assessment of current business and labor market conditions, fell 1.2 points to 140.2, according to the report.

“While weaker consumer assessments of the present situation and expectations contributed to the decline, the expectations component experienced the most significant drop. Consumers’ views on current labor market conditions continued to improve, consistent with recent employment and unemployment data, but their assessment of business conditions weakened,” stated Dana M. Peterson, Chief Economist at The Conference Board.

On the other hand, the Expectations Index, which reflects consumers’ short-term outlook on income, business activity, and labor market conditions, fell 12.6 points to 81.1, just above the threshold of 80, which often signals a recession.

Compared to November, consumers in December were substantially less optimistic about business conditions and future income. Additionally, pessimism returned regarding future employment prospects after cautious optimism prevailed in October and November, Peterson added.

Adult Consumers Are the Most Pessimistic

Among age groups, the decline in confidence in December was led by consumers over 35 years old, while those younger than that range were more confident.

Among income groups, the drop was concentrated among consumers with household incomes between $25,000 and $100,000, while those in the lower and upper income brackets showed only limited changes in confidence. On a six-month moving average, consumers under 35 years old and those earning more than $100,000 remain the most confident.

In December, consumers were slightly less optimistic about the stock market: 52.9% expected stock prices to rise in the coming year, compared to 57.2% in November.

Similarly, 25% of consumers anticipated stock prices would fall, up from 21.7%. The proportion of consumers expecting higher interest rates over the next 12 months rose to 48.5%, but remained near recent lows.

The percentage of those expecting lower rates dropped to 29.3%, down from recent months but still relatively high, Peterson noted.

Merril Wealth Management announced the launch of its Ultra-High-Net-Worth Advisory Group, a team of over 25 specialists led by Rob Romano, Head of Capital Markets Investor Solutions. The group is dedicated to creating comprehensive wealth and investment solutions for UHNW clients. It will also assist advisors in drafting personalized portfolios, including custom asset allocation, multi-asset portfolio construction, and traditional and alternative investment manager selection according to the firm.

In addition to providing bespoke investment solutions, the team will serve as a point of contact for advisors, assisting them in tapping into the full range of Bank of America services stated by the firm. These services include custom lending, trust and estate services through Bank of American Private Bank, philanthropy, art services and family office solutions.

“The establishment of a dedicated group to better support ultra-high-net-worth client engagement is the latest example of how we are supporting our advisors as they serve clients and grow their businesses,” said Brian Patridge, Head of Investment Solutions Group Specialist.

The Kemper Foundation, a philanthropic partner of the Kemper Corporation, has announced the Read Conmigo School Impact Grants to support Spanish and English education in Title I elementary schools.

The program will provide up to 22 annual grants of $10,000 each to eligible schools in Los Angeles, Broward, Miami-Dade and Dallas. These grants aim to improve bilingualism, further academic achievement and promote multicultural understanding.

Eligible schools include Title I public and charter elementary schools in specific counties across California, Florida and Texas. Funds can be used for dual-language resources, technology upgrades, educator training and community engagement.

Applications are open through The Kemper Foundation’s grants portal from January 8 to March 9, 2025. This initiative builds on the success of the Read Conmigo Educator Grants. It emphasizes The Kemper Foundation’s commitment to closing opportunity gaps and equipping students with essential skills for a globalized world.