Driehaus Capital Management announces the launch of the Driehaus Event Driven Fund as of August 26, 2013. A new liquid alternative offering, the mutual fund seeks low correlations to major asset classes while providing lower volatility than the S&P 500 Index with superior risk-adjusted returns.

The fund will be managed by K.C. Nelson, who leads the Driehaus Long/Short Credit Team. Mr. Nelson and his team currently manage distinct event-driven trading strategies in their long/short credit funds. According to Mr. Nelson, “We have found that event-driven trades often exist because of the complexity of the capital structure, the nontraditional nature of the investment opportunities, or the unwillingness of investors to participate in trades with binary outcomes. We believe this creates opportunities for positive asymmetric returns with low correlations to the equity and credit markets.”

Trades within the Driehaus Event Driven Fund will have a defined catalyst that will unlock the value of the trade in the near to intermediate term. “By combining the credit, equity and derivatives resources across our firm, we’ll identify opportunities globally to source mispricings in long, short and arbitrage trades based on hard catalysts, such as product launches, earnings releases, restructurings, and corporate actions,” said Mr. Nelson.

While the event-driven space has been a significant segment of the alternatives universe for more than two decades, relatively few liquid alternative event-driven funds are available to investors. “We believe investors will appreciate access to a liquid and transparent vehicle for a strategy that offers a differentiated market exposure,” said Rob Gordon, President and CEO of Driehaus. “We also expect investors to take comfort knowing that the fund is offered by a firm that has proven itself in the liquid alternative space and is managed by a team with significant experience with event-driven trades.”

BBVA Compass announced thatGabriel SanchezIniesta has been named its new chief information officer following Sergio Fidalgo’s appointment as Spain-based head of Applications & Architecture for BBVA Group.

Until now, Sanchez Iniesta served as BBVA Group’s Multichannel Technologies director. A native of Madrid, he was responsible for developing the multichannel architecture BBVA developed in many countries across its global footprint and the core banking platform it currently uses in Spain. He came to BBVA Group in 1997 following several years with Accenture.

Fidalgo, who was in charge of BBVA Compass’ Technology and Support Services unit for five years, successfully led a major transformation of the bank’s legacy technology into a core banking platform that enables real-time transactions. American Banker called it an “epic” project and “one of the largest bank core overhauls in the U.S.,” while one analyst told the Houston Business Journal it had the makings of a “game changer” for the banking industry.

Sanchez Iniesta inherits that ground-breaking platform and is well-positioned to lead the next phase of the bank’s technology growth, which will focus on multichannel banking, said BBVA Compass President and CEO Manolo Sanchez.

Wikimedia Commons. James Boyne deja su puesto de COO en Calamos Investments por la filantropía

Calamos Investments, announced the planned departure of James Boyne, President and Chief Operating Officer, effective September 30, 2013. Until that time, Mr. Boyne will act in an advisory role and assist the company in the orderly transition of his duties and responsibilities.

Boyne joined Calamos Investments in April 2008 and served in a number of executive positions since then. He has decided to pursue a leadership position in the non-profit sector, focusing on the betterment of children and young adults. Boyne and his family will be relocating to Steamboat Springs, Colorado.

“I appreciate Jim’s leadership during his tenure at the firm and wish the best to him and his family,” said John P. Calamos Sr., Chairman, Chief Executive Officer and Global Co-Chief Investment Officer.

The firm does not plan to replace the role of President and COO, and Boyne’s responsibilities will be assumed by other senior leaders at Calamos, including the firm’s Executive and Operating Committees.

Foto cedidaBen Wallace & Luke Newman de Henderson. Seeing Things in absolutes

Fear and greed have been powerful motivators over the past few years, with investors gripped in turn by panic about the health of the global economy and optimism that central banks have done enough to promote growth. From concerns about the burden of government debt in the western world, to the US ‘fiscal cliff’ leading up to the start of 2013, whichever way the pendulum has swung, investors have followed.

The past few months, however, have seen the steady emergence of a different trend. We first saw it at the start of 2012, when stocks were pricing almost entirely on market sentiment. At that time, the importance of economic newsflow far outweighed the detail of individual stocks. Since then, share pricing correlations have steadily fallen and the dominant macro-economic themes that have driven investors to buy or sell over the past few years are no longer overshadowing stock-specific drivers to quite the same degree.

Source: Bloomberg, CBOE S&P500 Implied Correlation Index (indicating the expected average correlation of price returns of the stocks that comprise the S&P500 Index), as at 7 August 2013

A market where prices move in tandem, such as we saw in the period prior to 2012, limits the opportunities for stock-pickers like us to generate active returns. The lower the correlation in share price movements, the greater the opportunity to find stocks capable of generating higher or lower returns than the market average. This gives room for independent stock characteristics to play a bigger role, providing more opportunities to generate profits from long and short stock-picking ideas.

It can be something of a challenge to overcome some investors’ ingrained preference for bond funds, particularly for those who lost money in the post-Lehman Brothers crash (15 September, incidentally, marks the five-year anniversary of when the company filed for bankruptcy). Bond markets have come under abnormal and sustained pressure in recent months, however, as markets consider the implications of the US Federal Reserve’s plan to start pulling back on its $85 billion per month bond-buying programme.

This has left investors looking for other options for their money in a low growth, low interest rate world. Absolute return funds, which are generally considered to sit somewhere between a bond fund and an equities fund in terms of potential risk are, in our opinion, an attractive halfway house.

For our Absolute Return strategies, the long and short books are equally important and, as always, the key is getting the right mix of holdings. It is an intrinsic part of our management style to be very proactive in scaling positions on the fund. The portfolio is divided into our core long book and a tactical short book, which allows us to move quickly when responding to market events, or when looking to exploit what is a diverse investment universe. Our willingness to utilise this flexibility to adjust the net and gross position has enabled us to generate consistent positive returns, while helping to preserve capital and minimise volatility.

January 2013 marked the first time in some years that we moved the gross exposure above 100%, a statement of confidence that it was a sensible time to put investors’ capital to work. At the time we took some material long positions to more defensive areas of the market that displayed very safe and secure dividend-paying characteristics, such as HSBC and Vodafone. HSBC in particular seemed very well positioned, with a recent dividend increase suggesting that future earnings might be quite good.

Financials has been quite a busy area for us in 2013, across both long and short books, given the sector’s sensitivity to economic data and monetary policy. Central banks have taken extraordinary measures in the past couple of years, directing the risk-free rate to help restore confidence in the economy and to make other asset classes more attractive. While we would not ordinarily choose to go long in miners, a number of resources stocks also seem unduly out of favour, given management changes and improvements in capital expenditure.

The fall in share pricing correlations hopefully marks an end to what has been a lingering hangover from the financial crisis, at least for the time being. In a perfectly efficient market, all investment decisions would be based on rational and measurable factors, with share price volatility driven primarily by the fundamentals of individual companies. Markets certainly aren’t perfect, but in this environment, we believe that an actively managed long/short strategy with an absolute return focus can play an important role for cautious investors.

Vincent Oswald, cofundador de Azure Partners. (Foto cedida por Azure. Los fondos de fondos de microfinanzas, “una inversión de atractivos retornos”

Azure Partners’ team offers one of the longest track record investing in microfinance and combines a total of 24 years of direct microfinance field experience combined with solid entrepreneurial background. For the co-founders of Azure Partners, Jack Lowe and Vincent Oswald, launching funds of funds was a natural step after managing the largest microfinance debt fund at BlueOrchard Finance from 2004 to 2008.

As explained byOswald, in an interview with Funds Society, microfinance provide an excellent investment case:

De-correlated investment

Stable returns and low volatility

Fast growing markets

Access to the real and informal economy

Vast social impact

Azure Partners, a swiss based investment advisor specialized in microfinance, advises two microfinance funds of funds:

– Azure Global Microfinance Fund (AGMF) is the first fund of funds managed by professional from the microfinance investment industry. It offers a diversified exposure to different investment funds with specific microfinance strategies, from traditional debt funds, to balanced debt and private equity funds, to Private Equity funds.

– Azure Microfinance Private Equity Fund (AMPEF) which aims to focus on investing in strong locally managed microfinance Private Equity funds focused on specific countries or regions with a hands on approach. The fund will combine 20% co-investments with 30% secondary purchases and 50% primary funds to deliver strong returns to our investors.

Respect to its investment process, Oswald said that they have a 5 steps investment process. “In comparison to more traditional fund of funds, we also conduct Due Diligence of underlying Microfinance Institutions in our portfolio, especially for Private Equity funds. This is a key part of our analysis and a clear added value to the decision process”.

Asked if the fund has a charitable side, the co-founder of Azure reply that investing in microfinance has a vast impact. “By its activity and type of clients, Microfinance generates an impact for millions of micro-entrepreneurs in the countries where we invest in”.

“We do not see the fund as charitable, as it delivers a credible financial return to its investors. However, we pay high attention to our investments social impact. Therefore, we developed our own Social Performance rating to analyze the funds we invest in and include it in our investment decision process”.

He also explained that they have atop-down / bottom-up approach in selecting their investment opportunities. “Usually, debt funds offer a worldwide exposure to microfinance markets and we focus in choosing the best one for the fund”.

He added that regarding the regional and private equity funds, they perform region and country analysis in order to chose the country, which will fit the investment allocation and diversification requirement of the funds. “We will then look for opportunities in these regions/countries. The fund managers looking for investors in their funds also directly contact us”.

Oswald explained that their fund is focus on microfinance activity only and in that sense, is very sector focus. Each product they advise has its own specific regional, country and single fund exposure limits.

At the end of June, AGMF had 6 investments positions, presenting indirect access to 169 Microfinance Institutions in 48 countries, providing financial services to more than 670.000 micro-entrepreneurs in the world. “For AMPEF, we are in fund raising mode and we plan to make 10 to 15 investments”.

In terms of sales policy, “for AGMF we use a combination of banking platforms (large banks promoting our fund to their clientele) and fundraising companies with a geographic focus. For AMPEF, we have signed a number of fundraising agreements also with geographical focus. We obviously also use our personal networks acquired through our years of activity in the investment world but we do not internalize investor relations or fundraising”.

AGMF has currently more than $6M of AuM and is expected to reach over $20 million by the end of the year. For AMPEF they are looking to raise $100 million in the course of two years.

Oswald believes that compared to other similar funds, “the funds of funds in microfinance offers a differentiated investment strategy to deliver attractive returns while managing the risk efficiently. It provides an active regional and country allocation, an exclusive access to secondary opportunities, access to smaller more innovative funds, access to regional funds, access to opportunities dedicated only to microfinance investors. In that sense, it’s an ideal product for an investor seeking a global exposure to the microfinance investment universe”.

They invest only in funds, holdings or SPVs. They do not do direct investments into Microfinance Institutions except co-investments. The YTD performance of AGMF is 0.92%, which represents 2.21% annualized. The back tested performance presents a 5% – 6% net return in USD once the fund will reach its target size. For AMPEF they are targeting a relatively net return to investors.

Despite the crisis, international fund management companies have grown almost continuously within the Spanish market in recent years. With the exception of some periods in which their assets have fallen (as was the case in early 2012), collective investment institutions of foreign companies which are available for sale in Spain have doubled their assets under management in a period of three years. As Inverco’s latest estimates indicate, the assets of foreign CIIs in Spain would be around Euro 60 billion ($80 billion) as at the end of June. This figure doubles the Euro 30 billion estimated by Inverco in late 2009.

Inverco, which performs its estimates with the data from the CII’s from which it receives information (in this case, extrapolating data from 24 fund management companies with Euro 45.5 billion in assets under management, which are approximately 75% of the total), estimates that figure as the amount traded in assets amongst all domestic customers, both retail and institutional. The data shows an increase of 13.2%, a total of Euro 7 billion, in the first half of the year. The capital gain is comparable to that managed by national fund managers, which, according to Inverco and Ahorro Corporación, during the first half of the year saw asset gains of almost Euro 10.6 billion, i.e. around an 8.5% growth.

A 30% share

Inverco estimates that the total CII assets marketed in Spain, both national and international, would be close to Euro 200 billion (137.5 billion managed by domestic companies, and 60 billion by foreign ones, according to data as at the end of July). According to this information, foreign managers have achieved close to a 30% share of the Spanish market, the highest in history. That figure would be lower when using data from the CNMV ( National Securities Market Commission), which takes into account all fund management companies; according to its latest available data, as at the end of March 2013, the securities supervisor estimates the assets managed by international asset management companies at 44.5 billion. Even so, foreign CIIs would have a weight in the industry of around 20%, which is four times higher than the March 2009 share (7%). And the money keeps rolling into them: in total, the amount of net subscriptions to foreign collective investment schemes which facilitate their data to Inverco stood at Euro 2.9 billion in the second quarter of 2013.

Diversification and product offers

According to experts, this trend of capital raising and growth is due to several factors, including the smaller business volume of international institutions in Spain, which allows them greater potential for growth, and the strong commitment which private banks have made since last year to international funds domiciled in for example, Luxembourg, as a way of diversifying against the risk of peripheral countries.

The gradual return of investors to mutual funds, encouraged by the improvement of the economic situation but also by the decision by the Bank of Spain of penalizing “extratipados” (extra high interest rate) deposits earlier this year, also explains the positive dynamics of international, as well as of the domestic CIIs. The fund management companies surveyed also point out the innovative supply of products, which is in line with market developments. By type of products, the fall of extratipos on deposits and on the Spanish risk premium has led investors towards absolute return funds or actively managed fixed income as the great alternative, as well as towards those which distribute income and dividends. Those institutions which are active in such funds, such as Deutsche Asset & Wealth Management, JP Morgan AM or Swiss & Global AM, are amongst those which are attracting more deposits (see table).

The leading management company in terms of new deposits was BlackRock, with Euro 885 million. “These results demonstrate the strength of our global platform which allows us to offer innovative solutions in any asset class, in any investment style or in any geographical region. Such flows also reflect greater investor confidence in the recovery of the global economy”, says Armando Senra, CEO of the aforementioned management company in Latin America and the Iberian Peninsula.

Trend Continuity

The question which follows the semester’s figures is whether this rate of growth in foreign CIIs marketed in Spain can be maintained. Some market sources believe that it will not remain the same in the coming months, due to the mark left by the falls in emerging market bond funds which had been set up as an alternative to conservative funds, and which will cause further rejection by investors in the coming months. Thus, some experts talk of a slowdown in inflows from here to the end of year, but are more optimistic regarding their evolution in the long term. “It is important for the industry to grow as a whole, both the domestic and international fund management companies, to avoid cannibalization preventing the sustainable growth of companies,” says an expert.

INTERNATIONAL ASSET MANAGERS WITH MORE INFLOWS IN SPAIN. Second Quarter 2013

Asset Manager

Net inflows (Euro million)

BlackRock Investment

885

Franklin Templeton Investments

716

JP Morgan AM

422

Swiss & Global AM

257

Deutsche Asset & Wealth Management

239

Source: Inverco. Estimates for June 30th, with data from 24 asset managers with Euro 45.5 billion in AUMs.

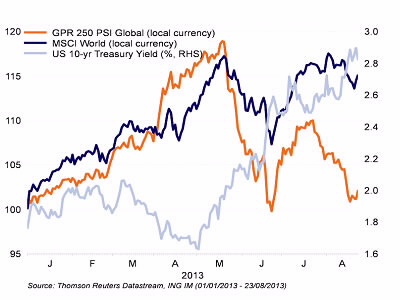

Wikimedia CommonsPhoto: Ikiwaner. The Effects of Rising Bond Yields on Markets

Investor risk appetite is getting depressed by the renewed rise in treasury yields in developed markets. In contrast to the correction in May/June, credit and commodity markets are holding up well. Real estate equities are having a hard time, while emerging market assets continue to struggle.

In this enviroment, ING Invesment Management scaled back their position in global real estate to neutral. Rising (real) interest rates in developed markets weigh relatively heavily on real estate equities as funding costs increase for this more leveraged asset class.

Real estate is very sensitive to the rise in treasury yields

Correction in equities, real estate and emerging markets

The renewed rise in government bond yields of developed markets has clearly started to weigh on investor risk appetite. With 10-year treasury yields in the US, UK and Germany increasing by 20 to 30 basis points in the past two weeks, especially equity and real estate markets have started to correct. The most probable reasons behind this are fears of an erosion of growth prospects and higher funding costs.

Also, emerging market (EM) assets have seen another round of downward pressure as higher US treasury yields further increased the risk of intensifying capital outflows. Especially emerging market currencies suffered last week, but also EM debt and equity markets underperformed their global peers.

Notable differences compared to last correction

At first sight, these dynamics look similar to the market evolution that occurred in late May and June. Some interesting differences are also visible below the surface, however. Most notable is the substantially higher resilience that is seen in credit and commodity markets. Both have hardly lost performance over the past two weeks, while they fell significantly during the May-June correction. Also, cyclical equity sectors are holding up quite well, while a notoriously “high beta” region like Europe is outperforming in equity space.

To view the complete story, click the attacehd document.

The past few weeks have been difficult for India as it struggles to stabilize its currency, the rupee, which has depreciated somewhat sharply against the U.S. dollar. The rupee has generally trended down over the past three years due to underlying fundamentals, but a widely anticipated tapering of stimulus by the U.S. Federal Reserve seems to have accelerated its fall. The currency movement has greatly impacted investor nerves and led them to increasingly question India’s balance-of-payments (BOP). However, fears of a potential BOP crisis may be overblown.

One of the key measures that determines the vulnerability of an economy to such a crisis is the external debt-to-GDP ratio. For India, that metric is nowhere close to the level of the early 1990s when the country needed to be rescued by the International Monetary Fund after finding itself on the verge of defaulting on its sovereign debt. Another reassuring factor is the country has foreign exchange reserves of nearly US$300 billion—although only enough to support up to seven months of imports.

Nonetheless, the falling rupee is a challenge to the economy, and policymakers can use this as a clarion call to bring in much-needed reforms. The Indian economy’s challenge has long been to attract sufficient foreign capital to fund domestic growth. On a sustainable basis, the flow of capital can occur either through a robust export industry or through foreign direct investment (FDI) in long-term projects. Reforms are critical to achieving either of these improvements.

However, we are concerned that policymakers are drawing the wrong conclusions about the current state of the rupee. Recent measures announced by the Indian government and the Reserve Bank of India (RBI) suggest that policymakers are viewing the rupee movements as a short-term issue while paying less attention to some of the structural problems confronting the economy. Hence the measures seem to focus on reducing the country’s need for U.S. dollars by restricting or raising the cost of “non-essential” imports such as LCD televisions or gold. Furthermore, in recent days, the RBI has placed some restrictions on the ability of its residents to move capital overseas. The efficacy of such measures is questionable.

The government may be aiming to plug the gap in funding India’s current account deficit by increasing reliance on shorter-term sources of funding, including external debt. While these measures may work in the interim, there must be a concerted effort to attract more sustainable sources of capital that can be achieved by easing the cost of doing business, and by improving domestic business competitiveness. Unfortunately, the country’s attempts to improve competiveness in recent years have been half-hearted. Last year’s much-heralded decision to open FDI in retail, for example, amounted to very little due to certain constraints placed on foreign companies seeking to invest in India.

The silver lining to all this is if recent events can become the impetus for Indian policymakers to pay attention to longer-term objectives of improving competition and productivity within the country. In the past, economic stresses have enabled progressive elements within the country to move forward with reforms. We continue to believe that the underlying attraction to investing in India remains intact, and may get a boost with a more thoughtful framework for economic reform.

Sharat Shroff, CFA Portfolio Manager Matthews Asia

The views and information discussed represent opinion and an assessment of market conditions at a specific point in time that are subject to change. It should not be relied upon as a recommendation to buy and sell particular securities or markets in general. The subject matter contained herein has been derived from several sources believed to be reliable and accurate at the time of compilation. Matthews International Capital Management, LLC does not accept any liability for losses either direct or consequential caused by the use of this information. Investing in international and emerging markets may involve additional risks, such as social and political instability, market illiquidity, exchange-rate fluctuations, a high level of volatility and limited regulation. In addition, single-country funds may be subject to a higher degree of market risk than diversified funds because of concentration in a specific geographic location. Investing in small- and mid-size companies is more risky than investing in large companies, as they may be more volatile and less liquid than large companies. This document has not been reviewed or approved by any regulatory body.

Foto: Mar del Este. ING vende su filial de seguros surcoreana por 1.650 millones de dólares a MBK Partners

ING announced this Monday that it has reached an agreement to sell ING Life Korea, its wholly owned life insurance business in South Korea, to MBK Partners for a total purchase price of approximately KRW 1.84 trillion (1.6 billion USD at current exchange rates). Under the terms of the agreement, ING will hold an indirect stake of approximately 10% in ING Life Korea for an amount of KRW 120 billion (106 million USD at current exchange rates).

ING has also reached a licensing agreement that will allow ING Life Korea to continue to operate under the ING brand for a maximum period of five years. In addition, over the course of one year, ING will continue to provide technical support and advice to ING Life Korea.

ING has made great strides in delivering on its programme to divest its insurance businesses as announced in 2009. Since then, ING has sold its insurance and investment management operations in Canada, Australia & New Zealand and Latin America, and a large portion of its insurance and investment management activities in Asia. In May 2013, ING’s U.S.-based retirement, investment and insurance business was successfully listed on the New York Stock Exchange, reducing ING’s stake to approximately 71%.

ING has accelerated preparations for the IPO of its European insurance and investment management businesses to be ready to go to market in 2014. The process to divest the remaining insurance and investment management businesses is on-going and any further announcements will be made if and when appropriate.

Transactions Details

MBK Partners is executing the transaction announced today through Life Investment, a private equity fund and will manage the investment in ING Life Korea for MBK Partners as well as for other investors in the fund. As part of the transaction, ING will hold an indirect stake of approximately 10% in ING Life Korea for an amount of KRW 120 billion (EUR 80 million at current exchange rates) which will be held by ING Insurance (ING Verzekeringen N.V.). As previously announced, the proceeds of the transaction will be used to further reduce the debt of ING Insurance.

The transaction announced today is subject to regulatory approvals and is expected to close in the fourth quarter of 2013. It does not impact ING’s Commercial Banking activities in South Korea.

Jeff Talpas. (Foto cedida por BBVA Compass). BBVA Compass pone a Jeff Talpas al frente de la nueva división de Wealth & Retail

BBVA Compass announced that William C. Helmshas been appointed vice chairman of the BBVA Compass board of directors.

Until now, Helms has led the bank’s Wealth Management business, overseeing private banking, asset management, international wealth management, broker-dealer activities and registered investment advisors.

“Bill brings a deep understanding of our strategic direction and will greatly enrich our board,” said Manolo Sanchez, BBVA U.S. country manager and president and CEO of BBVA Compass. “His leadership has helped us successfully implement our innovative, customer-focused business model across our growing U.S. footprint. We are fortunate to have his counsel.”

In addition to serving on the bank’s board of directors, Helms joins the board of BBVA Compass Bancshares, the bank’s holding company. He will be active in business development and in supporting the bank’s growth as directed by executive management. He also will oversee BBVA Compass’ national and local advisory boards and be involved in the bank’s government relations efforts.

Jeff Talpas, a member of the bank’s Management Committee who has overseen the bank’s Retail line of business, will lead the new combined Wealth & Retail Banking group. The move brings together all of the bank’s consumer segments in a single area led by Talpas, who has more than 25 years of experience in the financial services industry.

Helms joined Compass Bank in 2003 after serving in various leadership roles in the financial industry, including as co-president of Bank of America’s private bank. He serves on the Chancellor’s Council for the University of Texas System and as an advisory director for the McCombs School of Business at the University of Texas. He also serves on the board for the McGovern Museum of Health and Medical Science, and recently served on the boards of the Greater Houston Partnership, the Houston Grand Opera and the Museum of Fine Arts, Houston.