Investors Remain Optimistic, but Volatility Shock Leads them to Increase Cash in Portfolios

| By Beatriz Zúñiga | 0 Comentarios

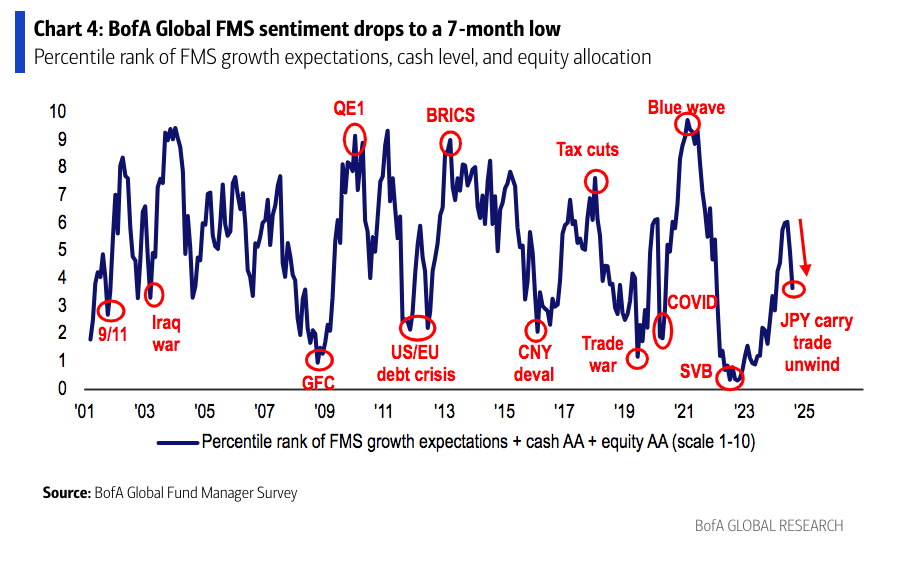

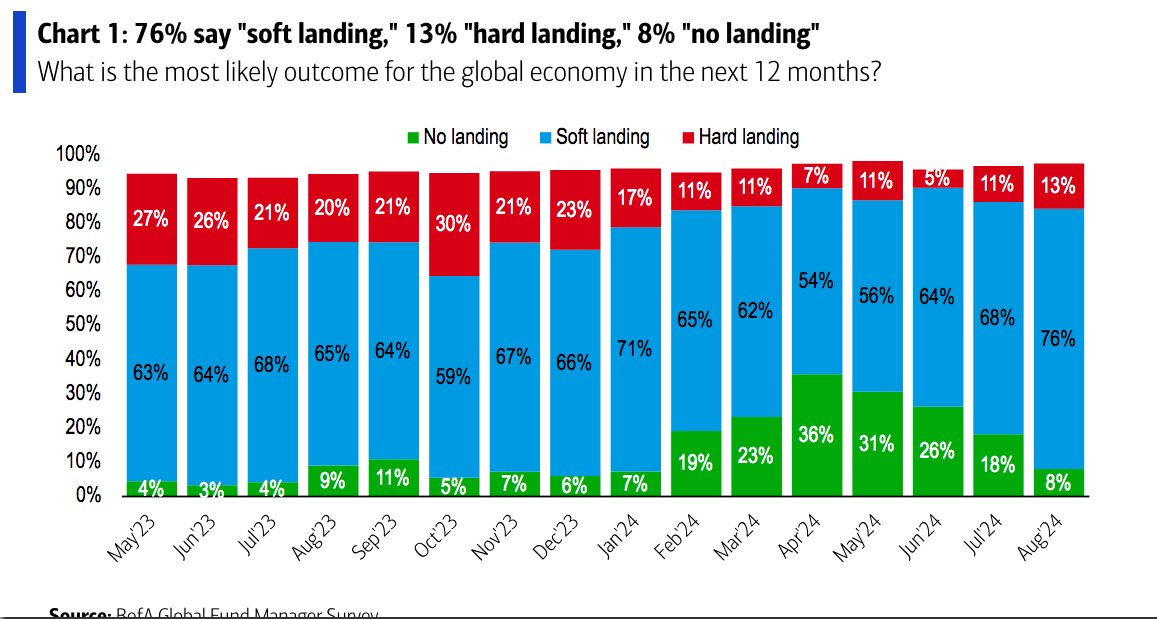

Despite the market correction in early August, investor optimism has not been affected. According to BofA’s monthly manager survey, 76% continue to expect a soft landing and a Fed action, now, of four or more cuts to ensure that this expectation of a soft landing is met.

However, the survey picks up that global growth expectations in the August survey fell sharply by 20% compared to July, in fact a net 47% of respondents expect a weaker global economy in the next 12 months. “Growth expectations and risk appetite declined in recent weeks due to the yen volatility shock and weak July employment data,” notes the BofA survey.

As a result, investors increased cash levels again for the second consecutive month, rising from 4.1% to 4.3%. “Our broader measure of FMS sentiment, based on cash levels, equity allocation and economic growth expectations, fell to 3.7 from 5.0 last month,” the firm notes.

As for monetary policy, 55% of investors believe that globally it is too restrictive, the highest figure since October 2008. In this regard, they point out that investors’ belief that policymakers should ease quickly is driving expectations of lower rates, which is why 59% expect lower bond yields, the third highest figure on record (after November and December 2023). Bond yield expectations are also lower, a sentiment that has been increasing month-over-month.

Coupled with monetary policy expectations is the conviction that a “soft landing” of the economy will be achieved, a conviction driven by the likelihood of lower short-term interest rates. Specifically, 93% of FMS investors expect lower short-term rates 12 months from now, the highest figure in the past 24 years.

Asset Allocation

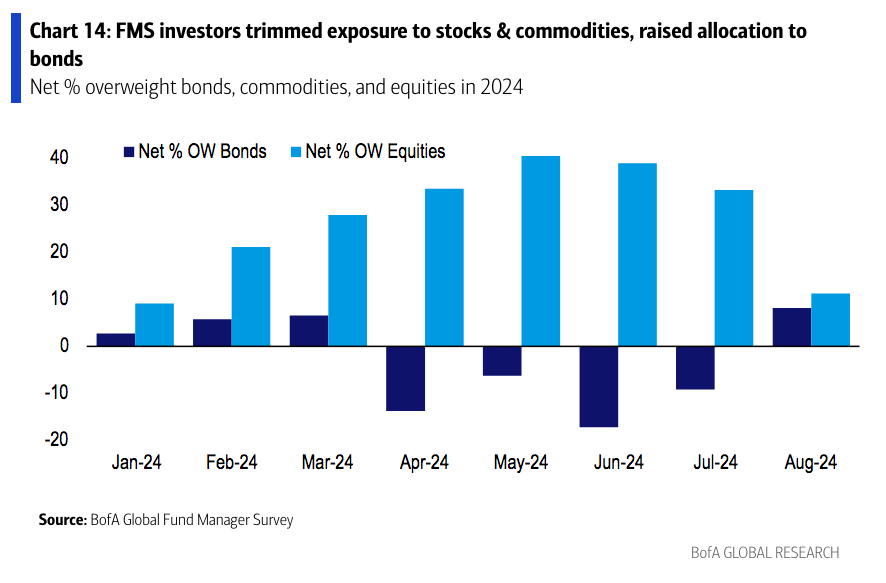

When it comes to talking about allocation within investors’ portfolios, the survey shows that in August investors rotated into bonds and out of the equity market. “The allocation to bonds increased to 8% overweight from 9% underweight. This is the highest allocation since December 2023 and the largest monthly increase since November 2023. In contrast, the allocation to equities fell by 11%, which is the lowest allocation since January 2024 and the largest monthly decline since September 2022. Notably, in absolute terms, 31% of FMS investors said they were overweight in equities, down from 51% who said so in July.

“In August, investors increased allocation to bonds, cash and health care and reduced allocation to equities, Japan, the Eurozone and materials. Investors are more overweight in healthcare, technology, equities and the U.S., and more underweight in REITs, consumer discretionary, materials and Japan. Relative to history, investors are long bonds, utilities and healthcare and are underweight REITs, cash, energy and the Eurozone,” BofA notes.

Finally, two curious tidbits of information left by this month’s survey is that the largest regional equity allocation was to the U.S., while the allocation to Japanese equities experienced the largest one-month drop since April 2016. “As a result, global managers’ allocation to U.S. equities relative to Japanese equities increased to the highest level since November 2021,” the survey concludes.