Insigneo announced the addition of Robert Moore as Senior Vice President within the team led by Alfredo Maldonado, Insigneo’s market head for New York and the Northeast.

Moore incorporation brings over three decades of international financial experience, further bolstering Insigneo’s commitment to providing exceptional wealth management services on a global scale, the firm said.

Starting his career as an Investment Advisor at PaineWebber, Robert held key roles at investment firms including Barrett & Co., the Bank of Bermuda, Merrill Lynch, and Morgan Stanley where he assumed the position as Senior Vice President in the Global Wealth Management Group, specializing in meeting unique financial needs for clients in the UK, Australia, New Zealand, Bermuda and the Caribbean.

Throughout his career, Moore has been actively involved in various philanthropic endeavors and cultural organizations, including currently serving on the Boards of the American Friends of the Australian National Maritime Museum, the American Friends of the Royal Museums Greenwich, and the American Friends of the Old Royal Naval College in the UK, Insigneo added.

“I am absolutely delighted to be joining Insigneo. I conducted a thorough investigation into several independent firms, and I am certain that my clients and I will benefit tremendously from Insigneo’s platform, support, and extensive experience and expertise with serving Offshore clients. I am very much looking forward to further assisting my existing clients, and growing my Offshore business, through my affiliation with Insigneo,” mentioned Moore.

On the other hand, Maldonado commented: “We are thrilled to have Robert join our Insigneo family. Not only is he an amazing global advisor and philanthropist, he also has tremendous integrity and embodies our principles and culture. We are lucky to have Robert on the team and look forward to him elevating our enterprise.”

IFC, a member of the World Bank Group, and T. Rowe Price announced plans to create a pioneering global blue bond strategy to increase access to finance for blue projects in emerging markets and help improve market standards for the nascent blue bond market.

The proposed T. Rowe Price Emerging Markets Blue Economy Bond Strategy (T. Rowe Price Blue) is expected to mobilize international capital from eligible investors to support blue labeled investments in emerging markets globally through blue bonds issued by financial institutions and real sector companies.

“The investor capital deployed into blue bonds through T. Rowe Price Blue will make a vital contribution to furthering a blue economy,” said Makhtar Diop, IFC Managing Director. “This first-of-its-kind strategy with a dedicated vehicle for blue investment will also be critical in promoting sustainable capital markets in emerging markets and developing economies.”

Blue investments seek to provide competitive returns while supporting the health, productivity, and resilience of the world’s oceans and water resources, which are vital for sustainable global development, especially in the face of climate change, overfishing, and pollution. Momentum is growing for blue finance, with interest from both investors and issuers in blue bonds and loans that fund ocean-friendly projects and safeguard clean water resources.

“We are proud to partner with IFC to further the blue economy,” said Rob Sharps, CEO and president of T. Rowe Price. “We’re gratified that our emerging markets investment experience can be leveraged in such a meaningful, innovative, and important way, providing opportunities for

positive investment returns while supporting sustainable capital markets and preserving valuable water resources for generations to come.”

The proposed T. Rowe Price Emerging Markets Blue Economy Bond Strategy will draw on IFC’s leadership in the blue bond market. Since 2020, IFC has invested and mobilized more than US$1.4 billion through 12 blue bonds and loans issued by private sector financial institutions and real sector corporates across emerging markets and developing economies.

To bolster the supply of blue bonds issued by real sector borrowers, T. Rowe Price Emerging Markets Blue Economy Bond investment activities will be complemented by a Technical Assistance Facility, or TAF, managed by IFC, designed to increase the quality and quantity of blue bond issuance in emerging markets.

By partnering on this innovative strategy, T. Rowe Price and IFC are sending a clear message to the market on the importance of mobilizing capital needed to make meaningful progress towards achieving the Sustainable Development Goals. Specifically, UN SDG 6 “ensure availability and sustainable management of water and sanitation” and SDG 14 “conserve and sustainably use the oceans, seas and marine resources”.

To ensure that the mobilized resources achieve the desired impact objectives, IFC and T. Rowe Price have jointly developed Blue Impact Investment Guidelines that will be implemented specifically for this strategy. These guidelines are aligned with IFC’s Guidelines for Blue Finance which were published in January 2022 to guide IFC’s own investments in support of a Sustainable Blue Economy.

Fidelity International has announced that Anne Richards, who has been CEO of Fidelity International for the past five years, will be stepping down from her full-time executive position. However, she will remain involved with the company in the capacity of Vice President.

In her new role as Vice Chair, Richards will focus on nurturing key external relationships and strategic partnerships, leveraging her extensive experience and insights. The transition will be managed over the coming months under the guidance of the Fidelity International Board. The organization is yet to announce details regarding her successor as CEO.

Reflecting on Anne’s tenure as CEO, Abby Johnson, Chair of Fidelity International, highlighted her significant contributions. “Anne has been instrumental in driving our organization forward, particularly in expanding our capabilities and services across various markets. Her leadership in sustainability has set a solid foundation for our future endeavors,” said Johnson. She also credited Anne for her efforts in fostering a diverse and inclusive workplace, introducing enhanced parental and carers leave policies, and advocating for dynamic working environments.

Fidelity International stands as a testament to long-term, purpose-driven investment strategies. Serving over 2.9 million customers worldwide, the organization manages $714.3 billion in total assets. With operations in more than 25 locations, its client base ranges from central banks and sovereign wealth funds to private individuals. Fidelity’s dedication to investment solutions and retirement expertise is evident in its comprehensive approach, including investment choices, administration services, and pension guidance.

The organization emphasizes that it offers information on products and services but does not provide investment advice tailored to individual circumstances, except under specific conditions by an authorized firm. Fidelity International operates as a collective of companies outside North America, focusing on delivering quality investment management services globally.

As Anne Richards prepares to transition to her new role, Fidelity International continues its commitment to building better financial futures for its clients, employees, and communities worldwide. The organization upholds its legacy of thinking generationally and investing for the long term, evident in its approach to asset management and solutions for workplace and personal investing.

While cryptocurrency used to make headlines for its radical performance, these days it’s often in the news because of lost fortunes, exchange bankruptcies and business fraud, said a Morgan Stanley report.

As investors monitor the crypto market, now is a good time to search for insights from past cryptocurrency trading cycles to understand what may lie ahead, the wirehouse added.

How “Halving” Affects Crypto Supply

Bitcoin is the leading cryptocurrency, accounting for about 50% of total digital assets by market capitalization, and, in many ways, acts as a proxy for the overall crypto market. One unique aspect of bitcoin is that it is designed to go through a process called “halving” that creates scarcity, so that bitcoins can maintain their value. Specifically, every four years, the number of bitcoins created every 10 minutes is cut in half. Eventually, when there are 21 million bitcoins in existence, no more bitcoins will be mined.

By intentionally limiting the supply of new bitcoin, the shortage caused by the halving can affect the price of bitcoin to potentially spur a bull run. There have been three such runs on bitcoin since its inception in 2011, each lasting 12 to 18 months after the halving.

The four-year cryptocurrency cycle roughly corresponds to the four seasons of the year:

Summer: Historically, most of bitcoin’s gains come directly after the halving. This bull-run period starts with the halving event and ends once the price of bitcoin hits its prior peak.

Fall: Once the price surpasses the old high, it tends to attract interest from the media, new investors and businesses, which can then drive prices even higher. This period represents the time between when bitcoin passes the old high and reaches a new one, which signals that the bull market has run its course.

Winter: In previous cycles, the bear-market decline has come when investors decided to lock in their gains and sell bitcoin, causing prices to drop while scaring off new investment. This period takes place between the new peak and the next trough. There have been three winters since 2011, lasting about 13 months each.

Spring: During this period preceding each halving, the price of bitcoin generally recovers from the cycle’s low point, but investor interest tends to be weak.

Is Crypto Spring Here?

Just as a farmer avoids planting seedlings in the winter or too late in the spring, crypto investors want to know when crypto spring has arrived to maximize their investment “growing season.” Here’s what to consider when trying to determine whether crypto spring is truly here, or if the market is still in the midst of crypto winter:

Time since the last peak: The trough of bitcoin in previous crypto winters has historically occurred 12 to 14 months after the peak.

Magnitude of bitcoin drawdown: Previous troughs were about 83% off their respective highs.

Miner capitulation: When bitcoin has neared the trough of past cycles, many bitcoin miners shut down their operations because they were losing money. When a miner shuts down, it makes it a little easier for the remaining miners. A statistic called “bitcoin difficulty” measures how easy or hard it is to mine bitcoin. When difficulty decreases, it is a sign the trough may be near.

Bitcoin price-to-thermocap multiple: “Thermocap” measures how much money has been invested in bitcoin since its inception. A lower bitcoin price-to-thermocap multiple indicates a trough, while a higher multiple indicates a peak.

Exchange problems: When the price of crypto drops, it tends to impact the viability of some crypto exchanges. Bankruptcies, bad news or new regulations may all indicate a trough.

Price action: A 50% increase in price from bitcoin’s low is typically a good sign that the trough has been achieved, although there have been examples of such a gain being followed by significant declines.

Estimates of when exactly the next halving will occur vary, but history indicates it has the potential to occur sometime around April 2024.1 Based on current data,1 signs indicate that crypto winter may be in the past and that crypto spring is likely on the horizon. However, keep in mind that there have only been three crypto springs to date. In other words, there is still a lot to learn.

One key thing to keep in mind: As with any investment, past performance doesn’t indicate future results. Potential risks such as encryption breaking, software bugs, recession or coordinated government action could emerge before the expected halving and disrupt the cycle.

While no one can tell you if now is the right time to buy or sell cryptocurrency, today is the right time to learn more about the crypto market’s cyclical tendencies so that you can ask questions, monitor trends and determine for yourself if the cycle will repeat a fourth time and whether to invest.

Lunate, a global alternative investment management company with more than $50 billion of assets under management, and BNY Mellon are investing in a new company, Alpheya, that will develop a customized wealth management technology platform for wealth and asset managers in the Middle East and North Africa (MENA).

Based in the Abu Dhabi Global Market (ADGM), Alpheya will be funded with a capital commitment of $300 million and is expected to start serving clients in 2024. BNY Mellon has a minority share in the company, says a statement released by BNY Mellon.

The new financial technology company will meet the growing demand in the Middle East from wealth and asset managers, private banks, and investment houses, for an end-to-end digital solution that delivers a range of services, including client onboarding, financial planning, portfolio construction, trading and rebalancing, risk management reporting, and analytics. Utilizing the latest security and data architecture, the platform will be designed to meet the data privacy and localization requirements for each market in the region, the firm adds.

“We look forward to leveraging our local industry and investment expertise with BNY Mellon’s long history in wealth technology solutions to help wealth managers in the Middle East meet the evolving needs of their clients,” said Seif Fikry, Managing Partner, Lunate. “Not only will this new platform transform wealth capabilities for financial institutions across MENA, it will also strengthen Abu Dhabi’s role as a global hub for wealth and asset management.”

Built on open and modular architecture, the platform will provide the digital tools and solutions for clients to meet the growing challenges of managing complex technology and numerous investment vehicles, so they can focus on engaging with their clients and expanding their business.

“BNY Mellon is one of the largest wealth management technology providers, and the new company will leverage our deep expertise in providing wealth managers and investors digital tools and solutions for enhancing portfolio management, seamlessly connecting to local and global providers, and harnessing world-leading data management capabilities,” said Akash Shah, Chief Growth Officer, BNY Mellon. “We are proud to invest in an organization which recognizes the need for a locally-developed wealth technology solution, and to support the burgeoning wealth management industry in the region.”

“Wealth franchises today are managing complex technology environments and a multitude of investment options, that are all supported by more data and analytics and increasingly sophisticated risk management practices,” said Roger Rouhana, CEO of Alpheya. “The creation of a wealth technology solution that provides digital tools and software solutions in one integrated platform and is customized for the Middle East, will greatly enhance the ability of regional wealth managers to grow in a scalable and client-centric way.”

From March 2022 through the publication of this article, the Fed raised its funds rate target 525 basis points to 5.5%, a nearly 23-year high. The funds rate target is now set more or less in line with the 1982-2008 average of 5.31%, up significantly from the period of near-zero rates that ran through most of the 2008-2021 period. The implications of interest rate (or cost of capital) normalization will reverberate through balance sheets, correlations, portfolio construction and portfolio management.

Regarding balance sheets, a gnawing question bandied about the financial press and market participants is whether there is too much debt in the system. This topic is always a concern from a macro perspective. Still, from an investment manager’s and portfolio’s perspective, the question should be, “Are you selecting ‘good’ balance sheets and avoiding ‘bad’ balance sheets?” A disciplined selection process between balance sheets is one of the hallmarks of successful fixed income investing.

In today’s fixed income environment, concern is emerging around the impact of inflation and rising labour costs on corporate balance sheets. Still, even more unease is developing around government balance sheets. We believe the current budget situation is a risk and one of several headwinds we are currently experiencing in the market. There will be more and more Treasury issuance, and the Treasury plans to term out some of this new paper, which means potentially more supply further out the curve. That, combined with the Fed’s quantitative tightening as it slowly winds down its balance sheet, inflation pressures deriving from labour, oil or lingering supply chain hiccups, are all part of the mosaic pushing the cost of capital higher and feeding expectations that the new era of normal interest rates will be here for the longer term. It’s the new normal.

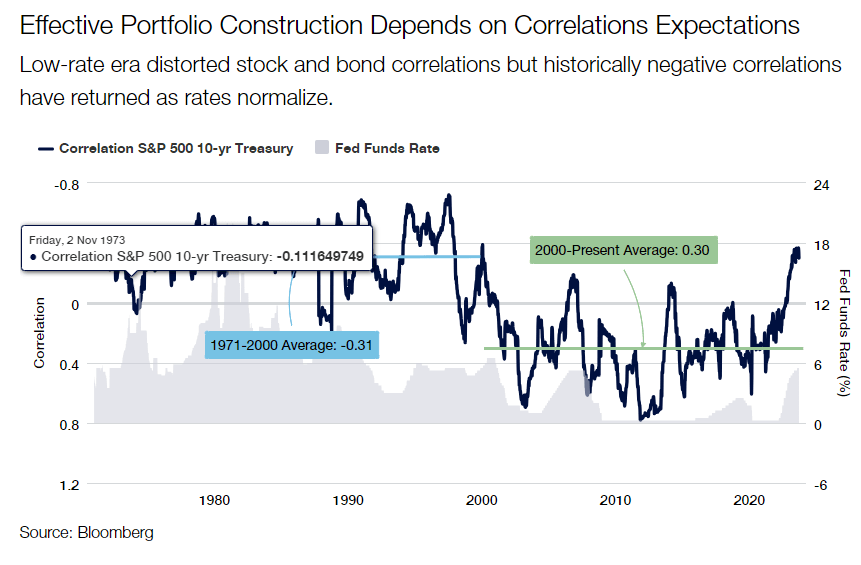

Regarding correlations, a critical change resulting from the higher interest rates is that it forces investors to wrestle with how bonds will fit into a broader portfolio going forward. As with balance sheet selection, the normalization of interest rates impacts fixed income’s role in portfolio construction. Recall that during the low-rate era, which goes back to about the year 2000 (during the dot-com bust when the Fed pushed its funds rate down as low as roughly 1% in 2003), the correlation between fixed income and equities turned positive and stayed there for about 20 years – nearly a generation.

Bonds performed well because interest rates were declining, and the resulting drop in the cost of capital drove equities higher. This period is fondly (or not so fondly in retrospect) remembered as the Greenspan, then Bernanke, then Yellen “put” as successive Federal Reserve leaders extended the Fed’s role beyond its traditional mandates to include suppressing excessive equity market volatility and keeping equity investors happy. It was not until 2022 that the Fed finally rid itself of this perceived obligation. That occurred when correlations spiked back into negative territory in tandem with the current tightening cycle.

In other words, with the normalization of interest rates, it’s reasonable to expect a return to negative correlations between fixed income and equity performance, as we saw before the low-rate era that dawned in 2003. During the 30 years from 1971 through 2000, the correlation between stocks and bonds was -0.31. That correlation flipped to +0.30 from 2000 through today, even considering that correlations normalized back to about -0.30 in recent months.

Regarding portfolio construction, the shift in cross-asset correlations has two significant consequences: First, bonds can behave differently from stocks in how they perform directionally. Secondly, fixed income is re-establishing its traditional role as ballast in an investment portfolio because there is actual yield in holding bonds. Over time, fixed income holdings help dampen portfolio volatility. The market takes care of itself, rather than the Fed taking care of the market.

From a portfolio construction perspective, asset allocators may now use fixed income to dampen the volatility of their equity holdings, provided the normal negative correlations between the asset classes continue. Given the likelihood of the Fed’s “higher rates for longer” mentality in the current inflationary market environment, negative correlations should extend into the foreseeable future.

We expect market volatility to rise as central banks no longer desire to suppress the cost of capital to push demand forward and stimulate growth. With increasing volatility comes the risk of dislocation, which, in our view, calls for managing fixed income portfolios and fixed income asset allocation with a much more agile and flexible approach. That contrasts with many managers’ predominant ‘siloed’ approach to improved income management.

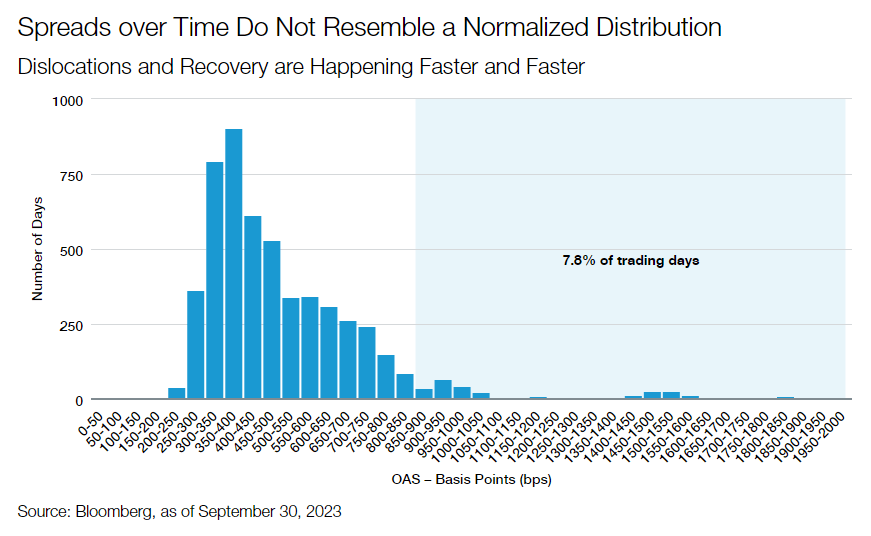

The speed at which credit spreads widened and recovered has increased remarkably over the past decade, most notably during the COVID crisis. During the dot-com bubble, high yield spreads blew out to more than 600 bps, and it took about three years for spreads to narrow to below that mark. During the Global Financial Crisis, it took high yield spreads about a year to complete the widening to narrowing cycle. Fast forward to the COVID crisis, and that same cycle took just one month. Why has this cycle shortened so much? Look to the Fed. The Fed has learned to utilize a variety of liquidity measures, tools, and communication to steady financial markets during each subsequent crisis. It doesn’t mean another era of zero interest rates is around the corner. Still, it’s essential to understand how much more effective central banks have become at providing support during uncertain situations.

This affirms our conviction that flexibility concerning a manager’s investment style and an investor’s asset allocation decisions will hold greater importance in achieving successful outcomes. These outcomes are where active management’s skill and agility should provide a distinct advantage over passively managed fixed income portfolios. From a portfolio management perspective, we favour having a defensively minded approach for most of a market cycle to allow the rotation into attractively priced assets when markets sell off.

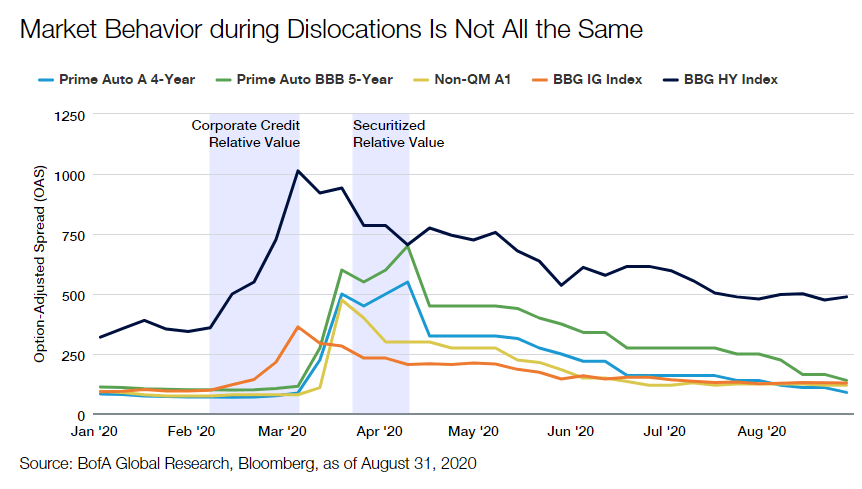

This style of management will likely be increasingly important going forward. Dislocations are increasingly more nuanced. Suppose you want to outperform and generate robust returns and income for your investors. In that case, managers need to understand that different markets dislocate at different times, even within a broader market sell-off. Within that period, if you are executing and making decisions faster, you can earn attractive excess returns across different sub-markets as value appears.

Another source of income in the fixed income markets is the ‘pull to par’ effect. Income matters, and savvy managers can boost returns during a period of high coupon securities. Agile investors may add lift returns by selecting bonds issued during the low-rate period but are now trading at a discount. As these bonds return to par closer to maturity, that provides impetus to aggregate returns.

For investors, we believe the implications of the new era of income focus on 1) the role of fixed income in the broader portfolio and 2) how best to capture value in an environment characterized by higher rates and higher volatility.

Investors need to re-evaluate how the fixed income asset class will behave from a return, risk, and correlation perspective. Higher rates and positive real yields allow fixed income to reassert itself as a provider of ballast to the broader portfolio. With the central bank ‘put’ in hibernation, it is possible to see the correlation return to, and remain, negative as was the case for markets before 2000.

We believe higher rates will be coupled with higher volatility. A moderate market dislocation occurs once every 2-3 years, and we expect this trend to continue. For investors, this means incorporating more flexibility in how managers capture opportunity and how allocators manage asset allocation. We think ‘style box’ investing will be more challenging – higher volatility favors strategies with a broader opportunity set and managers who quickly capture dislocation. Allocators, if possible, should incorporate this flexibility into their own decision making, as downside protection and the ability to reallocate capital to dislocated markets can enhance long-term excess returns.

Opinion article by Jeff Klingelhofer, co-head of investments and Managing Director for Thornburg IM.

Photo courtesyLuca Paolini, Chief Strategist of Pictet Asset Management

Just as the markets had started taking the Ukraine-Russian war in their stride, the latest grim developments in the Middle East remind investors of how quickly geopolitical crisis can boil up. The conflict in Gaza comes at a point when economies are looking vulnerable.

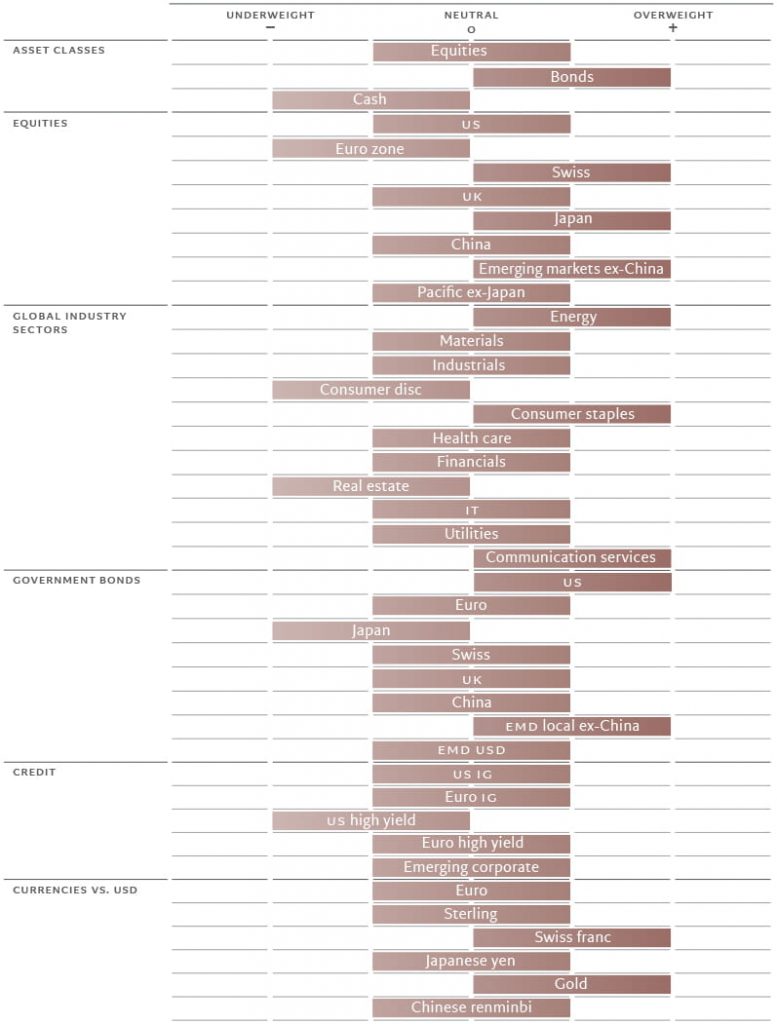

The United States is in our view at the cusp of slowing significantly as US Federal Reserve rate hikes of the past year feed through to consumers. And though the Chinese economy looks like it has troughed, sentiment there remains depressed. Elsewhere, Europe’s resurgence is slow in coming. As a consequence we remain neutral equities. Valuations for stocks may be more palatable following the market’s recent pull-back and corporate earnings look resilient for now, but muted economic growth means there’s no compelling case to buy.

Our defensive stance is reinforced by our overweight in bonds.

Fixed income markets have suffered significant upheaval this year and the prospect of a surge in government bond supply is a growing worry given substantial public sector deficits, particularly in the US. Yet with bonds offering the most attractive yields for many years – they hit 5 per cent on 10-year US Treasuries, while real yields are at multi-decade highs – and a likely slowdown in both growth and inflation, we continue to hold an overweight in fixed income.

Fig 1. Monthly asset allocation grid

November 2023

Source: Pictet Asset Management

Our business cycle indicators show that while emerging market economies remain resilient, developed markets are slowing. Within developed markets, the euro zone has better prospects than the US, although both are growing below potential. Over the short-term, the stickiness of inflation remains a concern, with headline price pressures having picked up. And should the conflict between Hamas and Israel expand beyond that immediate region, oil prices would respond. But we think overall that disinflationary forces hold sway, driven by subdued growth and easing supply chain pressures.

We expect the US economy to slow to well below potential and this year’s current rate of rate of expansion of 1.9 per cent. That’s mostly because we expect consumption to be muted as American households work through the savings surplus they built up during Covid. The euro zone is also subdued, with countries dependent on manufacturing faring especially badly. But that should improve with China’s slow recovery.

Japan remains the one bright spot in the developed world: we see it as the only major developed economy growing above potential in 2024. Consumer spending is strong, while governance reforms across the corporate sector are helping attract foreign capital.

Liquidity conditions continue to diverge across the world, with the US and Europe tightening and Japan witnessing the opposite (for now); China continues to offer modest stimulus.

In the US, higher real rates are proving a drag on loan-making. Also inhibiting the flow of credit is a pick up in the pace of quantitative tightening by the Fed and an increase in issuance of US government securities to cover the country’s significant budget deficit. Net US bond issuance is likely to come to USD300-500bn per quarter for the current quarter and quarters to come, compared to less than USD200bn during the previous quarter. Debt servicing costs will further add to the upward pressure.

Elsewhere, China’s flirtation with deflation could prompt Chinese authorities into taking a more aggressive monetary stance. Meanwhile in Japan, there are signs that a move towards tightening is imminent, though timing is a question.

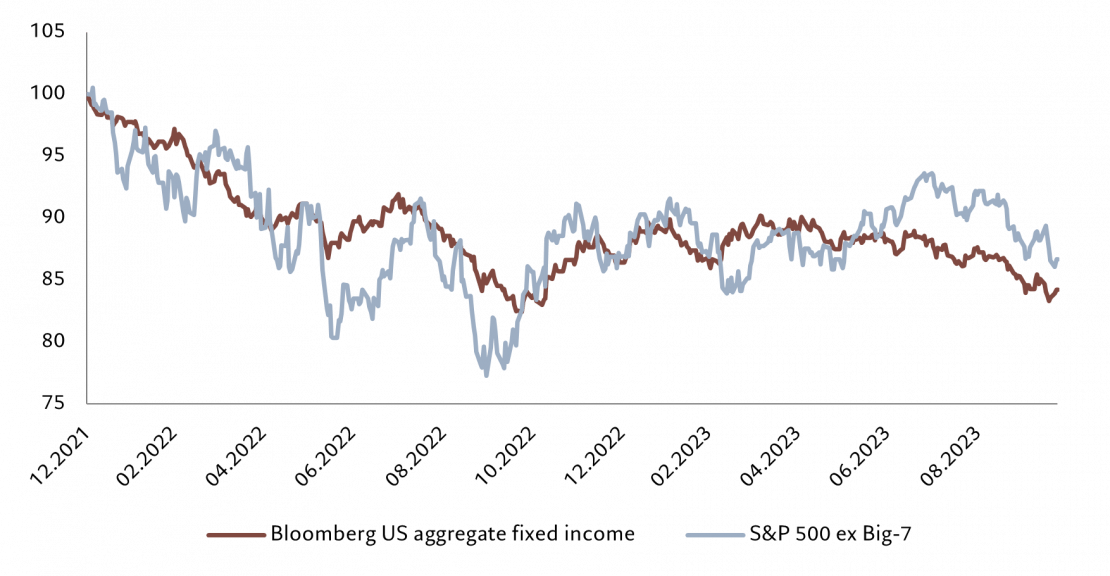

Fig. 2 – Not so nifty

Performance of US equities ex-big 7 stocks vs US aggregate fixed income

*Top 7 by current market cap: AAPL, MSFT, AMZN, GOOG, NVDA, META, TSLA.

Source: Refinitiv, MSCI, IBES, Pictet Asset Management. Data covering period 31.12.2021 to 25.10.2023.

Our valuation metrics clearly favour bonds over equities, not least because of a recent jump in yields. US equity price-earnings (PE) multiples remain above our model estimate. The 12-month price to earnings (PE) ratio for the market is 12 per cent above our secular fair value forecast of 16 times. The ‘Magnificent 7’ tech stocks that had been dominating the equity market’s performance, weakened somewhat, but are still on a rich forward PE of 28 times, which represents an 80 per cent premium to the rest of the market. But the rest of the market has tracked developments in bond yields (see Fig. 2).

Relative to bonds, equities are very expensive in the US. For the first time since 2001, stocks’ 12-month earnings yield is below the Fed funds rate and the gap between the earnings yield and the real bond yield is below 2 per cent. This has only happened four times in the past half-century.

Our technical indicators show weakening trends for equities, led by declining momentum in Japan and a deterioration in the euro zone. Seasonality remains favourable for the market over the next month, however. The bond trend has also deteriorated. Sentiment remains weak, suggesting oversold conditions for eurozone and Chinese equities. Within fixed income, high yield credit and emerging market hard currency bonds also look oversold.

Piece of opinion written by Luca Paolini, Pictet Asset Management’s Chief Strategist.

The SEC has approved Finra’s request to relax controls on home-based work for brokers/dealers. The new regulations approved by the SEC facilitate remote inspection of broker offices and reduce the frequency of required examinations.

This change, originally proposed by Finra, reflects a significant adjustment in the supervision of stockbrokers, moving from annual reviews to once every three years for home offices.

The SEC’s decision follows an extensive period of debate and opposition, particularly from investor advocates, who expressed concerns about the increased flexibility granted to brokers and their employers, as reported by AdvisorHub. The SEC has stated that these new rules are in line with its broader responsibilities to prevent fraud and protect investors.

Finra’s initiative to adapt its inspection procedures to the post-pandemic era has been a focal point since the onset of the COVID-19 pandemic closures.

In 2020, the regulatory body temporarily suspended its in-person inspection requirements, extending this relief measure until the end of this year due to concerns that arose, notably from state regulators and plaintiff attorneys.

The remote inspection plan, proposed as a three-year pilot, received additional comments from the SEC in August. However, despite ongoing opposition, Finra defended its proposal, arguing that advancements in surveillance technology allow for more effective remote monitoring, adds the specialized media. Additionally, restrictions were put in place to prevent high-risk firms and brokers from participating in the pilot program.

In its approval, the SEC emphasized that the pilot would provide firms with greater flexibility, while mitigating risks by implementing specific safeguards. These measures would limit eligibility to certain member firms and locations only.

Finra officials told the SEC that the rule change, allowing less frequent examinations of home offices, aligns these residential spaces with its definition of a “non-branch” location.

The industry has broadly supported these rules, as they allow firms to maintain remote examiners hired during the pandemic, avoiding the need to terminate them if they were required to work in-office.

HANetf, Europe’s independent white-label UCITS ETF and ETC platform, and leading provider of digital asset ETPs, is delighted to announce its partnership with Tidal Financial Group, US-based leading ETF investment and technology platform, to offer ETF white label services to one another’s clients, announce the firm.

Under the agreement, HANetf will extend its suite of services to include Tidal’s extensive client base, allowing them to access the diverse world of UCITS ETFs, ETNs, and ETCs.

Tidal will, in turn, provide HANetf’s clients and network the opportunity to venture into the U.S. market with 40 Act and 33 Act ETFs, setting the stage for a seamless and integrated approach to both markets.

Through this partnership, both companies will be able to offer their clients flexible options to enter both or either of the European and US markets irrespective of their global footprints. This essentially bridges the gap between the European and US ETP markets for Global asset managers looking to launch funds.

This dual approach can help to safeguard asset managers’ intellectual property by launching their IP in both wrappers and markets. It also facilitates access to a broader audience of global investors who may have specific preferences, such as tax considerations and time zones.

The US and European ETF markets are the two largest ETF markets globally, and the collaboration between HANetf and Tidal will enable their clients to tap into both markets without compromise. Both wrappers are also popular in other geographies including Latin America and Asia. Arguably, if asset managers want to deliver their investment strategies to a global audience they will be able to achieve this through issuing UCITS and 40 Act ETFs.

HANetf can launch ETFs quickly, and cost-efficiently, via its company-owned Irish ManCo and ICAV platforms. It also supports SICAV depending on asset manager choice. Beyond ETFs, HANetf can also offer clients the ability to launch ETCs via its ETC platform, and other ETPs on its multi-asset platform. Since its first launch in 2018, HANetf has launched over 45 products and accrued over $2.6 billion assets under management (AUM).

Tidal owns and operates its own trusts, providing a robust platform for asset managers to enter the ETF market, and has partnered with over 54 ETF issuers with more than 118 leading ETFs on the market. It currently has over $9.5 billion in AUM.

Both HANetf and Tidal offer full fund management, regulatory, trade execution and operations services. In addition to infrastructure, both firms are equipped with comprehensive marketing and distribution capabilities, which are often regarded as the most challenging aspects of achieving success in the ETF market.

Hector McNeil, Co-Founder and Co-CEO of HANetf comments: “We are very proud to announce our agreement to work with Tidal in order to offer US ETF white label capability to our clients. Since launching HANetf five years ago, we have had multiple requests from global clients to be able to offer both UCITS and US ETF capability. Working with Tidal matches up the leading US white label provider and Europe’s first and leading white label provider. Clients will be able to either supplement their UCITS ETF offering with 40 Act ETFs or if they haven’t entered the ETF market will be able to offer both wrappers to allow simultaneous launch in both of the World’s leading ETF markets in one fell swoop.”

Mike Venuto, Co-Founder and CIO of Tidal Financial Group comments: “We are excited to expand our relationship with HANetf. Over the past few years, we have participated in the growth of European ETFs as a sub-advisor to HAN clients. With this partnership, we are now able to connect our US based customers with our counterparts in Europe. Recently, ETF Express recognized Tidal as the Best US White Label Platform due to our full service offering. Through this partnership, our clients will be able to repurpose the innovations, ideas and content we produce with them here to also access the European UCITS ETF market.”

ZEDRA, a global specialist in Active Wealth, Corporate & Global Expansion, Fund Solutions and Pensions & Incentives, announces its plan to acquire LJ Fiduciary and Alvarium Private Office (“APO”), with offices in the Isle of Man, Geneva and the UK.

LJ Fiduciary and APO will be rebranded and merged into the existing ZEDRA Group.

LJ Fiduciary’s and APO’s service offering includes global private client and corporate administration services. This latest acquisition will enhance ZEDRA’s strategy in the Active Wealth and corporate services space, reinforcing the ambition to be recognised as an international leader in Active Wealth, Corporate & Global Expansion, Funds Services and Pensions & Incentives.

ZEDRA will welcome 59 employees who have been providing trust, corporate, marine and aviation, and family office administration services through its offices in the Isle of Man, Geneva and London.

This brings ZEDRA’s headcount to over 1,000 experts across 16 countries spanning Asia, Oceania, the Americas and Europe. Both organizations share the same core values of close client relationship management, assisting them with their personal interests, family requirements and business interests.

Their combined capabilities provide clients with access to a more diverse service offering, adding value and deepening client relationships.

Ivo Hemelraad, CEO at ZEDRA, commented: “We are delighted to welcome the team from LJ Fiduciary and APO. The combined extensive experience and knowledge will be a great asset as we look to further grow our footprint and our capabilities.”

The transaction is subject to regulatory approval.