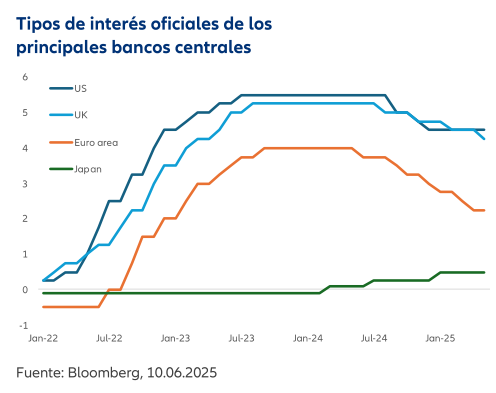

Since December, the Federal Reserve has kept its monetary policy unchanged, after swiftly reducing its target rate from 5.25% to 4.25% over the last four months of 2024. For this meeting, it is expected to maintain the status quo, as it has shown reluctance to take new action.

According to Erik Weisman, Chief Economist at MFS Investment Management, the only point of interest may come from the new set of forecasts in the Summary of Economic Projections (SEP), which could point to slightly slower growth, combined with slightly higher inflation.

“We’ll also be watching the dots—the Fed’s interest rate forecasts—which could shift to indicate only one rate cut this year. Overall, none of this is likely to surprise investors. The Fed will probably acknowledge that the backdrop remains uncertain, and that the best course is to do nothing. As for potential rate cuts, it’s fair to assume they’ve been delayed, and none is likely before the fourth quarter of this year,” Weisman argues.

Focus on the Fed

Although no changes or cuts are expected from the Fed, investment firms agree that the pressure on Powell and the central bank has increased. “One of the hallmarks of U.S. President Donald Trump’s two terms has been his willingness to publicly challenge the Fed Chair whenever he believed interest rates were too high or that the institution had acted too slowly. In fact, Trump has claimed he should participate in monetary policy decisions and has attempted to undermine the central bank’s authority. Moreover, before taking office, U.S. Treasury Secretary Bessent even said that if the government announced in advance who the next Fed Chair would be, it could weaken the current chair’s power,” notes the senior economist at Allianz GI.

These pressures are compounded by the complex geopolitical environment. “If not for exogenous shocks, tariffs, and oil, it seems the Fed has successfully concluded the post-pandemic monetary policy cycle, to borrow Christine Lagarde’s phrasing about the ECB two weeks ago. May’s U.S. CPI data was particularly encouraging. While it’s highly likely that the Fed will reaffirm its ‘wait and see’ stance this week, the FOMC’s dot plot for 2026 and 2027 could show some divergence among members, with hawks and doves emerging, divided over the risks of persistent inflation in the U.S. We wouldn’t be surprised if only one rate cut is shown in the new dot plot. However, we believe the longer-term dots will be more interesting,” says Gilles Moëc, Chief Economist at AXA IM.

According to his estimate, assuming the median projection remains unchanged from March, three cuts (to 3.37%) are expected in 2026. “However, the dispersion around the median might be more telling than the median itself. In fact, we could see a group of doves pushing for quicker cuts and faster convergence toward neutrality,” he adds.

Will the Fed Make More Cuts?

Philip Orlando, Senior Vice President and Chief Market Strategist at Federated Hermes, sees potential for the Fed to cut rates twice this year. “CPI and PCE inflation indicators have declined year-to-date through April and are now at four-year lows. The Fed’s June 18 monetary policy meeting includes an updated summary of economic projections. Officials will need to reconcile their restrictive monetary policy—since the upper bound of the federal funds rate is currently at 4.5%—with the fact that nominal CPI is only 2.3% year over year,” he explains.

In his view, there is significant room to lower rates to 3% over the next 12–24 months, and he expects two quarter-point cuts later this year: “The most likely timing would be September and December, and we expect the Fed to set the stage for these cuts at its June and July 30 FOMC meetings, as well as at its Jackson Hole summit in Wyoming from August 21 to 23. With the prospect of lower rates and no recession on the horizon, we maintain our target of 6,500 for the S&P 500 this year and 7,000 in 2026,” he says.

Markets Watch the Dot Plot

Finally, Harvey Bradley, Co-Head of Global Rates at Insight Investment, notes that beyond Fed Chair Powell’s press conference, markets will closely watch the Fed’s quarterly dot plot for signals on how and when the central bank might resume its cutting cycle.

“In both March and December, the median projection was for two rate cuts by year-end, which is roughly what markets are currently pricing in. Given the uncertainty facing markets, it’s difficult to predict whether the forecasts will change significantly. On one hand, Fed members may now factor in a higher effective tariff rate, with early signs of tariff-related inflation beginning to show. On the other hand, less volatile—or ‘stickier’—sources of inflation, especially in major categories like rent, are showing impressive and potentially sustainable signs of disinflation. The labor market is also showing some cracks, with continuing jobless claims at cycle highs. This could help the Fed continue normalizing its monetary policy. Altogether, the projections may remain largely unchanged,” he argues.

Insight’s base case is for two cuts this year, followed by further reductions in 2026 toward a terminal rate of 3%, driven by below-trend growth outcomes—a landing zone the Fed would likely describe as “broadly neutral.” “In any case, while the Fed remains on hold, we believe this could be a good opportunity for investors to lock in relatively high yields in fixed income while they are still available,” concludes Bradley.