How to Manage Talent in the Asset and Wealth Management Industry

| By Amaya Uriarte | 0 Comentarios

According to the latest report by Morgan Stanley and Oliver Wyman, AI tools and generative automated models have shifted from tasks typically handled by the middle and back offices—such as report preparation and operational controls—to front-office functions.

“While these advancements initially benefited employees by gradually enhancing their productivity, they are now starting to translate into efficiency gains for the company, with experiences indicating up to a 30% improvement in analytical activities,” the document states. This evolution represents an opportunity due to the efficiency it brings, but also a challenge in how to leverage that efficiency and integrate it with professionals in the sector.

The Paths of AI-Driven Efficiency

The report outlines two paths companies can take to capitalize on this efficiency. First, it suggests reinvesting efficiency gains to enhance analysis, arguing that “AI frees up analysts’ time, allowing them to increase the depth and breadth of research, which ultimately enables stronger alpha generation.” Second, it points to optimization as a way to create leaner cost structures.

“Instead of reinvesting time, some companies are reducing their analyst base and relying on AI to handle repetitive and lower-value tasks. Reinvesting efficiency has the advantage of maintaining a stable base of analysts without disrupting the traditional career path of analysts. However, it is likely to reshape their role and the associated required skills: proficiency in AI and automation tools, and the ability to generate original insights based on AI-generated results. It also challenges the learning curve for junior analysts, as they would be required to oversee AI-generated outputs without first mastering the underlying analysis themselves,” the report notes.

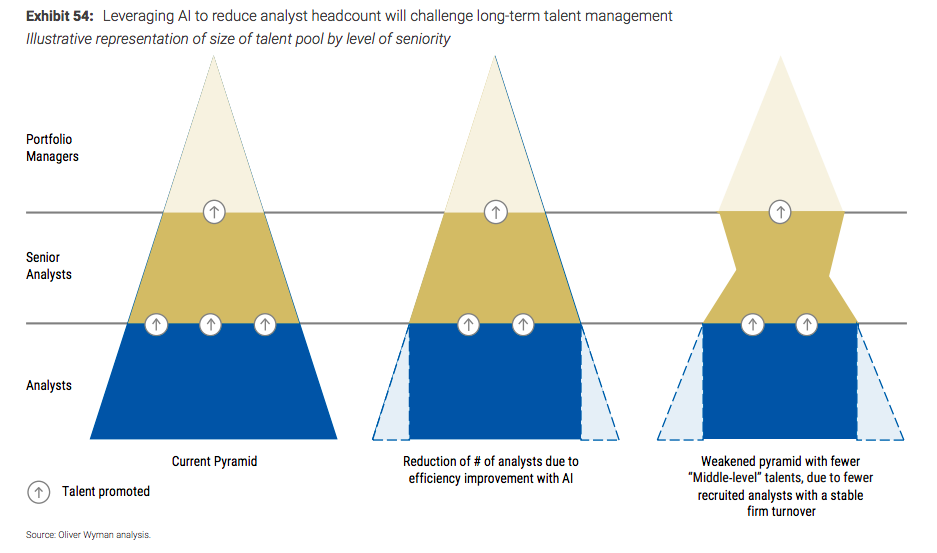

Furthermore, it acknowledges that reducing the number of junior analysts may provide immediate cost savings but warns that, in the medium term, it creates the challenge of the “hourglass effect”: a narrowing at the mid-senior level, which weakens the succession pipeline for senior analyst and portfolio management positions. “Just as many firms are actively seeking to ‘juniorize’ teams to control costs, this exacerbates the seniorization trend. Already, portfolio managers are becoming increasingly senior, with 50% of them having more than 25 years of experience (compared to 39% in 2020),” the report states.

“In This Context, Human Resources Functions Must Adapt Quickly and Work Hand-in-Hand With Investment and Technology Teams to Redesign Workforce Planning, Integrate AI Capabilities Into Learning Pathways, and Structure Sustainable Succession Strategies That Ensure Long-Term Organizational Resilience,” the report proposes in its conclusions.

Attracting and Retaining New Talent

The document argues that the growing influence of AI in this industry requires asset managers to seek new and scarce skill sets outside the core group of finance graduates. Furthermore, as both the asset management and wealth management industries shift toward a more client-centric model, each must increasingly cultivate a workforce that excels in relationship-building, emotional intelligence, and cultural sensitivity.

“While this broadens the scope of potential hires beyond traditional financial and mathematical backgrounds, it also forces asset managers to compete for these more transferable skills with broader industries (particularly tech companies). Therefore, firms must renew their value proposition to attract this wider audience,” the document states.

In addition to attracting and retaining talent, the conclusions assert that HR departments in investment firms need to rethink their approaches to people development in order to adapt to the hybrid “human + AI” mode of work. As explained, “teaching practical AI knowledge must be balanced with building stronger judgment skills. Leaders, in particular, may need support in change management, cross-functional collaboration (investment, data, engineering), and the ethical use of AI.”

In this regard, the report presents a clear proposal: “Rotations, hands-on AI labs, and mentorship pairings between senior portfolio managers and technologists can be used alongside traditional HR approaches to preserve deep expertise while building the leaders of the future.”

Finally, the report emphasizes that scaling AI within traditionally conservative asset and wealth management cultures will require a deliberate cultural shift. “Existing cultural profiles will shape how quickly and widely AI is adopted, so tailoring interventions to current and lived cultures will be more effective. Designing the workforces and cultures of the future will also require activating the right incentive levers and creating regular rituals, such as recognizing AI-driven improvements in performance reviews, internal showcases of AI achievements, and leaders visibly modeling new behaviors,” the report concludes.