From Asset Management to Investment Vehicle Design: The Silent Shift in US Offshore and LATAM

| By Elsa Martin | 0 Comentarios

In the US Offshore and Latin American markets, the conversation among asset managers is evolving. Generating performance remains fundamental, but it is no longer enough. Increasingly, the focus is on how to operate and scale an investment strategy efficiently while maintaining portfolio flexibility and operational consistency.

This shift is a response to an environment marked by higher rate volatility, increased investor sophistication, and a growing demand for investment vehicles that are more accessible and operable on an international level.

Two trends summarize this transition:

- Structural portfolio liquidity

- Operational scalability

Portfolio liquidity and flexibility

Liquidity has ceased to be solely a tactical component of “cash management” and has become a structural design element of the portfolio. Today, managers seek the ability to rebalance, rotate positions, and adjust exposures quickly, even when working with alternative or multi-asset strategies.

The growth of listed vehicles reflects this trend. According to the Investment Company Institute (ICI), US ETFs reached approximately $13.37 trillion in assets by the end of 2025, with nearly 30% year-over-year growth. This progress is driven not only by cost efficiency but also by the operability and flexibility these vehicles offer to managers and distributors.

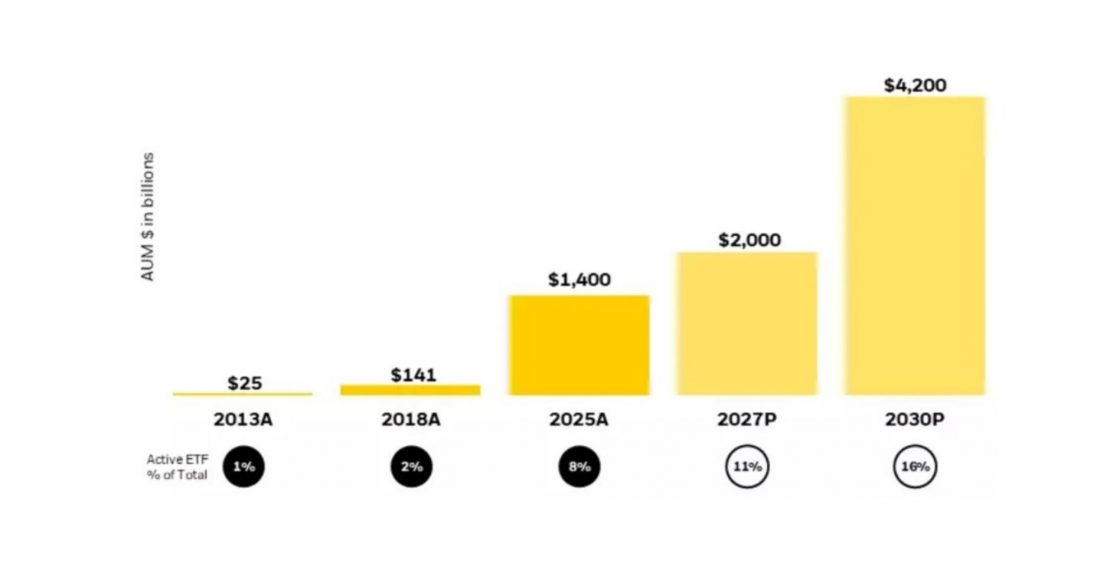

Parallel to this, the active ETF market continues to expand. BlackRock projects that global active ETF assets under management (AUM) will triple, reaching $4.2 trillion by 2030. This growth confirms that managers are utilizing tradable structures not just for passive exposure, but also for active and differentiated strategies.

For asset managers operating between LATAM and US Offshore, this implies a practical reality: the vehicle’s structure can be as important as the investment strategy itself, as it determines the ease with which the portfolio can be adjusted, distributed, and maintained over time.

In this context, solutions like those from FlexFunds allow for the transformation of investment strategies into vehicles designed to facilitate cross-border operations, international distribution, and integration into portfolios managed through global custodians. Rather than creating liquidity on its own, proper structuring improves the strategy’s operability within the offshore ecosystem.

Operational scalability

If liquidity defines portfolio flexibility, operational scalability defines the sustainability of growth.

As a manager increases their investor base or distribution channels, operational frictions arise: repetitive execution per account, misaligned portfolios, increased administrative burden, and difficulty maintaining consistency in performance and reporting.

Structuring strategies into investment vehicles allows for centralized strategy management and standardized distribution. Instead of replicating a strategy across multiple individual accounts, the manager can administer a single vehicle that consolidates execution and keeps investors aligned. This approach reduces operational friction, improves track record consistency, and ensures that AUM growth does not lead to a proportional increase in operational complexity.

This is where solutions like FlexFunds’ function as operational infrastructure for the asset manager, facilitating the transition from a fragmented management model to one centered on the strategy.

A new logic for growth

In today’s environment, liquidity and scalability are no longer independent concepts. The ability to adjust a portfolio, distribute a strategy internationally, and maintain operational efficiency are all part of the same architecture.

For asset managers looking to expand in US Offshore and LATAM, the key question is no longer just what strategy to build, but what structure will allow them to operate and scale it sustainably over time.

If you want to learn how FlexFunds solutions can help you simplify and scale your portfolio management with greater operational efficiency and more agility for tactical decisions, please do not hesitate to contact our experts at info@flexfunds.com