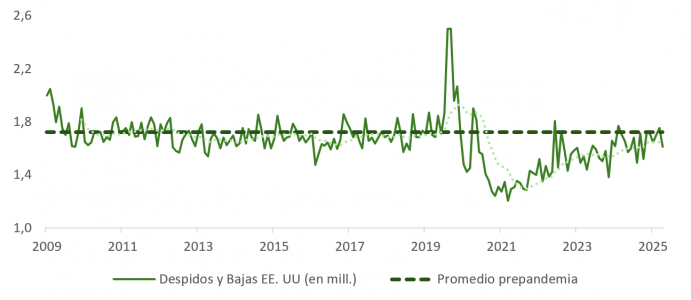

The year begins with few surprises on the macroeconomic front. The U.S. labor market remains in a gray area: hiring appears sluggish, yet there are no significant increases in layoffs. The December ADP private employment report came in below expectations (41,000 vs. the expected 50,000), although it confirms a trend of stability since mid-2025. For Friday’s payroll report, an increase of around 60,000 jobs is anticipated, along with a slight improvement in the unemployment rate from 4.6% to 4.5%.

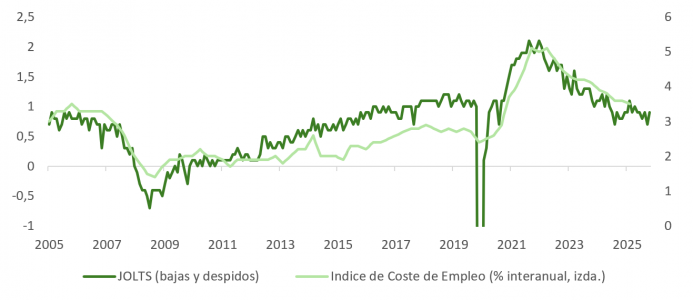

The November JOLTS survey reinforced this mixed picture: job openings declined from 7.67 to 7.15 million, but voluntary quits rose, typically a sign of worker confidence. Layoffs remain stable. The message? A fragile balance, with no clear signs of acceleration or systemic deterioration. Even so, the divergence between public and private employment could distort the broader interpretation. The BLS’s upcoming methodological revision in February could mark a turning point in how labor data is assessed.

In this context, the Fed maintains its “wait and see” approach, with growing attention on employment trends as a key variable for adjusting monetary policy. The possibility of an additional rate cut by mid-2026 will largely depend on how the labor market evolves in the second quarter.

Growth, CAPEX, and Focus on the Tech Sector

The Atlanta Fed’s GDP model projects above-potential growth. The recovery remains concentrated in specific sectors, such as technology, which generate little direct employment. Focus will turn to fourth-quarter results from hyperscalers to assess whether investment momentum is holding. However, BEA data shows that tech CAPEX has lost traction in recent months.

The potential slowdown in tech investment comes at a time when the market is beginning to demand concrete results. Investors are no longer rewarding narratives alone, they are starting to penalize models without clear profitability. This could lead to a rotation toward sectors with more visible fundamentals.

ISM Services and Favorable Signals for Risk Assets

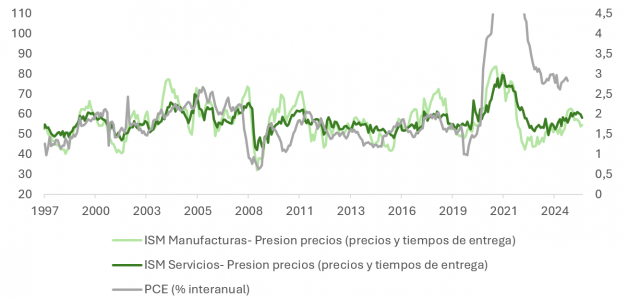

The ISM services index exceeded expectations (54.4) and showed improvements in the new orders and employment components (the latter rising to 52, entering expansion territory), while the prices subindex declined. This combination of easing inflationary pressure and modest gains in activity and employment is favorable for risk assets, helping to keep the 10-year Treasury yield below 4.2%. That, in turn, supports equity valuations and strengthens expectations that the Fed could cut rates more than markets had anticipated after its last meeting.

The composite ISM and JOLTS indicators support the case for wage moderation. Layoffs are at a six-month low, and the Challenger index fell from +23.5% to -8.3% in December. This environment reinforces the post-pandemic normalization narrative, with a soft landing increasingly gaining traction as the baseline scenario.

AI, Productivity, and Pressure on Wages

The accelerated adoption of AI tools is beginning to show effects on productivity and labor structure. While it enhances efficiency, it also reduces employees’ bargaining power, contributing to further moderation of real wages in 2026.

Although large-scale AI investment began in 2024, its impact on productivity remains uneven. Some major companies have achieved tangible improvements, while others are still in the exploratory phase. The market is beginning to differentiate between those with a clear monetization strategy and those without.

This shift in focus will also have implications for the labor market. Sectors such as financial services, marketing, and administrative technology could see workforce adjustments in favor of leaner structures.

Energy, Housing, and the Electoral Agenda

On the geopolitical front, U.S. control of Venezuela’s oil sector, with a projected release of 30 to 50 million barrels, could stabilize crude prices between $50 and $60. This aligns with Trump’s goals of protecting the purchasing power of his electoral base.

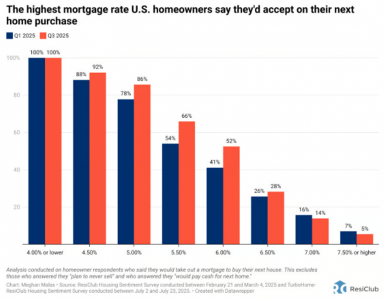

President Trump is also seeking to improve housing access. His proposals include limiting the role of institutional investors in the residential market, allowing retirement savings to be used for home purchases, and promoting mortgage portability. In addition, he is pressuring Fannie Mae and Freddie Mac to acquire up to $200 billion in MBS, which would lower real estate financing costs. If fully implemented, the 30-year mortgage rate could fall below 6%, compared to the historical average spread of 1.76% over the 10-year Treasury (currently at 2.03%).

These measures carry a strong electoral component. The early 2025 ResiClub survey suggests they could help revive the housing market. Understanding the behavior of the “lower leg” of the K-shaped economy will be key to sector allocation in portfolios.

Political Stimulus and Inflation Expectations

With limited fiscal space (debt-to-GDP above 120%), Republicans may intensify the use of alternative policies: deregulation, tax cuts, selective tariff reductions, and access to cheaper financing. The OBBBA plan will play a key role in catalyzing investment during the first half of the year.

At the same time, inflation could ease more than expected in the second half of 2026. The impact of tariffs is likely to fade, and productivity gains from AI may have a meaningful disinflationary effect. Trump may also choose to ease certain trade sanctions (including those on China), aiming to support growth and broaden his electoral base.

In addition, private consumption could rebound if direct transfer mechanisms, such as checks or temporary subsidies, are activated. The conditions for a more expansive second half in terms of consumption are in place, as long as external shocks do not materialize.

Sector Rotation and a Rally Beyond Technology

While AI-related CAPEX and productivity gains are expected to remain in the spotlight, the rally could extend to previously lagging sectors such as industrials and consumer goods. Active sector selection will be key in 2026 to capture shifts in the composition of growth. Valuations continue to show exploitable dispersion.

In this environment, maintaining a balanced exposure across technology, advanced manufacturing, and services could be a prudent strategy. Additionally, cyclical sectors may benefit from an extended economic cycle if consumption holds and inflation continues to ease.

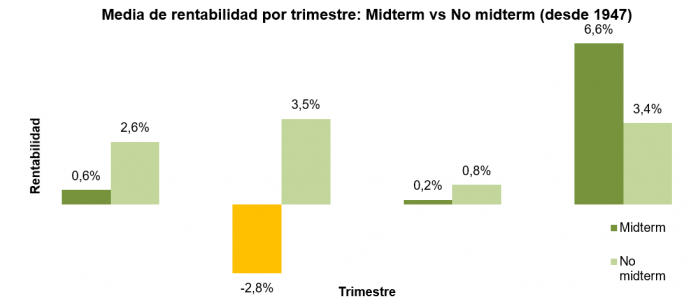

Tactically, the combination of contained interest rates, disinflationary pressure, and active policy measures could create a favorable backdrop for maintaining exposure to risk assets during the first half of the year. However, we anticipate increased volatility and will be monitoring historical parallels with U.S. midterm election periods.