Photo: Jean-Christophe BENOIST. Have investors become more sensitive to central bank decisions?

Central bank actions have arguably been the single most important driver of market performance since 2009. The turnaround was catalysed by the US Fed’s pursuit of unconventional monetary policy, spawning ‘sons and daughters’ of QE as other central banks hopped on the bandwagon. Since the advent of QE1 (November 2008) the MSCI World Index has roughly doubled in US dollar total return terms, and 10-year treasury yields have been as high as 3.98% (April 2010) and down to as low as 1.40% (July 2012). No wonder investors are on tenterhooks when central bank decisions fall due, and why they scrutinise statements for evidence of future intentions. In the case of the bond markets, central banks have had an explicit policy of driving yields lower across the yield curve and implicitly pushing prices higher, in order to stimulate higher economic activity. In equities, however, policy has been less clear cut, but nevertheless the Fed in particular has spoken about confidence levels and wealth effects being driven by asset prices. It seems reasonable to deduce that they have been supportive of their move higher.

But, inevitably, as economic activity improves, the taps will have to be turned off. And therein lies the rub. Going cold turkey won’t work in a market that has become very fond of virtually unlimited liquidity. In this respect, US tapering is a more nuanced version of stopping QE: in theory stepping down asset purchases weans markets off central bank support a little at a time. But, the beginning of this withdrawal period is something that the world fears – not simply because of the risk of a policy error, but because a return to fundamentals-based investing has to occur. This could greatly affect areas of the capital market that have seen substantial inflows, an effect recently seen clearly in emerging market debt. The pace of economic recovery will differ across countries/regions, so greater care will have to be taken with asset allocation decisions. Making the correct call on fixed income exposure could be one of the most crucial decisions if the outlook for rates changes dramatically

Article by Bill McQuaker, Head of the Multi-Manager Team at Henderson Global Investors

Photo: Cogito Ergo Imago . Puerto Rico is the Weakest-Funded State Pension System According to Morningstar

Morningstar published the 2013 edition of its research report, “The State of State Pension Plans,” which analyzed current data for pension plans administered by all 50 states. New this year, Morningstar also included an analysis of the pension plan administered by the Commonwealth of Puerto Rico. Morningstar’s municipal credit analysts found that based on two key funding metrics, the state of Wisconsin had the strongest-funded state pension plan system while Illinois had the weakest among all 50 states, for the second year in a row. However, Puerto Rico ranked the weakest among all the pension systems evaluated by Morningstar.

Morningstar’s pension plan analysis focused on two key metrics:

Funded Ratio: the ability of a pension plan to meet its obligations, which is calculated by dividing the pension plan’s assets by its liabilities, and

Unfunded Actuarial Accrued Liability (UAAL) Per Capita: the unfunded liability per capita, representing the amount each person in the state would need to pay to fully fund this unfunded liability.

“Pension plans are inherently challenging to understand because of their complexity, weak disclosure requirements, and their sheer number. In addition, pension accounting is filled with assumptions, which leads to a lot of uncertainty. During the last few years, there has been a lot of negative attention focused on pensions, but new standards approved by the Governmental Accounting Standards Board could spark some significant changes,” Rachel Barkley, municipal credit analyst for Morningstar, said. “We’ve seen the funded levels of state pension plans continue to decline during the last year, albeit modestly, and the bankruptcy filings of San Bernardino, Calif. and Detroit, Mich. may have significant effects on the national level.

“On the upside, recent data indicate that long-term investment returns are generally in line with assumptions used by most pension plans. Additionally, in recent years most states have implemented some level of pension reforms.”

Additional key conclusions from Morningstar’s review of state pension plan systems include:

Wisconsin remains the strongest-funded state pension system; the state’s funded ratio is 99.9 percent, a 0.1 percent increase from last year, and the liability per capita is $18, which fell $3 from 2012;

Illinois continues to have the weakest-funded state pension system, with a 40.4 percent funded ratio, falling 3 percent compared to last year, and a liability of $7,421 per capita, an increase of more than $900 compared to 2012;

Puerto Rico’s pension system is weaker than Illinois’, with a funded ratio of 11.2 percent and a liability of more than $8,900 per capita. According to the Commonwealth, all three of its pension plans are projected to deplete their assets over the next few years, but recently passed reforms may mitigate the losses;

Twenty-six states and Puerto Rico fall below Morningstar’s fiscally sound threshold of a 70 percent funded ratio; Puerto Rico has the lowest funded ratio;

Twelve states have an aggregate funded ratio of 80 percent or more, led by Wisconsin for the second year in a row;

Seven states have a UAAL of less than $100 per capita. Wisconsin has the lowest UAAL per capita for the second year in a row. Thirteen states have a UAAL under $1,500 per capita, which is Morningstar’s threshold for “Good” unfunded liability levels; and

Alaska had the highest UAAL per capita for the second year in a row, currently more than $10,000.

Morningstar’s state pensions research report also includes a discussion of trends, pension reform, recent bankruptcies, shortcomings in disclosure and transparency, and federal legislation. Morningstar analysts also compiled aggregate pension data by state, including assets, funded ratio, and UAAL per capita, along with individual pension plan data by state.

Wikimedia CommonsFoto: Hermann Luyken. BBVA will Invest $2.5 Billion in South America by the End of 2016

BBVA president and COO Angel Cano presented the bank’s strategic plan for South America, with investments totaling $2.5 billion over the next four years (2013-2016). “Our goal is to become the region’s top digital bank and the one most preferred by customers,” Mr. Cano said at BBVA’s Economic Symposium on “Investing in South America” in Lima (Peru). “South America is of fundamental importance for the group’s development,” he added.

During his address BBVA’s president emphasized that South America is “a key element” of the group’s strategy. For this reason it will continue to boost its presence in the region. “Therefore today we are launching a very ambitious investment plan covering the next four years,” he explained.

Mr. Cano pointed out that “emerging countries will contribute more than 60% of world growth in the next decade.” In this regard he emphasized that emerging economies will lead world growth and South America “will continue play an important role.” Since 2007 the region’s growth has been nearly four times that of developed countries and according to expectations growth will double in the coming years. The Andes region (Chile, Colombia and Peru) will be one of the most dynamic.

“This is because these countries together with Mexico have formed the Pacific Alliance and have started a process to integrate trade and finance, and facilitate the movement of people”, he said. “This will certainly boost economic activity in the region.”

The 2013-2016 strategic plan: $2.5 billion in investment

“Some 40% of this investment is earmarked for technology-related projects that will make BBVA the region’s leading digital bank. The remaining 60% will be spent on growth-related items that extend infrastructure and the distribution networks,” he added.

By 2016 it plans to double the number of internet customers to five million and multiply by eight those that bank via mobile devices.

Mr. Cano went on to explain the three basic areas of the strategic plan. “The first aspect entails segmented and specialized management, which aims to deepen customer understanding. We want to know their needs and the key to this is segmentation,” he said. “Secondly, we are going to extend our distribution network by increasing the branch network 18% and adding 30% more ATMs. We will also encourage digital channels because they will play a fundamental role in banking in the coming years. Lastly, we are going to continue the transformation process, speeding up processes and making them safer and more reliable by means of digitalization and automation.”

Foto: Poco a poco. La plataforma de alternativos de Citi supera los 500.000 millones de dólares en activos bajo gestión

Citi has surpassed $500 billion in alternative assets under administration, affirming its leadership as one of the largest fund administrators in the alternative asset management industry.

The $500 billion figure includes over $300 billion in Hedge Fund assets under administration, and over $200 billion of committed Private Equity capital under administration.

“Our leading solutions across the hedge fund and private equity asset classes have positioned us well to capitalize on the ever increasing trend towards convergence of styles in alternative asset management,” said Mike Sleightholme, Global Head of Hedge Fund Services, and Joe Patellaro, Global Head of Private Equity Services, in a joint statement. “As institutional investors continue to demand more operational capabilities from their alternatives managers, Citi is there to provide superior solutions across our global platform. These factors have been a growth engine for our businesses.”

This is a significant milestone for Citi and shows that clients are embracing the cutting edge technology and tailored services needed to grow their businesses.

Recent hedge fund mandates awarded to Citi include Mackenzie Investments Pte. Ltd., the Singapore–based subsidiary of a leading Canadian asset manager, while recent private equity mandates include Delta Partners, a leading management advisory and investment firm.

Citi also launched its private equity services in Luxembourg through a dedicated Centre of Excellence for closed-ended funds, allowing the bank to provide end-to-end private equity servicing solutions in the growing Europe, Middle East and Africa (EMEA) market.

Photo: Stéphane Cloâtre. The Danger of Duration With a Monetary Policy Change

The Federal Reserve’s years-long zero-interest rate policy has flattened Treasury yields to where rising interest rates and inflation are almost assured manifestations, according to Pioneer Investments’ latest blue paper, “The Danger of Duration With a Monetary Policy Change”, written by Michael Temple, Senior VP and Director of Credit Research. In this scenario, “investors may have to face the threat of rising bond yields with periods of significant volatility”.

The Key Points for this Blue Paper are:

“The Great Monetary Experiment,” the Federal Reserve’s zero rate policy, may be coming to an end. But many investors may be being lulled into a potential false sense of security that rising rates are a long way off. The Fed not only expects the yield curve to steepen, but may in fact encourage it. This could be a wakeup call.

The U.S. economy may likely surprise to the upside shortly, driven by multiple secular forces including a resurgence in home prices and home construction, an energy renaissance, and a revival of credit demand.

This would propel a normalization of the yield curve and many scenarios could emerge. With the Fed Funds rate anchored at zero, the sequencing and speed of monetary accommodation removal could have consequences as to how fast the yield curve adjusts.

The fear of an imprecise course correction is palpable among many investors and economic pundits. There is a growing fear that the Fed may commit to zero far longer than economically necessary. The consequence could be an escape from Treasuries by retail, institutional and foreign investors.

Investors need to be aware of the potential consequences to their fixed income investments as this paradigm shift takes place. The blue paper explores the math of duration, which is particularly dangerous in this historicallylow yield environment. However, not all duration is bad. Indeed, spread duration has the ability not only to help cushion the loss but also provide strong and positive excess returns in a rising yield-curve and interest-rate environment.

As financial markets grapple with the coming structural change in the yield and interest rate environment, high-quality, fixed-income bonds will likely experience periods of significant volatility. The transition to a new investment paradigm is rarely smooth.

Finally, the report takes a look at the fixed income subsectors that are being viewed as “refuges” from what may be a turbulent transition to higher rates.

You may access the complete report through this link.

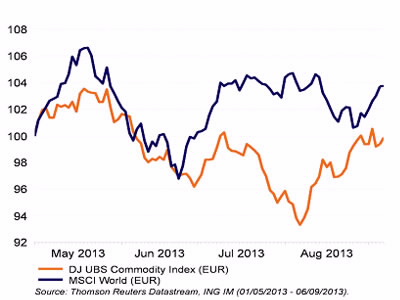

Wikimedia CommonsBy Hao Wei from China. Improvement in Chinese Data is Very Welcome

Data indicate that the Chinese economy may have found some temporary support. According to the MarketExpress report published by ING Investment Management, Further support for commodities and other risky assets could come from abating tapering fears and a stabilization in bond yields.

For equities, commodities and other risky assets it will probably not be a smooth ride in the weeks ahead. We mention risks as geopolitics (Middle East), tapering and the German elections (September 22). Furthermore, Japan has to decide upon the increase of the sales tax and in the US debt-ceiling discussions will soon emerge. In the near term, these factors could weight on risky asset prices.

Nevertheless, we remain inclined to look for more rather than for less cyclical tilting. We point to the ongoing favourable economic data, globally. Recently, the improvement in Chinese data also provides support. The data add more juice to the overweight in cyclical sectors. Furthermore, the situation changed for the better for commodities.

Commodities bottomed in August after better Chinese data

Rising yields are biggest headwind for commodities

The biggest headwind for commodities currently seems to be the rise in bond yields in the developed economies. Not only capital flows to emerging markets are reduced for that matter, they are also putting (commodity) demand and emerging market currencies under downward pressure. Depreciating currencies in the emerging world themselves also prevent supply discipline at commodity producers in emerging markets. After all, depreciating currencies lower their production costs and increase their revenues in (appreciating) US dollars.

Welcome support for commodities and risky assets

As already said, the recent improvement in Chinese data is very welcome in the September month which is traditionally the weakest month in the year for equities, commodities and other risky assets. Currently, the better data in China were even more welcome against the background of some additional risks (Middle East, tapering) that the global economy and global markets have to digest. A most welcome support for the commodity asset class would arise from abating tapering fears and from some stabilisation in government bond yields.

To view the complete story, click the attached document.

Foto: Martin Falbisoner. CTPartners adquiere la firma de headhunters mexicana Taylor Executive Consultancy

CTPartners, a leading global retained executive search firm, has signed a Letter of Intent to acquire Taylor Executive Consultancy Latam S. de R.L. Eduardo Taylor will join CTPartners as Managing Partner, Mexico.

Taylor is a seasoned multinational executive search consultant with over 17 years of experience placing executives in global and regional companies. His primary focus is in the Industrial and Consumer Products markets where he has completed searches at the most-senior levels, including CEO and Board of Directors. He has also worked with clients on succession planning and management assessment.

Brian Sullivan, Chief Executive Officer of CTPartners, said, “Eduardo is a client-centric executive search consultant who has demonstrated superb leadership in running his own successful search firm, as well as when he was the Managing Partner of the largest search firm in Mexico. Eduardo is highly regarded in the board rooms of the largest Mexican companies throughout the country, and we are very pleased to have him leading our search consultancy.”

Nestor D’Angelo, Managing Partner for CTPartners in Latin America, said, “Eduardo’s commitment to his clients and his personal standards for providing the very best search experience are exactly what CTPartners is all about. Eduardo will complement our strong team in Mexico, an extremely important market for us. We are very excited he has joined our Latin American team to continue to strengthen our leadership in the region.”

Taylor commented, “CTPartners is a perfect fit for me and for clients in Mexico. The philosophy of transparency and accountability on every search is what I have built my career on, and I am thrilled to join a firm with the same principles. Global, regional and Mexican companies will benefit from CTPartners consultative, quality-driven approach.”

Wikimedia CommonsPhoto: Jason Auch. J.P. Morgan Appoints Edinardo Figueiredo to Lead Brazil Private Bank Business

J.P. Morgan announced that Edinardo Figueiredo will join the firm to head its Brazil Private Bank business.

He will be based in São Paulo and report jointly to José Berenguer, Brazil Senior Country Officer of J.P. Morgan, and Chris Harvey, Head of Latin America Private Banking.

“Edinardo is a first-rate private banker and business leader, and we are thrilled that he is joining J.P. Morgan,” Mr. Berenguer said. “As we build upon our continued momentum in Brazil, we are fortunate to be able to draw on Edinardo’s deep understanding of the market, significant investment experience, and strong management skills.”

Mr. Figueiredo, 45, joins J.P. Morgan from UBS, where he was Chief Executive Officer (CEO) of its Brazil wealth management business. He was previously with Banco Itau, where he was most recently CEO of its private banking business in Luxembourg and Switzerland. He has also held senior positions focusing on investment products at BankBoston and ABN AMRO in Brazil.

“Brazil is a key market for J.P. Morgan, and our clients look to us for local and global capabilities to serve their complex wealth management needs, particularly during volatile markets,” said Harvey. “Throughout his career, Edinardo has shown himself to be a strong and strategic partner, and we look forward to his leadership.”

MSCI has launched a new Emerging Markets index – the MSCI EM Beyond BRIC Index. The index, a subset of the widely used MSCI Emerging Markets Index, is comprised of 17 countries and excludes the BRIC countries – Brazil, Russia, India and China – which currently represent over 40% of the MSCI Emerging Markets Index.

“The BRIC countries have been recognized over the past few years as key drivers of economic growth within the Emerging Markets and many institutional investors already have exposure to those countries within their portfolios,” said Deborah Yang, Managing Director and Head of the MSCI Index Business in Europe, the Middle East, Africa and India. “We have launched the MSCI EM Beyond BRIC Index in response to client demand and believe it offers a new way to track and evaluate the Emerging Markets opportunity set for those wishing to invest in countries outside the BRIC region.”

To help diversify the representation across the 17 countries in the index, the weights of larger Emerging Market countries such as Taiwan and Korea are capped on a quarterly basis at 15%, giving greater prominence to smaller Emerging Market countries including Thailand, Malaysia and Indonesia.

The MSCI EM Beyond BRIC Index has outperformed the MSCI Emerging Markets Index since 1999 (12.0% gross annualized return in USD vs 11.1%). Between 1999 and 2007, the MSCI Emerging Markets Index outperformed the MSCI EM Beyond BRIC Index by 2.1 percentage points (20.1% vs 18%). Since 2007, the MSCI EM Beyond BRIC Index has had a positive annualized performance of 2.83% while the MSCI Emerging Markets Index had a negative performance of 2.1%.

The index may be licensed for benchmarking or as the basis for financial products such as ETFs and structured products.

Wikimedia CommonsPhoto: Pete Stewart . WE Family Offices refuerza su equipo y estrena oficina en Nueva York

WE Family Offices, founded in January of 2013 by Managing Partners Maria Elena Lagomasino, Santiago Ulloa and Michael Zeuner, announces the hiring of three industry experts to its team of professionals. Each brings extensive wealth management experience to the firm, which has recently surpassed $2 billion in assets under management.

Family office veteran Bruce Arella will join the global firm as a partner and head of real estate investing and will be responsible for serving US-based clients. He will join the firm’s Strategic Investment Committee and Implementation Committee and will be based in WE’s newly opened Manhattan office.

In addition, the firm has recently hired Joseph Kellogg and Elaine King to join its Miami office. Mr. Kellogg comes on board as the firm’s wealth planning executive to work with clients and their external tax and estate planning professionals. Ms. King joins as director of family education and governance to advise client families and develop educational programs, content and learning events on topics including succession planning, financial literacy, and mission and strategy.

New partner Bruce Arella echoes the firm’s commitment to providing independent advice to UHNW clients saying, “The unique business model and approach of WE Family Offices helps clients look at their wealth strategically, as they would any business or enterprise. They stay in control of their wealth, while we provide them with the support and services they need. The more transparent, retainer-based service model is something I looked long and hard to find and represents the leading edge in family wealth management.”

Managing Partner and CEO Maria Elena Lagomasino comments, “WE Family Offices’ mission is to serve as our clients’ advocate, providing independent advice without any regard to sales of product. Each of these individuals joins the firm with a long track record of advocating for and advising wealthy families, and we are fortunate to have them join our team”.