For just under six months, markets have begun to anticipate with great force the arrival of inflation. One of the most powerful triggers, which caused the Fed to adopt a more aggressive stance and raised alarm bells among investors, was Donald Trump’s arrival to the US presidency; elected in the November elections, he’s been leading the country since last January. However, when referring to the reflationary trend in the market, Paul Shanta, Head of Fixed Income Absolute Return at Old Mutual Global Investors, is very graphic in pointing out that the inflationary trend goes far beyond politics. “Trump did not invent US inflation,” he said firmly in the framework of a recent event held in Oxford by the management company.

“By 2014 we were starting to see a rise in wages and in core services in the country. Inflation was there before Trump,” he recalls. Pressures began with interest rates in negative territory and, it soared as early as last July. So, according to the expert, it would be more appropriate to say that “Trump cannot do anything to curb inflationary expectations,” instead of saying that it is he who generates them.

It is true, however, that the President’s plans are inflationary: the tax cut project, the infrastructure program, and his commercial proposals, will support that increase in prices that occurred prior to his arrival

However, the market is not accounting for higher inflation- it expects only 2% up to 2026 – and that’s where the fund management company sees opportunities:Shanta explains how they position their debt fund with absolute return strategy to benefit from this imbalance, with positions to benefit from a rebound in US inflation. “The interest rate markets are getting ahead of themselves,” he says.

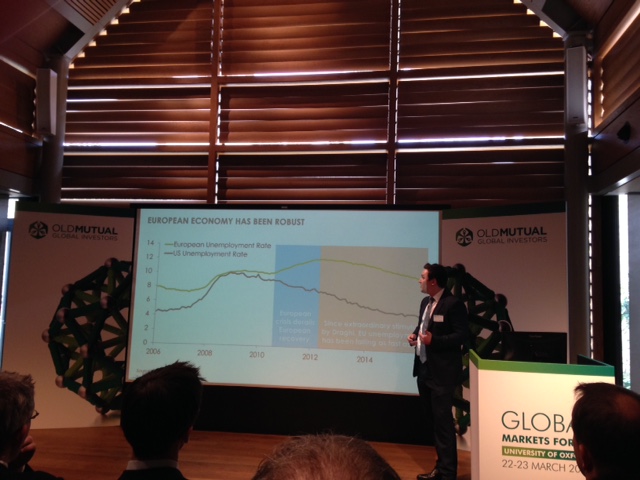

On the situation in Europe, he values Draghi’s work in achieving, like the Fed in the US, the falling unemployment is rate in many countries. And points out that “Inflation is not just the story of the US,” since consumer prices are also rising, and in markets such as Italy, France, Germany, and Spain are already reaching 3%. “Inflationary pressures are starting in Europe, with underlying Euro area inflation rising,” he insists.

However, there are also imbalances between market projections (from 1.3% at the end of 2020, with 67 basis points of ECB rate increases in that period), and reality (the ECB projects 1, 7%), therefore something’s amiss. “It‘s not consistent: expectations of market inflation are too low, while expectations of rate increases are very high.” The fund management company tries to take advantage of these differences.

The Arrival of Turbulence

At the conference, Mark Nash, a multi-sector fixed income manager, warned that in fixed income, “the days of earning easy money are over” and pointed out that after a rally environment in all assets (fixed income doubled its value in six years), there is a time for changes, marked by structural factors, causing him to predict volatility and turbulence.

Among those changes to be considered, populism in the face of problems such as low wages, inequality, or immigration; the demographic changes, with the growth of the aging population and the increase in dependency ratios; the new role of central banks … “Financial assets will be impacted: there are many turbulences ahead.”

By Alicia Miguel Serrano

By Alicia Miguel Serrano