The Miami Industry Hopes for a Quick Resolution of U.S. Election Results

| By Marcelo Soba | 0 Comentarios

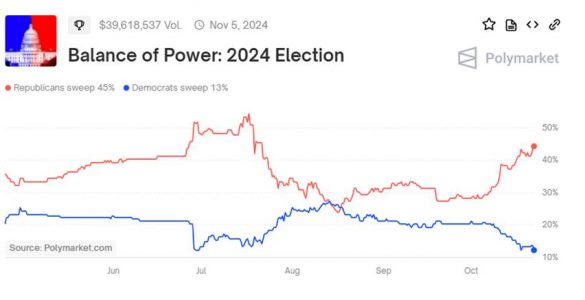

On Tuesday, November 5, U.S. elections will close, and who will lead the White House remains a big question. Although Donald Trump holds a slight edge according to betting markets, what matters most to the financial industry is a swift announcement of results without any dispute.

With this context, Miami’s buy-side representatives are analyzing potential scenarios and how the elections could impact investors.

Ignacio Pakciarz, Founder and CEO of BigSur Partners, expressed that he expects a “Red sweep” where Republicans win both the executive and both houses of Congress.

“We’re basing this primarily on betting markets and a range of financial indicators that consistently point to this outcome,” the expert stated.

According to Pakciarz, the market could experience a minor “relief rally” of 2-3% just from the elimination of electoral uncertainty—so long as there is no “contested election,” which would be the worst scenario. On the other hand, for BigSur’s CEO, “the best outcome would be a divided government.”

Alejandro Behrens, Managing Director at MAXIMAI Investment Partners, commented that he expects a “highly contested election” that will hinge on the swing states.

Behrens warns that “the market will react depending on the clarity and speed with which the results are known.” He agreed that much will also depend on how balanced the government will be, taking into account the Senate and House results.

“Markets usually tend to prefer a more divided government. For me, the best outcome for investments would be one where the winner is known quickly. I think the worst scenario would be one where doubts linger, and it takes several days or even weeks to find out who the new president will be. This would definitely not be positive for the markets and would cause a lot of uncertainty,” he reflected.

Fernando de Frutos, Chief Investment Officer at Boreal Capital Management, outlined three scenarios that could affect the market.

Firstly, who ultimately wins and how anticipated the result was. Secondly, whether the losing party contests the results; and finally, how Congress will be structured.

According to De Frutos, currently, prediction markets show Trump with a slight lead and around a 30% probability of a “Republican sweep.” However, “this advantage has been declining, and polls indicate a very close race,” he clarified.

Given these possible scenarios, for Boreal Capital Management’s CIO, a “Republican sweep” could be positive for stocks in the short term, but might impact bonds, as deficits and tariffs could lead to a rise in interest rates, which in turn could place downward pressure on stocks.

In this regard, De Frutos clarified that “investors generally value all available information, but the impact of fiscal and economic policies often materializes over time and may not immediately influence markets.”

However, the effects of policies related to regulation, tariffs, and taxes tend to be more immediate, the expert explained, noting that the “Trump trade” in 2016 serves as a clear reminder of how markets can react swiftly to policy changes.

Investor Recommendations

It’s well-known that election periods bring volatility and uncertainty for investors. For this reason, financial advisors need to have clear recommendations for their clients.

In this aspect, BigSur Partners “prioritized a healthy rotation toward sectors with good valuation levels.” According to Pakciarz, these sectors would benefit from deregulation that a Trump administration would bring.

Behrens, for his part, worked to help his clients “stay calm and continue with a long-term focus regardless of the election outcome.”

De Frutos, in turn, believes that beyond the “immediate market reaction,” regardless of the electoral outcome, the U.S. will continue to be one of the most attractive markets for investors.

The expert emphasized that for clients with a medium- or long-term investment horizon, “these elections are basically background noise” and noted that historically, stock markets have risen under both Republican and Democratic presidents, and “staying out of the market can be costly in the long run.”

“Since post-election market reactions are notoriously hard to predict, we do not recommend making drastic adjustments based solely on the election results,” he concluded.