The S&P 500, the most representative index of the U.S. economy, has accumulated a return of around 7.5% so far this year (data as of July 23, 2025). In the same period, the MSCI Emerging Markets has gained nearly 18%, the EuroStoxx 55 has advanced 8.5%, and the Topix has added more than 6%. This is a somewhat novel situation after the strong dominance of the U.S. stock market in recent years. These returns are accompanied by positive flows, particularly towards Europe, raising the question: Are we at the beginning of a major rotation?

Small Changes, Big Changes

“It is too early to talk about a major rotation, but smaller ones should occur,” says Benjamin Melman, Chief Investment Officer at Edmond de Rothschild AM. The expert cites several reasons that are holding back this major rotation, starting with the fact that “international diversification from the U.S. investor’s perspective has not been rewarded, as foreign assets have shown lower Sharpe ratios from a historical standpoint.” Melman also points out that “there is no recession in sight in the U.S.” and that the monetization of AI is not yet a market topic, “so U.S. investors are not in a hurry to invest abroad.”

That said, the expert does believe that U.S. investors “could slightly reduce their underexposure to some international assets” towards markets like Japan, Europe, or emerging markets. “Likewise, international investors overweighted in U.S. assets could also reduce their exposure to the U.S., as the American giant’s supremacy that prevailed at the beginning of the year has lost significant momentum,” he concludes.

The Moment for European Equities

Other experts consulted for this report are more categorical. For example, Sabrina Denis, Senior Portfolio Strategist at Janus Henderson, highlights that one of the “most notable surprises” of 2025 has been the strong rebound of non-U.S. stocks, evidenced by the 16% rise of the MSCI All Country World Index (ACWI) ex-USA (as of June 2025), compared to just over a 2% increase of the S&P 500 in that time, which for the expert “clearly indicates that a significant rotation towards developed markets outside the U.S. is already underway.” “This performance is not just a short-term anomaly but is supported by deeper structural changes and attractive valuations in non-U.S. markets,” she adds.

Víctor de la Morena, Chief Investment Officer at Amundi Iberia, summarizes the sentiment of many investors these days: “There is no doubt that the American economy remains the most important in the world; however, the European economy has gained relevance or ‘momentum’ recently thanks to economic recovery and European stimulus plans that are being increased and will serve as a major catalyst for the coming years, especially in infrastructure and defense.”

From Jupiter AM, European equity managers Niall Gallagher, Chris Legg, and Chris Sellers state that they see the possibility of “a shift in the economic order that could benefit European equities.” Specifically, the trio of experts believes that “structural changes in trade, capital allocation, and government policies are contributing to a long-awaited shift towards Europe.”

In particular, the managers point to the attractiveness of Southern European countries, a region they consider “is approaching the end of nearly two decades of deleveraging.” This implies that “consumer debt is low, the banking sector is healthy and capable of supporting expansion, and even immigration patterns are positive.” Additionally, as they indicate: “These countries have abundant and cheap energy, such as Spain, which has significant solar and onshore wind resources.”

This positive outlook on European equities is also shared by Andrew Heiskell, Equity Strategist at Wellington Management, and Nicolas Wylenzek, Macroeconomic Strategist at the firm: “European equities have entered a regime change that has recently accelerated, which could lead to the largest rotation since the global financial crisis.”

While the strategists warn that “this transition is not without challenges,” they also highlight Value segment stocks as the main beneficiaries, such as banks, telecoms, defense companies, or European small caps. They also believe that companies key to the energy transition with high entry barriers, such as network operators, as well as companies they refer to as “quality stable compounders”—that is, “resilient companies with consistent growth and strong balance sheets, whether Growth or Value style”—will benefit.

Conversely, they state that “the main losers could be those that benefited from globalization and a low-interest-rate environment.”

New Arguments

Mario González, Head of Capital Group’s business in Spain, Portugal, and US Offshore, points out that since “Liberation Day” on April 2, U.S. equities have shown a strong correlation with non-U.S. equities—something expected in a period of high volatility—but adds that “once things settle, the situation for non-U.S. stocks looks favorable.”

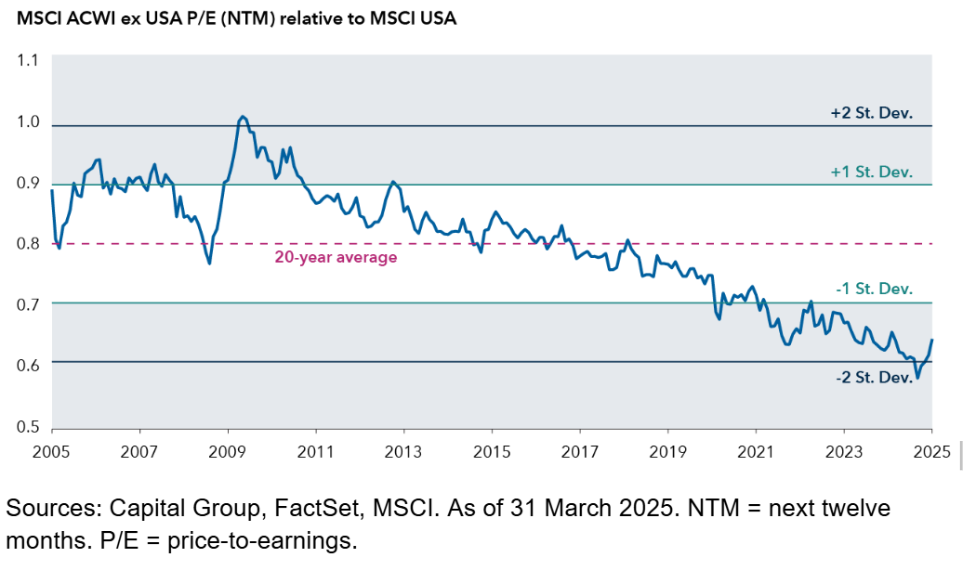

The expert indicates that the starting valuations of non-U.S. markets remain “much lower than in the United States.” He provides some data: on one hand, the MSCI ACWI ex-USA trades at 13 times forward 12-month earnings, while the MSCI EAFE (international developed) trades at 14 times, both near their 10-year averages and at a significant discount compared to the S&P 500, which trades at 20 times earnings.

Non-U.S. stocks are trading near their lowest level in 20 years relative to U.S. stocks.