KKR announced the completion of the acquisition of Varsity Brands by KKR from Bain Capital and Charlesbank. As the new majority owner of Varsity Brands, KKR will support the Company as it continues to grow its business.

The Varsity Brands platform offers an extensive range of high-quality, customized solutions, services and experiences that support school and team sports, athletics and spirit programs, reaching over eight million athletes and students annually. The Company is a national marketer, manufacturer and distributor of customized team uniform and apparel solutions and team-specific sporting goods and equipment serving more than 150,000 customers, including colleges, universities, schools, club teams and recreational programs.

Additionally, the Company has strong, long-standing relationships with iconic global athletic brands such as Nike, adidas, Under Armor, New Balance and lululemon. Varsity Brands is also a leading organizer of cheerleading competitions and training camp programs.

“Today is a pivotal moment for Varsity Brands as we welcome KKR as our new investor. We see immense growth potential as we advance our mission to support teams, schools and communities, elevating the experience for young people nationwide. This is a proud day for the Varsity Brands team, whose commitment and performance are critical to our continued success. I am also excited for our colleagues to join KKR and our leadership team as co-owners of the Company,” said Adam Blumenfeld, CEO of Varsity Brands. “We are grateful for the support and partnership from Bain Capital and Charlesbank. Their support has been instrumental in laying the foundation for our continued success. I want to express my sincere gratitude for their belief in our mission and role in shaping the Varsity Brands we know today.”

With a history spanning five decades, Varsity Brands serves as a catalyst for positive change, supporting the physical, mental and emotional well-being of students and athletes through innovative resources and programs that help kids feel connected, supported and inspired to excel.

Most recently, the Company debuted a new initiative, SURGE, which stands for Strength, Unity, Resilience, Growth and Equity, aiming to empower girls to stay in sports. SURGE encourages female athletes to lead healthy, successful lives through a variety of free online tools for coaches to build self-esteem, instill confidence and prioritize mental health. Additionally, the Varsity Brands IMPACT School Partnership Program offers schools tailored solutions to enhance school pride, boost student engagement, and foster community spirit.

“Varsity Brands is a leading solutions-oriented services provider with a mission to elevate the student experience through sport and spirit, helping schools and teams foster greater participation, enthusiasm and community,” said Felix Gernburd, Partner at KKR.

KKR will support Varsity Brands in creating a broad-based equity ownership program to provide all the Company’s employees with the opportunity to participate in the benefits of ownership. This strategy is based on the belief that team member engagement through ownership is a key driver in building stronger companies. Since 2011, more than 50 KKR portfolio companies have awarded billions of dollars of total equity value to over 100,000 non-senior management employees.

KKR is making this investment primarily through its North America Fund XIII. Terms of the transaction were not disclosed.

Goldman Sachs and Jefferies served as financial advisors and Simpson Thacher & Bartlett LLP served as legal advisor to KKR.

BofA Securities and William Blair served as joint financial advisors and Kirkland & Ellis LLP served as legal advisor to Varsity Brands.

TD Bank Group announced that the Bank continues to actively pursue a global resolution of the civil and criminal investigations into its U.S. Bank Secrecy Act (BSA)/anti-money laundering (AML) program by its U.S. prudential regulators, the FinCEN and the U.S. Department of Justice.

In anticipation of a global resolution, which will include monetary and non-monetary penalties, the Bank has taken a further provision of US$2.6 billion in its third quarter financial results to reflect the Bank’s current estimate of the total fines related to these matters. The Bank expects that a global resolution will be finalized by calendar year end.

TD also announced today that it has sold 40,500,000 shares of common stock of The Charles Schwab Corporation (“Schwab”). The share sale will reduce TD’s ownership interest in Schwab from 12.3% to 10.1%. In connection with this sale, TD has agreed not to sell any additional Schwab shares for a period of 45 days, subject to certain exceptions. TD has no current intention to divest additional shares.

After giving effect to this provision, TD’s Common Equity Tier 1 (“CET1”) ratio will be 12.8% as of July 31, 2024. In TD’s fourth fiscal quarter, the provision will have a further negative impact of 35 bps on its CET1 ratio from the increase in operational risk. Also in the fourth fiscal quarter, the Schwab share sale will increase TD’s CET1 ratio by 54 bps.

“We recognize the seriousness of our U.S. AML program deficiencies and the work required to meet our obligations and responsibilities is of paramount importance to me, our senior leaders, and our Boards,” said Bharat Masrani, Group President and Chief Executive Officer,TD Bank Group.

“Our remediation program is well underway. TD has strengthened its U.S. AML program with the addition of globally recognized leaders and talent from across the industry, including experts from regulatory agencies, law enforcement and government. The Bank is also making important investments in data and technology, training, and process design. We are building stronger foundations for our U.S. business, where 30,000 colleagues proudly serve more than 10 million Americans from Maine to Florida,” added Masrani.

“TD continues to work constructively with our regulators and law enforcement towards resolution of our U.S. AML matters and looks forward to bringing additional clarity to our shareholders, clients and other stakeholders,” concluded Masrani.

The SEC announced awards of more than $24 million to two whistleblowers whose information and assistance led to an SEC enforcement action and an action brought by another agency.

The first whistleblower will receive an award of $4 million, while the second whistleblower will receive an award of $20 million. While the first whistleblower reported first, prompting the opening of the investigation, the second whistleblower received the higher award, as their information and substantial cooperation proved critical to the success of the actions.

“Today’s awards highlight the incredible public service provided by whistleblowers,” said Creola Kelly, Chief of the SEC’s Office of the Whistleblower. “The information would have been difficult to obtain in the absence of the whistleblowers as it pertained to conduct occurring abroad.”

Payments to whistleblowers are made out of an investor protection fund, established by Congress, which is financed entirely through monetary sanctions paid to the SEC by securities law violators.

Whistleblowers may be eligible for an award when they voluntarily provide the SEC with original, timely, and credible information that leads to a successful enforcement action. Whistleblower awards can range from 10 to 30 percent of the money collected when the monetary sanctions exceed $1 million.

As set forth in the Dodd-Frank Act, the SEC protects the confidentiality of whistleblowers and does not disclose any information that could reveal a whistleblower’s identity.

Americana Partners welcomes Javier Altimari as Founder and Managing Partner of its international division, Americana Partners International (API).

Altimari will be based in Houston and be part of the API Board, along with Jorge Suárez-Vélez, Founder and CEO. Previously, Altimari was a Senior Director and Portfolio Manager at Oppenheimer & Co.

“As more than US$30 Trillion change hands between generations across the globe, we are going to capitalize on a once in a lifetime opportunity to help the next generation of international ultra-high net worth clients,” said Altimari. “This partnership enables us to develop a solid infrastructure for international investors and assemble an elite team to extend our expertise and service to the market.”

At Americana Partners International, Altimari will advise families and institutions on long-term investment needs, developing investment strategies that respond to clients’ risk profiles and to their long-term goals. He will play a leading role in the management of the firm’s day-to-day business, while seeking opportunities to expand its international footprint.

On June 25, 2024, Americana Partners, an RIA with $7.5 billion in assets under advisement, launched Americana Partners International to provide family office services to international ultra-high-net-worth families and institutions, and appointed Jorge Suárez-Vélez, Founder and CEO. Formerly a Managing Director at Allen Investment Management, the RIA arm of investment bank Allen & Co, Suárez-Vélez has over 20 years of industry experience, and deep expertise in Mexican political and economic issues.

“As API seeks to become the go-to platform for international financial advisors, Javier will be instrumental in our effort,” said Suárez-Vélez. “He brings a wealth of experience having worked with domestic and international investors, giving them access to high value-added financial services, and a broad offering of investment vehicles – all while helping them navigate complex cross-border, multi-generational, and multi-jurisdictional planning.”

Americana Partners is a member of the Dynasty Network, which includes 55 independent firms and over 400 advisors. For more than a decade, Dynasty has championed the benefits of independent wealth management for high net worth and ultra-high net worth clients and has contributed to the movement of assets from traditional brokerage channels to the independent channels of wealth management.

Shirl Penney, Founder and CEO of Dynasty Financial Partners, added: “API is pioneering the approach to serving an increasingly international high-net worth client base and their trusted advisors. I cannot think of a more qualified person to help lead this charge than Javier. Our partnership with Jorge Suárez-Vélez, Javier Altimari, and Americana Partners will help us craft and enhance the platform that many other elite international financial advisors will want to be a part of.”

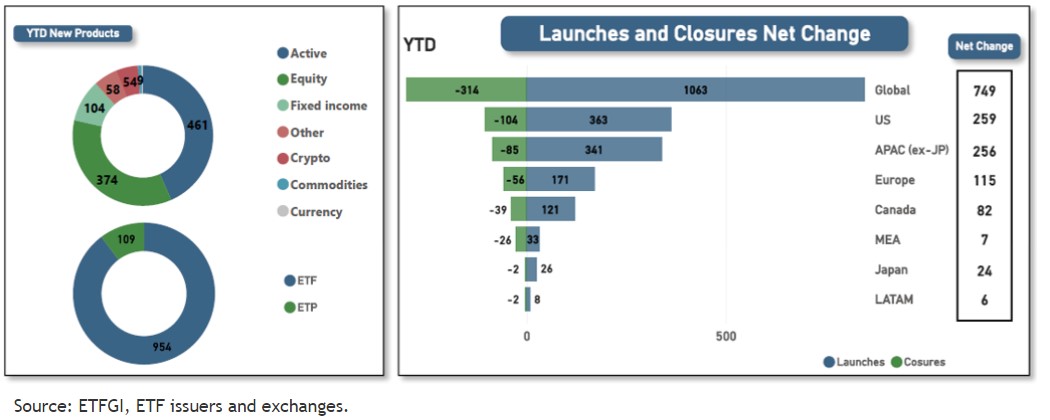

The ETFs industry continues to break records, according to ETFGI, an independent analysis and consulting firm specializing in these vehicles. The latest achievement is a historic high of 1,063 new products listed in the first seven months of the year. This figure surpasses the previous record of 988 new products listed in the first seven months of 2021.

After accounting for 314 closures by the end of July, there has been a net increase of 749 products. This exceeds the previous record of 988 new ETFs listed at this point in 2021.

In terms of distribution of new launches, a total of 363 ETFs were listed in the United States, while 341 were in Asia-Pacific (excluding Japan), and 171 in Europe. The highest number of closures also occurred in the United States (104), followed by Asia-Pacific (excluding Japan) with 85 closed funds, and Europe with 56.

A total of 281 providers contributed to these new launches, spread across 39 exchanges worldwide. There have been 314 closures from 107 providers on 24 exchanges. The new products include 461 active ETFs, 374 equity ETFs, and 104 fixed-income ETFs.

Chart 1: Inflows and closures of new products in the global ETF sector

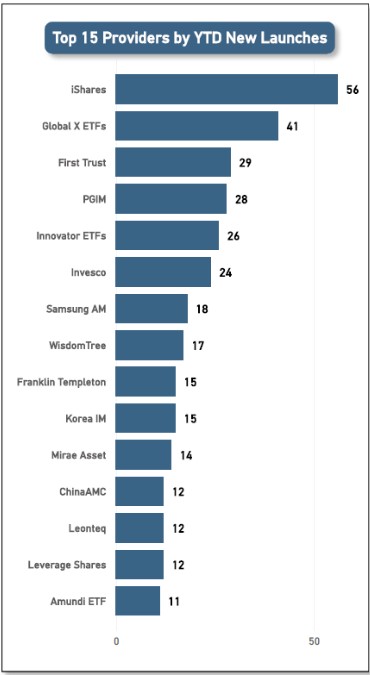

The 1,063 new products are managed by 281 different providers. iShares recorded the highest number of new products with 56, followed by Global X ETFs with 41 new launches, and First Trust with 29. Additionally, these products are managed by 281 different providers. Once again, iShares is the provider with the most new product launches, with 56, followed by Global X ETFs with 41, and First Trust with 29.

Chart 2: The Top 15 Providers of New Launches

Source: ETFGI, ETF issuers and exchanges.

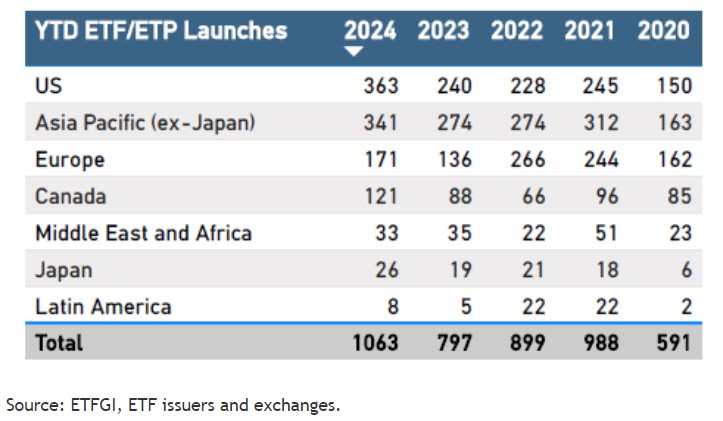

When analyzing the listing activity of new products in the first seven months of the year from 2020 to 2024, ETFGI observes that the global ETF industry has seen a significant increase in the number of new launches, rising from 591 to 1,063.

In 2024, the United States and Asia-Pacific (ex-Japan) recorded the largest launches, with 363 and 341 new products, respectively. Latin America registered the fewest launches: only 8.

The United States, Asia-Pacific (ex-Japan), Canada, and Japan have shown the peak of launches in 2024 with 363, 341, 121, and 26 respectively. Europe reached its highest number of launches in 2022, with 266, while Latin America recorded a total of 22, both in 2022 and 2021. Finally, the Middle East and Africa reached 51 launches in 2021.

Chart 3: New Listings in the First Seven Months of the Year in the Global ETF Industry: 2020 to 2024

The number of product closures by the end of July 2024 decreased in all regions compared to the same period in 2023. This year, the United States and Asia-Pacific (excluding Japan) recorded the highest number of closures, with 104 and 85 respectively. Meanwhile, Japan and Latin America had the lowest number, with only two closures each in these regions.

According to a report by Ortec Finance, wealth managers and financial advisors are influenced by social media activity when discussing valuations and stocks, which sometimes hinders their ability to provide professional advice to clients. This is affirmed by 95% of the respondents in the firm’s survey.

Of these, more than eight in ten (82%) say they are increasingly influenced by this factor, and more than one in ten (13%) are highly influenced. Only 4% say they are not particularly swayed by social media activity around the stock market and equities, and just 1% say they are not influenced at all.

Additionally, 93% of wealth managers and financial advisors believe that social media noise about the stock market and specific stocks makes it harder for them to provide professional advice to clients due to how clients react to this noise or the impact it has on advisors and wealth managers.

“Despite the many benefits that social media brings, our research shows that the noise surrounding it is an obstacle for many financial advisors and wealth managers. With a younger generation increasingly turning to social media as their source of information for everything from politics to DIY, they are also using it as a source of financial advice. However, our research shows that social media is having a negative impact on many financial advisors and wealth managers, as well as hindering their ability to provide solid professional advice to clients,” explains Tessa Kuijl, Managing Director of Global Wealth Solutions at Ortec Finance.

Federal Reserve Chairman Jerome Powell announced this Friday at the Jackson Hole symposium that the time for monetary policy tightening has arrived, but the pace will depend on macroeconomic data.

“The time has come for policy to adjust. The direction of travel is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks,” Powell said according to the speech published by the Fed.

The head of the federal monetary authority reviewed the evolution of the country’s macroeconomic situation since the pandemic and assured that the Fed will do “everything in our power to support a strong labor market while continuing to make progress toward price stability.”

With appropriate moderation in monetary policy, “there are good reasons to believe that the economy will return to 2% inflation,” he said. Powell also emphasized the importance of maintaining the strength of the labor market at the same time.

“The current level of our official interest rate gives us ample room to respond to any risks we may face, including the risk of further unwanted weakening of labor market conditions,” he explained.

At the 2024 annual symposium entitled “Reassessing the Effectiveness and Transmission of Monetary Policy”, the president addressed the presidents of the Fed’s divisions in each state. He provided explanations as to why the measures implemented in recent years, including rate hikes to control rising prices, had been taken.

In this regard, Powell analyzed the behavior of inflation from the peak during the pandemic to the current decline.

The onset of the pandemic quickly led to shutdowns in economies around the world, which meant a time of radical uncertainty and severe downside risks. Additionally, the Fed chairman recalled the government and congressional assistance, such as the passing of the CARES Act.

“At the Fed, we used our powers in unprecedented ways to stabilize the financial system and help prevent an economic depression,” he emphasized.

However, Powell assured that pent-up demand, stimulus policies, pandemic-related changes in work and leisure practices, and additional savings associated with restricted service spending contributed to a historic increase in consumer spending on goods.

“That’s how inflation arrived. After being below target throughout 2020, inflation surged in March and April 2021. The initial inflation burst was concentrated rather than widespread, with extremely large price increases for scarce goods like motor vehicles,” he asserted, later insisting that this situation indicated a transitory inflation regime.

“The Transitory Inflation ship was full, with most analysts and central bankers from advanced economies on board. The common expectation was that supply conditions would improve reasonably quickly, that the rapid recovery in demand would run its course, and that demand would rotate from goods to services, reducing inflation,” he commented.

However, in June 2022, inflation reached its peak of 7.1 percent, forcing the Fed into a rate hike rally throughout 2023 and part of this year.

After this review, Powell concluded by assuring that “the pandemic economy has proven to be unlike any other, and much remains to be learned from this extraordinary period.”

The Securities and Exchange Commission has adopted a rule updating the dollar threshold for a fund to be considered a “qualifying venture capital fund” for purposes of the Investment Company Act of 1940.

The rule updates the dollar threshold to $12 million in aggregate capital contributions and uncalled committed capital, up from the original threshold of $10 million.

Qualifying venture capital funds are excluded from the Act’s definition of an “investment company.” The Economic Growth, Regulatory Relief, and Consumer Protection Act of 2018 requires the Commission to index the dollar amount for this threshold for inflation once every five years.

New rule 3c-7 implements this statutory directive and adjusts the dollar amount to $12 million dollars, based on the Personal Consumption Expenditures Chain-Type Price Index.

The rule also establishes a process for the Commission to make future inflation adjustments to the threshold every five years.

It will be effective 30 days after publication in the Federal Register.

Principal Financial Group announced that Deanna Strable, executive vice president and current chief financial officer, is named president and chief operating officer. Dan Houston will continue to serve as CEO and Chairman of the Board.

“Deanna has been instrumental in driving strategy, financial results, and operations to enable Principal to grow and continue to create value for our customers, shareholders, and employees,” said Houston. “Her appointment as president and COO reflects her extensive experience and proven leadership within the organization, and I am excited to continue our strong partnership.”

In this new role, Strable will have direct responsibility for the three businesses of Principal – Retirement and Income Solutions, Benefits and Protection, and Asset Management. Strable has served as CFO since 2017, after previously serving as president of the company’s workplace benefits and insurance business. She joined Principal in 1990 as an actuarial assistant and has held various actuarial and management roles throughout her career.

“In my nearly 35 years at Principal, I’m more confident than ever in our ability to deliver value and grow sustainably to continue to serve our customers and meet the expectations of our shareholders,” said Strable. “I look forward to the opportunity to further contribute to our ongoing success in this new role.”

As part of this transition, Joel Pitz, senior vice president and controller, will serve as interim chief financial officer. Pitz has been with Principal for nearly three decades, holding senior executive finance roles across the company, including serving as CFO for the international pension and long-term savings business.

His deep expertise in financial management and his comprehensive knowledge of the company’s operations make him well suited to oversee financial functions at Principal during this period.

Managing technological needs remains one of the biggest challenges for advisors, according to the latest Cerulli Edge-The Americas Asset and Wealth Management Edition.

According to the research, the most frequently identified challenges in using technology include compliance restrictions that limit functionality or impose other limitations on advisors’ ability to use technology (73%), followed by a lack of integration between tools/applications (71%), and a lack of time to learn and implement (70%).

Since the COVID-19 pandemic, advisors have significantly increased their use of technology. While adoption has proven to be a boon for practices that have incorporated these types of tools, the industry still has a long way to go, the report notes.

Additionally, there is an opportunity for central offices and fintech companies to strengthen the training and support they offer.

“Many of the challenges advisors identify in using technology are challenges that can be overcome through knowledge-sharing efforts to educate and inform advisors about the potential power of more effectively leveraging the technology tools they already have at their disposal,” says Michael Rose, director.

However, according to the study, only half of the advisors are satisfied with the training and support they receive. More structured advisors, who can better leverage specialized technology and offer more comprehensive services to their clients, represent one of the most important market segments for software providers, brokers, and custodians, who are the primary technology providers for these advisors.

“Given the great importance that advisors place on the technology at their disposal, it is crucial that brokers/dealers, custodians, turnkey asset management providers, and other companies that provide technology platforms to advisors obtain sufficient and ongoing feedback to ensure that the technology stack they offer remains aligned with the evolving needs of the practices they serve,” concludes Rose.