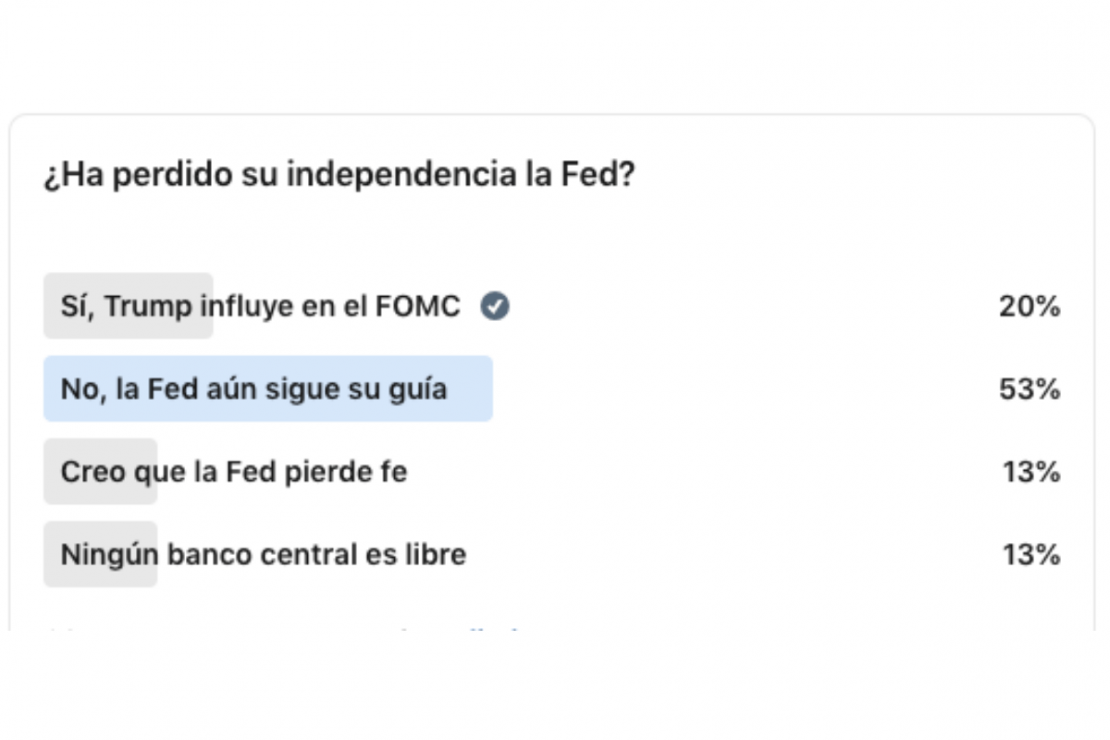

The Debate Over the Fed’s Independence Will Remain Alive

The debate over the independence of the Fed will remain ongoing, as it extends beyond the figure of Jerome Powell himself, whose term as Chair ends in May 2026. According to Felipe Mendoza, CEO of IMB Capital Quants, the discussion around his succession is intensifying. “Donald Trump will interview Christopher Waller for the position, while Kevin Warsh’s odds have risen to 41%, compared to the 90% that Kevin Hassett had at the beginning of December. Trump has stated that the next Fed Chair should consult him on interest rates and that he wants to see them at 1% or lower within a year. Jamie Dimon, CEO of JPMorgan, has said that Warsh would make a great Fed Chair. In this context, White House advisor Kevin Hassett argued that economic data points to inflation heading toward the 2% target and that, although Trump has strong views, the Fed must maintain its independence.”

Additionally, according to Álvaro Peró, Head of Fixed Income Investments at Capital Group, the debate surrounding the Fed is a clear example of a broader trend experienced in 2025. “Significant shifts have occurred in the macroeconomic and geopolitical landscape. Principles that have underpinned the global economy for decades—such as free trade, globalization, and central bank independence—are being called into question,” Peró explains.

The Risks of Losing Independence

According to experts at Vontobel, compromising the Fed’s independence entails significant risks. “When a central bank’s credibility weakens, markets stop interpreting its policies through the lens of economic data and begin to view them from a political perspective. This shift first becomes apparent in expectations. Survey-based measures may appear stable for some time, as both households and professional analysts tend to adjust their views gradually. However, market prices react more quickly. Investors incorporate an inflation risk premium into their base outlook, which is why implied inflation rates often exceed survey-based expectations once credibility is in doubt,” they explain.

In their view, uncertainty around the central bank’s reaction function raises the term premium on longer-dated maturities. “Long-term rates begin to reflect additional compensation for potential policy errors and inflation volatility, rather than just the expected path of short-term interest rates. If fiscal objectives—such as the desire to keep financing costs low relative to nominal growth—begin to influence monetary policy, decisions may tilt toward financial expediency. While this may ease short-term funding pressures for the public sector, it functions as an inflationary tax on savers and raises the required returns on private assets,” they add.

As history shows, financial conditions tend to follow a predictable sequence. That is, the yield curve steepens as the short end responds to a more accommodative monetary stance, while the long end shows resistance. Credit spreads settle at higher levels as lenders price in increased uncertainty. “The dollar tends to strengthen during periods of stress when liquidity tightens in a crisis, but it then weakens if real yields are suppressed and the policy framework appears less sound,” the asset manager’s experts conclude.