Insigneo, an international firm specialized in wealth management, has welcomed Renato Bisconcini and Renato Rizzatti to its team. Both join as Managing Directors and investment professionals to expand coverage in Brazil. According to the firm, the team comes from BTG Pactual and brings experience in managing sophisticated portfolios for ultra-high-net-worth and high-net-worth clients in Brazil.

Before their time at BTG Pactual, Bisconcini and Rizzatti held key positions at Morgan Stanley, where they built a strong reputation for delivering tailored financial strategies to Brazilian families and institutional investors. Their decision to join Insigneo reinforces the firm’s commitment to attracting top-tier talent and expanding in Latin America.

“We are thrilled to welcome Renato Bisconcini and Renato Rizzatti to the Insigneo family. Their deep knowledge of the Brazilian market and proven track record are invaluable. These two professionals represent the high caliber of advisors we strive to work with, and their addition strengthens our position as the leading platform for international wealth management,” said Alfredo J. Maldonado, Managing Director and Head of Market for the Northeast Region.

By joining Insigneo, the team will leverage the firm’s open architecture platform and technology to offer clients a wide range of global investment solutions tailored to their evolving needs. Their addition to the Insigneo network represents a strategic step, strengthening its wealth management capabilities with top industry talent across Latin America.

“We are excited to join Insigneo. The firm’s entrepreneurial structure, open architecture platform, and tech-driven infrastructure expand what we can offer, more options, greater customization, and a smoother client experience. Insigneo will allow us to move faster, tailor solutions more precisely, and maintain a client-centered approach across market cycles,” said Bisconcini and Rizzatti in a joint statement.

The start of 2026 confirms the resilience of the economic cycle despite geopolitical noise (Greenland, Iran, Venezuela) and political uncertainty (Fed independence, ICE, and a potential shutdown).

Rather than weakening, the baseline scenario is solidifying into a disinflationary expansion, closely resembling the 1995–1999 period. The delayed transmission of the Fed’s three rate cuts in Q4 2025 is beginning to show, just as the fiscal impulse (OBBBA, stimulus checks, tax refunds, and fiscal measures in Japan and Germany) shifts from being a drag to becoming a tailwind for cyclical activity.

Monetary policy: Powell relies on price dynamics

The Fed’s first meeting of 2026 was widely anticipated by markets. Powell delivered a more constructive outlook on growth and the labor market. While his assessment could be read as slightly hawkish, the overall tone was dovish. The focus of his remarks shifted from labor market conditions to price dynamics.

Powell indicated that the recent inflation overshoot is largely due to tariffs, which added up to half a percentage point to the cost of living. Without them, core PCE would already be just above 2%.

The message was clear: the bias is toward future rate cuts, although the bar for action remains high. Current conditions support holding rates steady for now, with markets no longer expecting a cut before June.

Fed succession: risk of a hawkish shift

On Friday, Kevin Warsh was named as Powell’s successor. A former Fed governor (2006–2011), Warsh is known for his critical stance on expansionary monetary policy. He has opposed QE programs beyond the initial post-subprime round, arguing that they distort markets, fuel inflation, and politicize the Fed.

His conservative approach and preference for orthodox monetary policy—emphasizing price discipline, a leaner balance sheet, and limited intervention—have raised concerns among investors. He has even questioned recent decisions such as the 50 basis point cut in September, which he views as politically motivated. His appointment could strain the current balance between growth and financial stability and may strengthen the dollar.

Inflation, productivity, and dollar dynamics

The disinflationary trend continues. Productivity growth is outpacing GDP, easing wage pressures. Oil prices are supportive, and rents are moderating, while the impact of tariffs on the CPI is expected to fade in the coming months.

Despite this favorable macroeconomic backdrop, the recent decline in the dollar, coinciding with a rally in real assets such as gold, silver, and copper, appears to reflect a narrative of eroding monetary credibility rather than underlying fundamentals.

Treasury Secretary Scott Bessent publicly defended a “strong dollar” policy, which helped stabilize the EUR/USD exchange rate after a technical oversold condition. However, the interest rate differential between the United States and the Eurozone suggests that a political risk premium is weighing on the pair, bringing it closer to April 2025 levels.

Earnings and Market Sentiment: Software in the Spotlight

The earnings season for the software sector reveals a technical capitulation. Companies like MSFT, NOW, and SAP have seen significant declines—not due to poor results, but rather their inability to justify previously high valuations. Adding to the pressure are concerns that AI solutions such as Anthropic Cowork could disintermediate major SaaS providers, threatening the traditional per-user licensing model.

The sector is clearly oversold. However, sentiment and technical damage will take time to recover. Key indicators to watch include upcoming data on Net Revenue Retention (NRR), cRPO, and company guidance. The market is looking for signs that renewals and workflow organization continue to hold up, and that AI has not yet had a structurally negative impact. Workday’s earnings on February 25 could be the catalyst to shift this narrative.

Circularity in the AI Ecosystem: Are Funding Rounds Inflated?

Another source of concern comes from the funding side. Reports of a potential $100 billion round for OpenAI, allegedly backed by its own partners (Nvidia, Amazon), have reignited fears over excessive circularity in the AI ecosystem. The perception that capital circulates within a closed loop of beneficiaries undermines the credibility of projected growth models.

AI Investment: Persistence and Barriers

Despite these concerns, AI investment shows no signs of slowing. The focus has shifted toward closed models with access to user data and reasoning capabilities—elements that could create durable barriers to entry.

While the market now demands tangible results, the disruptive potential and monetization opportunities continue to justify capital deployment. In 2026, AI-related CapEx will remain a key driver of corporate growth.

In conclusion, despite volatility and political risks, the macroeconomic backdrop remains constructive. The combination of robust growth, disinflation, and monetary prudence supports risk exposure. However, sector rotation, the evolving AI narrative, and the interpretation of post-Powell monetary policy will be critical to tactical portfolio construction in the first half of 2026. In the short term, there are also technical signals worth monitoring closely.

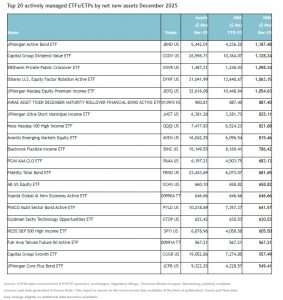

Global assets in actively managed ETFs reached a new all-time high of $1.92 trillion at the end of December, surpassing the previous record of $1.86 trillion set in November 2025. This means that, in 2025, assets grew by 64.5%, rising from $1.17 trillion at the end of 2024 to $1.92 trillion.

According to ETFGI’s analysis of the data, “during December, the global actively managed ETF industry recorded net inflows of $56.23 billion, bringing total net inflows for 2025 to a record $637.47 billion.” This flow activity was driven by globally listed, actively managed equity ETFs, which saw net inflows of $33.31 billion. “This brought total inflows for the year to $361.33 billion, significantly higher than the $211.34 billion accumulated in 2024,” they noted.

Actively managed fixed income ETFs also saw strong demand, with $18.56 billion in inflows in December and $237.93 billion year-to-date, well above the $139.69 billion recorded in 2024.

They note that “the substantial inflows can be attributed to the 20 top active ETFs by new net assets, which collectively gathered $15.89 billion during December.” Specifically, the JPMorgan Active Bond ETF (JBND US) attracted $1.19 billion, marking the largest individual net inflow.

In the past twelve months, Japan has been responsible for some market volatility, something we are not accustomed to. A sign of this has been the recent sharp bond sell-off, which drove yields to record levels and attracted media attention. The combination of a weak yen, the rebound in long-term yields, the fiscal challenges that need to be addressed, and the Bank of Japan’s (BoJ) monetary policy normalization process are part of the elements behind these movements.

To this is added the fact that, over the weekend, the country will hold early elections, which were called earlier this year by Sanae Takaishi, Prime Minister and leader of the Liberal Democratic Party of Japan (LDP).

“This move by Takaishi aims to assert control over her own party and coalition, in order to implement her multi-year reflation strategy. The markets rightly fear that giving her more political capital means more fiscal deficits and inflationary pressures, hence the massive sell-off in the bond market and the jump in stocks. The yen reflects the fear that the Bank of Japan may be hindered by the executive from normalizing real interest rates quickly enough to contain inflationary pressures,” explains Raphael Gallardo, Chief Economist at Carmignac.

For now, the current expansive fiscal policy and uncertainty on the political front highlight the structural obstacles the country is facing, including negative real yields and an already high level of debt.

“The new prime minister wants to take advantage of her very high current popularity rating to win seats for the Liberal Democratic Party and regain control of the Lower House against a Democratic Party for the People, the opposition party, which is unprepared,” adds Martin Schulz, Head of the International Equity Group at Federated Hermes.

Moreover, stocks reacted positively, boosting the “Takaichi Trade,” which includes the aerospace and defense, nuclear, cyber, and domestic exposure sectors.

“Although we have observed some yen depreciation, the restrictions on Chinese exports and the increase in inflationary pressures could negatively affect the confidence of Japanese households and businesses in the short term, so ensuring internal political unity in the long term could help Japan’s negotiating position internationally, especially with the upcoming summit between Japan and the United States. Among the risks we are observing are internal political gridlock and a further unwanted depreciation of the yen,” notes Schulz.

Implication for the Markets

To understand why this weekend’s Japanese election is important, it is necessary to reflect on the role Japan plays in the markets. First, after several decades, it seems to be breaking out of economic stagnation. “Japanese equity valuations have been particularly affected by the persistent reflation scenario. In these environments, the relationship between interest rates and price-to-earnings (P/E) ratios tends to invert. This has caused the P/E ratios of Japanese companies to barely exceed 17 times over the past twenty years, compared to the nearly 20-times average over rolling 10-year periods recorded by U.S. equities,” explains Noriko Chen, Portfolio Manager at Capital Group.

Secondly, it should be remembered that Japan plays a significant role as a “major financier” in recent years through the large carry trade that many have taken advantage of as a technical strategy, and upon which much of today’s leverage has been built.

“By keeping interest rates at zero or even negative levels, the Bank of Japan allowed a large amount of trillions of dollars to flow into risk assets around the world, especially the United States. Today, that cycle appears to be ending with the normalization of monetary policy, which is forcing the unwinding of massive positions,” states Laura Torres, Chief Investment Officer at IMB Capital Quants.

In view of the early elections this weekend, Ray Sharma-Ong, Deputy Global Head of Bespoke Multi-Asset Solutions at Aberdeen Investments, explains that if the Liberal Democratic Party (LDP) were to secure a majority and move forward with its fiscal agenda, several macroeconomic repercussions could be expected in the markets.

“Growth and aggregate demand will increase, driven by considerable fiscal stimulus and targeted investment in strategic sectors such as defense and energy. In addition, inflation expectations and Japanese government bond yields will rise, reflecting the market’s anticipation of a larger fiscal deficit, increased public spending, and greater uncertainty regarding the long-term fiscal path. And finally, the Japanese yen will weaken, as markets price in a weaker fiscal position, a larger fiscal deficit, and the possibility of a slower consolidation of public finances,” argues Sharma-Ong.

Although all eyes are on the record highs gold is setting, the truth is that another precious metal is experiencing a true rally: silver. It posted a spectacular year-end surge that has continued into the early weeks of 2026. In fact, in 2025, the metal appreciated by nearly 150%, clearly outperforming gold.

So far, gold’s current bullish trend has been supported by falling real interest rates, a weaker dollar, and market concern over the implications of rising U.S. public debt levels, the cost of servicing that debt, and the impact on U.S. Treasury bonds. But what factors are driving silver’s performance?

According to Claudio Wewel, currency strategist at J. Safra Sarasin Sustainable AM, the silver market has recorded a structural supply deficit for five consecutive years. “However, this imbalance hadn’t triggered a significant price reaction until 2025, when the uptrend accelerated and took on a virtually parabolic pattern toward the end of the year,” he notes. Wewel attributes this sharp upward movement, which even surpassed the absolute price increases seen ahead of the peaks in 1980 and 2011, to the combination of several factors:

Decline in U.S. interest rate expectations: In the second half of 2025, the market began to focus on the appointment of a successor to Federal Reserve Chair Jerome Powell. “The expectation of a more accommodative Fed, which could implement several rate cuts in 2026, has weakened the U.S. dollar and increased the appeal of non-interest-bearing assets such as silver and gold,” he notes.

Inclusion on the U.S. critical minerals list: In early November 2025, the U.S. Department of the Interior added silver to its list of critical minerals. Thanks to its high electrical conductivity, this material is essential for manufacturing high-performance chips and for the development of infrastructure linked to artificial intelligence. Its inclusion on the list, along with fears of potential U.S. tariffs on silver, alerted the market to potential supply risks and prompted an advance in silver shipments to the U.S. As a result, the London market recorded physical outflows of the metal, reducing local reserves.

Chinese export restrictions: Since the beginning of the year, China has implemented stricter controls on silver exports. This decision is part of a broader strategy to secure access to critical minerals and limits silver exports during 2026 and 2027 exclusively to government-approved companies.

Growing relevance as a store of value: Finally, silver is gaining prominence as a monetary metal. Compared to other commodities, its storage cost is low, and it has a long historical track record as a key material in coinage. The high per-unit cost of physical gold purchases is excluding many low- and middle-income buyers in emerging markets, positioning silver as a more “affordable” alternative to gold in these countries. As a result, household demand has increased in India and China. In Shanghai, buyers are paying a premium of around $10 per ounce over the London market price.

“The sharp surge in the price of silver has brought the gold/silver ratio to around 50. Given that this indicator fell to levels near 40 in previous bullish cycles, silver could significantly surpass $100 per ounce in the current cycle. In principle, our positive view on gold supports this scenario, and speculative positions do not appear excessive,” states Wewel.

However, he warns that although the physical supply deficit should keep silver prices elevated in the short term, the metal tends to experience much deeper corrections than gold after a prolonged rally due to its higher volatility. “Since momentum is losing strength, the risk-return balance now seems less attractive for silver. This also implies that, from these levels, it should be difficult for silver to continue outperforming gold,” he concludes.

Tensions have eased for now, but the controlled disorder on the geopolitical front is here to stay, which also brings a new perspective on the role of certain financial assets. According to some experts, while gold is gaining traction among investors, U.S. Treasury bonds, another classic safe-haven asset, appear to be suffering a noticeable loss of relevance as an investment asset.

The trend analysts observe is that investors are increasingly using gold as a hedge against equity risk, displacing long-term Treasury bonds. “This shift reflects a structural collapse in the traditional relationship between equities and fixed income: since 2022, correlations have remained close to zero, which has eroded the effectiveness of bonds as a diversifier. Historically, duration exposure cushioned declines in risk assets. However, recent episodes, such as the drop after Liberation Day, where equities and long-term bonds were sold simultaneously, have undermined confidence in bonds as a reliable hedge,” notes Lale Akoner, Global Market Analyst at eToro.

Flows show that investors are allocating to equities and gold simultaneously, while reducing exposure to long-term bonds. For Akoner, this trend reflects more than just inflation hedging and a reallocation in portfolio risk management. “If the correlation between bonds and stocks remains unstable, gold’s role as a volatility buffer could solidify, redefining how portfolios hedge downside risk across the cycle,” she explains.

The Loss of the Throne

Since the mid-1990s, bonds issued by the U.S. government have become the world’s most widely used reserve asset, dethroning the one that had reigned until then: gold. As Enguerrand Artaz, strategist at La Financière de l’Échiquier, explains, paradoxically, that crown they held was largely thanks to Europe. “While U.S. debt gradually gained presence in reserve assets, gold’s share quickly declined and European central banks sold their gold reserves to prepare for the advent of the euro. Thus, the yellow metal fell from 60% of global reserves in the early 1980s to 10% in the early 2000s. In parallel, U.S. Treasury bonds rose from 10% to 30%. These levels remained generally stable for two decades. However, the situation has reversed again. In fact, after overtaking the euro in 2024, gold has once again surpassed U.S. debt in global reserves since September 2025,” says Artaz.

In his view, this shift is explained by two underlying dynamics. The first is the gradual erosion of the volume of U.S. debt held by foreign investors since the mid-2010s. And the other ongoing dynamic is the strong increase in gold purchases since 2022 amid greater geopolitical uncertainty driven by the conflict between Russia and Ukraine.

The expert believes there are good reasons for these two dynamics to continue: “The return of geopolitical conflicts and a gradual but powerful trend toward the regionalization of the world favor the use of gold as a reserve asset: gold is not directly dependent on a state and is virtually the only asset capable of absorbing the flows leaving U.S. bonds.”

One data point that helps contextualize this reflection is that the gold and U.S. debt markets are of comparable size, around 25 and 30 trillion dollars, respectively, and far larger than other asset classes. According to the analysis by the LFDE expert, “this phenomenon has accelerated in recent months in parallel with the sharp increase in the price of gold (139% since the end of 2023), but also structurally: the aggressive trade policy of the Trump Administration has heightened the propensity of central banks and investors to abandon the dollar as the preferred safe-haven asset.”

In a final reflection, Artaz points out that doubts about the “health of U.S. public finances” and increased disaffection with U.S. debt could cause the dollar to lose its status as a reserve currency. “There’s only one step left, but it would not be wise to take it. Adding all instruments together, the dollar remains the world’s primary reserve asset and, even if gold dethroned it, it would still be a reference. On the other hand, the U.S. debt market, which is 30% held by investors outside the U.S., could become a geopolitical battleground. That would allow gold to continue to shine,” he concludes.

Outside the Geopolitical Battle

Artaz’s conclusion deserves a few lines: could large holders of U.S. debt end up using their bonds as a “weapon”? For example, it caught the attention of the investment community that last week, two Danish pension funds and one Swedish fund announced they were actively selling U.S. bonds.

Moreover, it’s worth remembering that China, in particular, has reduced its purchases of U.S. bonds by nearly 40% since 2013. This move has been replicated by several central banks in Southeast Asia, increasingly inclined to align with the Chinese yuan rather than the dollar on the monetary front. In contrast, Japan, which remains the largest foreign holder, has maintained the absolute value of its portfolio, but the percentage has dropped sharply, from 10% of total U.S. negotiable debt in 2010 to less than 5% today. Meanwhile, other developed countries have globally maintained their percentages but without increasing them, and only the United Kingdom has effectively increased its investments in U.S. debt.

It is inappropriate to assert that these movements are driven by geopolitical intent, but we can indeed analyze the likelihood of such a scenario. For example, Eiko Sievert, director of public and sovereign sector ratings at Scope Ratings, considers it unlikely for the EU. “The possible sale and rebalancing of reserves into other currencies or assets would be gradual and unlikely to result from a legislative act or moral suasion by EU authorities in response to Trump’s retaliations. Moreover, private investors will be very careful not to harm the value of their portfolios, which could occur if large amounts of U.S. debt were sold in a short period,” he explains.

According to Sievert’s analysis, such a sale of assets would also entail risks to a greater or lesser extent, depending on the pace and scale of the sale. And given the interdependence, unless those selling U.S. debt purchase EU or member state debt, there would be a contagion effect on EU spreads as well. “The implications could be far-reaching, as reduced demand for the U.S. dollar could also lead to a strengthening of the euro, which could weaken economic growth in EU member states focused on exports. In fact, on a global level, a massive sell-off would likely generate volatility, widen spreads, and affect the money market, with possible implications for global liquidity, potentially prompting intervention by monetary authorities,” he concludes, describing a scenario that remains quite distant.

Unlike in previous years, currency markets in 2025 were largely driven by geopolitics, and following a wave of new political developments in the early days of 2026, that trend appears likely to continue. According to experts, this is particularly true for the U.S. dollar.

In fact, the greenback has weakened notably over the past week: the DXY index has fallen by approximately 2%, and the euro/dollar exchange rate is now trading below the firm’s three-month forecast of 1.18. Analysts explain that this has happened despite a solid growth outlook in the U.S. and expectations that the next Fed rate cut won’t arrive until June.

“The recent weakness of the dollar seems to be largely driven by inconsistencies in U.S. foreign and domestic policy, which have undermined investor confidence. As a result, narratives around currency devaluation have resurfaced, pushing the dollar lower even in the absence of macroeconomic catalysts. Although it has weakened, it remains significantly overvalued. That’s why we continue to expect further declines as its interest rate advantage narrows,” says David A. Meier, economist at Julius Baer.

That said, not all analyses place the full weight of the dollar’s decline on geopolitics. In the view of Jack Janasiewicz, portfolio manager at Natixis IM Solutions, the recent drop in the U.S. dollar stems from moves in the Japanese yen, following weekend speculation about potential Fed intervention in the USD/JPY exchange rate. However, beyond these technical factors, he acknowledges that “the tensions over Greenland have weakened confidence in the U.S. dollar, which is why we’re seeing it hit recent lows again.”

A Trend Since 2025

Last year, the dollar’s decline was concentrated mainly in the first half of 2025, following President Trump’s announcement of reciprocal tariffs in April, marking a significant escalation in his global trade war.

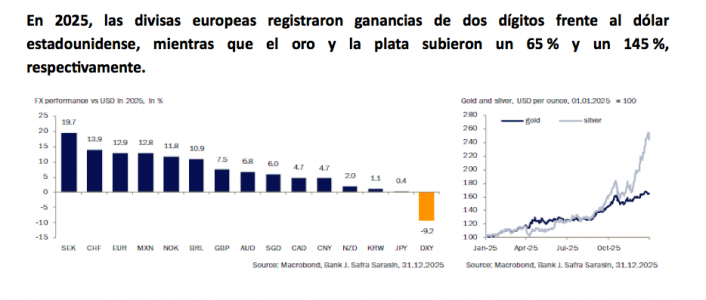

“The dollar’s depreciation largely reflected a sharp rise in currency hedging on expectations of a weaker dollar. European currencies posted double-digit gains as the ‘sell America’ market narrative took hold in the second quarter of 2025, prompting a rotation into European assets. Precious metals were the main beneficiaries of the uncertain political backdrop in 2025, with gold rising 65% and silver surging by a spectacular 145%,” recalls Claudio Wewel, FX strategist at J. Safra Sarasin Sustainable AM.

Looking ahead to this year, Wewel believes that the weight of geopolitics and decisions by the Trump administration will continue to influence the dollar’s performance, and he anticipates a bearish trend for 2026. “The currency remains overvalued by historical standards. We see this argument as particularly relevant in the current political environment. Structural demand for the dollar should decline if the U.S. continues to pursue predatory policies, which would also justify lower fair-value exchange rates compared to the past,” he emphasizes.

He adds another nuance to his outlook: “In 2026, we also expect support for the dollar to weaken from a relative cyclical perspective. Economic growth should converge more between the U.S. and the eurozone, as the European economy benefits from the disbursement of the German fiscal package.”

Threats to Its Status

So far this month, the dollar index (DXY) has dropped approximately 1.5%, reaching its lowest level since September 18. Based on its performance yesterday, in line with this trend, some analysts conclude that the market is rotating positions, rather than turning to the dollar as a safe haven, investors are now seeking other assets. Despite this, experts do not believe the dollar will lose its status as a reserve currency or safe-haven asset.

“The book Smart Money, by Brunello Rosa, argues that the main threat to the dollar comes from China’s global expansion. Through policies such as the Belt and Road Initiative and the development of Beijing’s central bank digital currency (CBDC), China is slowly increasing the use of the renminbi in global trade payments. Control over global supply chains and raw materials goes hand in hand with global monetary hegemony. There is still a long way to go before the dollar’s reserve currency status faces a terminal threat,” says Chris Iggo, chief investment officer (CIO) at AXA IM Core, BNP Paribas Asset Management.

However, Iggo does acknowledge that the growing use of CBDCs, along with a more bipolar global balance of power, poses a threat. “Having influence over a larger share of the world’s oil supply is a counterbalance to these risks, as is maintaining strategic relationships with major oil producers, particularly Saudi Arabia. But there are also risks to the dollar beyond geopolitics: the deterioration of the U.S. fiscal position, potential political interference in monetary policy, and the possibility that global investors will respond to political and economic uncertainty by reducing their dollar allocations in global portfolios. The rise in gold, silver, and platinum prices in dollar terms likely reflects both geopolitical risks and concerns related to U.S. economic policy. For the United States, the biggest threat is that declining confidence in the dollar could increase the cost of financing its twin deficits. Higher Treasury yields would be bad news for an equity market already trading at very high valuations,” he concludes.

Photo courtesyMiguel Ángel Sánchez Lozano, interim global CEO of Santander AM.

In place of Samantha Ricciardi, who will officially leave the firm this Friday, the asset manager has appointed Miguel Ángel Sánchez Lozano as interim global CEO. According to an internal statement, he will take on these responsibilities alongside his current role as head of distribution for the Santander network at Santander Asset Management (SAM).

With this appointment, the firm re-establishes visible leadership following the announcement of Samantha Ricciardi’s departure. The move comes as the bank has just completed the integration of its two asset managers, Santander Asset Management and Santander Private Banking Gestión, creating a single entity with approximately €127 billion in assets under management.

A Homegrown Professional

Sánchez Lozano joined the SAM Group in January 2019 as CEO of Santander Asset Management and Santander Pensiones in Spain. Prior to this, he held various roles within Grupo Santander. Before taking on his role at SAM Spain, he served as head of investment product distribution at Santander Corporate and Investment Banking. In 2013, he joined Grupo Santander as head of treasury product distribution (FX & FI and RSP) at Santander Global Corporate Banking.

Before joining Santander, he was deputy general manager at Banesto, where he was responsible for treasury product distribution. Earlier at Banesto, he also served as head of investment products. Miguel Ángel began his professional career at Banesto in 1996, where he held roles in FX & equity trading and structuring.

He holds a degree in economics from CEU Luis Vives, and two postgraduate qualifications: a General Management Program from IESE and a master’s degree in financial markets from CEU. He has also completed the Advanced Specialization Program in Options and Financial Futures from the Options and Futures Institute and a behavioral finance program from the Chicago Booth School of Economics.

The 2026 edition of the Davos Forum closed with images, speeches, and agreements that help shape the new global order in which investors and asset managers will have to navigate. “This is a time of uncertainty, but also of possibility; it is not a time to pull back, but to lean in. The World Economic Forum is not about reacting to the moment. It is about creating the right conditions for us to move forward,” stated Børge Brende, President and CEO of the World Economic Forum, at the closing of the event.

In this context, and during his speech, Larry Fink, Interim Co-Chair of the World Economic Forum and CEO of BlackRock, argued that economic progress must be shared. “We believe prosperity needs to go further than it has gone, and we believe institutions like the World Economic Forum remain important to make that happen,” he stated.

Indeed, the theme of this edition, which emphasized dialogue, appeared to have tempered the tone of U.S. President Donald Trump. “He claimed to have held constructive talks on Greenland with the NATO Secretary General and canceled the planned tariff hikes set for February 1. At the same time, a meeting between the United States, Ukraine, and Russia was scheduled to address peace in Ukraine, a signal of geopolitical de-escalation that helped risk assets rebound. Gold pulled back but approached the $5,000 mark again this week,” summarized Edmond de Rothschild Asset Management.

Beyond the speeches and broader goals of Davos, markets experienced a week marked by geopolitical noise and volatility, yet equity indexes barely corrected as corporate earnings continued to support valuations. In response to these risks and uncertainty, investors moved toward safe-haven assets, particularly gold. But what are the key messages from Davos that truly matter for the industry?

Fragmentation, Risk, and Geopolitics

According to investment firms, a context of growing fragmentation and geoeconomic conflict has become increasingly evident, seen in trade, sanctions, and supply chains. In this sense, the Davos agreement on Greenland is a clear example of this fracture.

“Investors continue to seek protection for their portfolios, as tensions in global alliances and unresolved risks keep uncertainty levels high. With central banks increasing their gold purchases over the past year and a macroeconomic environment that continues to support accumulation of the asset, we foresee further price gains,” stated Mark Haefele, Chief Investment Officer at UBS Global Wealth Management.

For Thomas Mucha, Geopolitical Strategist at Wellington Management, geopolitical cycles tend to be long, historically lasting between 80 and 100 years. “Structural changes like the ones we are witnessing occur only once per century and tend to be disruptive. Therefore, while market risk is structurally higher in this new regime, 2026 will still offer ongoing opportunities to identify winners and losers within portfolios,” he noted.

Given the high probability that this shift toward national security will persist for years, Mucha believes 2026 could be a good moment to increase exposure to long-term investment themes across both public and private markets. “These themes include: defense and military tech innovation (e.g., artificial intelligence, space and aerospace technologies); critical minerals and rare earths; biotechnology; cyber defense; and renewable energy and climate resilience strategies. This dynamic plays out regionally, nationally, by sector, and at the company level, as well as across all asset classes. It naturally favors active management, as it allows for more agile risk mitigation and differentiation than a passive approach. Opportunities for alpha could emerge through long/short and other alternative strategies. In any case, prudent investors should incorporate geopolitical perspective into their portfolio strategy for 2026 and beyond,” the expert emphasized.

Focus on AI

Another major theme was artificial intelligence, which was present in most of the leaders’ discussions. In Davos, a repeated idea was that the core challenges are trust, governance, and alignment, while warnings were issued regarding job displacement and uneven distribution of productivity gains. The narrative is shifting from “adopt AI” to “prove value and control.”

For asset managers, approaching opportunities in AI goes beyond the spotlight on the Magnificent Seven. “The expansion of AI infrastructure, increased defense spending, and strong demand in the aerospace industry are creating structural tailwinds for the sector. On top of that, greater AI adoption in industrial processes is already showing improvements in productivity and operational efficiency. Looking ahead to 2026, a more favorable macroeconomic environment could boost cyclical segments of the sector and broaden opportunities beyond the large tech firms,” stated Principal Asset Management.

Echoing Davos sentiments, AI-related infrastructure is considered a solid opportunity for investors. “The growing infrastructure needs associated with AI, particularly the construction of data centers, are creating investment opportunities beyond the tech sector. Industrial companies in construction and engineering, electrical equipment, and construction machinery (making up roughly 22% of the sector) supply key components for data centers, from electrical design to cooling systems and battery storage. Some estimates suggest global investment in data centers could reach $7 trillion by 2030 to meet rising energy demands, largely driven by AI workloads,” noted Principal AM.

Sustainable Innovation

As concluded at the Davos Forum, AI and emerging technologies are fundamentally transforming all industrial sectors and the global labor market, driving profound changes in skill requirements and entire professions across both advanced and emerging economies. “When a proven technology like AI merges with emerging fields such as quantum computing or synthetic biology, ideas move from lab to market faster, shaping how industries grow and unlocking new ways to improve the world around us,” they noted. “I would advocate for developing countries: build your infrastructure, engage with AI, and recognize that AI is likely to close the technology gap,” said Jensen Huang, founder, president, and CEO of Nvidia.

The Forum advocated for the responsible and equitable use of technologies like AI, stressing the need to balance their potential with associated risks. Industry leaders encouraged peers to draw lessons from history to guide the deployment of AI. To meet future energy needs, it was emphasized that technology must scale, grids must be modernized, and access to innovation must expand. A new report on clean fuels suggests that global investment in clean fuels could rise from around $25 billion today to over $100 billion annually by 2030, driven by new demand and government ambitions.

New corporate move in the industry. Janus Henderson has signed a definitive agreement to acquire 100% of Richard Bernstein Advisors (RBA), a research-driven multi-asset macro investment manager. According to the firm, the acquisition positions Janus Henderson as a leading provider of model portfolios and separately managed accounts (SMAs). The transaction is expected to close in the second quarter of 2026.

Founded in 2009 by Richard Bernstein and headquartered in New York City, RBA is an asset manager focused on longer-term investment strategies that combine top-down macroeconomic analysis with portfolio construction based on quantitative models, and oversees approximately 20 billion dollars in client assets.

“Widely recognized as an expert and thought leader in style investing and asset allocation, Richard Bernstein has over 40 years of experience on Wall Street, including as Chief Investment Strategist at Merrill Lynch & Co.,” the firm states.

RBA offers its clients differentiated asset allocation solutions supported by the firm’s intellectual capital.

As part of the transaction, Richard Bernstein will join Janus Henderson as Global Head of Macro & Customized Investing, and will sign a multi-year agreement with the Company to lead the next phase of growth for RBA.

Key points of the deal

This acquisition will allow Janus Henderson to significantly strengthen its position in model portfolios and SMAs. Upon completion of the transaction, Janus Henderson will be among the top 10 model portfolio providers in North America, placing it at the forefront of a segment with strong growth prospects. In addition, RBA’s broad experience in distributing model portfolios and SMAs will allow Janus Henderson to enhance its distribution capabilities, including those targeting wirehouses and Registered Investment Advisors (RIAs).

“As demand for model portfolios and SMAs continues to accelerate across the industry, we are very pleased to announce this strategic acquisition of RBA, which will allow us to expand our investment capabilities for our clients, enhancing our current offerings in model portfolios and SMAs. Richard and his investment team are recognized for their research expertise, proven investment strategies, and innovative top-down macro approach. We believe that the investment and distribution capabilities of both RBA and Janus Henderson are a winning combination and position Janus Henderson for long-term success and market leadership in model portfolios and SMAs,” said Ali Dibadj, CEO of Janus Henderson.

For his part, Richard Bernstein, CEO and CIO of Richard Bernstein Advisors, added: “We are thrilled to join Janus Henderson in this new stage of RBA’s evolution. Our shared approach, deeply rooted in research, the mindset of putting the client first, our strength in active ETFs and product innovation, as well as our distribution capabilities, will allow us to develop customized models and expand our reach among clients. We will remain committed to offering our clients our industry-leading intellectual capital and market perspectives. Our macro investment approach will complement Janus Henderson’s bottom-up fundamental investment strategies, expanding our combined capabilities for the benefit of our clients.”

iMGP sells its stake to Janus Henderson

In parallel with this transaction, iM Global Partner (iMGP) has announced that it will sell its stake in Richard Bernstein Advisors (RBA) to Janus Henderson, as part of the acquisition of 100% of RBA. Following this announcement, Philippe Couvrecelle, Founder and CEO of iM Global Partner, stated: “Our mission has always been clear: to identify top boutique managers, partner with them to grow, and offer high-quality investment solutions to clients around the world. The acquisition of RBA by Janus Henderson is a very positive outcome for the firm and for clients, and a clear proof of our strength in identifying leading investment boutiques, as well as the value our partnership platform can create for our asset manager partners.”

Couvrecelle emphasized that iM Global Partner is a growing company. “We already have ambitious plans to accelerate our long-term expansion, and this transaction provides additional momentum to capitalize on our expertise in partner selection, forge new relationships, and further advance our growth strategy in Europe, the United States, and Asia,” he added.

For his part, Richard Bernstein, CEO and CIO of the firm, noted that iM Global Partner has been an excellent and highly supportive partner for RBA over the past five years. “Everyone at RBA is deeply grateful for iMGP’s help in driving our growth, and we wish them the greatest success in their future projects,” he said.