China’s strong close in 2025 keeps the country’s outlook firm for 2026 and its growth target around 4%-5%, driven by technological innovation and investment. Looking ahead to next year, some of the tailwinds expected to support the Asian giant include stronger domestic consumption and improved diplomatic relations with the U.S.

“Although these factors could support the Chinese stock market, policy missteps are always a risk, and companies and consumers should play a leading role in driving growth,” note sources from KraneShares.

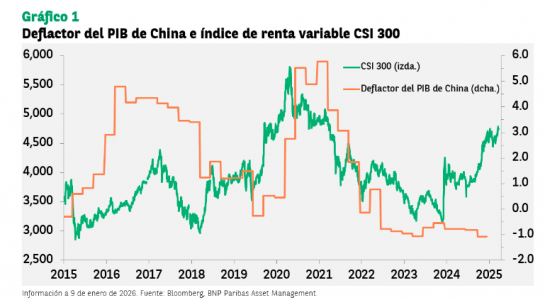

Macroeconomic Data: The GDP Deflator

According to Robert Gilhooly, senior economist specializing in emerging markets at Aberdeen Investments, the set of easing measures announced in recent weeks, along with the signal that cuts to key interest rates will occur in due course, will help underpin real GDP growth in 2026.

“However, the outlook for nominal growth may remain more challenging, as illustrated by the record streak of 11 consecutive quarters of negative growth in the GDP deflator. In fact, although recent data on fixed asset investment points to some success in reducing investment in the automotive industry, the economy-wide overcapacity is likely to continue weighing on inflation, partly because the People’s Bank of China (PBOC) appears more willing to allow greater appreciation of the renminbi. The large number of maturing fixed-term deposits opens the door to further interest rate cuts, while protecting banks’ net interest margins (NIM). A key question is whether these significant household savings will flow into the stock market; however, it is likely to be very difficult to spark a slow bull market,” Gilhooly concludes.

In this regard, Ecaterina Bigos, Chief Investment Officer for Asia excluding Japan at AXA IM Core (part of BNP Paribas AM), believes the country’s GDP deflator remains firmly in negative territory, falling for the third consecutive year, marking the longest stretch of broad price declines since the late 1970s.

“For equity investors, the GDP deflator is a key indicator for assessing corporate performance, profit growth potential, and overall market conditions. Despite signs of rising inflation, China continues to face various deflationary pressures. The country’s economy, which has been impacted by the decline in the real estate market and weak consumption, has struggled to emerge from the deflation recorded since the end of the pandemic. Overproduction in certain sectors has led to an oversupply of goods, forcing companies to cut prices to stay afloat,” explains Bigos.

Betting on Technological Innovation

In this context, KraneShares expects China’s 15th Five-Year Plan, scheduled for release in the first quarter, to support the development of high-tech industries, increase technological self-sufficiency, and stimulate domestic demand and inflation. “Efforts to curb overcapacity and downward competition, especially in the solar panel industry, could bear fruit in 2026, potentially resulting in improved corporate profit margins and inflation,” they add.

For now, the draft of this plan suggests that technological innovation and broad economic expansion are key priorities. At the same time, behind the scenes, top government leadership is paying close attention to the growth of domestic consumption.

Focusing on the main goals outlined during the 2025 Central Economic Work Conference (CEWC), an annual economic meeting involving President Xi and the State Council—KraneShares experts highlight deepening the expansion of the “Artificial Intelligence +” policy; reforming policies to support high-quality development while correcting destructive competition; and stabilizing the real estate market through city-specific policies to optimize housing supply, including purchasing part of the existing commercial housing stock for affordable housing use.

“In December, President Xi published an article titled Expanding Domestic Demand Is a Strategic Move. In it, he stated that ‘expanding domestic demand is related to both economic stability and economic security,’ and that domestic demand will be supported, among other measures, by ‘promoting employment and improving social protection,’” they add.

The Relationship with the U.S.

KraneShares experts believe that the restart of diplomatic relations between the U.S. and China could bring greater clarity to global export markets for Chinese goods, the status of their ability to import high-end chips, and reduced volatility in equity markets, especially abroad.

“We believe markets are underestimating President Trump’s desire to reestablish U.S.-China relations. We are optimistic that the trade and national security measures already implemented or underway could give the Administration the confidence to work toward improving long-term relations,” they note. These measures include reshoring automobile manufacturing and other critical industries to the U.S., as well as export restrictions on chips.

“We believe President Trump may expand the trade truce established with President Xi during their meeting in South Korea earlier this year. Although we may see tougher legislative initiatives in Congress, such as the BIOSECURE Act, we think it is unlikely these will seriously derail the White House’s efforts,” they add.

Implications for Chinese Equities

Without a doubt, 2025 was a strong year for Chinese equities, driven by improved confidence, especially in growth and technology sectors. Many investors reallocated their portfolios during the year, although some remain on the sidelines, particularly U.S. investors sensitive to geopolitical headlines. And despite the challenging macroeconomic environment, Chinese equity markets posted returns above 10% in 2025.

In Bigos’ view, this divergence from macroeconomic trends may be due to the strong performance of sectors such as technology, thanks to advances in artificial intelligence, as well as biotech and others that also benefit from anti-involution initiatives. “Moreover, the increase in liquidity has supported the revaluation of companies, as savings have been redirected into equities: a dividend yield more attractive than deposit interest rates is drawing investors. Meanwhile, fixed income returns have declined, market volatility has increased, and the real estate market remains weak, prompting investors to seek alternative investment avenues,” she explains.

Looking ahead to this year, KraneShares experts believe that the 15th Five-Year Plan’s focus on technological self-sufficiency, anti-involution policies that improve corporate earnings, and increased consumer spending will allow for a strong year in China’s equity market. “Meanwhile, we believe the Trump administration will seek to move forward with the reestablishment of diplomatic relations with China, reducing headline risks and allowing some U.S. investors to reallocate their investments,” they emphasize.

For the AXA IM expert (part of BNP Paribas AM), weak confidence in the private sector and among consumers, along with supply-demand imbalances, increasingly limit the potential for reflation and, ultimately, corporate profits. “Reviving domestic demand is essential to achieve sustained long-term growth, but it will still take time to redirect the economy toward higher consumption levels. For now, economic policy remains focused on an investment- and trade-driven growth model, with an emphasis on developing a modern industrial system and achieving technological self-sufficiency. In this context, investors should pay close attention to those areas that benefit from this policy direction and from technological innovation,” concludes Bigos.