Photo courtesyJohn Kerschner, Global Head of Securitized Products and Portfolio Manager at Janus Henderson.

Janus Henderson expands its range of CLO ETFs with a new fund that invests in AA- and A-rated securities. According to the firm, this new vehicle complements the flagship Janus Henderson ETFs JAAA and JBBB. The Janus Henderson AA-A CLO ETF (JA) has secured $100 million in seed capital from The Guardian Life Insurance Company of America (Guardian), as part of the previously announced multifaceted strategic partnership between Guardian and Janus Henderson.

The fund aims to provide access to high-quality AA- to A-rated CLOs, with broad diversification benefits based on historically low daily volatility and low correlation with traditional fixed income markets. In doing so, the asset manager expands the firm’s successful CLO ETF franchise and its global leadership in this segment.

According to the firm, the fund will be managed by long-tenured portfolio managers John Kerschner, CFA, and Nick Childs, CFA, who bring decades of experience in securitized markets and a combined track record managing securitized ETFs, including JAAA, JBBB, JMBS, JABS, and JSI. In addition, Jessica Shill, who also manages JAAA and JBBB, will join the management team for JA.

“Securitized markets are proving to be a strength for investors at this time, offering competitive returns and diversification. JA seeks to enable investors to position portfolios for resilience and growth in a changing economic environment. Given the strong demand for Janus Henderson’s flagship CLO ETFs, we are excited to provide clients with access to another segment of the CLO market,” said John Kerschner, Global Head of Securitized Products and Portfolio Manager at Janus Henderson.

The firm emphasizes that this launch strengthens its CLO product range by offering a fund that aims to invest in instruments with a credit rating positioned between those of the firm’s JAAA and JBBB ETFs.

Insigneo has announced the addition of a team from Bolton Global Capital. According to the firm, this move represents a significant expansion of Insigneo’s presence in the Northeastern United States and adds top-tier talent to its flagship Park Avenue offices. “This strategic addition underscores Insigneo’s commitment to capturing a greater share of the international wealth market within the United States, as the team joins the firm with $500 million in assets under management,” they highlight.

The team is led by industry veterans Ruben Lerner and Ariel Materin, who join Insigneo as Managing Directors, along with Jennifer Ramos, who assumes the role of Vice President, Client Relations. Together, they focus on delivering tailored financial solutions for ultra-high-net-worth (UHNW) families and institutional clients, with particular expertise in Latin American (LatAm) markets. Their addition further strengthens Insigneo’s presence in New York and brings into its expanding network one of the largest teams originating from Bolton in the region.

Ruben Lerner began his career at Merrill Lynch before moving to Morgan Stanley and later serving as Managing Director at Bolton. Ariel Materin also held leadership roles at Bolton and developed a significant part of his career at Morgan Stanley, specializing in complex investment strategies for international clients. Together, they bring decades of experience and a strong track record in managing large client portfolios.

“The team’s commitment to the UHNW and institutional segments aligns perfectly with Insigneo’s mission to deliver a truly global wealth management platform. By establishing this team along the prestigious Park Avenue corridor, Insigneo is positioned to offer greater accessibility and local insight to its growing base of domestic and international clients,” said Alfredo J. Maldonado, Managing Director and Market Head for New York and the Northeastern region.

The firm notes that their addition also strengthens Insigneo’s position as one of the leading international wealth management firms. “By equipping top-tier investment professionals with advanced technology and a broad range of global investment solutions, the firm continues to support the complex needs of high-net-worth and institutional clients,” they state.

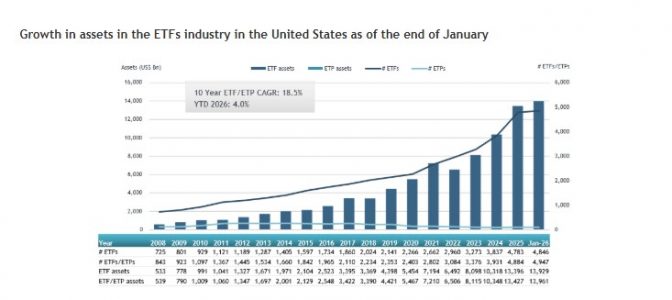

2026 begins strongly for the US ETF market. According to data published by ETFGI, assets in this class of vehicles listed in the US reached $13.96 trillion, after achieving the largest monthly inflows in history: $166.65 billion, compared to $9.025 billion in January 2025.

This means that in the first month of the year, industry assets increased by 4%, and the strong level of inflows could mark a clear trend for the rest of the year. Regarding flows, equity ETFs stood out with strong demand, gathering $78.14 billion, more than triple the $24.55 billion recorded in January 2025. Meanwhile, fixed income ETFs contributed $29.02 billion in net inflows, compared to $20.28 billion a year earlier. Commodity ETFs recorded $3.68 billion in net inflows, “a sharp turnaround from net outflows of $1.06 billion in January 2025,” explain ETFGI. Lastly, active ETFs also experienced significant growth, attracting $64.71 billion in net inflows, compared to $44.03 billion in January 2025.

According to ETFGI, iShares is the largest provider by assets, with $4.13 trillion, representing a 29.6% market share; Vanguard is second with $3.99 trillion and a 28.6% share, followed by State Street SPDR ETFs with $1.90 trillion and a 13.6% share. “The top three providers, out of a total of 462, account for 71.8% of the assets under management invested in the US ETF industry, while the remaining 459 providers each have less than a 6% market share,” they conclude.

Bank of America Private Bank announced the launch of Art Consulting, a new service designed to help Private Bank and Merrill clients navigate the complex and often opaque art market. The initiative seeks to offer independent and specialized guidance for the building and strategic management of collections.

The launch comes at a time when art is consolidating its role as a cultural and financial asset. The latest fall auction season in New York reached $2.2 billion in sales, reflecting growing investor interest in integrating art into their estate planning.

“Art collections stand at a unique crossroads. They are a profound means of personal expression and, at the same time, hold significant financial value,” said Drew Watson, Head of Art Services at Bank of America. “Our goal is to bring clarity to the market and help clients make informed decisions, whether they are acquiring their first piece or refining a multigenerational collection,” he added.

A structured approach for collectors

The new service offers comprehensive guidance tailored to each stage of the collecting process. It includes advice on art history, market dynamics, and emerging trends, and is structured through a multi-stage process covering initial consultation, strategy definition, execution support, and long-term advisory.

In addition, Art Consulting will provide discreet access to fairs, galleries, auctions, and private dealers, along with market updates and analytical resources that enable clients to make informed decisions.

The service will be led by Dana Prussian Haney for Private Bank clients and Caroline Orr for Merrill clients. This new offering complements the institution’s existing Art Services platform, which includes art-backed lending, consignments, estate planning, philanthropy, and access to exclusive art world events.

The initiative reinforces Bank of America’s positioning within the global cultural ecosystem, supported by its longstanding partnerships with museums and artistic institutions. In an environment where high-net-worth clients seek diversification, alternative assets, and multigenerational planning, art is consolidating its role as a tool that combines financial value, family legacy, and personal expression.

83% of investors plan to maintain or increase their investment in real estate compared to the previous year, in a context where Mexico is expected to regain momentum in 2026, supported by more contained inflation and a gradually more favorable monetary policy.

CBRE Mexico presented the results of its Investment Sentiment Survey in Mexico for the first quarter of 2026, a study that gathers investors’ expectations regarding their investment intentions, strategies, preferred sectors, and markets. Data collection was carried out between November 10 and December 10, 2025, and confirms an environment of greater resilience and discipline in the real estate market.

The Transportation and Logistics sector continues to lead the expansion phase, reinforcing the growth of the industrial sector, while Office and Retail show signs of stabilization, which together point to a solid and resilient outlook for the industry.

Regarding the factors driving investment, participants primarily highlighted the reduction in debt costs and the improvement in rental outlooks, supported by disciplined supply, resilient occupier demand, and greater interest in industrial and digital infrastructure, enabling more focused value creation and more precise financial evaluation of projects.

Although challenges such as Central Bank policy and an uncertain geopolitical environment persist, overall concerns have declined compared to 2025. With inflation around 3.6% and an expected GDP growth of 1.2% for 2026, the environment favors more disciplined execution, better price alignment, and selective value-focused transactions.

Looking ahead to 2026, 59% of investors expect to keep their allocation to real estate stable, while 37% plan to increase it. Notably, the percentage of those seeking increases above 10% rises to 20%, reflecting a shift toward higher-conviction growth strategies. Reductions in allocation remain marginal, at around 2%.

In terms of strategy, Opportunistic and Core position themselves as the favorites, configuring a “barbell” approach: opportunistic for higher returns and core as an anchor in low-risk assets to strengthen portfolio resilience.

By sector, Industrial and Logistics lead preferences with 35%, supported by net absorption of 2.46 million m² in 3Q 2025, compared to 2.33 million m² in 3Q 2021. Retail and Data Centers also strengthen their position with 18% and 8% of preferences, respectively, reflecting resilience and diversification in an environment of regional supply chain reconfiguration.

Regarding markets, Mexico City remains the country’s main investment destination, while Monterrey shows stability.

“The results of this survey confirm that the real estate market in Mexico enters 2026 with a stronger foundation, where pricing discipline, selectivity in transactions, and focus on strategic sectors such as Industrial and Logistics are setting the course for investment,” said Lyman Daniels, President of CBRE in Mexico, Colombia, and Central America.

For his part, Santiago Mijares, Head of Capital Markets Mexico at CBRE, commented: “We see investors combining Core and Opportunistic strategies to balance risk and return, in an environment where relative macroeconomic stability and resilient demand continue to provide value creation opportunities in the country’s main markets.”

The Financial Action Task Force (FATF or GAFI by its English acronym) has updated the list of high-risk jurisdictions for presenting serious deficiencies in systems for the prevention of money laundering and terrorist financing.

Following this update, and compared to the previous list published in October 2025, the FATF has included two countries, Kuwait and Papua New Guinea, which must improve their prevention systems, and has not removed any from the previous list. “The Financial Action Task Force periodically updates this list to encourage the countries or jurisdictions included to apply additional measures to protect the international financial system from risks related to money laundering and terrorist financing,” recall the experts at finReg360.

Therefore, the list, updated as of February 2026, of countries and territories at high risk for presenting strategic deficiencies in this matter is as follows:

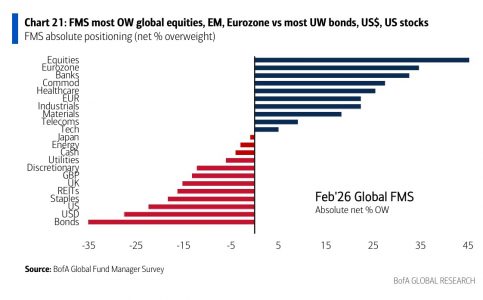

Bank of America’s February global fund manager survey confirms the rotation in asset allocation from the U.S. toward Europe and emerging markets. Looking at the absolute positioning of FMS investors (% net overweight), it is observed that, this month, investors are more overweight in equities, emerging markets, and the eurozone, and more underweight in bonds, the U.S. dollar, and the U.S.

Compared with history, that is, the past 20 years, investors are overweight the euro, commodities, and bank stocks, and underweight the U.S. dollar, cash, and REITs. In fact, investors’ overweight position in emerging market equities has risen to a net 49%, the highest level since February 2021. In addition, for the first time in 10 months, a majority of managers believe that small caps will outperform large caps (net 18%).

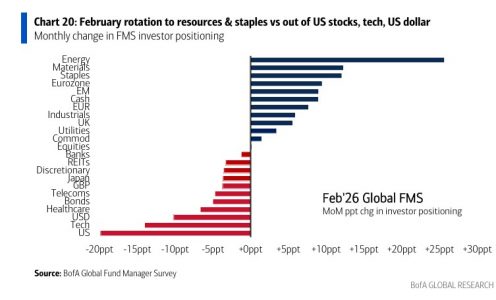

Another significant data point, which also shows a certain sector rotation, is that investors increased allocations to energy, materials, and consumer staples, while allocations to technology in U.S. equities and to the U.S. dollar were reduced. We may also be facing a change in perception regarding which investment style could perform better in the current context. “A net 43% expect value stocks to outperform growth over the next 12 months, the highest reading since April 2025,” the survey indicates.

Looking for further developments in asset allocation, the February survey also shows that the combined allocation to equities and commodities stands at a net 76%, the highest level since January 2022. “Historically, FMS allocation to equities and commodities (risk assets) has been correlated with the ISM manufacturing PMI. However, recently the two have diverged significantly, as manufacturing PMIs have lagged,” BofA explains. Finally, the survey highlights another shift, this time in currencies: “A net 23% is overweight the euro, a historic high since October 2004. In fact, FMS investors have been consistently overweight the euro since July 2024.”

A Look at Sectors and Market Capitalization

Investment firms had already detected this rotation, which we first clearly saw in the second half of 2025. In the opinion of Nenad Dinic, Equity Strategy Analyst at Julius Baer, the recent style and sector rotations show that the market is broadening beyond the concentration in mega-cap technology. “We view these ongoing rotations as a healthy development and expect them to continue in the short term,” notes Dinic.

For this expert, after three years in which U.S. mega-cap technology stocks drove most of the gains in the global market, equity markets are now experiencing a notable and healthy rotation. “We see these rotation developments as constructive and timely. Concentration risk is declining as crowded positions in the large U.S. technology complex are unwound, creating room for greater diversification. European equities stand out with expected earnings growth of around 8% and greater fiscal support, especially in cyclical and value-oriented segments. At the same time, maintaining an allocation to high-quality defensive exposures can provide stability. Asian markets, including Japan, India, and China, are also benefiting from a renewed capital rotation, while global emerging market equities are strongly supported by solid upward earnings revisions and the tailwind of an expected Fed easing,” he argues.

From Edmond de Rothschild AM, they believe that the main victim of this sector rotation is technology, and particularly software. “Concerns about the enormous investment needs in AI increased during the week and triggered sharp declines in U.S. technology giants, even among those that reported good results. In addition, improvements in the new Anthropic model, with its impressive capabilities in computer code generation, fueled fears about software companies’ ability to compete. As a result, the sector continued to lose ground and has already accumulated a drop of nearly 30% from the peak reached last October. The correction was especially severe in market segments exposed to retail investors, who are suffering significant losses—including those stemming from the massive sell-off in crypto assets—and are now forced to unwind positions across all risk asset classes,” they explain.

Anthony Willis, Senior Economist at Columbia Threadneedle Investments, believes it is too early to say how far this rotation will go, but acknowledges that we are witnessing changes in sentiment regarding how AI will evolve. “We are in an early phase of adoption and at the beginning of a long-term trend. Over time, greater clarity will emerge, but for now investors are being somewhat more cautious with respect to large technology companies. One positive aspect of the recent difficulties in the technology sector is that other sectors that had gone unnoticed are receiving greater attention. We have seen small caps, value stocks, and other regions demonstrate better performance, including Japan, Asia, and Latin America,” notes Willis.

Direction: Cyclical and Old Economy Stocks

For his part, Steve Chiavarone, Deputy CIO of Global Equities at Federated Hermes, agrees with this style rotation reflected in the latest Bank of America survey. According to his analysis, the market is moving in a more cyclical direction: “Cyclical value companies and old economy names are starting to respond and participate more. And given the volatility we have seen so far this year, defensive dividend-paying names are also starting to respond and, in many cases, lead.”

For Chiavarone, this broadening is something market participants have been waiting for over the past two years, and it is now clearly visible in large dividend-paying companies, which are also participating and, in many cases, leading. “This broadening is something market participants have been waiting for over the past two years, and we are now clearly seeing it in large-cap value, on both the cyclical and defensive sides. At the same time, small caps are beginning to outperform for the first time in several years,” he argues.

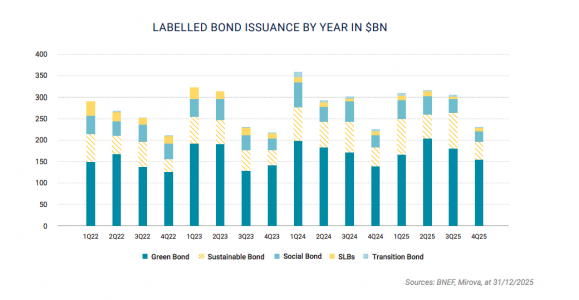

Sustainable investment has gone from enjoying great popularity to becoming a minor issue in global portfolios. However, the growth of sustainable assets has not been relegated to the “background.” This is the case with bonds labeled as sustainable. In fact, in 2025 it was confirmed that the labeled debt market is consolidating: issuance closed the year at around 6% above 2024.

According to Mirova in its latest report, adjusting for issuances by U.S. agencies, whose labeled debt issuance has surged over the past two years, volumes stood at around 1,170,000 million dollars. “The momentum that began in 2023 continued throughout 2024 and was maintained in 2025. The market is largely dominated by sustainable and green formats, while other formats have lost weight; they now represent 80% of the market, compared to 70% in 2021. However, although the transition bonds launched by Japan in 2024 struggled to gain traction in 2025, there is a possibility that they may gain renewed momentum in 2026. The ICMA framework published in October (B(ey)ond Green – October 2025) provides official guidelines for issuers and investors, thereby reducing the risk of greenwashing,” it notes as the main trends.

In the opinion of Johann Plé, of BNP Paribas AM, one of the most notable milestones of this asset class is its shift toward a more mature market, in which issuance levels are settling into a more predictable range. “This universe has moved from being a niche to becoming a consolidated offering. Ultimately, green bonds are firmly positioned as the backbone of the sustainable bond investment universe. In 2025 they continued to be the main driver of GSS growth (approximately 61% of total GSS issuance) and the primary source of new issuers, underscoring their central role in market expansion,” he notes.

In fact, he highlights that last year corporates once again were a major driver of issuance, accounting for 55% of total volume (compared to 51% in 2024). “This greater contribution from corporates not only reflects significant investments in renewable energy and energy efficiency, but also the credibility of the instrument, since most issuers are repeat issuers—that is, they issue more than one green bond,” adds Plé.

Main Trends

Mirova’s report highlights that Europe is showing signs of maturity, with significant penetration of sustainable bonds in certain sectors, while Asia-Pacific is consolidating its position as the fastest-growing region. At the same time, a reduction in the relative weight of the American continent is being observed. One of the most striking data points is the “greenium,” that is, the yield difference between a sustainable bond and a comparable conventional one. In this case, the document notes that it remains limited, “which may reduce the incentive for some issuers, especially in a context of potential scarcity of eligible assets,” it acknowledges in its conclusions.

In the opinion of Agathe Foussard and Lucie Vannoye, fund managers at Mirova (Natixis IM), its growth is likely to be in line with that of the conventional bond market, at around 10%, reflecting a broadly stable penetration rate. “The market should receive a boost from outstanding labeled bonds that are set to mature and require refinancing, as well as from a recovery effect in the utilities sector. On the other hand, the use of sustainable formats could be slowed by strong greenium compression and the risk of a shortage of eligible assets,” they explain.

By contrast, the report detected an unexpected slowdown in the issuance of sustainable sovereign bonds in 2025. Despite this, Europe continues to lead this segment, with several countries accounting for a significant portion of the market, in contrast to the weight of the United States in the traditional sovereign market and its limited presence in the labeled sovereign bond market. According to the report, there is no doubt that these sustainable bonds remain a public financing tool.

Catalysts for 2026

Looking ahead to this year, the BNP Paribas AM expert believes there are factors that should continue to support optimism around this asset class. “One is technical, due to the maturities expected in the coming years: the proportion of green bonds maturing is expected to increase by 30% in 2026 compared to 2025, reaching approximately 170,000 million dollars. These maturities will mainly come from banks and quasi-sovereign issuances and should support the market going forward, although there is no guarantee that all of these maturities will be refinanced through green bonds,” he notes as the main factor.

In addition, he adds that strong investments in renewable energy, grids, and green buildings should continue. Although themes such as climate adaptation and water (blue bonds) are emerging trends that are likely to attract greater interest, allocation will grow slowly in the short term partly due to structural factors. “In this context, 2026 could see a refocusing of the green bond market toward ‘historical’ issuers, more naturally aligned, with a higher proportion of readily accessible eligible assets, reflecting where investments and refinancing needs are actually occurring. Other issuers may choose to exit. A rebound in the APAC region could also be expected, as taxonomy updates over the past year may boost issuance,” states Plé.

Ultimately, Plé believes that, with a size roughly similar to that of the euro investment-grade credit market, investors should expect issuance to stabilize and to be more influenced by technical factors and investment schemes. “Overall, we would expect green bonds to remain the main driver of issuance growth, still dominated by European issuers and, more broadly, by euro-denominated issuances,” he concludes.

The U.S. Challenge

Beyond dramatic headlines predicting the slow death of this asset class, Mitch Reznick, global head of sustainable fixed income at Federated Hermes, believes there are factors that show it as an evolving and indelible part of the capital markets. “Starting with the labeled bond market, figures suggest that primary issuance in sustainable bond markets in 2025 may have reached 1.2 trillion dollars, representing a slight increase compared to 2024. What makes this figure particularly striking is that the number of labeled corporate bonds issued outside the U.S. has fallen by nearly 40%. However, in recent years there has been a notable boom in the U.S. in labeled social securitized bonds, which has remained strong well into 2025,” notes Reznick.

According to the expert, the state of Texas turns out to be one of the U.S. states—if not the leading one—that invests the most in and adopts renewable energy. For example, in 2024, renewable sources in Texas generated more than 166 GWh of energy, even ahead of California. In his view, this trend could continue after several legislative initiatives against renewables failed to pass this year. “California, along with Texas and a handful of southern states, continues to top the rankings in renewable energy investment,” he adds.

Finally, from a regulatory standpoint, the U.S. is reducing sustainability disclosure requirements, while Europe appears to be losing momentum in this area. “Meanwhile, the rest of the world is moving forward. In Asia, India, the United Kingdom, and Australia, the focus is on including ‘transition’ activities in disclosures and taxonomies. This inclusion makes a great deal of sense. If the global economy is to pivot in a way that generates economic value sustainably, a successful transition is essential,” concludes Reznick.

With more than three decades in the financial industry, from corporate banking to wealth management, Víctor Hugo Soto, Founder & CEO of Trust Beyond Family Office, built a proposal focused on Latin American high net worth clients in the US offshore segment, with a clear philosophy: understand risk, diversify, and always remain invested, identifying with the legacy of John Bogle, founder of Vanguard and inventor of index funds.

In an interview with Funds Society, he provides very concrete definitions: he does not believe in stock picking or market timing, considers that ETFs are today the most efficient tool for structuring diversified portfolios, maintains a cautious stance toward the rise of alternatives due to liquidity concerns, and warns that the main structural risk going forward is the high level of indebtedness of the United States and other developed economies, such as Europe, Japan, or China.

Even so, he maintains a constructive outlook for this year, with opportunities in fixed income, equities outside the U.S., emerging markets, and commodities, as well as a limited exposure to Bitcoin as a diversifying asset.

His career began 30 years ago at Banco de Crédito del Perú (BCP), the main subsidiary of Credicorp, where he worked for two decades. There he worked in corporate banking, conducted equity research, worked in the trading area, and was involved in portfolio management. “I learned how a bank operates from the inside, particularly from the corporate banking side, understanding how loans are structured and granted and how relationships with companies from various sectors are managed. Then I moved into the world of investments, where I deepened my knowledge of company valuation, fixed income analysis and trading, as well as the construction and management of investment portfolios,” he summarized to Funds Society.

The shift of Víctor Hugo Soto toward wealth management was consolidated in 2009, when Credicorp created its Multi Family Office segment and he was appointed to lead it. Later, his time at the Mexican firm INVEX in the United States allowed him to participate in structuring the wealth management offering for Latin American clients. And in 2021, he decided to launch his own RIA in Florida, registered with the SEC, seeking greater strategic independence.

Along those lines, the mission of Trust Beyond focuses on the client and on holistically addressing all of their wealth-related needs, integrating investment strategy, financial planning, coordination with tax and legal advisors, and generational support under a long-term vision, he explained.

Discretionary Management and Client Focus

Trust Beyond primarily works with clients with more than 5 million dollars, mostly Latin Americans, primarily Peruvians and Uruguayans, although it also has some U.S. clients. The firm operates mainly under discretionary mandates, with monthly or quarterly meetings, depending on the client’s needs.

For Víctor Hugo Soto, the core of advisory services is empathy and the absolute centrality of the client in the relationship. “The client is the most important thing. That is why you have to enjoy teaching and explaining how the world of finance works, so that the client understands how investment markets operate and makes decisions with greater confidence. Their peace of mind and satisfaction are always the priority,” he stated.

His philosophy is based on three pillars:

Clearly understand the client’s risk profile and needs.

Build a diversified and efficient portfolio.

Remain invested without attempting to anticipate market movements.

There is a rare but highly damaging phenomenon for portfolios called “Triple Red,” which consists of a simultaneous decline in U.S. equities, U.S. Treasuries, and the dollar. A note from MSCI analyzes the phenomenon and argues that a similar configuration could exist today: political uncertainty that deteriorates institutional confidence, price pressures linked to tariffs that complicate potential monetary easing, and the possibility of coordinated retaliation acting as an external shock channel.

A “Triple Red” episode breaks “classic” diversification and, for non-U.S. investors, adds a second blow: in addition to losing from the decline in assets, they also lose due to currency depreciation. For this reason, MSCI recommends subjecting portfolios to stress tests based on scenarios already known in history.

The Risk of a Persistent Pattern and a Bit of Historical Perspective

MSCI emphasizes that “Triple-Red” episodes were more common before 2000 and almost disappeared for nearly two decades, which led many investors to take favorable correlations (equities vs. bonds) and the role of the dollar as a safe haven for granted. The key risk, according to the text, is not only that a one-off episode occurs, but that it transforms into a regime (a persistent pattern lasting months or years), because in that case diversification becomes structurally eroded.

To understand when and how a Triple-Red regime can last, MSCI analysts look to history and highlight two precedents where the dynamic was not a simple market “scare.” The first is the stagflation of the 1970s (1973–74): a context of external shocks (then, the oil embargo), high inflation, and authorities caught between fighting inflation or supporting growth, which weakened the credibility of economic policy and favored simultaneous sell-offs across multiple asset classes.

The second precedent is the period following the Plaza Accord in the late 1980s, when coordinated efforts to weaken the dollar coincided with equity market tensions (including the 1987 crash) and upward pressure on bond yields.

Based on this framework, the report highlights that the worst historical episode for a foreign investor in a typical 60/40 portfolio occurred in 1987, with an approximate cumulative drawdown of 31% over four months.

Seeking a Predictive “Stress Testing” Framework

To quantify impacts, MSCI uses its predictive “stress testing” framework and applies the shocks to a diversified global portfolio combining global equities, bonds (mainly U.S.), and real estate, among other components.

The report notes that for a dollar-based investor there may be some relative “relief” from certain European assets, because euro appreciation would increase the dollar returns of European bonds. However, the impact changes drastically for European investors: when translating results into local currency, the estimated decline of the “composite” rises to around 19% in euros and 20% in Swiss francs, precisely because dollar depreciation amplifies losses in U.S. assets.

The final message is one of risk management: MSCI suggests that, instead of treating recent episodes as transitory anomalies, investors could benefit from stress-testing their portfolios against sustained correlation breakdowns, reviewing currency exposures (and the implicit reliance on the dollar as “insurance”), and identifying allocations more resilient to a stagflation-type environment.