El Miami Fintech Club ha anunciado a Steve McLaughlin, fundador y CEO de FT Partners, para una charla exclusiva en su evento del 13 de febrero en Miami.

McLaughlin, ex banquero de Goldman Sachs especializado en FinTech y Servicios Financieros durante más de 20 años, será entrevistado por Alejandra Slatapolsky, cofundadora del Miami Fintech Club.

“Estamos encantados de organizar esta animada charla con uno de los líderes del sector”, declaró Max Shelford, cofundador del Miami Fintech Club.

El debate se basará sobre “el estado de la industria, las oportunidades de crecimiento, los movimientos estratégicos de los actores clave y sus predicciones para el futuro”, dice el comunicado al que accedió Funds Society.

El objetivo del evento es reunir a la creciente comunidad fintech de Miami para establecer contactos, debatir tendencias y obtener información de uno de los principales expertos en este campo, que fue recientemente clasificado en el puesto número uno en Institutional Investor’s “Most Influential Dealmakers in FinTech“.

“La discusión ofrecerá perspectivas poco comunes de esta industria en rápida evolución de los que saben”, agregó Shelford.

El Miami Fintech Club organiza eventos periódicos para reforzar la reputación de Miami como centro emergente de innovación financiera. El grupo fomenta la creación de redes, el intercambio de ideas y las asociaciones dentro del ecosistema fintech local, dice la información proporcionada por la organización.

El aforo es limitado, por lo que la organización recomienda a los interesado deberán inscribirse en el siguiente link.

What a difference one quarter, let alone one year, can make. Markets entered 2023 battered and bruised. A war in Ukraine and a war on inflation threatened to wreck the global economy. Cracks emerged as a succession of banks (Silicon Valley, Signature, First Republic, Credit Suisse) failed. In keeping with recent history, Congress took us to the precipice before agreeing to more spending. Tragically, another front has opened in the battle against the axis of Russia/Iran/China. Yet, notwithstanding signs of economic deceleration, inflation appears headed south while employment remains steady. Remarkably, the odds that the Federal Reserve pulls off a soft landing have grown; as Chair Powell noted in his most recent testimony: “so far, so good”.

Merger Arbitrage concluded the year on a strong note as Pfizer successfully completed its acquisition of Seagen (SGEN-NASDAQ) for $43 billion in cash. This followed a comprehensive second request process conducted by the U.S. Federal Trade Commission (FTC). Additionally, Bristol-Myers received U.S. antitrust approval in Phase 1 for its acquisition of the targeted oncology company, Mirati Therapeutics (MRTX-NASDAQ), contributing to a positive antitrust sentiment. Deal spreads, including those for Capri Holdings (CPRI-NYSE), Albertsons (ACI-NYSE), and Amedisys (AMED-NASDAQ) among others, firmed in response. Global M&A activity reached $2.9 trillion, marking a 17% decrease compared to 2022. However, the U.S. market remained robust with $1.4 trillion in announced deals, maintaining a level comparable to 2022.

Worldwide M&A totaled $2.9 trillion in 2023, a decrease of 17% compared to 2022 activity. However, fourth quarter deal making increased 23% sequentially compared to third quarter 2023, an encouraging sign that deal making may be recovering. The US remained a bright spot for deal activity with deal volume of $1.4 trillion, a decline of about 5% and accounting for 47% of worldwide M&A (compared to 42% in 2022.) Energy & Power was the most active sector with deal volume that totalled $502 billion and accounted for 17% of overall value. Industrials, Technology and Healthcare M&A each accounted for 13% of total M&A in 2023. Private Equity acquisitions totalled $566 billion and accounted for 20% of total deal activity. Despite PE deal volume declining 30% compared to 2022, it was still the sixth largest year on record for PE acquisitions.

Reflecting on a volatile year in the convertible market, we have some positive takeaways. Issuance returned to pre-pandemic levels at relatively attractive terms. We expect the pace of issuance to accelerate in 2024 as companies face a maturity wall that must be refinanced. We expect the allure of relatively lower interest rates in convertibles will bring many more companies to our market offering continued asymmetrical return opportunities. Additionally, convertibles that were issued at unattractive terms at market highs in 2021 have generally found bond floor and some offer a compelling yield to maturity. Companies that can have been repurchasing these bonds in an accretive transaction, or refinancing them by issuing converts with a more attractive profile. We expect this trend to continue in 2024 and continue to look for opportunities in this segment of the market.

Opinion article by Michael Gabelli, managing director at Gabelli & Partners

2022 will be remembered as a challenging period for financial markets, characterized by the ineffectiveness of traditional strategies and notable losses in global stock indices. Amidst this scenario, portfolio managers were forced to face the sale of positions backed by illiquid assets, highlighting the critical need for adaptability in investment management.

The rapid rise in interest rates in the United States and the Eurozone, driven by the urgency to curb runaway inflation, became a fundamental trigger for financial challenges. Additionally, the threat of recessions in major developed economies and geopolitical uncertainty created a landscape full of uncertainties for portfolio managers.

In this context, the 1st Report of the Asset Securitization Sector, sponsored by FlexFunds, serves as a tool to understand how financial advisors in different regions deal with the complexities of the current financial environment. The report analyzes short-term expectations, challenges in portfolio management, and key trends in the asset securitization sector through a series of questions directed at industry experts from over 80 companies in 15 countries in LATAM, the United States, and Europe.

In situations of uncertainty and volatility, portfolio management must seek the redistribution of financial resources to minimize risks and maximize returns. Portfolio diversification among different assets, sectors, and industries is a traditional strategy, but it is crucial for clients to understand the risks associated with each financial product. A delicate balance between risk and return, along with periodic rebalancing, becomes essential to maintain long-term goals and strategies.

Macroeconomic variables play a fundamental role in investment decision making. Economic growth, interest rates, inflation, the labor market, and government policies directly impact the health and performance of an economy. In this regard, the study conducted in this area has been broken down into four questions:

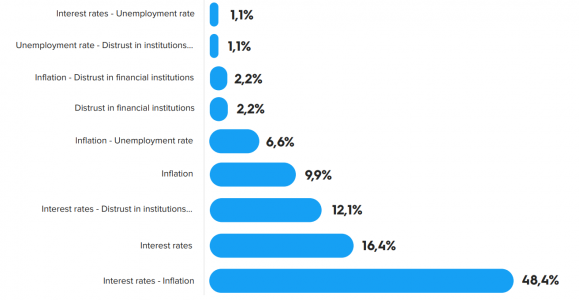

What variables will have the greatest influence on the markets in the next 12 months?

The results in Figure 1 show that almost half of the respondents believe that the main variables influencing the markets in the coming months will be interest rates and inflation, with interest rates being the primary variable considered by 78% of the sample, followed by inflation at 64.8%. Distrust in financial institutions is a factor considered by 17.6% of respondents.

Thus, the main variables to watch in the coming months are inflation and the evolution of interest rates until the end of their upward cycle.

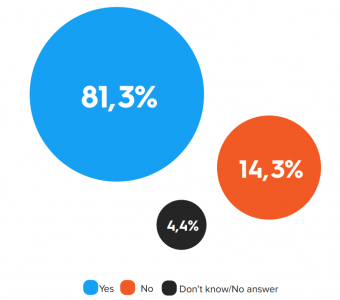

Considering that uncertainty is an inherent characteristic of financial markets, experts were asked if they believe investors are demanding more conservative positions. 81.3% of respondents believe that their clients are indeed demanding more conservative positions, compared to 14.3% who disagree with this statement, as seen in the following graph:

The situation in the financial markets during the year 2022/23, with losses in major indices and returns on stocks, investment funds, and assets, has generated an increase in perceived risk, increasing aversion to it. Both portfolio managers and investors are more inclined to modify their investment strategies to redistribute their portfolios towards more conservative positions.

The 1st Report of the Asset Securitization Sector provides portfolio managers with insights based on the survey results from nearly a hundred industry experts, where their expectations about interest rates and a possible recession in the United States over the next 12 months are also addressed. Download it now to learn their response and the main trends within the sector: Will the 60/40 model continue to be relevant? Which collective investment vehicles will be more used? What is the expected evolution for ETFs? What factors to consider when building a portfolio?

Cerulli projections indicate that total passive mutual fund and exchange-traded fund (ETF) assets will surpass total active mutual fund and ETF assets by early 2024, according to U.S. Product Development 2023: Resource Reallocation Through Product Rationalization.

However, the flight toward passive may be slowing, as active management seeks ground in vehicles other than the mutual fund.

Approximately 10 years ago, passive mutual funds and ETFs were neck and neck in the asset race against each other, while they collectively held one-quarter of the marketshare of total mutual fund and ETF assets. Since then, passive assets in the two vehicles have stolen one to three percentage points of marketshare from actively managed assets each year, reaching 49% of marketshare as of the end of 2Q 2023, according Morningstar.

However, the gains in passive marketshare may not represent the full story. Passive management primarily exists only within mutual funds, ETFs, and collective investment trusts (CITs). According to the research, looking across mutual funds, ETFs, CITs, money markets, retail separately managed accounts (SMAs), and alternative structures, active management still holds 70% of marketshare as of the end of 2022 and the pace of outflows has slowed in recent years.

As the industry looks into the future, questions persist regarding how much marketshare passively managed assets will eventually control, and whether the trend toward passively managed assets will slow based on changing economic conditions and investor preferences. “Time will tell where the critical point exists upon which passive investing becomes a risk, where the mechanism of blindly buying securities based on their prices rather than their cash flow could blow back,” says Matt Apkarian, associate director.

Performance aside, the drivers of demand for active and passive are based on attitudes toward management styles, and the belief or lack of belief that active managers can outperform in various market environments or over full market cycles. Geopolitical shock (73%) and recession (69%) are the scenarios most believed to increase demand for active management, while a sustained equity bull market (50%) is the scenario most believed to decrease demand for active management.

“Expansion of strategies and allocations outside of the largest U.S.-based asset classes can stand to give support to active management, as assets appear to be on a path to continue moving into passively managed products within the portfolio core of U.S. equity and fixed income,” adds Apkarian.

“Asset managers must adapt to changing demand from financial advisors and end-investors to remain relevant in the industry. Increased focus on defined outcome products with better downside capture can serve to be the tool that meets advisor needs when attempting to provide their clients with a smooth ride toward their financial goals,” he concludes.

Portfolio management faces several complex challenges that require the constant attention of industry professionals. The 1st Annual Report of the Asset Securitization Sector, sponsored by FlexFunds, highlights the top 10 challenges facing portfolio managers when raising capital and acquiring clients.

Raising Capital and Acquiring Clients: A Competitive Battleground

Tightening regulations, which can increase costs and create barriers for new investors, is one of the first complications portfolio managers encounter. Intense competition to attract clients and capital adds to this challenge, especially when differentiation between financial products is minimal.

Lack of understanding on the part of investors and clients about investment strategies and financial products can generate fear and indecision, especially in environments of low returns or lack of liquidity.

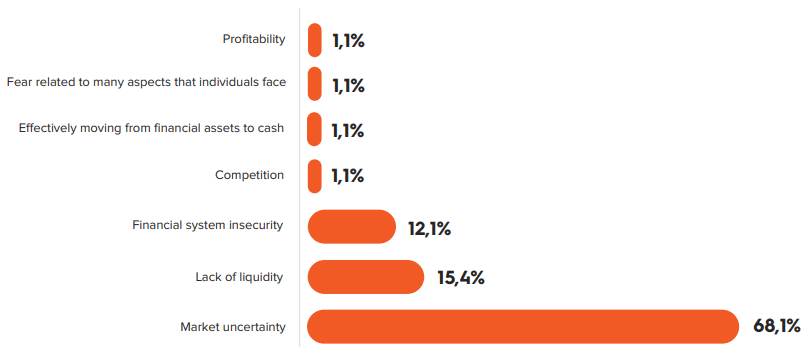

However, market uncertainty, arising from volatility or structural factors, stands out as the most problematic factor for acquisition.

FlexFunds’ report studies the main trends in asset management, which included the participation of more than 80 companies from 15 countries in LATAM, the United States, and Europe. This report reveals that 68.1% of participants consider uncertainty the most significant challenge, followed by lack of liquidity (15.4%) and financial system insecurity (12.1%). These factors accounted for 95.6% of the responses.

Market volatility undermines investor confidence and increases risk aversion, delaying investment decisions. Overcoming these challenges requires tactics that address uncertainty and improve client understanding of investment strategies.

Difficulties in Client Portfolio Management

According to the FlexFunds’ report, investment portfolio management faces several complex challenges, the top 10 of which stand out:

Client risk tolerance: Each client has a different risk tolerance, requiring careful balance in portfolio composition.

Market volatility: Financial markets are inherently volatile, requiring frequent adjustments to maintain portfolio balance.

Changes in economic conditions: Economic and market conditions impact asset returns, requiring adaptability in investment strategy.

Proper diversification: Achieving optimal diversification can be challenging, requiring in-depth analysis and specialized knowledge.

Asset selection and active management: Identifying strong asset investment strategies and actively managing the portfolio involves constant monitoring and informed decision-making.

Costs and fees: Balancing costs with the quality of services and results is essential to maintaining the client’s net return.

Effective communication: Clear and effective communication is crucial to understanding the client’s changing needs and ensuring trust over time.

Compliance and regulation: Keeping compliant with regulations and ethical standards is essential for asset managers.

Managing client emotions: Handling client emotions during volatility is crucial to avoid impulsive decisions.

Relative performance and expectations: Addressing client expectations and explaining relative performance is vital to maintaining trust.

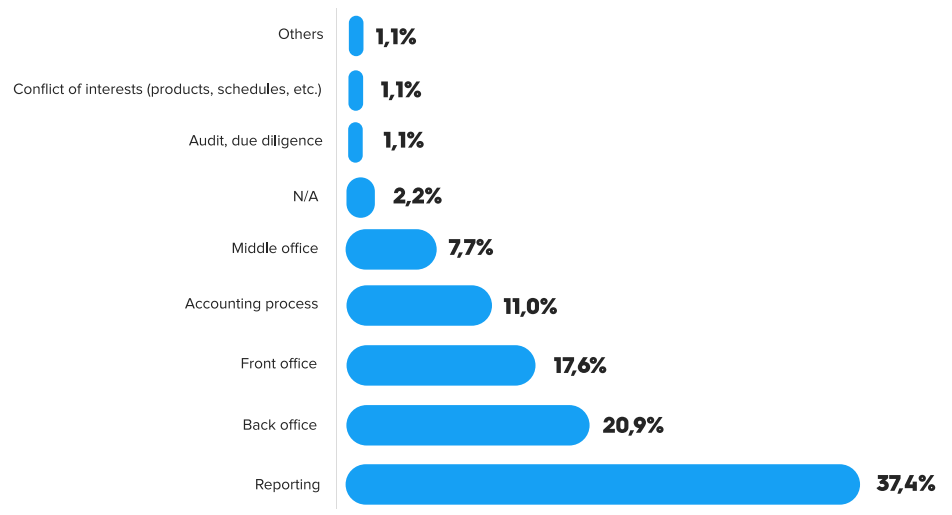

When industry professionals in more than 15 countries were asked, “What are the main difficulties you face in client portfolio management?” respondents identified reporting (37.4%), back-office (20.9%), front-office (17.6%), the accounting process (11%), and middle-office (7.7%) as the primary challenges in portfolio management.

Dive into a detailed analysis of the difficulties in portfolio management. From risk tolerance to emotional client management, FlexFunds’ 1st Annual Report of the Asset Securitization Sector reveals the daily complexities that portfolio managers face. Discover how industry leaders address market volatility, appropriate diversification, and regulatory challenges.

Download the full report to uncover innovative strategies, practical solutions, and exclusive insights on portfolio management in the competitive financial world 2024. Will the 60/40 model remain relevant? Which collective investment vehicles will be most utilized? What is the expected evolution of ETFs? What factors should be considered when building a portfolio? among others.

Did the year 2022 destroy the relevance of the 60/40 model? Are portfolio managers willing to implement other options? What alternatives are available in the market for asset managers to facilitate portfolio diversification? According to FlexFunds, a leading company in the design and launch of investment vehicles (ETPs), uncertainty becomes the playing field, and adaptation becomes imperative.

FlexFunds, has taken the initiative to prepare the 1st Report of the Asset Securitization Sector: a study of the main trends of these financial instruments to raise capital in international markets. This report reveals that despite poor results in the last year, more than half of the surveyed asset managers continue to bet on the 60/40 portfolio diversification model (request this full report by sending an email to info@flexfunds.com).

The 60/40 portfolio management model is an asset allocation strategy that involves a 60% weighting of the portfolio in equities and a 40% in fixed-income assets. This approach is commonly used by portfolio managers as a way to diversify risk and ensure a certain level of return in an investment portfolio.

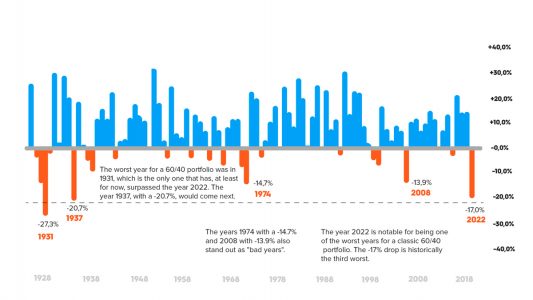

The year 2022 marked a dark milestone for 60/40 portfolios, worsening even the negative returns experienced during the economic crises of 2001 and 2008. Traditional recipes failed, and both the fixed-income and equity markets suffered significant losses. The war in Ukraine and the rapid rise in interest rates in the U.S. and the eurozone created a very complex scenario where the orthodoxy of the price relationship between stocks and bonds was not met.

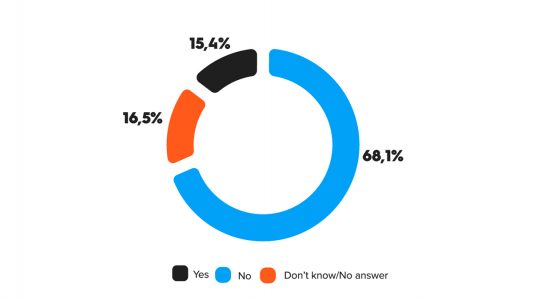

To the question, “Do you think the 60/40 portfolio composition model worked in the last 12 months?” more than 68% of asset managers and investment experts answered that the 60/40 model did not work, while 15.4% believe it did. However, 16.5% of the sample does not have a clear opinion on the matter. It is worth noting that among those who believe it did not work, almost 75% think it was due to the rise in interest rates, while nearly 10% argue that it was due to the decrease in equities.

Amid the uncertainty, portfolio management becomes a delicate art. Diversification, a cornerstone, was challenged by the lack of correlation between fixed income and equities. Traditional strategies, such as the 60/40 model, faltered, revealing their vulnerability to the changing economic and financial paradigm.

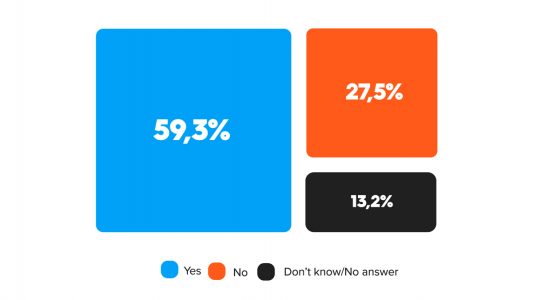

However, despite the majority of respondents agreeing that the 60/40 model did not work, when asked, “Do you think the 60/40 model will remain relevant?” 59% of asset managers and investment experts believe that this strategy will continue to be relevant. This fact highlights two aspects: first, its future application will depend on how the markets and economic conditions evolve, and second, perhaps paradoxically, it contradicts the earlier assertion that most respondents believe it did not work in 2022, yet now there is a majority opinion that it will remain a relevant strategy.

The global trend in portfolio diversification with new asset classes such as real estate, crypto assets, and private equity offers divergent alternatives to the classic 60/40 model in the international market. FlexFunds, through its asset securitization program, provides investment managers with the flexibility to design a portfolio with multiple asset classes and repackage it for distribution through Euroclear to private banking platforms.

How should asset managers adapt? What investment vehicles do investment advisors prefer to diversify their portfolios? What are the industry’s biggest challenges for clients and capital acquisition? Discover all of these key trends and more in the 1st Report of the Asset Securitization Sector by FlexFunds, which gathers the opinions of more than 80 asset managers and investment experts from 15 countries in Latin America, the U.S., and Europe.

Request it by sending an email to: info@flexfunds.com

Insigneo announced the appointment of Verónica López-López as Managing Director in Miami.

Before joining Insigneo, López-López served as Executive Director at Morgan Stanley for 14 years, where she cultivated her expertise in wealth management and client relationship building.

López-López brings a wealth of experience and a distinguished career to her new role as a Managing Director at Insigneo. With a professional journey that spans over three decades, she has gathered vast knowledge of the financial industry.

Her financial career commenced in 1988 at The Bank of Tokyo Mitsubishi (MUFG) in Japan. Subsequently, she ventured into the Japanese Chamber of Trade and Investments in Venezuela. Her international experience includes working in Corporate Finance as well as serving in private banking and wealth management divisions at Citibank, Merrill Lynch International, and UBS International, across cities such as Miami, New York, and Caracas.

“Veronica’s expertise in providing wealth management services to high-net-worth individuals, families, and corporations is extremely well-rounded,” said Jose Salazar, Market Head for Insigneo. “Her years of experience combined with her intellectual and social capital have allowed her to build close and enduring relationships with her clients, making informed decisions jointly with them. We are very excited to have someone of Veronica’s caliber as part of the Insigneo team of Financial Advisors.”

“I am thrilled to embark on this exciting journey with Insigneo alongside a new team and associates. I look forward to contributing my knowledge and experience to provide our clients with exceptional financial advisory services, leveraging my deep-rooted relationships with clients to help them make informed decisions about their financial futures with the open and flexible architecture of Insigneo and their world-class custodians,” expressed Verónica López-López, Managing Director at Insigneo.

Lopez-Lopez’s appointment comes amid the departure of many financial advisors from Morgan Stanley after the wirehouse announced significant changes for accounts in several Latin American countries.

Among the firms that have added more advisors are Bolton, Insigneo, Raymond James and UBS.

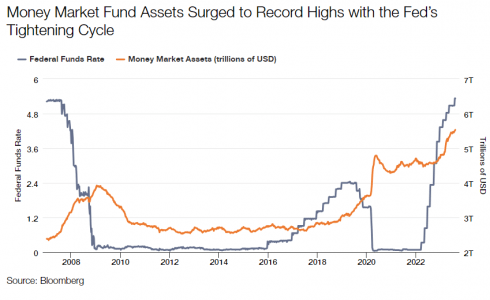

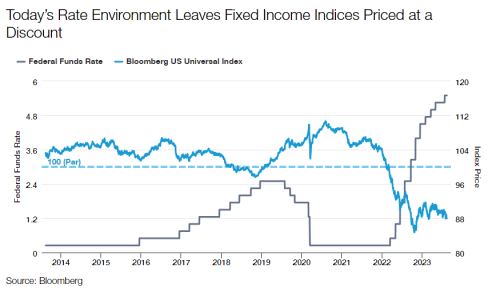

In the world of investing, fixed income has traditionally been associated with stability and income generation. This role has been uniquely challenged since the spring of 2022, when the Federal Reserve embarked on a series of massive rate hikes – at one point, four 75 basis points hikes in a row – which the markets have not experienced in a generation. Not surprisingly, many fixed income strategies and indices posted the worst total returns in their history, but the silver lining to rate hikes has been the return of higher yields in short-dated instruments such as Treasury bills. Naturally, many investors flocked to the front-end of the curve, taking advantage of these elevated yields, but now is an opportune time to reallocate some of this cash into the fixed income space.

Let’s begin by discussing the current interest rate environment, specifically the implications of the Fed’s hiking cycle. The Fed and other central banks have used their policy rates as tools to bring exceedingly elevated levels of inflation back towards what they deem to be “normal” or within their respective target ranges. While this has caused some anxiety among investors, particularly in risky asset markets, it has also led to attractive yield generation in short-term instruments like Treasury bills, money market funds, and certificates of deposit (CDs). As of July 31, 2023, the 6-month Treasury bill yielded 5.46%, the highest level in 23 years. As yields have risen, the money has followed, with prime and taxable money market funds taking in a combined $744 billion in flows for the 1-year period ending July 31, 2023, per Morningstar. Contrast this to the taxable bond space, which has experienced a net outflow of $85 billion over the same period.

Rising rates also have the effect of increasing the coupons paid on new fixed income securities, which should support forward looking returns. But perhaps more importantly, the rate sell-off has decreased the dollar price of bonds already in existence, many of which are government or investment-grade corporate bonds with low credit risk. As a result, the bond market is priced at a discount even though fixed income securities, with the exception of a default event, mature at “par” or $100. It is this “pull to par” that should drive attractive returns and ultimately better economic outcomes than even the seemingly attractive yields provided by cash instruments today.

The term “pull-to-par” refers to the tendency of fixed income securities to move towards their face value (par value, or $100) as they approach maturity. Bonds priced at a discount will see their prices rise as they get closer to maturity, while bonds trading at a premium (that is, above $100) will see their values fall to par over time. In today’s environment, with the Fed near or at the end of the tightening cycle (as of this writing), fixed income securities with prices below their par value have potential for meaningful price appreciation. That appreciation, in addition to regular coupon payments, leads to larger total returns for investors. We believe this total return likely eclipses the yields that may be earned on short-end instruments.

To illustrate how unique the current fixed income environment is, let’s examine historical price data for various fixed income indices over the last 10 years. In the chart below, we show average price for the Bloomberg U.S. Universal Index. For the vast majority of the 10-year period, average price for the index was either near or above par, with the mean dollar price at about $102. Rising rates have driven the average dollar prices of the index, and active portfolios as well, down to near unprecedented levels, currently below $90. Given the quality of the constituents of the index, it is reasonable for an investor to believe that these bonds will pull back to par as they get closer to maturity, thereby providing investors with an additional boost to performance over and above just clipping coupon payments.

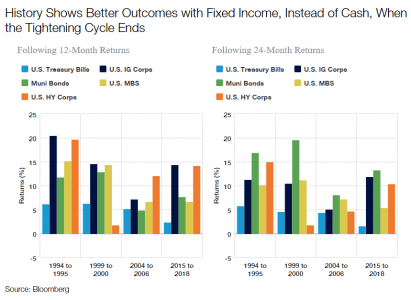

Another lens to look at the relative value of owning fixed income versus cash instruments can be seen in historical data on how both have performed in an environment similar to the present one, that is, with the Fed near or at the end of its hiking cycle. We looked at data for the last four Fed tightening cycles going back to the mid-1990s to see how both cash and fixed income performed as the cycles ended. We used the ICE BofA U.S. Treasury Bill Index as a proxy for short-term instruments and selected four Bloomberg indices representing both above and below investment-grade securities for fixed income. As the table shows, the subsequent one- and two-year returns produced, in most cases, better economic outcomes when owning fixed income as opposed to staying invested in Treasury bills. In the current environment where the Fed is at or near the end of its tightening cycle, and with an elevated chance of economic weakness going into 2024, fixed income has a similar potential to outperform cash instruments this time around.

By combining both the return generators of coupon and the “pull-to-par” effect, investors may outperform Treasury bills, CDs, and money market funds in the months and years ahead. We believe active management remains a valuable tool to capture these excess returns and potentially add alpha over benchmark indices. Many fixed income securities with attractive risk and reward characteristics, such as short-dated, investment-grade rated bonds within the asset-backed securities and residential mortgage space, sit outside of benchmarks and represent some of today’s most compelling opportunities.

The concept of earning coupon plus the pull-to-par represents a valuable opportunity for fixed income investors moving forward. By understanding how this phenomenon impacts fixed income securities’ total return, investors can capitalize on the current opportunity it presents. When combined with effective active management strategies, the pull-to-par effect may serve as a powerful tool to achieve outperformance and enhance overall returns. But timing is of the essence. The economy will eventually weaken, and perhaps tip into recession. Yields today look to be interesting even in a high-quality portfolio. So now is the time to make those moves, not to wait until yields fall.

Opinion article by Rob Costello, client portfolio manager in Thornburg Investment Management.

Robeco announced the restructuring of its American operations into the entity Robeco Americas, headquartered in New York, and the expansion of its agreement with LarrainVial, which includes the wholesale business in US Offshore and Latam, based in Miami.

LarrainVial will continue to distribute Robeco’s funds for Latin American institutional clients as it has been doing for the past twenty years.

María Elena Isaza and Julieta Henke, directors and sales managers of Robeco’s US Offshore and Latam business, will join LarrainVial as managing directors and “will continue to be based in Miami,” according to a memo sent to Robeco’s clients, which Funds Society has accessed.

Both Isaza and Henke will receive full support from Robeco and LarrainVial to continue their growth efforts in the region, offering the same exceptional service and products to clients, adds the exclusive communication for clients.

“This appointment will not have any impact on the operational and contractual aspects of our commercial relationship with our American and Latam Offshore clients. Everything remains the same!”, emphasizes the communication that was not made public.

On the other hand, Robeco will centralize its operations into a single hub, with all Robeco employees based in New York. This hub will serve GFIs, the U.S., Canada, LATAM, and US Offshore.

The amalgamation of Robeco’s activities in America will be led by Ignacio Alcántara and “is driven by the desire to offer efficiency in customer services in a highly regulated and competitive market,” says the statement released by the firm.

The focus also aims to ensure consistency in client interactions, optimize resource allocation, and facilitate ongoing compliance with industry regulations.

“By centralizing our operations in America and forging strong partnerships, like the one we have with LarrainVial, we are better positioned to effectively serve our clients in the future… We have been working closely with LarrainVial in the LATAM markets (excluding Brazil) for over 20 years, and we are excited to extend this cooperation to the US Offshore and LATAM market. LarrainVial’s extensive experience and presence in America align perfectly with our mission to offer top-tier investment solutions to our clients,” commented Malick Badjie, global director of Sales and Marketing at Robeco.

On the other hand, Fernando Larraín, CEO of LarrainVial, said that “with a rich history spanning over 90 years, LarrainVial has amassed extensive experience in the distribution business across America. The US Offshore market is of immense importance to LarrainVial as a key area for growth.”

Julius Baer will change its regional structure, create encompassing responsibility for client experience, and strengthen the importance of people management and culture. As a result, the Group makes new appointments to the Executive Board. The changes in structure and leadership are designed to enhance the delivery of its targets for the 2023–2025 strategic cycle and beyond.

As of the beginning of 2024, Julius Baer Group complements its leadership team through a number of in-house promotions and select new hires.

The changes in regional structure will create maximum proximity to clients and their needs, thereby accelerating the growth of the Group’s franchise. The newly created division Client Strategy & Experience will set global standards in client service, providing support, segment management, marketing, and front risk management for all Regions. With the representation of Human Resources in the Executive Board, the updated leadership structure further reflects the central role of people and culture in Julius Baer’s strategy of focus, scale and innovate.

Commenting on the changes, CEO Philipp Rickenbacher said: “Creating value for our clients and stakeholders is at the heart of our purpose – it is the key to our success. Our organisational structure and freshly composed leadership team, with its blend of in-house and new talent, will create the momentum and continuity needed to achieve our targets. It is also the optimal structure to fuel Julius Baer’s ability to capitalise on the growth opportunities in the wealth management industry.”

Further changes effective 2024

Yves Robert-Charrue decided to leave the Group at the beginning of 2024 and will therefore step down from the Executive Board. Philipp Rickenbacher said: “The unrivalled position that Julius Baer enjoys today in Switzerland, Europe, and the Middle East is an outstanding achievement of Yves Robert-Charrue and his teams. A highly esteemed and valued colleague since 2009, I would like to thank Yves for his leadership and loyalty and wish him the very best for his professional and personal future.”

Beatriz Sanchez will also step down from the Executive Board, reflecting her wish to relinquish operational responsibilities, and assume the strategic role of Chair of Americas at Julius Baer as of January 2024. Philipp Rickenbacher said: “Betty Sanchez has been invaluable in re-structuring the Americas business and positioning it for renewed growth. I am immensely grateful for her great contribution and delighted that she will continue to work with us in her new role.”

Background on new Executive Board members, with designated roles

Sonia Gössi, Switzerland & Europe, will join Julius Baer on 1 January 2024 from UBS, where she was Sector Head Wealth Management Europe International North. She started her career in audit and business consulting and joined UBS in 2004, where she held senior client-facing roles in wealth management as well as various risk control and risk management positions.

Carlos Recoder Miralles, Americas & Iberia,today Head Western, Northern Europe & Luxembourg at Julius Baer, joined the Group in 2016 from Credit Suisse, where he started his career in private banking in 1997 and last held the role as Head Private Banking Western Europe.

Rahul Malhotra, Emerging Markets, is currently responsible for Julius Baer’s Global India franchise (onshore and non-resident), Japan, and Asian clients served out of Switzerland and Japan. He joined from J.P. Morgan in 2021. Rahul will be based primarily in Dubai, recognising the financial hub’s central role for these growth markets.

Thomas Frauenlob, Intermediaries & Family Offices,will join on 1 April 2024 from UBS. He is currently the Head of UBS’s Global Financial Intermediaries Business and was previously in charge of their Swiss Global Family Office and Ultra High Net-Worth franchise. He started at UBS in 2010 as Head Equities Switzerland, following roles in the institutional business of Deutsche Bank and Goldman Sachs.

Sandra Niethen, Client Strategy & Experience,is currently Chief of Staff and Head of Strategy at Julius Baer, a role she has held since 2020. Her financial services career of over 20 years spans a number of senior positions in private wealth and asset management, in international client-facing, strategy development, and sales management roles at Deutsche Bank and DWS.

Guido Ruoss, Chief Human Resources Officer & Corporate Affairs,has been Global Head Human Resources at Julius Baer since 2015. Previously he was responsible for business and product management in the Bank’s Investment Solutions division. He joined Julius Baer in 2008, after several years in the asset management and alternative investment industry.

Christoph Hiestand, Group General Counsel, has been with Julius Baer since 2001 and has held the role of Group General Counsel since 2009. Before joining the Bank, he worked as an attorney-at-law in law firms in Germany and Switzerland.