The S&P 500 and the Nasdaq, Heavily Weighted in Tech, Reached New All-Time Highs a Week Ago, Driven by Positive News on U.S.–China Trade Talks That Boosted Investor Sentiment. UBS Global Wealth Management expects that, with companies reporting strong third-quarter results in a favorable environment, U.S. equities will continue to rise in the coming months.

In fact, they point out that the three key factors driving market performance—earnings, monetary policy, and investment—are currently favorable: “The Fed’s easing policy points to a supportive macroeconomic environment. The strong start to third-quarter earnings suggests solid profit growth. The strong demand for computing resources should support robust investment in artificial intelligence (AI),” they state. As a result, Mark Haefele, Chief Investment Officer at UBS Global Wealth Management, acknowledges that they maintain their “attractive” view on U.S. equities and expect the S&P 500 to reach 7,300 points by June 2026.

Could We Be Facing a Year-End Stock Market Rally? For Chris Iggo, Chief Investment Officer at AXA IM, “markets have continued to behave very benignly so far in October,” and he believes that “the earnings season will be strong enough to support the belief that current valuations are sustainable, which could allow for a potential market rally in November, a month that is usually strong for the S&P 500.” Looking ahead to the coming weeks, he highlights that “the market is strongly anticipating a Fed rate cut on October 29, followed by another before the year-end holidays,” in a context where “inflation fears have subsided.”

Room for Active Management

This market behavior reignites the long-standing debate over whether the U.S. large-cap market is too efficient for active managers to outperform. As concluded by Schroders in its latest report, many critics of active fund management use the zero-sum game argument to claim that it is mathematically impossible for active fund managers to outperform passive ones net of fees, which is “categorically false.”

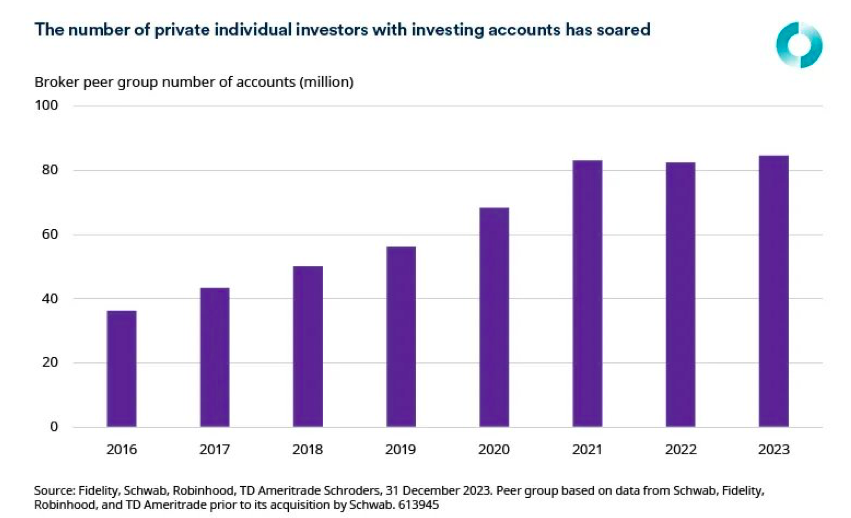

“The increase in the number of investors and the value of investments not allocated according to overall market weightings means we can be more optimistic about the future of active management than we were about the past. It doesn’t mean the average fund manager will outperform, but it does mean it should not automatically be assumed that they can’t or won’t. Now is the time to reconsider your beliefs about active and passive management, even in markets you thought were efficient,” argue Duncan Lamont, Head of Strategic Research, and Jon Exley, Head of Specialized Solutions at Schroders.

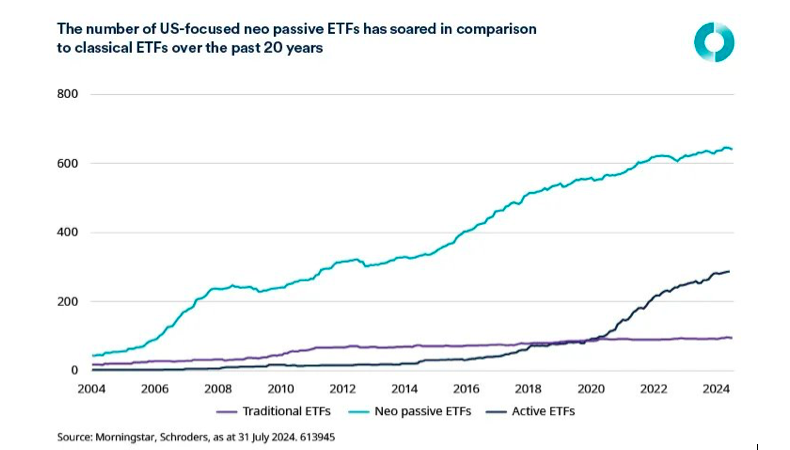

The firm defends in its report that there may be greater opportunities for active managers to outperform in the future than in the past. In fact, it challenges the old formulation of the “zero-sum game” argument and adds that the classic view of the market as divided between active and passive investors should now include a new category: the “neo-passive.”

As Lamont and Exley explain, what has changed recently is the rise of investors who fall into this “active investor” category but are not active equity fund managers. “That’s why we believe we can have more confidence in the future prospects of active fund managers. First, there has been a proliferation of ETFs in recent years that do not follow the broad market. We call these ‘neo-passive.’ In the U.S. alone, there are now more than six times as many of these ETFs as traditional ETFs, and inflows into these strategies have been 50% higher than those into traditional ETFs from early 2018 to the end of July 2024,” they argue.