The private credit default rate (PCDR) of Fitch Ratings in the U.S. increased to 5.8% for the trailing twelve months (TTM) through January 2026, up from 5.6% in December 2025. This marks the highest rate since its inception in August 2024.

The PCDR consists of two components: the Model-Implied Credit Opinion (MCO) default rate and the Privately Monitored Rating (PMR) default rate. In January, the MCO default rate increased from 4.5% to 4.7%, and the PMR default rate rose from 9.2% to 9.4%.

Fitch recorded 11 PCDR default events in February, nearly double the 2025 monthly average of 5.9. This approaches the peak of 13 default events recorded in November 2025.

Default activity spanned 10 sectors, two of which were broadcasting and media. Nine new unique defaulters emerged, with two repeat defaulters completing the 11 default events. Of the 11 default events, seven involved the introduction of payment-in-kind (PIK) interest in lieu of cash interest, three were related to distressed maturity extensions, and one resulted from an uncured payment default.

In the 12-month period through January, 74 unique defaulters generated 89 events. Interest payment deferrals and the introduction of PIK in lieu of cash interest drove 60% of defaults. Distressed maturity extensions accounted for 27%, and uncured payment defaults represented 6%. The remaining 8% involved bankruptcies, liquidations, and debt-for-equity swaps or out-of-court restructurings in which sponsors exited their investments.

Healthcare services providers remained the sector with the highest number of unique defaulters in the 12-month period through January 2026. Fitch’s sector outlook for healthcare services providers in 2026 is “neutral.” Positive demand growth supports a stable operating environment; however, stricter eligibility rules and redeterminations under the 2025 Medicaid Act are expected to reduce enrollment and increase the number of uninsured individuals.

Consumer products recorded eight unique defaulters, the second-highest number over the past 12 months. The sector’s default rate increased from 11.0% in December 2025 to 12.8% and more than doubled from the 6.1% recorded in January 2025. Fitch expects weak consumer conditions to limit transaction volumes in the sector, particularly for discretionary goods, as highlighted in the U.S. Consumer Products Outlook for 2026.

Technology software, the third-largest PCDR sector by number of issuers, recorded only three unique defaults in the trailing twelve months (TTM) through January 2026. The sector’s default rate declined from 7.5% in January 2025 to 1.9%. Fitch expects risks for the software and cloud services industry to emerge primarily over the medium term, according to the Software and Cloud Services Outlook for 2026. While AI could lower barriers to entry for new competitors, the mission-critical nature and high switching costs of many enterprise software products continue to protect incumbent operators.

iShares, Amundi, Vanguard, Invesco, and Xtrackers outpaced their rival ETF issuers in 2025 thanks to strong asset-gathering momentum and new launch activity, according to the new ranking published by ETF Stream. The study, titled ETF Issuer Power Rankings 2025, concluded that the trio of U.S. asset managers recorded significant relative progress compared with their competitors in the European listed ETF market.

The report reached this conclusion based on its own methodology, which evaluates five metrics over a 12-month period: flows (absolute and relative in 2025); trading (cumulative volume and volume relative to the number of ETPs); revenues (absolute fee income and revenue relative to the number of ETPs); activity (number of ETP and strategy launches); and presence (absolute flows by product class).

According to the report, the world’s largest asset manager, BlackRock, tops this issuer ranking for the first time after not only surpassing its own results from previous years, but also recording in 2025 more net inflows and higher trading volume in its European ETF business than its next four competitors combined.

To highlight some of the figures that explain its leadership, iShares recorded net inflows of $92.8 billion in equities and $36.1 billion in fixed income, comfortably more than double those of its closest competitor and around 40% higher than the amounts it posted in each category last year. “Its leadership extended across most segments, with particularly wide gaps in ESG, emerging markets and commodities, where it added $26 billion, $12.1 billion and $7.7 billion in net new assets, respectively,” the report notes.

It also left virtually no front uncovered, with 36 new launches spanning from active core building blocks to collateralized loan obligations (CLOs) and corporate crossovers, quantum computing and AI themes, new ways of weighting U.S. and global equities, and its long-anticipated entry into cryptoasset exchange-traded products (ETPs).

The New York-based manager’s cumulative trading volume in 2025, at $1.84 trillion, marked a notable increase from $1.47 trillion the previous year and was more than three times that of the next most liquid issuer. “It remains to be seen whether its 2026 initiatives in more active launches and more targeted exposures can maintain the same growth pace on an already colossal scale,” the report states.

From second to fifth place

Following iShares’ lead is the European firm Amundi. Europe’s largest asset manager climbed the ranking again after adopting an offensive strategy in low-cost core products and in its retail offering, while also outlining a plan to establish a meaningful presence in the European active ETF and white-label segments. “The launch of its low-fee core range and the expansion of its well-established synthetic replication platform supported $33.9 billion in equity ETF inflows, alongside demand for its well-positioned country-sector strategies, including its European banks product. The firm also recorded $16.9 billion in fixed income strategies, led by strong investment in exposures such as short-duration euro corporate debt,” the report states.

Looking ahead to this year, a shift in focus will see the firm join players such as State Street and DWS in supporting third parties entering the market by offering capital markets support, alongside plans to develop its own in-house active ETF range and a more granular fixed income offering.

Notably, after Amundi, third and fourth place in the ranking are once again occupied by U.S. firms: Vanguard and Invesco. According to the report, Vanguard, founded by Jack Bogle, reached the podium for the first time after ending a three-year drought without launching European ETFs, undertaking ambitious retail distribution initiatives and cutting fees on its core offerings. The Pennsylvania-based manager recorded significant net inflows, attracting $31.7 billion in new money during 2025—the third-highest figure among all issuers—despite ending the year with a limited range of just 40 products.

For its part, Invesco broke into the top five after posting the second-largest inflows in the smart beta and commodities segments, which, together with market performance, drove 44.6% growth in assets under management in its European ETP business.

Rounding out the top five is another European firm: Xtrackers by DWS. “The firm showed strong traction, with the fourth-largest inflows and the third-highest cumulative trading volume, reaching $472.3 billion. However, outflows in certain segments meant that its solid $31 billion in net new assets were less impressive in relative terms compared with the $39 billion in inflows that its European Xtrackers business had gathered the previous year,” the report notes. Like Amundi, the German manager benefited from partnerships with third parties. Specifically, it launched an ETF of ETFs in collaboration with Zurich Insurance and two active equity ETFs based on AI together with DJE Kapital.

Industry trends of the year

“While core indexed exposures continue to account for the bulk of scale in European ETFs, the past year has been characterized by issuers racing to lead the market in active ETF launches, retail distribution and third-party ETF-as-a-service offerings,” explains Jamie Gordon, editor of ETF Stream.

According to the report, other leading ETF providers in Europe made notable strides in asset gathering and strategic initiatives, ranging from new partnerships with neobrokers to capitalize on the growing weight of retail investors to launching full ranges of active ETFs for the first time. “Many even began to ‘rent out’ their capabilities to allow new managers to enter the format for the first time,” they add.

It also notes that competition in the nascent European active ETF segment is intensifying, with new entrants gradually eroding the dominance of market leader J.P. Morgan Asset Management. Nordea and Robeco, which narrowly missed inclusion in this year’s ranking, both ranked among the top 25 issuers by net new asset inflows in their new ETF businesses.

Looking ahead, future-oriented themes experienced a revival driven by defense after two years of net outflows, enabling specialists such as VanEck, WisdomTree and Global X to improve their position compared with last year’s ranking.

In light of these findings, Pawel Janus, co-founder and head of analytics at ETFbook, believes that European ETFs continue to show strong structural growth, reflected not only in rising assets under management but also in accelerating product innovation and an increasingly broad issuer landscape. “The market’s competitive dynamics are evolving rapidly, especially with the expansion of active ETFs and increasingly specialized strategies. In this environment, scale alone is no longer enough. Issuers must differentiate themselves through innovation, distribution strength and operational excellence,” Janus concludes.

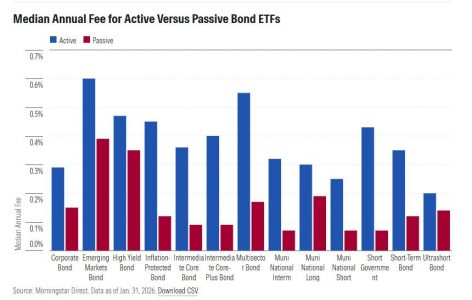

The market for active bond ETFs has grown exponentially in recent years, with net investment inflows exceeding $270 billion in just the past two years. Total assets under management reached $490 billion at the end of January 2026, and active ETFs now represent one fifth of the total assets in bond ETFs. Firms have responded to this growing demand by launching more than 270 strategies over the past two years, and these new entrants account for a quarter of all active bond ETFs, according to a Morningstar study.

Given this “dizzying” pace of development, an investor may wonder whether an active bond ETF has a place in their portfolio. At Morningstar, they believe that while the investment merits of each ETF vary, “there are some important considerations that should guide investors in the right direction.”

The Price of Active Management

Active bond ETFs carry a premium compared with their passive counterparts: their average annual fee of 0.45% is higher than the 0.24% average for passive bond ETFs. Active managers also tend to charge more in riskier categories: the average fees for emerging markets or multisector active bond ETFs are nearly double those of corporate or ultrashort bond ETFs. “While these complex segments of the market offer greater upside potential, they can also expose investors to higher volatility and sharper drawdowns. A higher price does not always translate into greater management skill,” the firm notes.

In contrast, the difference in fees between active and passive ETFs is not uniform across all categories. Managing a bond fund is a costly task in riskier and more nuanced categories, such as emerging markets or high-yield bonds. As a result, investors do not face a significant increase in costs in these cases if they choose active management, as Morningstar explains.

On the other hand, cost compression among passive ETFs in safer and more straightforward categories, such as intermediate core and intermediate core-plus, makes it difficult for active managers to compete on fees. “Active ETFs in these categories must offer an even greater edge for the investment to be worthwhile,” the firm concludes.

More Risk, More Reward?

According to Morningstar’s Active/Passive Barometer, active bond managers are more likely to outperform their passive counterparts than active equity managers. Although their success rate hovers around 50% over longer periods, active bond managers have more tools at their disposal to generate excess returns.

A recent analysis by Eric Jacobson and Maciej Kowara, of Morningstar, explains why active bond managers find it easier to achieve better results. The study notes that indexed funds face limitations that active managers do not, and that they can gain an advantage simply by including asset subclasses that fall outside the scope of the indexes or by tilting toward certain risks, provided this is done prudently.

To keep an index investable, most providers limit the range to the most liquid, or most heavily traded, part of the bond market and exclude more complex securities, such as floating-rate bonds or convertibles. Market value weighting also tilts index portfolios toward the higher-quality segments of the market, typically Treasury bonds or higher-rated corporate bonds.

In many categories, active managers’ ability to achieve better results lies in their flexibility to take on more risk than an indexed portfolio typically allows. While they may benefit more when riskier bonds rebound, this can also cause many active portfolios to lag behind their indexed counterparts during stressed markets.

So far, the average active corporate bond ETF has remained close to its benchmark because managers have limited room to maneuver in this largely investment-grade category. However, in categories where managers have a broader range of asset subclasses to choose from—such as intermediate core and short-term—and greater flexibility in terms of credit risk—for example, intermediate core-plus—the situation is slightly different: the sharp decline in March 2020 and the subsequent rebounds during the 2021 recovery point to the higher levels of risk these managers take to outperform their benchmarks, according to the Morningstar study.

“For a conservative portfolio that uses bonds as a counterbalance, these sharp swings are likely too risky to justify their potential returns,” Morningstar notes, adding that investors can use a “well-constructed” active portfolio to achieve “greater benefits in these categories, but they must understand that these returns come with additional risk.” Therefore, active bond ETFs require “more frequent reviews and more thorough due diligence compared with many passive bond ETFs.”

The Advantage of Manager Selection

The firm notes that some segments of the bond market are better suited to active management: high-yield bonds and emerging markets bonds are two of them, “given their relatively lower liquidity and higher credit risk.”

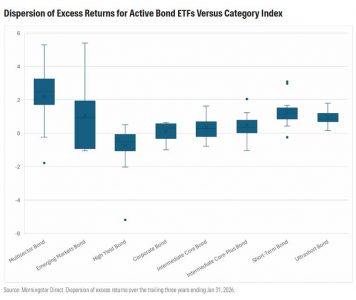

However, choosing an active ETF in any of these categories does not guarantee success. The greater margin for error also makes it harder for active managers to avoid pitfalls. The chart shows the dispersion of excess returns of active bond ETFs relative to their respective category index over the past three years. “The range is narrow for relatively safer categories, such as ultrashort- or short-term bonds, but widens dramatically for emerging markets or multisector bond ETFs,” the firm notes.

The outperformance of active bond ETFs often comes with higher risk. A good active manager can ensure that investors are adequately compensated for it. Choosing an experienced management team with a consistent track record, especially during periods of market stress, should be beneficial for investors.

Photo courtesyMarlen Lopez, Senior Wealth Advisor and Founding Partner of Excelsis Global Private Wealth.

The vision of Marlen López, Senior Wealth Advisor and Founding Partner of Excelsis Global Private Wealth, on the offshore U.S. advisory industry has been shaped by her experience at major firms, her entrepreneurial journey, and her ability to interpret the trends that have defined this business.

López began her career at JPMorgan Chase, where she learned how to build strong, lasting client relationships, developing a skill that would become the backbone of her professional path. However, it was during the Great Recession, when she transitioned into a new role as a financial advisor, that her career reached a turning point.

“My transition to Merrill Lynch during this period of intense market instability represented a transformative challenge. I took on the responsibility of supporting families and high-net-worth clients as they navigated economic uncertainty, refining my ability to design resilient wealth strategies and build deep, trust-based relationships,” López recalls.

The Courage to Be Entrepreneurial

Although she later continued her professional development at firms such as Wells Fargo Advisors, it was not until 2021 that, together with four other independent global wealth management teams, López brought her project, The Lopez Private Wealth Group, into the creation of Excelsis Global Private Wealth, in partnership with Sanctuary Wealth.

“The relationship I had cultivated with the founders of Sanctuary Wealth during my time at Merrill Lynch was key to this transition. Their confidence in our mission and vision allowed us to collaborate in developing an independent, boutique model designed to exceed the expectations of our high-net-worth clients. Sanctuary Wealth not only shares our philosophy, but also provides a comprehensive platform that includes products, technological innovation, and operational support, allowing us to focus on delivering truly personalized, world-class service,” she explains.

Regarding her business decisions, López’s assessment is clear: “The Lopez Private Wealth Group represents the commitment to excellence that has always guided me. Our mission is to deliver top-tier financial expertise, personalized service, and innovative strategies that create value at every stage of life and across every generation of the families we serve.”

An Environment of Consolidation

That mission remains unchanged, even within a business landscape marked by strong consolidation, increasing sophistication, and a redefinition of the advisory model. In her view, these three dynamics are unfolding simultaneously and intertwining to shape a new era in the wealth management industry.

“Consolidation is reflected in the rise of independent models and RIAs, which offer advisors greater autonomy and competitiveness. More advisors are migrating toward models that allow them to operate with greater independence and control over their practices, whether by partnering with platforms like Sanctuary Wealth, which offer flexibility without sacrificing access to high-level tools, or by building their own models from the ground up,” she states.

For López, sophistication is evident in the growing demand for comprehensive, highly personalized services similar to those of family offices—once reserved exclusively for the ultra-wealthy and now extending to a broader client base. “Finally, the redefinition is being driven by demographic, technological, and cultural shifts, such as the generational transfer of wealth, which requires advisors to adapt to new expectations around personalization, advanced technology, and human connection in order to retain key assets,” she adds.

Industry Trends

Over the years, she has observed a significant shift in the profile of offshore clients, driven by a combination of geopolitical uncertainty and generational change. “One of the most notable trends we see is the increasing sophistication of clients, with a clear focus on multigenerational wealth planning. This evolution is largely due to geopolitical instability in many of the countries we serve, which has heightened demand for expert guidance to navigate the uncertainties clients face daily, not only in their home countries, but globally,” she explains.

At the same time, she notes that as these challenges have intensified, so too has the need for robust portfolio strategies that provide clients with a sense of security and peace of mind. “In times of uncertainty, clients are highly focused on protecting their wealth and ensuring the long-term financial stability of their families. They rely on us as trusted advisors to help them build and safeguard their wealth in ways that address not only what is within their control, but also mitigate risks arising from external factors beyond their reach.”

Another significant shift has been the emergence of a younger, more technologically savvy generation stepping into leadership roles within the families they serve. “The evolving profile of offshore clients reflects a combination of global uncertainties and generational transformation. This has amplified the need for knowledgeable and adaptable expert teams capable of guiding clients through these complexities,” she affirms.

Within this broader industry transformation, the strength of the client relationship remains a cornerstone of successful business practices, particularly in the offshore market. In López’s view, trust, transparency, and ongoing education are critical components in building and sustaining that bond.

“While platforms and technology can enhance efficiency, streamline processes, and provide valuable insights, human connection and the ability to genuinely understand and address a client’s needs are irreplaceable. These relationships are cultivated through consistent communication, delivering on commitments, and honesty, qualities that foster loyalty and long-term partnerships. It is the fusion of people-centered values with platform-driven capabilities that creates a dynamic and impactful client experience,” she emphasizes.

Looking Ahead

When asked what she expects from the industry in the coming years, her message is clear: wealth management will undergo significant evolution driven by personalization, technology, and shifting client expectations. “Clients, regardless of their wealth level, demand highly personalized services similar to those offered to ultra-high-net-worth (UHNW) individuals. Advanced technology, including AI, predictive analytics, and digital platforms, will streamline operations, but human connection and ‘white-glove’ service will remain irreplaceable,” she argues.

As she notes, a key development, highlighted by Adam Malamed, CEO of Sanctuary Wealth, is the democratization of the family office experience: “Firms will expand access to high-level holistic services, such as multigenerational planning, family governance, and financial advisory, making them available to a broader range of clients.”

She also underscores that significant intergenerational wealth transfers highlight the need to connect deeply with future wealth holders, aligning services with their values, such as interest in ESG investing. In this context, she maintains that firms that cultivate a strong cultural identity and entrepreneurial flexibility will attract both advisors and clients, ensuring resilience and growth in a competitive environment. “To thrive, firms must embrace innovation while prioritizing relationship-building, constantly evolving to meet client needs. Those that fail to adapt risk losing relevance in this transformative era,” López insists.

Her main conclusion regarding the offshore business is that “while it faces challenges such as geopolitical uncertainty stemming from trade tensions, changes in immigration policies, and perceptions of protectionist measures by the United States toward Latin America; as well as strict regulation (KYC/AML) requiring longer and more complex processes to ensure global compliance and combat illicit activity; and tax complexities related to withholding taxes, succession laws, and legal structures that may be confusing for foreign investors—it remains highly attractive to Latin American investors seeking refuge, diversification, and growth in a stable, secure environment with access to liquid markets and unique opportunities.”

She emphasizes that “to capitalize on these opportunities, clients and advisors must adapt to changing conditions, prioritizing transparency, regulatory compliance, and delivering an innovative, highly personalized approach that responds to modern market demands.”

Insigneo has announced a strategic agreement with Fund@mental, a global platform focused on enhancing investment decision-making through data-driven insights. According to the firm, this integration incorporates Fund@mental’s technology into Insigneo’s proprietary Alia platform, equipping all of Insigneo’s investment professionals with powerful tools to analyze funds, build portfolios, and develop client proposals.

The firm notes that this represents another step in its commitment to innovation, operational efficiency, and client-focused service. Following the integration, Alia users benefit from a more streamlined analysis and proposal development process. Insigneo’s investment professionals now have access to these enhanced capabilities through Alia, further reinforcing the firm’s technology-driven growth strategy.

“At Insigneo, we believe technology should enhance human potential, not replace it. Bringing Fund@mental into Alia aligns with our vision of a more agile wealth management ecosystem grounded in stronger analytics. This integration not only saves time for our investment professionals but also enables them to grow their businesses more efficiently,” said Javier Rivero, President and Chief Operating Officer (COO) of Insigneo.

The Fund@mental platform, designed by wealth managers for wealth managers, offers features such as real-time market monitoring, comprehensive fund evaluations, and integrated collaboration tools. Available in English and Spanish, it connects the global wealth management community with clarity and precision, helping professionals navigate increasingly complex investment environments.

“We are excited to collaborate with Insigneo, a leader in global wealth management. Our mission has always been to simplify investment decisions through transparent technology, and integrating with Alia expands that impact to a broader network of committed professionals,” said Gustavo Cano, Founder and CEO of Fund@mental.

Alia is Insigneo’s next-generation wealth management platform, designed to unify custody, trading, reporting, analytics, and operational tools within a single ecosystem. According to the firm, the platform reflects Insigneo’s strategy to modernize the way investment professionals manage their practices through integrated technology and more efficient workflows.

There is broad consensus that global economic growth will remain stable in 2026, although political uncertainty, particularly regarding the U.S., as well as geopolitical conflicts, will persist. In this context, the rating agency EthiFinance Ratings expects sovereign ratings to remain stable, especially due to continued access to markets, orderly debt management, and a monetary policy environment in the process of normalization. However, the agency warns that rating differences are becoming increasingly pronounced, driven by disparities in potential growth, political and institutional instability, and uneven fiscal trajectories.

These outlooks and reflections are relevant because, as Antonio Madera, Chief Economist at EthiFinance, notes, a rating is “that big elephant that is hard to move, but when it moves, it makes noise.” In his experience, specialized investors assign ratings the role they are meant to have, that of assessing solvency in a way that should remain stable throughout cycles and not be sensitive to them. “Unlike what happened during the sovereign debt crisis, when an acute solvency problem exacerbated by a financial crisis was signaled, in this case the perception is one of greater acceptance of ratings around the assigned levels,” he warns.

Divergences in Europe

In Europe, by country, the EthiFinance Ratings Sovereign Credit Map places Germany, the Netherlands, and the Nordic countries among those with the highest level of confidence in policy execution and fiscal preservation; while Portugal and Greece show that fiscal adjustments and structural reforms can reshape a sovereign profile; and France, Italy, and Spain face “challenging” fiscal positions, with high public debt and persistent fiscal deficits, although with differences among them.

According to his analysis, Portugal is a clear example of a country capable of moving from intervention to a balanced public finance position, a path that Greece also appears to be following, “although still with very worrying levels of public debt,” he adds.

Doubts About the U.S.?

Regarding the U.S., Madera acknowledges that Moody’s downgrade last year is not, in itself, a reason to question the country’s ability to meet its obligations in full and on time, in terms of default probability, the difference between AAA and AA is minimal, as it remains an extremely safe issuer. “Rather, it underscores that its current fiscal position, debt burden, external deficit, and institutional quality are no longer fully aligned with the level of excellence required of a AAA-rated country,” he notes.

Madera is confident that, just as he does not foresee an upgrade to the U.S. rating, he also sees no grounds for a further downgrade. However, he acknowledges a meaningful risk related to the institutional factor, an element that often goes unnoticed in developed countries but serves as the cornerstone underpinning their ratings.

“Political deadlocks over the debt ceiling, the inability to outline a clear fiscal path, and/or recurring threats to the Fed’s independence erode investor confidence and weigh on governance. Added to this is the fact that the U.S. rating rests in part on the dollar’s role as the world’s reserve currency. While I have no doubt that the dollar will continue to play that role, geopolitical volatility and concerns about the fiscal outlook have nonetheless weakened it, prompting some investors to seek safer currency alternatives across the Atlantic. In this context, the path toward fiscal consolidation becomes even more essential,” Madera explains.

Faced with a lower U.S. rating, markets tend to magnify uncertainties, although in this specific case they have already priced in the likelihood that an upgrade will not materialize in the short or medium term. “Not belonging to the group of triple-A countries excludes certain institutional investors who require that rating threshold, although the shrinking number of countries within that select club is prompting a reassessment of investment policies,” he explains.

Based on his experience, what truly concerns him is the cyclical dimension driven by geopolitical uncertainty and declining confidence. “Among other effects, it directly increases the cost of debt and, consequently, erodes the fiscal buffer, something that undoubtedly exacerbates the imbalances mentioned earlier,” he adds.

Diversity in LatAm

In Madera’s view, Latin America occupies a significant place on the complex geopolitical chessboard that has taken shape in recent years, one on which the U.S. appears keen to maintain influence, as reflected in recent developments in Venezuela and threats of broader regional spillovers. “Amid this uncertainty, we see a positive development in the historic agreement between Europe and Mercosur, which opens access to a vast potential market for both sides and is likely to support economic growth in the region. Moreover, foreign capital flows may increasingly turn toward these markets, many of which require investment, in search of alternatives to the U.S.,” he highlights.

Overall, his outlook for the region remains stable, and he does not expect these risks or opportunities to materialize in the near term. “Chile, Mexico, Peru, and Brazil will continue to exhibit the strongest solvency levels in the region. However, they will not be immune, particularly Peru and Brazil, which face elections this year, as does Colombia, to a climate of institutional fragmentation, intensified by external pressures fueling polarization. In other countries across the region with dollarized economies, the effects may be mixed, both in terms of international trade and debt dynamics,” Madera notes.

When asked about the “overlooked strong ratings” in the region, he once again points to Chile, Uruguay, and Peru. “The first two stand out for their greater governmental stability and institutional quality, with Chile also benefiting from more balanced public finances. Peru, while broadly comparable, faces greater political tensions than the other two,” he concludes.

After the sale of 25% of the shares of the Mexican bank Banamex to Mexican businessman Fernando Chico Pardo was completed in December 2025, this Monday Citigroup, the bank’s owner, announced the sale of another equity stake.

Citi sold 24% of Banamex’s shares to a group of companies as well as to Family Offices; among the firms that acquired part of Banamex’s shareholding are names such as General Atlantic (its largest growth capital investment in Mexico to date), Afore SURA (a member of SURA Asset Management), Banco BTG Pactual (reaffirming its commitment to Mexico), Chubb (current partner for non-life insurance distribution), as well as funds managed by Blackstone, Liberty Strategic Capital, and Qatar Investment Authority (QIA).

“We are honored to have the support of these buyers as we prepare for Banamex’s initial public offering,” said Ernesto Torres Cantú, Head of Citi International.

The executive also stated: “Their investment is an additional endorsement of Banamex’s long-term strategy, its market leadership, and its growth prospects. The commitment of these investors strengthens Banamex’s fundamental position within the Mexican banking system.”

If the transaction is authorized by the relevant authorities in Mexico, Citi will have sold 49% of Banamex and, according to the institution, it does not foresee additional sales for the remainder of 2026.

According to the information, Citi sold a total of 24% (around 499 million shares) of Banamex’s common shares, at a fixed price of 43 billion pesos (around $2.5 billion); for the firm, this implies a price-to-book value under Mexican accounting standards of 0.85 times and a price-to-tangible-book value of 1.01 times under Mexican accounting standards, subject to customary purchase price adjustments.

Citigroup reported that each investor’s equity stake has been limited to a maximum of 4.9% of the total. The transactions are subject to customary closing conditions, including obtaining approvals from Mexico’s antitrust regulator, and are expected to be completed in 2026.

Chico Pardo Remains the Largest Individual Shareholder

Fernando Chico Pardo, current Chairman of the Board of Directors of Banamex, remains the largest individual shareholder, following the completion in December of his purchase of 25% of the bank’s shares. As its largest private individual shareholder, he actively participated in the selection process and will be actively involved in integrating the new minority investors into Banamex.

“The divestiture of Banamex remains a strategic priority for Citi. Any decision regarding the timing and structure of Banamex’s proposed initial public offering (‘IPO’) and any additional sale will continue to be guided by various factors, including, among others, financial considerations, market conditions, and obtaining regulatory approvals,” Citi said in its statement announcing the new sale of 24% of the bank’s shares.

With a series of structural trends underway in the investment world, it is not surprising that categories such as private markets, real assets, and the world of crypto investments are featured in the projected futures of several industry players. Imagining the world of wealth management in the United States, the market that sets the roadmap for financial industries globally—in 2035, the consulting firm McKinsey & Company sees that an increasingly multipolar world will require even more diversified portfolios, enhancing the relevance of these asset classes.

“If the current interest in private equity, real assets (such as real estate and infrastructure), shares of unlisted companies, commodities, and digital assets continues, investor portfolios will be broader, more global, and more customized than ever in the next decade,” the firm stated in its report, titled “US Wealth Management in 2035: A Transformative Decade Begins.”

The global context, and particularly the U.S. trajectory, points to a greater need to diversify portfolios, according to the firm. If trends toward multipolarity continue internationally, they forecast, and the dominant position of the U.S. dollar erodes, “the importance of foreign assets, currencies, and commodities, as a hedge against concentration risk and currency depreciation, would only increase.”

Recent data from the International Monetary Fund (IMF) show that the U.S. dollar’s share of global foreign exchange reserves has been declining from its peak and stood at around 57% in the third quarter of 2025, its lowest point in a decade.

For their part, McKinsey highlights that real assets and commodities would act as inflation hedges and sources of “tangible value,” while the role of positions in unlisted companies would be to provide exposure to innovation, through “companies that remain private for longer.”

Tomorrow’s portfolios would also have regulatory implications, naturally. “Interest in digital assets, including tokenized assets and instruments that apply blockchain, would drive the need for an evolution in regulatory approaches,” the consulting firm stated in its report.

Portfolios Increasingly Moving Away from the 60/40 Model

In its view of the wealth management industry in 2035, portfolio construction logic will change in this market environment. In the event that the global economy becomes more multipolar and less dollar-centric, McKinsey expects portfolio construction to become not only more diversified, but also more customized and more integrated with household balance sheets.

The firm’s studies indicate that these growing alternative asset classes continue to gain traction. On one hand, they noted, the crypto asset ETF and ETP market already stands at around $150 billion in AUM. On the other, their expectation is that retail client investments in alternative assets will grow between 1.5 and 2 times over the next five years.

“Advances in tokenization, stablecoins and digital settlement networks, artificial intelligence, and open financial architecture will further democratize access to private markets,” McKinsey predicts.

In this regard, for the consulting firm, the traditional 60/40 portfolio model will need to change over time. The result of this evolution would be multi-asset and multi-vehicle portfolios, with private, public, real, infrastructure assets, digital instruments, and alternative sources of income.

“Investors may incorporate design principles focused on inflation, with real assets and commodities as structural components to preserve purchasing power and hedge against currency deterioration. Portfolios may also incorporate greater exposure to foreign currencies and commodities to mitigate concentration risk and capture new sources of growth,” the firm stated in its report on the wealth management industry.

Along these lines, the consulting firm predicted that direct indexing would replace traditional ETFs. This would be driven by demand for tailored exposures, greater tax efficiency, and portfolios aligned with personal goals and sustainability preferences.

What CEOs Should Know

For those leading wealth management companies in the U.S., there is much to prepare for based on these projections.

The consulting firm expects clients to demand “frictionless access” to a broader, more global, and tax-optimized investment universe, including private, real, digital, and tokenized assets.

“Meeting this expectation will require a redesign of product platforms, data infrastructure, and partnerships,” the firm stated in its report. Thus, CEOs in the sector will need to decide what to offer, how to offer it, and how to integrate and deploy these products.

“This will likely mean investing in technology ecosystems that integrate public, private, and digital positions within unified and tax-optimized frameworks,” they added.

According to McKinsey, in an initial stage industry leaders will determine critical product and experience needs, and the technology, data, and architecture requirements these entail. Later, in the architecture stage, the focus will be on building more technological and other capabilities, defining variables such as in-house versus external solutions and potential partnerships, among others.

Treasuries, oil, and private credit have dominated attention over the weekend, reminding investors that we are in a year marked by uncertainty, by the weight of geopolitics, and by sensitivity to liquidity, but above all by the market’s ability to digest this context.

Javier Molina, Market Analyst at eToro, believes that we are facing “a latent risk in a complacent market.” According to his view, we are at a delicate point in the cycle, although the surface of the market does not yet clearly reflect it. “When you connect the dots, labor data, gold behavior, aggregate valuations, flows, and credit, a much more complex picture begins to emerge than the dominant optimistic tone suggests. Although macro noise is beginning to accumulate, the market is not reacting with fear. Inflows into equity funds and ETFs continue, week after week. But when you look more closely, the story changes. The bulk of flows is not going aggressively into equities. It is going into credit. Into corporate fixed income, into instruments that offer returns via ‘yield’ with lower relative volatility. In other words, money is not decisively increasing its bet on beta, but rather prioritizing carry and quality,” explains Molina.

Message for the Investor

At PIMCO, they agree that markets can appear calm, even when vulnerabilities are accumulating beneath the surface. In fact, traditional volatility measures, such as the VIX and the MOVE index, may signal complacency in both equity and fixed income markets, even in situations of rising risk.

“Investors have enjoyed a bull market in equities that has lasted for years, driven largely by technology. But as AI continues to revolutionize industries and the broader economy, the stock market volatility observed in recent days, especially in technology-related sectors, demonstrates how uncertain the outlook remains,” note Marc Seidner, Chief Investment Officer of Non-Traditional Strategies at PIMCO, and Pramol Dhawan, Head of the Emerging Markets Portfolio Management Team at PIMCO.

In this context, their message to investors is clear: expect the unexpected. For both experts, 2026 requires an agile mindset prepared for uncertainty:

“Be prudent and disciplined with valuations. U.S. equity valuations still appear elevated, leaving little room for error and increasing susceptibility to sudden fluctuations. Be alert to signs of market complacency and make greater use of relative value strategies rather than directional bets. Also maintain flexibility across regions, not just sectors, with the ability to move capital decisively and find value, especially when attractive yields are available in many countries. And finally, be agile enough to react quickly when volatility creates dislocations, whether in Japanese government bonds, U.S. agency MBS, or emerging market sovereign bonds, leveraging global scale and local presence to identify opportunities.”

Trade Policy: A Blow to Trump’s Tariffs

Taking quick stock of what the past 72 hours mean for investors, the first issue to mention is that the U.S. Supreme Court ruled against the Administration by 6 votes to 3, finding that the use of the International Emergency Economic Powers Act (IEEPA) to impose tariffs is unlawful. Consequently, President Trump expressed his disagreement with the decision, calling it “deeply disappointing” and labeling the justices who supported it as “unpatriotic.” He also announced that he would resort to all possible laws to impose a new global levy. “Overall, the decision on tariffs does not alter our positive view on financial markets. The decision is slightly favorable for equities insofar as a lower tariff rate improves household purchasing power, limits inflation concerns, and supports further rate cuts by the Fed,” says Mark Haefele, CIO of UBS Global Wealth Management.

Following the announcement, U.S. equities reacted positively to the decision: the S&P 500 rose 0.7% and the tech-heavy Nasdaq advanced 0.9% immediately after the ruling. However, as experts at Bloomberg highlight, the Supreme Court’s decision affected the U.S. bond market, valued at 30 trillion dollars, by threatening to increase the government’s budget deficit and cause further damage to an economy already grappling with elevated inflation and unemployment. The issue is that the U.S. government could face more than 175 billion dollars in claims if the ruling leads to refunds.

According to the firm’s experts, although Trump said he would approve a new 10% global tariff to replace those he has just lost, the long-term outlook remained unclear, given that the legal provisions he invoked contemplate temporary levies.

On the matter, Jack Janasiewicz, Portfolio Manager at Natixis IM Solutions, notes that with the midterm elections in November, affordability has come to the forefront, and the time required to implement alternative tariffs could allow for some price relief in the meantime.

“That said, we do not expect U.S. companies to suddenly reverse the price increases that have already been implemented. Rather, we expect companies to hold firm, allowing the decline in tariff-related costs to help bolster margins in the meantime. The bigger issue revolves around the prospects for issuing refunds, which complicates the situation and raises many more questions that need answers. Until we have greater clarity on this, we can expect the Treasury market to experience a slight bearish steepening and marginal weakness in the U.S. dollar,” argues Janasiewicz.

Geopolitics: Iran and Oil

The geopolitical situation in the Middle East remains a hot topic. Last week saw a massive redeployment of U.S. forces to the region and harsh rhetoric toward Iran. This move comes as Iran’s Supreme Leader threatens to sink U.S. warships and joint naval exercises between Russia, China, and Iran have been announced in the Strait of Hormuz. Consequently, some voices suggest that the Trump administration may be close to launching a large-scale military campaign against Iran, exceeding previous operations in scope.

“Geopolitical tensions remained elevated in January amid concerns that the West might launch possible military strikes against Iran. This news flow exerted some upward pressure on oil prices and helped reinforce the reflation narrative,” says Cristina Matti, Head of European Small & Mid Cap Equities at Amundi.

Undoubtedly, the conflict with Iran dominates the oil market, and prices are inflated with a considerable geopolitical risk premium. In the view of Norbert Rücker, Head of Economics and Next Generation Research at Julius Baer, a military confrontation seems inevitable, but such an escalation does not necessarily entail a disruption of oil supply, as recent years have repeatedly demonstrated. “More importantly, today’s oil market is very resilient on the supply side, thanks to ample storage, production exceeding consumption, and spare production capacity. While we are not certain whether the current rally will peak at 70 or 80 dollars, we are more confident that the risk premium will decline and oil prices will return below 60 dollars by midyear. Amid the current geopolitics, we maintain our neutral view,” acknowledges Rücker.

Private Credit and Liquidity

In the private markets sphere, the siren songs are led by Blue Owl, one of the largest private credit firms, which has carried out significant sales of private credit assets worth around 1.4 billion dollars as part of its response to liquidity tensions and investor redemption pressures. According to the asset manager, the assets sold consist primarily of direct lending loans originated by the firm and sold to large institutional investors such as public pension funds and insurers, but the market interpreted the episode as a sign of liquidity risk in retail-oriented products.

Analysts highlight that this event has had repercussions in the market on three fronts: the drop in Blue Owl’s share price and the temporary contagion to other similar firms such as Ares, Apollo, Blackstone, KKR, and TPG; in the BDC universe, the episode reinforced fears that, in the face of further redemptions, funds may have to sell assets or activate limits, which typically translates into discounts and weaker sentiment; and finally, it brought back to the forefront the debate about private credit’s exposure to software/IT services.

When assessing how all this will affect private credit’s outlook, Gregory Ward, Deputy Head of Global Product Management and Private Credit Chief Investment Officer, and Chris Gudmastad, Head of Private Credit at Loomis Sayles (affiliate of Natixis IM), believe that capital spending related to artificial intelligence and technology will offer attractive opportunities for the private credit market. “In our view, increased M&A activity and strategic investment in growth should also drive a more diverse set of investment opportunities. Strong investor demand should persist, fueled by the rise of investors attracted to less mature areas of private credit (e.g., ABFs) and new non-institutional sources of capital that are emerging,” they state.

Finally, they conclude by highlighting several risks to watch this year, such as “increased competition among lenders, which could lead to yield compression and more aggressive deal structures,” or “macroeconomic uncertainty, such as interest rate volatility or a slowdown in economic growth, which may expose weaker borrowers and potentially result in higher default rates.”

In February 2026, the SEC (U.S. Securities and Exchange Commission) approved a significant amendment to the regulations of the Financial Industry Regulatory Authority (FINRA) regarding gifts and business courtesies. According to the update to the well-known Gifts Rule (Rule 3220), the annual limit on permitted gifts has been increased from 100 to 300 dollars per recipient. This is the first adjustment to this amount since 1992 and responds both to the cumulative inflationary erosion over more than three decades and to the need to adapt the rule to current practices in the financial sector.

For financial advisors and professionals who serve high-net-worth clients, the change provides greater flexibility in the area of business courtesies, without altering the guiding principle of the rule: to avoid improper incentives or conflicts of interest. “The new threshold maintains the limit per person and per year, reinforcing the logic of prudence and proportionality. In practice, the update brings economic coherence to a figure that had become outdated, while preserving the control framework designed to protect the integrity of professional relationships,” explain representatives from the U.S. authority.

Beyond the quantitative increase, the reform incorporates greater technical clarity: FINRA has codified within the rule itself criteria that had previously relied on dispersed interpretative guidance, including aspects such as the valuation of gifts, their aggregation when there are multiple recipients, and the treatment of courtesies linked to events or business activities. Likewise, “certain exclusions are defined more precisely, such as personal gifts unrelated to professional activity or certain condolence gifts, providing legal certainty to both firms and registered professionals,” the update notes.

For experts, this change is also significant because it expressly authorizes FINRA to grant exemptions in specific cases, under certain conditions. This authority introduces an additional degree of supervised flexibility, particularly relevant for entities with complex structures or an international presence. At the same time, the SEC emphasizes that the update does not reduce expectations regarding internal supervision: firms must maintain systems and procedures reasonably designed to ensure effective compliance with the rule.