The S&P 500 and the Nasdaq, Heavily Weighted in Tech, Reached New All-Time Highs a Week Ago, Driven by Positive News on U.S.–China Trade Talks That Boosted Investor Sentiment. UBS Global Wealth Management expects that, with companies reporting strong third-quarter results in a favorable environment, U.S. equities will continue to rise in the coming months.

In fact, they point out that the three key factors driving market performance—earnings, monetary policy, and investment—are currently favorable: “The Fed’s easing policy points to a supportive macroeconomic environment. The strong start to third-quarter earnings suggests solid profit growth. The strong demand for computing resources should support robust investment in artificial intelligence (AI),” they state. As a result, Mark Haefele, Chief Investment Officer at UBS Global Wealth Management, acknowledges that they maintain their “attractive” view on U.S. equities and expect the S&P 500 to reach 7,300 points by June 2026.

Could We Be Facing a Year-End Stock Market Rally? For Chris Iggo, Chief Investment Officer at AXA IM, “markets have continued to behave very benignly so far in October,” and he believes that “the earnings season will be strong enough to support the belief that current valuations are sustainable, which could allow for a potential market rally in November, a month that is usually strong for the S&P 500.” Looking ahead to the coming weeks, he highlights that “the market is strongly anticipating a Fed rate cut on October 29, followed by another before the year-end holidays,” in a context where “inflation fears have subsided.”

Room for Active Management

This market behavior reignites the long-standing debate over whether the U.S. large-cap market is too efficient for active managers to outperform. As concluded by Schroders in its latest report, many critics of active fund management use the zero-sum game argument to claim that it is mathematically impossible for active fund managers to outperform passive ones net of fees, which is “categorically false.”

“The increase in the number of investors and the value of investments not allocated according to overall market weightings means we can be more optimistic about the future of active management than we were about the past. It doesn’t mean the average fund manager will outperform, but it does mean it should not automatically be assumed that they can’t or won’t. Now is the time to reconsider your beliefs about active and passive management, even in markets you thought were efficient,” argue Duncan Lamont, Head of Strategic Research, and Jon Exley, Head of Specialized Solutions at Schroders.

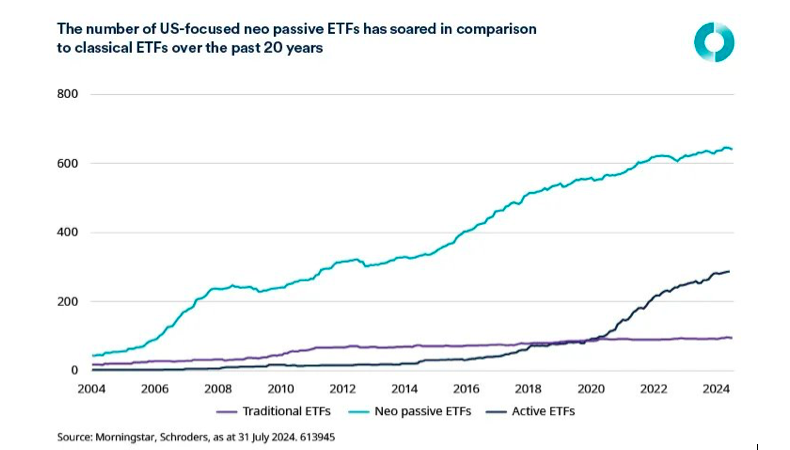

The firm defends in its report that there may be greater opportunities for active managers to outperform in the future than in the past. In fact, it challenges the old formulation of the “zero-sum game” argument and adds that the classic view of the market as divided between active and passive investors should now include a new category: the “neo-passive.”

As Lamont and Exley explain, what has changed recently is the rise of investors who fall into this “active investor” category but are not active equity fund managers. “That’s why we believe we can have more confidence in the future prospects of active fund managers. First, there has been a proliferation of ETFs in recent years that do not follow the broad market. We call these ‘neo-passive.’ In the U.S. alone, there are now more than six times as many of these ETFs as traditional ETFs, and inflows into these strategies have been 50% higher than those into traditional ETFs from early 2018 to the end of July 2024,” they argue.

The Return of Private Stock Pickers

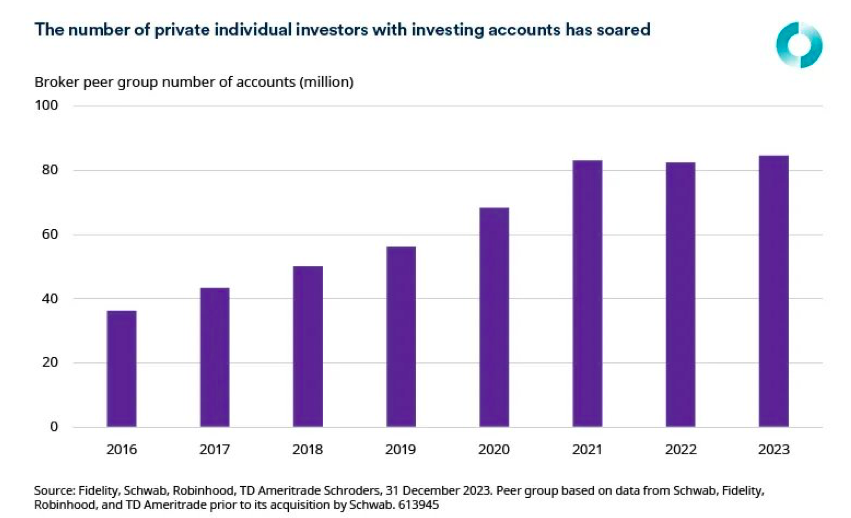

For the asset manager, another shift is the rise of the retail investor. “Accelerated by the move to commission-free trading at several major U.S. brokers, individual investor participation in the stock market has increased. This trend accelerated during COVID, when many people found themselves with more time and money on their hands. The GameStop saga brought trading and investing discussions to the table in many households. In 2023, the number of people with trading accounts at one of the four major brokers was more than double that of 2016,” explain Lamont and Exley.

They Also Acknowledge That While the Number of Monthly Active Users on Major Brokerage Apps Has Declined From Its Pandemic Peak, It Remains More Than 60% Above 2018 Levels. Unlike many other post-pandemic trends, Americans’ interest in investing has endured.

“Of course, many of these individuals may be buying S&P 500 ETFs, but the evidence suggests otherwise. Data from the Federal Reserve’s Survey of Consumer Finances shows that direct stock holdings as a proportion of total financial assets have increased to levels not seen since the peak of the dot-com bubble. This figure includes only directly owned stocks and excludes mutual funds or ETFs,” Lamont and Exley add.

Other Issues: Transactions Lastly, the authors of the report point out that the other side of the zero-sum game argument that does not hold up in the “real world” is the idea that any investor can truly be “passive” in the sense defined by William Sharpe. In their view, it is simply not possible to earn market returns by allocating money according to the weightings of each stock in a benchmark index, then going to sleep and letting the market do the rest.

“What about initial public offerings? Or promotions or demotions from one market segment to another, such as large-cap versus small-cap? Or other changes, such as MSCI’s decision a few years ago to increase the proportion of Chinese ‘A-shares’ included in its major benchmark indices?” they point out.

Their opinion is that all these types of transactions create opportunities for wealth transfer from passive to active investors. “Active investors can trade ahead of index changes and then sell to passive investors when they become forced buyers. Index rebalancing leads to increased trading volumes and price variability in the affected stocks—something that is popular for certain active strategies to target. Active investors can also participate in IPOs, where passive ones generally do not, being forced to buy in the secondary market. All trades incur costs,” they conclude.

Three major central banks held their October meetings, highlighting the divergence in their monetary policy approaches. David Kohl, Chief Economist at Julius Baer, succinctly summarizes the situation: “The Federal Reserve maintains a restrictive policy stance but is expected to ease due to signs of labor market weakness; the ECB sees limited need to act, as inflation is within target and growth risks are not particularly severe; and the Bank of Japan continues its accommodative policy, despite inflation being above target.”

A similar view is offered by Salvatore Bruno, Deputy CIO and Head of Active Management at Generali AM (part of Generali Investments). He focuses on the risk of the Federal Reserve losing its independence: the fiscal expansion promised by the Trump Administration requires low interest rates to limit the cost of debt interest payments, which already exceed 10% of fiscal revenues. This has created strong pressure on the Fed from the administration to resume the rate-cutting cycle. “It won’t be easy to resolve the conflict between the White House and the Fed before the expected change of the central bank’s chair in mid-2026. Nonetheless, there seems to be room for further rate cuts, though possibly fewer than the market expects,” the expert notes.

Regarding the ECB, Bruno sees a different scenario. The market does not anticipate further cuts, as inflation is expected to stabilize and growth prospects appear to have improved. He explains that investors will need to evaluate planned fiscal expansion — especially in Germany — and the potential spillover effects of French political tensions on local interest rates.

A Cinematic Take on Monetary Policy

José Manuel Marín Cebrián, economist and founder of Fortuna SFP, analyzes the current divergence among central banks through a cinematic lens, drawing on the film The Good, the Bad and the Ugly, starring Clint Eastwood.

In his view, the “good” is the ECB and its “monetary siesta”: Christine Lagarde, like a sheriff who has already cleaned up the town, has decided to let the dust settle. With CPI at 2.2%, she feels the job is done. No more cuts, no bailouts, no surprises. Rates stay where they are, and the message is clear: “We’ve done enough — now let others manage.” Meanwhile, the euro fans itself in the sun, the Frankfurt hawks toast with Riesling, and investors breathe easy (for now). The ECB appears disciplined, calm, and with a cool trigger finger. But like any desert hero, it could discover that danger also lurks in calm… especially if European growth gets stuck halfway between the desert and the saloon.

The role of the “ugly” goes to the Fed and its “dance with Trump”: Jerome Powell faces a tougher role. In his personal duel, he battles three foes — inflation, the labor market, and Donald Trump. Inflation has settled at 3%, employment is starting to show signs of weakness, and political pressure from Mar-a-Lago echoes even in the Fed’s hallways. The result is a script full of dilemmas. Powell promises two rate cuts for 2025 and four or five for 2026, trying to please everyone. But markets already suspect this dovish feeling could end in tragedy if inflation returns to the dance. Powell, sweating under his hat, keeps calm as he counts his rounds: each cut must be precise, or the dollar sheriff may lose control of the town.

Finally, Marín Cebrián casts the “bad” as the Bank of Japan and its “rusty revolver”: the eternal misunderstood villain. After decades of firing negative rates, it now seems ready for the unthinkable — raising them. The yen, once feared by none, is now moving like a runaway outlaw, and markets wonder if the BoJ will finally deliver justice to its inflation. The dilemma is classic: raise rates too fast and kill growth; don’t raise them, and the yen bleeds. The result is a Kurosawa-style script, with Zen economics, meticulous decisions, and a lead character who only fires after meditating for three days straight.

Marín Cebrián describes the final showdown in monetary terms: the good (ECB), the ugly (Fed), and the bad (BoJ) stand at the crossroads of the global economy. Lagarde watches calmly, Powell tries to keep his composure, and Ueda sharpens his monetary katana. “As always, the markets place their bets and wait for the first shot. Because in the global economy, the winner isn’t the fastest… but the one who holds their ground,” the expert concludes.

Federal Reserve

Following the latest rate cut in October, responses from financial firms have continued. Guilhem Savry, Head of Macro and Dynamic Allocation Strategy at Edmond de Rothschild Private Banking, sees long-term U.S. interest rates likely remaining higher than previously forecast. However, the end of quantitative tightening, he says, is a reason to support short-term bonds, while the Fed is likely to resume purchasing Treasury bills.

He notes significant disagreement within the FOMC, with some members citing the lack of official data as a compelling reason to avoid another rate cut in December. This divergence and the uncertainty around the Fed’s next chair “could complicate further rate cuts in the coming months,” though the expert still believes a December cut is likely, which should continue to support equity markets and U.S. government debt.

European Central Bank

Konstantin Veit, portfolio manager at Pimco, believes that after the ECB’s decision to hold rates steady, there is little justification for further monetary adjustments. He considers the 2% interest rate “a level likely seen as the midpoint of a neutral range by most Governing Council members.” He adds that Pimco tends to agree with the prevailing view within the ECB that medium-term inflation risks remain broadly balanced. Given the ECB’s reaction function is not geared toward fine-tuning, he still expects “a prolonged period of interest rate inaction.”

Sandra Rhouma, Vice President and European Economist on the Fixed Income team at AllianceBernstein, still anticipates a cut in December, but given the ECB’s latest stance and recent data, “the bar is now higher than it was a few months ago.”

Bank of Japan

The Bank of Japan also held rates steady, offering no surprises, according to Sree Kochugovindan, Senior Research Economist at Aberdeen Investments. The expert notes the overall tone of the press conference was dovish: spring wage negotiations remain the cornerstone of monetary policy direction, and Governor Kazuo Ueda expressed concern that sectors affected by tariffs — such as manufacturing — may struggle to raise wages.

Amid doubts over its independence, Ueda made clear that the BoJ will act in line with its mandate, not under political pressure. Even Prime Minister Takaichi reiterated the Bank of Japan Act, which legally enshrines the institution’s independence.

Kochugovindan maintains his view that the bank will wait at least until January to raise rates by 25 basis points, to 0.75%. “Beyond that, we see a very gradual pace of hikes, as the Bank of Japan will wait for domestically driven core inflation to accelerate,” he concludes.

Photo courtesyPilar Gómez-Bravo, Co-CIO of Fixed Income at MFS Investment Management

The market is experiencing a moment of effervescence: this year there have been multiple headlines about cryptoassets, capital expenditures (capex) related to artificial intelligence (AI), and the opportunities offered by private asset markets. But are any of these vectors currently in bubble territory?

Pilar Gómez-Bravo, co-CIO of fixed income at MFS Investment Management, has decades of experience that allow her to identify where cracks in the system may be appearing—ones investors should keep an eye on. During a recent presentation in Madrid, she emphasized that there is currently no red alert, though she encouraged investors to “make a list of the things that bother us and that we don’t fully understand,” stressing the importance of expectations versus the actual reach of these three market vectors, especially in regard to AI.

Gómez-Bravo offered several keys for identifying bubbles. First, she pointed out the importance of determining whether it is a productive bubble—one that leaves usable assets behind after it bursts—or not. She gave the example of the dot-com bubble, which left behind infrastructure like fiber optic cables that continued to be used for years. In contrast, with assets like gold or cryptocurrencies, price collapses leave behind few if any reusable elements. Therefore, another essential point in analyzing a bubble is evaluating whether there will be winners after it bursts.

How to Assess AI From a Fixed Income Investor’s Perspective

The key to understanding whether there is a bubble around AI—and whether it might burst soon—Gómez-Bravo explained, lies in the ability of companies directly linked to this trend to monetize their capex investments. In her view, current multiples have not yet reached the levels seen during the dot-com bubble.

According to her estimates, it would take $1 trillion in profits to justify current investment levels. Additionally, many MFS clients expect to see signs of monetization in the next 18 to 24 months.

“The U.S. consumer doesn’t want to pay for LLMs (large language models), and token prices are falling. That’s why the strategy is for companies to pay for their use,” she explained. However, profitability would come more from reducing labor costs—through layoffs or lower hiring—than from a direct increase in revenue.

She also warned of the social risks of AI, especially due to the high energy consumption of data centers, which raises electricity costs and impacts inflation. “There is a risk of a populist backlash, as the heavy electricity use by these centers affects the utility bills of nearby residents and could spark protests against the construction of new facilities.”

The Role of Private Markets in Financing AI

For Gómez-Bravo, the concern is not so much about high valuations or increased investment in AI-related infrastructure, but rather the emergence of a closed ecosystem in which the Magnificent Seven finance operations among themselves. As an example, she noted that OpenAI, still unlisted, has announced $500 billion in capex despite remaining in the red.

“AI growth is largely being financed with private debt,” she explained, noting that only half of AI investment is funded by cash flows. Currently, AI accounts for more than 14% of investment-grade (IG) debt.

The expert’s warning is clear: the bubble could take on a systemic character if the traditional financial system starts participating. “When banks begin financing private debt operations, the risk will increase.” She mentioned examples like J.P. Morgan and UBS, both of which have exposure to failed private deals such as First Brands, which recently defaulted.

“It will be crucial to monitor the correlation between bank balance sheets and the private market,” she emphasized, pointing especially to U.S. regional banks. “Private markets are neither good nor bad, but they involve systemic risks, lack regulation, and are not always transparent.”

She also flagged the rise in venture capital funding rounds conducted off-balance sheet—a sign of fragility that may take time to surface. She further warned about a new accounting issue: data centers are amortized over six years, while the chips that power them only have a two-year lifespan.

Cryptocurrencies and Stablecoins

Although she clarified that she is not a specialist on the subject, Gómez-Bravo shared reflections on the rise of cryptocurrencies, particularly stablecoins (digital currencies backed by dollars), whose access to retail investors has expanded following recent regulations.

The growth of stablecoins, she noted, implies captive demand for Treasuries, and the U.S. government has shown its intent to support this trend through new debt issuance. The only obstacle, she warned, could be the independence of the Fed, as its high-rate policy puts pressure on the short end of the curve—just as the U.S. Treasury increasingly relies on short-term issuance.

“For now, the Fed’s policy is not a problem, but in the future the rise of stablecoins could become a threat to Treasuries, which act as the collateral of the global financial system,” Gómez-Bravo concluded.

At Its October Meeting, the U.S. Federal Reserve (Fed) Cut Rates by 25 Basis Points, as Expected, Setting the Target Range for Federal Funds at 3.75%-4.0%. For experts, the most relevant point was that the statement accompanying this decision reiterated concern about the labor market’s development, noting that “the risks to employment have increased in recent months,” while maintaining more moderate language regarding inflation, describing it only as “slightly elevated.”

Powell has emphasized data dependence in 12 unique speeches in 2025. For Alexandra Wilson-Elizondo, global co-CIO of Multi-Asset Solutions at Goldman Sachs Asset Management, the conclusion of this meeting is clear: policy has been set on “autopilot,” following the trajectory outlined by the dot plot, unless new reliable data changes the outlook.

“A single moderate inflation release, well-anchored expectations, and anecdotal signs of cooling support a cautious stance toward rate cuts. If conditions hold, another 25 basis point cut is likely at the December meeting,” says Wilson-Elizondo.

In the view of Jean Boivin, Head of the BlackRock Investment Institute, the Fed reaffirmed that the softening of the labor market remains a key factor. “We see a weaker labor market as helping to reduce inflation and allowing the Fed to lower interest rates. U.S. private sector indicators and state-level unemployment claims point to greater moderation in the labor market, although without a sharp deterioration that would raise concerns about a more pronounced slowdown. We are monitoring alternative data sources while we await the end of the government shutdown to analyze the September and October data for confirmation,” notes Boivin.

Upcoming Cuts

With this cut, justified by economic conditions, the Fed underlined its independence from political pressures. And despite having restarted the rate-cutting cycle, Powell was cautious during his remarks at the press conference following the meeting, stating that a rate cut in December is “far from a foregone conclusion,” which rattled markets that had already fully priced in a new cut.

“At the same time, the Fed acknowledged that the current government shutdown has limited access to economic data. This lack of visibility led the Fed to refrain from offering clear guidance on whether another cut will occur at the December 2025 meeting. Powell’s statements suggest that the Fed assumes the shutdown could extend through December 2025. Once the shutdown ends and macroeconomic data becomes available, we expect it to support a rate cut in December 2025,” adds Ray Sharma-Ong, Deputy Global Head of Multi-Asset Bespoke Solutions at Aberdeen Investments.

Tiffany Wilding, economist at PIMCO, interprets Powell’s clear statements on the December meeting as an effort to push back against market pricing. “Just before the October meeting, shorter-term federal funds futures contracts priced in a probability above 90% for a December cut. Powell’s comments worked. At the time of writing, the market-implied probability of a December cut has dropped to about 70%. A cut in December remains our base case, but with less certainty,” she explains.

Even with the Fed’s narrative around lack of data visibility, investment firms are confident that further rate cuts are coming. For example, UBS Global Wealth Management maintains its forecast of two additional cuts between now and early 2026—with improved liquidity continuing to support risk assets. For David Kohl, Chief Economist at Julius Baer, the October rate cut is a prelude to further reductions in the cost of money. “The FOMC reduced its benchmark interest rate and opened the debate about another cut at the next meeting. The differing stances within the FOMC and the lack of labor market data due to the government shutdown make it difficult to determine the interest rate path at this time. We continue to expect additional 25 basis point cuts at future FOMC meetings amid slower job growth,” he states.

“Powell also highlighted the two dissents in the FOMC decision as evidence that the Committee is not following a preset course. He reinforced this more hawkish tone by suggesting that data uncertainty. Looking ahead, we expect this lack of information to result in a more dovish stance. We foresee an additional cut before year-end, in line with this dynamic and with the revealed preference for a more accommodative stance, evidenced in the early end to QT,” adds Max Stainton, Senior Global Macro Strategist at Fidelity International.

The End of QT

In the view of Max Stainton, Senior Global Macro Strategist at Fidelity International, this accommodative (or dovish) stance was reinforced by the announcement of an early end to Quantitative Tightening (QT), now scheduled for December 1, with reinvestments in MBS to be redirected to Treasury bills starting on that same date.

“Although most analysts expected this announcement at the December FOMC meeting, recent tensions in funding markets appear to have unsettled the Committee about the possibility of increased interest rate volatility, caused by a slight shortage of reserves. Taken together, this continues to demonstrate the Fed’s shift toward greater attention to labor market developments,” he explains.

According to Eric Winograd, Chief U.S. Economist at AllianceBernstein, today’s decision to stop reducing Treasury holdings was not a surprise and should not have significant implications for markets or the economy. “The Fed will continue reducing its holdings of mortgage-backed securities (MBS), but maturities of these will be reinvested in Treasury bills, thus helping the Fed move toward a balance sheet composed solely of Treasury securities, as is its goal,” he indicates.

Regarding QT, he explains that it has largely proceeded as the Fed expected: in the background, with about $5 billion over recent months, and the change now announced is trivial. “Under the current framework for implementing monetary policy, the Fed seeks to maintain bank reserves at ample levels, which means not testing the lower bounds of the market’s tolerance for balance sheet reduction. In fact, the Fed’s balance sheet has already been reduced from a peak of approximately $9 trillion to the current $6.5 trillion,” he clarifies.

In essence, the end of quantitative tightening mainly affects the reserve structure and the functioning of the money market and says little about the future path of official interest rates. That said, the timetable outlined by the Fed disappointed markets, which were expecting earlier implementation in November 2025. “Equity and interest rate markets reacted negatively to Powell’s hawkish tone during the press conference, reinforcing the framework that bad news is good news: weaker economic data would likely lead to greater easing, which could support equity markets,” notes Sharma-Ong.

New Potential Acquisition Deal on the Horizon for the Asset Management Industry. Janus Henderson has confirmed it has received an acquisition proposal from Trian Fund Management, its current majority partner, and General Catalyst Group Management, along with its affiliated funds (General Catalyst).

“The company’s board of directors intends to appoint a special committee to consider this proposal, which was received by letter on October 26 and contemplates the acquisition of all outstanding common shares of Janus Henderson not already owned or controlled by Trian, for $46.00 per share in cash,” Janus Henderson explained in its statement. This would value Janus Henderson’s business at approximately $7.1 billion.

The asset manager acknowledges that Trian first disclosed its investment in Janus Henderson in October 2020 and, as stated in its letter, “publicly submitted the proposal in accordance with its disclosure obligations, as an amendment to its Schedule 13D filings.” Currently, Trian has two representatives on Janus Henderson’s board of directors. “The company values the history of constructive collaboration it has maintained with Trian over the past few years. The special committee is expected to be composed of directors unaffiliated with either Trian or General Catalyst,” Janus Henderson clarified.

The asset manager made it clear that “there can be no assurance that the proposal will result in a definitive agreement or that a transaction with Trian, General Catalyst, or any other third party will be completed.” To conclude the matter, Janus Henderson stated in its release that it does not intend to make further comments unless it deems additional disclosures appropriate.

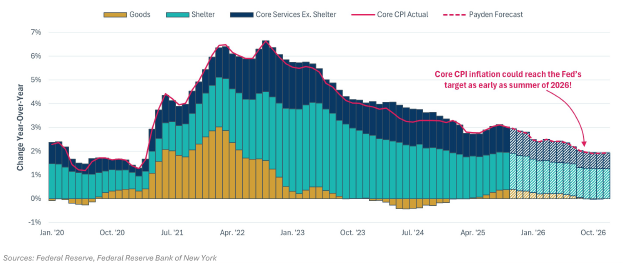

The U.S. Federal Reserve (Fed) faces its monetary policy meeting with the latest headline CPI data for September still resonating, highlighting a further slowdown in underlying price pressures. The index rose 0.3% month-on-month—compared to the previous 0.4%—while core inflation slowed to 0.2%—down from the previous 0.3%.

The report revealed that core CPI inflation increased by 0.2% in September, aligning with the Fed’s 2% inflation target. “Specifically, while tariffs pushed up goods prices, core services and housing prices continue to moderate. Owners’ equivalent rent—the most significant and sticky component of core CPI inflation—recorded its lowest monthly reading since January 2021. The moderation in core inflation, along with continued labor market weakness, supports the possibility of another rate cut by the Fed at this week’s FOMC meeting,” explains Payden & Rygel.

Looking ahead to 2026, in their view, as tariff-related price pressures fade over the next 12 months and service inflation continues to cool, we can anticipate a scenario in which core CPI inflation reaches the Fed’s 2% target by late summer 2026. And, as the Fed governor noted in his latest speech, inflation on track toward 2% will not pose “an obstacle to a more neutral monetary policy.”

“The Fed officials will not be going into the October FOMC meeting completely blind, though they will be navigating through an uncomfortable haze. Since the federal government shutdown began earlier this month, there has been a scarcity of U.S. macroeconomic data releases, particularly regarding the labor market, and we don’t yet know when this data drought will end. At least, the Fed received the September CPI data on Friday, for which a slight uptick is expected,” notes the latest report by Ebury, the global fintech specialized in international payments and currency exchange.

According to the experts, the Fed could rely on this data to restart the cycle of rate cuts. If this happens, it would be the second consecutive cut and would confirm that the Fed is now more concerned about the labor market slowdown than about potential inflation spikes.

A New Cut

Experts agree that the communication received from the Fed ahead of the October FOMC meeting suggests that the lack of available data will not prevent central banks from cutting rates by another 25 basis points. “Which seems odd, considering we are flying blind due to the absence of new official data caused by the government shutdown. However, it is reasonable to assume that labor market conditions have not changed significantly since last month,” says Christian Scherrmann, chief U.S. economist at DWS.

He adds that renewed concerns about the health of the financial system, stemming from weaknesses in certain credit sectors, could provide final support for a 25 basis point rate cut and the end of quantitative tightening. “So far, so good, and markets appear well-positioned in terms of expectations for the upcoming meeting. However, beyond the October meeting, it would be unwise to become complacent. While another cut in December is consistent with the current dot plot, the median of Fed members only marginally supports this outcome. Not everyone favors rapid cuts, and some have voiced concerns about potential inflationary pressures,” Scherrmann argues.

“Historically, precautionary cuts have rarely been one-off measures. A new round of easing would not only mirror last year’s sequence of three consecutive cuts—totaling 100 bps between September and December—but also align with previous ‘insurance cycles.’ In three out of four cases since 1980, the Fed cut rates again within 90 days of the first reduction. Given the limited visibility in the current economic, political, and trade environment, as well as the ‘curious balance’ observed in the labor market—where both labor supply and demand have significantly moderated over the year—monetary policy decisions remain highly data-dependent. Although it would take considerable positive surprises in growth and inflation to avoid a new cut, upcoming price and employment data (with the September jobs report still unpublished due to the shutdown) could decisively influence the FOMC’s decision,” says Michael Krautzberger, global CIO for fixed income at Allianz Global Investors.

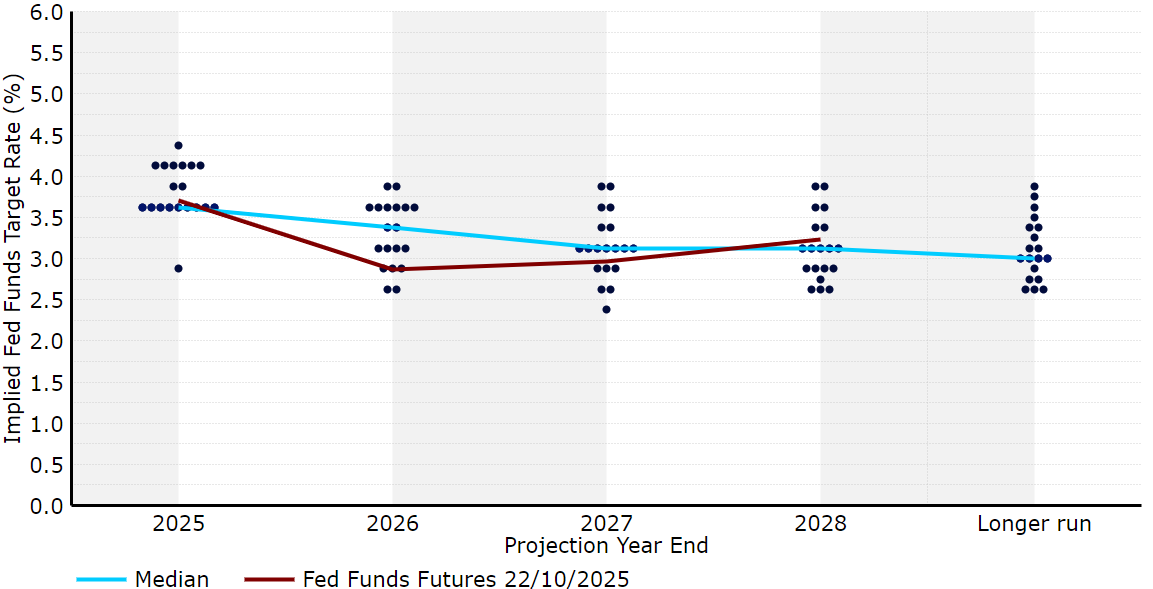

In the opinion of Guy Stear, head of developed market strategy at the Amundi Investment Institute, the Fed is expected to cut rates not only in October but also in December and two more times in the second quarter of 2026. “The market expects this as well, and the more interesting question is whether the Fed’s press conference will support the very aggressive cuts already priced into the curve through early 2027. Equally important will be understanding how the Fed plans to address shrinking liquidity at the short end, given the large volume of Treasury issuance in recent months. We could see a slight increase in two-year yields in the U.S. if the Fed disappoints the market’s aggressive expectations for rate cuts, but yields could also be supported if the Fed starts increasing system liquidity,” Stear explains.

What We Know

Experts have been trying to find clues about the Fed’s upcoming narrative from Chair Powell’s speech on monetary policy outlook at the National Association for Business Economics last Tuesday in Philadelphia. Specifically, Powell confirmed to markets that the October rate cut, which the Fed had already hinted at in its previous meeting, remains on the table. In the same speech, he expressed concern over lower hiring levels, which could pose a real risk to the U.S. economy. He also explicitly stated that, based on the available data, the labor market outlook had not changed since the September meeting, when the Fed’s dot plot outlined two additional cuts for 2025.

“Powell focused on the Fed’s balance sheet and stated that the reduction could be concluded in the coming months. The speech did not introduce any new elements, and the Fed appears on track to reduce rates by 25 basis points at its upcoming meeting on October 28 and 29. The odds of easing at each of the next two meetings have risen above 100%, so the momentum for a 50-basis-point easing cycle is starting, though it remains unlikely in our view,” says Karen Manna, fixed income client portfolio manager at Federated Hermes.

This month’s meeting will not include updated macroeconomic projections or a new dot plot. Therefore, in Ebury’s opinion, markets will scrutinize the tone of the bank’s statement and Powell’s press conference. “Given the absence of new economic releases, we believe the bank’s statement will be practically the same as in September. The Fed will likely once again highlight downside risks to employment, possibly noting that they have increased, and that the federal shutdown has made the decision-making process more difficult. However, the upside risks to inflation remain a headache for the Fed and should warrant a cautious response, despite the belief that the inflationary impact of tariffs will be transitory,” the fintech argues in its report.

More Accommodative Liquidity Conditions?

Cristina Gavín Moreno, head of fixed income at Ibercaja Gestión, agrees with this view and adds what she sees as the most relevant aspect of the meeting: “The end of the quantitative tightening (QT) process and the optimal size of the Fed’s balance sheet are additional points of discussion that are on the table, and this meeting could shed more light on them.”

Florian Späete, senior bond strategist at Generali AM, part of Generali Investments, notes that although the language is vague, Powell’s remarks suggest that quantitative tightening (QT) could end as early as this year. “This measure had previously been expected in the first quarter of 2026. It would represent a shift toward more accommodative liquidity conditions, easing pressure on funding markets. Improved liquidity and downward pressure on the term premium would offset the increasingly pronounced steepening trend in yield curves. However, overall, we assume that global yield curves still have room to steepen, given the higher inflation environment and rising public debt levels,” he states.

According to his analysis, since QT was already expected to end in early 2026, the impact on risk assets and the U.S. dollar is likely to be limited. “The easing of financial conditions, further interest rate cuts by the Fed, and relatively modest investor positioning are also favorable factors. The depreciation of the U.S. dollar, which we had already anticipated, should also be supported by the end of QT. The possible end of QT by the Fed is consistent with the idea of a less restrictive monetary policy in the United States,” he concludes.

John Lamb, Equity Investment Director at Capital Group, analyzed the effects of Trump’s policies, the role of Europe, and highlighted attractive opportunities in the healthcare sector. He affirmed that there is a shift in the global balance, anticipated “some additional weakness” in the U.S. economy, and noted that the “inflationary rebound resulting from tariffs” has yet to materialize. However, the United States remains “resilient” thanks to strong investment in technology and data centers, and its exceptionalism continues to hold beyond the short term.

He also commented that by 2026, the ECB may need to consider raising rates “two or three times,” and that the euro could reach 1.30 against the dollar next year in a context of U.S. dollar weakness. Regarding emerging markets, he noted that China faces the challenge of structurally lower growth, while Indian companies appear overvalued.

This was shared during an in-person meeting with Funds Society, during a stop on the roadshow the specialist conducted in Miami to present Capital Group’s New Perspective Strategy, the global equity strategy the firm has been managing for over 50 years, investing flexibly in quality multinational companies driving global change.

Trump’s Impact and U.S. Economic Resilience

While acknowledging certain challenges stemming from the Trump administration’s policies, Lamb stated that the so-called “American exceptionalism” has not come to an end. “We take a balanced stance. We’re not fully on one side or the other. There are arguments both for and against,” he said.

Lamb expanded on Trump’s tariff policies, which in his view have created short-term difficulties for the U.S. economy. Still, he emphasized the resilience of U.S. companies and the economy as a whole, which have adapted to the trade tension environment.

According to Lamb, the full impact of the tariffs has yet to show up in the data. “We believe we haven’t yet seen the entire effect on the U.S. economy. Our short-term growth and inflation forecasts are less optimistic than the consensus,” he stated.

In that regard, he anticipated “some additional weakness” and warned that the inflation rebound linked to tariffs “has not yet materialized.” However, beyond the short term, Lamb argued that many of the fundamentals of American exceptionalism remain in place, driven by a combination of factors: “deep and liquid capital markets, a strong entrepreneurial spirit, and the rule of law… Many of those components remain intact,” he stated.

He also noted that growth has been supported by robust investment in tech infrastructure, particularly in data centers. While there may be risks of overenthusiasm in that segment, Lamb does not foresee a recession.

Diverging Monetary Policy

In this global context, Lamb said that Europe has performed better than expected. He considers it reasonable for the market to be pricing in three to four rate cuts by the Federal Reserve, but expects the European Central Bank to face the opposite challenge.

“The shift in Europe’s fiscal regime, with strong public spending—especially in Germany—could boost growth while also generating inflationary pressures,” he explained. In his view, the eurozone could potentially see two to three rate hikes.

Lamb also projected that the euro could reach 1.30 against the dollar next year amid U.S. dollar weakness. However, he added that “in the long term, the U.S. will likely benefit from a productivity boost driven by investment in artificial intelligence.”

Healthcare: Targeted Opportunities

Speaking about equities, Lamb pointed to the healthcare sector, where he sees attractive opportunities.

“It’s been a challenging time for the sector,” he admitted, citing negative factors tied to U.S. government policies on drug pricing and reimbursement, as well as tariffs. “But valuations are now near historic lows in relative terms.”

The expert believes political risks have diminished and that the sector combines “attractive valuations with an exciting innovation pipeline.” He cited specific examples such as Eli Lilly, which is about to present clinical trial results for a new oral version of its weight-loss drugs—a development that could “significantly open up the market and expand its reach.”

Capital Group’s New Perspective Strategy does not make “large macro bets by region,” he explained. “We focus on finding the right companies, regardless of where they are domiciled,” he concluded.

Since last Friday, Malaysia’s capital (Kuala Lumpur) has been the setting for the fifth round of trade negotiations between China and the U.S., following a staged escalation in tensions last week. According to experts, these meetings have aimed to ease the atmosphere ahead of the face-to-face meeting between Xi Jinping and Donald Trump, which will take place in three days.

At DWS, they emphasize that the Asian giant is better prepared to face the trade and tariff challenges posed by the U.S. Firstly, as explained in the latest report by its CIO, the situation is not new. “China was already a key focus of U.S. foreign policy under President Biden. Moreover, although China remains one of the main targets of the United States’ tariff policy, its impact was diluted in April, when Washington imposed punitive tariffs on multiple countries worldwide. China also responded quickly to Trump’s return, adopting economic policy measures aimed at stability. And finally, the share of Chinese exports destined for the U.S. has halved over the past eight years, now standing at around 10%. Ultimately, China’s economy today is much less dependent on international trade than is commonly assumed: in 2024, exports accounted for less than 20% of GDP, compared to 36% in the case of the European Union,” they point out.

Just last week, China announced its new five-year plan, which largely signals a continuation of recent policy priorities—under the umbrella of “high-quality development”—placing increased emphasis on accelerating technological self-sufficiency and scientific capabilities. In the opinion of Robert Gilhooly, senior economist specializing in emerging markets at Aberdeen Investments, this will be seen as a continuation of the effort to improve and expand domestic manufacturing capabilities, as outlined in the ‘Made in China 2025’ plan, though it is unlikely the name will be renewed, as it has irritated key trade partners.

“Recently, policy has attempted to boost consumption, but geopolitical pressure is likely to keep priorities tilted toward the supply side of the economy, which will make it harder to eliminate deflationary pressures—even if authorities focus on sectors with well-known overcapacity issues, such as automobile manufacturing, solar energy, and batteries,” Gilhooly notes.

The Secret of Tariffs

In addition to China’s stronger position at the negotiating table, Philippe Waechter, chief economist at Ostrum AM (a firm affiliated with Natixis IM), argues that, at its core, the U.S. tech sector cannot fully decouple from the Asian country. “Trump’s response, with tariffs on China 100% higher than those already in place, is a reaction born of helplessness, as the United States cannot do without many Chinese products. Chinese advances are harming the U.S. tech and defense industries. What’s new is the shortage this could cause on the other side of the Atlantic. It is no longer a matter of prices, but of a break in the value chain. It’s not comparable, and the consequences for U.S. industry could be far greater than the mere application of customs duties,” Waechter states.

As the Ostrum AM expert recalls, “The U.S. economy is strong, but artificial intelligence plays a major role: it explains 92% of growth in the first half of the year. Without it, GDP would have grown just 0.1%. The U.S. economy is likely not as robust as it appears.”

For Sandy Pei, senior portfolio manager at Federated Hermes, despite the renewed escalation of the trade war, the risks facing China’s economy are well understood and already priced in. “We expect supportive policies to stimulate the economy, particularly for high-tech industries, especially in areas where China currently lags behind global leaders. However, financial support is likely to taper off quickly, as the government prefers a market-driven approach: only the most competitive companies will come out ahead,” she argues.

Chinese Equities

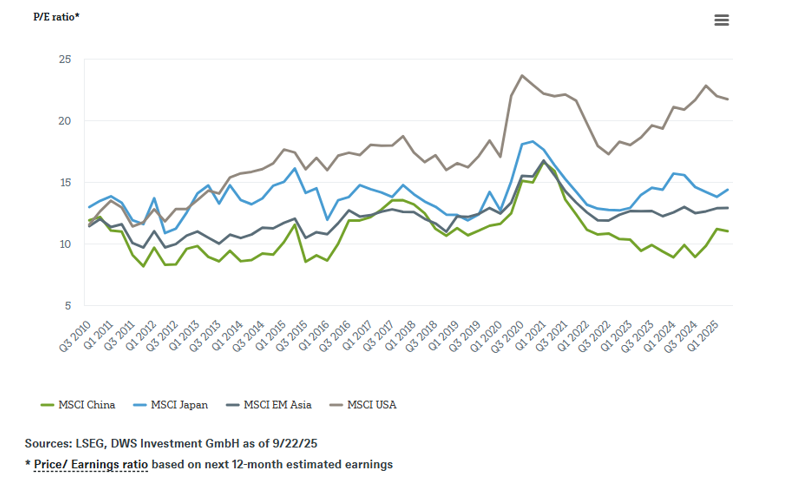

For now, no other country is subject to as intense a burden of tariffs and sanctions from the United States as China. However, the Asian giant also appears to be the best-prepared country for a second Trump term, and DWS believes Chinese equity markets may be benefiting from this. “Sometimes, equity markets can be ironic. Chinese stocks began to rebound roughly at the time Trump returned to the presidency in January 2025,” notes the latest report from its CIO.

The document points out that the factors driving the Chinese stock market are primarily internal rather than external. And, prior to the rebound seen this year, they were far from favorable. “Since 2021, the Chinese market has lagged behind the U.S. and Europe. The problems are well known and, in part, remain unresolved: an oversaturated real estate market, an aging population, high levels of local government debt, power concentrated in the party, weak consumer confidence and high savings rates, inconsistent data quality, and overcapacity in numerous sectors. The government’s ‘anti-involution’ strategy aims to address some of these issues,” it notes.

From the asset manager’s perspective, after adjusting its economic policy, the MSCI China index has gained nearly 40% so far this year, and they consider valuations to have returned to the average of the past fifteen years. “The deterioration of confidence in other regions is boosting China’s position, where the likelihood of a gradual recovery is increasing. Even if a broad-based recovery does not occur, opportunities in the technology sectors could continue to offer solid upside potential, despite the recent valuation reassessment,” says Sebastian Kahlfeld, head of emerging markets equities at DWS.

Federated Hermes Acquires 80% Stake in U.S. Real Estate Investment Firm FCP Fund Manager

Federated Hermes, Inc., specialists in active investment management, has reached an agreement to acquire 80% of FCP Fund Manager, L.P., a U.S.-based private real estate investment manager headquartered in Chevy Chase, Maryland.

FCP specializes in investing across the U.S. multifamily residential asset class, deploying capital through predominant equity and various debt vehicles. Since its inception, FCP has invested, operated, and/or financed more than $14.6 billion in gross asset value, including over 75,000 multifamily residential units.

Upon completion of the transaction, FCP and its team of over 75 members will continue managing investment portfolios and other business operations from their current locations. FCP has six offices in the U.S., including its headquarters in Chevy Chase, Maryland, and local coverage in 19 U.S. markets, providing significant local knowledge and capabilities in high-growth areas of the country.

The total purchase price of up to $331 million includes $215.8 million in cash and $23.2 million in Federated Hermes Class B common stock, which will be paid and issued at closing, along with opportunities to receive additional contingent payments of up to $92 million over several years following the closing.

The transaction strengthens Federated Hermes’ goal of enhancing and growing its offerings in Private and Alternative Markets, where it already has a well-established mix of businesses operating primarily outside the U.S. in private equity, private credit, infrastructure, and real estate, as well as market-neutral strategies, with assets totaling $19 billion as of September 30, 2025.

The transaction will introduce additional expertise as Federated Hermes seeks to develop product solutions for its clients at a time of increasing demand for the private markets asset class. It will also expand Federated Hermes Real Estate’s capabilities in the U.S. market and complement its existing real estate operations in the United Kingdom, established in 1983, with $5.5 billion in assets under management as of September 30, 2025.

J. Christopher Donahue, President and CEO of Federated Hermes, said: “We are delighted to announce today the signing of the purchase agreement for this transaction. Upon closing, this transaction will allow Federated Hermes to enter the U.S. real estate market at a time when the multifamily residential sector is enjoying strong fundamentals and significant growth opportunities. FCP brings a long-standing track record of real estate investment performance, driven by risk-adjusted returns, deep knowledge of local and regional markets, and strong relationships with the communities in which it operates.

An additional attraction is the complementary experience and knowledge in the residential sector, which are vital to continuing to grow our real estate businesses in both the U.S. and the U.K.”

Esko Korhonen, Founding Managing Partner of FCP, said: “At Federated Hermes, we have identified a company with shared values and a strong commitment to building a private markets business. FCP is uniquely positioned to lead the expansion of the private market with Federated Hermes in U.S. residential sector assets. This transaction provides an opportunity to strengthen our institutional platform, enhance our growth trajectory, and provide expanded resources, improving our position as a leading national real estate firm.”

Federated Hermes was represented by K&L Gates LLP and advised by KPMG LLP and Hodes Weill & Associates. FCP was represented by Goodwin Procter LLP and advised by Berkshire Global Advisors.

The transaction was approved by the board of directors of Federated Hermes, Inc. and the executive management of FCP, and is expected to close in the first half of 2026, subject to certain conditions, including obtaining third-party consents and the expiration or termination of the waiting period under the Hart-Scott-Rodino Act of 1976. This transaction will be Federated Hermes’ second Private Markets acquisition since early 2025, following its acquisition of Rivington Energy Management Limited, a U.K.-based infrastructure developer, in April 2025.

Complacency has been one of the most repeated words by investment managers and experts to describe the market in recent months. While stock markets—especially the S&P 500—remain at record highs, experts are now placing less emphasis on the idea that markets are in a “complacent” state, given two sharp movements that occurred over the past week.

Instead, the two words that seem to remain valid in describing the current market are resilience and volatility. “The global outlook reflects a confluence of factors that are keeping markets in a state of fragile stability. In the U.S., corporate strength contrasts with political and trade uncertainty, while in Europe, regulatory pressure and energy dependency remain latent risks. Asia shows resilience thanks to expectations of stimulus and trade agreements, although Japan faces the challenge of balancing monetary and fiscal policy in a high-tariff environment,” says Felipe Mendoza, market analyst at ATFX LATAM.

Gold Adjustment

The headline this week was the sharp 5% correction in gold, after reaching October highs near $4,400 per ounce. According to experts, the strength of the dollar this week put pressure on precious metals, triggering one of the most pronounced drops in years for both gold and silver, as investors looked to lock in profits following a bullish streak.

“From a technical perspective, gold broke through key intraday support levels, which accelerated algorithmic selling and deepened the decline. However, the underlying context remains solid. Central banks continue to buy at a steady pace, and physical demand in Asia remains strong, particularly in China and India. These factors continue to serve as structural buffers against short-term speculative moves,” adds ATFX LATAM.

According to Claudio Wewel, FX strategist at J. Safra Sarasin Sustainable AM, the recent correction is due to broad-based profit-taking driven by a combination of factors. “Although the coming days will likely be marked by volatility, we believe the fundamentals supporting a renewed increase in gold prices remain strong in the medium and long term. Geopolitical uncertainty remains very high, and gold is still underweighted in portfolios. Therefore, we expect investors who had previously stayed away from the metal to continue turning to it and increasing their positions. Finally, the growing interest from stablecoin issuers and an uptick in outflows from crypto assets represent additional upward drivers for gold,” says Wewel.

Simon Jäger, portfolio manager on the multi-asset team at Flossbach von Storch, adds another factor to explain the situation: “Due to ongoing geopolitical conflicts, the central banks of China and Russia in particular have massively increased their gold reserves in recent years. We believe this trend will likely continue. As a result, this year gold has replaced the U.S. dollar (or U.S. Treasury bonds) as the largest investment within central banks’ foreign exchange reserves globally.”

Credit Stumble

The other key topic was U.S. credit. It began last week when regional U.S. banks came under pressure after several lenders reported loan write-downs linked to a bankrupt real estate investment trust (REIT).

As Axel Botte, Head of Market Strategy at Ostrum AM (a Natixis IM affiliate), explains, Tricolor (a subprime auto lender) and First Brands (a leveraged auto parts company) have become the first casualties of accumulated delays in auto loan payments and the sharp increase in tariffs on auto parts.

“Two regional banks are now reporting they were victims of fraud related to loans to credit funds with unfavorable exposure to commercial mortgage-backed securities. The opacity of private credit funds has long been recognized as a risk factor. It’s difficult to assess the systemic risks tied to their activities, but once you spot one cockroach, there are likely more hidden. While the credit minefield may remain contained, reports from the main regional banks are not raising alarms for now; however, credit quality will remain a focal point. The Fed’s announcement to pause balance sheet reduction suggests Jerome Powell is particularly attentive to liquidity conditions,” he argues.

“A senior executive from a major U.S. bank warned that spotting ‘a cockroach’ usually signals there are more, reflecting concern that isolated defaults could foreshadow a broader wave of bankruptcies. To make matters worse, wholesale funding rates have climbed above normal levels, which historically signals a shortage of reserves in the banking system,” adds Benoit Anne, Senior Managing Director and Head of the Market Intelligence Group at MFS Investment Management.

Anne calls for calm, explaining that her team at MFS IM sees no reason for panic. “To begin with, recent remarks by Fed Chair Jerome Powell suggest a review of quantitative tightening at upcoming FOMC meetings. This should ease downward pressure on bank reserves. As for the recent defaults, our investment team considers them isolated, relatively small, and unrelated, which reduces the likelihood of a systemic credit event. In fact, broader markets—including asset-backed securities (ABS) and collateralized loan obligations (CLOs)—have not shown significant spread increases related to these episodes. Overall, it’s worth noting that continued disruptions could create mispricings, offering active managers the chance to deploy capital at attractive valuations,” she explains.

End of the Private Credit Cycle?

Lale Akoner, Global Markets Strategist at eToro, takes a broader view: “We see the credit events in October as idiosyncratic blowups, not systemic fractures. Both companies operated in narrow, high-risk segments of the market—subprime loans with high leverage. The losses were real but concentrated. Crucially, most regional banks showed limited or fully provisioned exposure, with no signs of widespread credit deterioration. This was a wake-up call on layered credit risk, but not a repeat of SVB or 2008 in our view. That said, the opacity of financing structures, the increasing use of PIK interest, and interconnections between funds require closer monitoring through 2026. The good news is that we are in a falling interest rate environment, not in a tightening cycle.”

In this broader reading of the private credit market, Francesco Castelli, Head of Fixed Income and Portfolio Manager of the Euro Bond Fund at Banor SICAV, believes that credit markets are approaching an inflection point in the credit cycle. He notes that “Private Credit markets are behaving like Telecoms in 2000 or Banks in 2007—they were the triggers for major crises in the credit cycle.”

In his view, private credit markets have grown exponentially in recent years due to the high returns they offered, despite not being publicly traded and therefore not pricing in market value on a daily basis. This, in his opinion, makes it harder to detect stress phases, although there are tangible warning signs.

“The main red flag is the behavior of Business Development Companies (BDCs), publicly traded vehicles providing access to private lending, which have entered bearish territory after years of strong gains. This sharp reversal reflects growing investor concern over whether high dividends will continue as borrowers’ cash flows deteriorate and defaults rise. The sudden $10 billion default of First Brands has fueled investor concerns and could be a potential trigger for a broader market reassessment. Combined with the persistent underperformance of CCC-rated bonds compared to higher-quality high yield over the past six months, the message is clear: investors are increasingly distinguishing based on credit quality,” concludes Castelli.