The market for active bond ETFs has grown exponentially in recent years, with net investment inflows exceeding $270 billion in just the past two years. Total assets under management reached $490 billion at the end of January 2026, and active ETFs now represent one fifth of the total assets in bond ETFs. Firms have responded to this growing demand by launching more than 270 strategies over the past two years, and these new entrants account for a quarter of all active bond ETFs, according to a Morningstar study.

Given this “dizzying” pace of development, an investor may wonder whether an active bond ETF has a place in their portfolio. At Morningstar, they believe that while the investment merits of each ETF vary, “there are some important considerations that should guide investors in the right direction.”

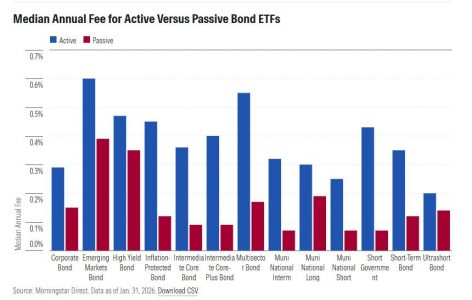

The Price of Active Management

Active bond ETFs carry a premium compared with their passive counterparts: their average annual fee of 0.45% is higher than the 0.24% average for passive bond ETFs. Active managers also tend to charge more in riskier categories: the average fees for emerging markets or multisector active bond ETFs are nearly double those of corporate or ultrashort bond ETFs. “While these complex segments of the market offer greater upside potential, they can also expose investors to higher volatility and sharper drawdowns. A higher price does not always translate into greater management skill,” the firm notes.

In contrast, the difference in fees between active and passive ETFs is not uniform across all categories. Managing a bond fund is a costly task in riskier and more nuanced categories, such as emerging markets or high-yield bonds. As a result, investors do not face a significant increase in costs in these cases if they choose active management, as Morningstar explains.

On the other hand, cost compression among passive ETFs in safer and more straightforward categories, such as intermediate core and intermediate core-plus, makes it difficult for active managers to compete on fees. “Active ETFs in these categories must offer an even greater edge for the investment to be worthwhile,” the firm concludes.

More Risk, More Reward?

According to Morningstar’s Active/Passive Barometer, active bond managers are more likely to outperform their passive counterparts than active equity managers. Although their success rate hovers around 50% over longer periods, active bond managers have more tools at their disposal to generate excess returns.

A recent analysis by Eric Jacobson and Maciej Kowara, of Morningstar, explains why active bond managers find it easier to achieve better results. The study notes that indexed funds face limitations that active managers do not, and that they can gain an advantage simply by including asset subclasses that fall outside the scope of the indexes or by tilting toward certain risks, provided this is done prudently.

To keep an index investable, most providers limit the range to the most liquid, or most heavily traded, part of the bond market and exclude more complex securities, such as floating-rate bonds or convertibles. Market value weighting also tilts index portfolios toward the higher-quality segments of the market, typically Treasury bonds or higher-rated corporate bonds.

In many categories, active managers’ ability to achieve better results lies in their flexibility to take on more risk than an indexed portfolio typically allows. While they may benefit more when riskier bonds rebound, this can also cause many active portfolios to lag behind their indexed counterparts during stressed markets.

So far, the average active corporate bond ETF has remained close to its benchmark because managers have limited room to maneuver in this largely investment-grade category. However, in categories where managers have a broader range of asset subclasses to choose from—such as intermediate core and short-term—and greater flexibility in terms of credit risk—for example, intermediate core-plus—the situation is slightly different: the sharp decline in March 2020 and the subsequent rebounds during the 2021 recovery point to the higher levels of risk these managers take to outperform their benchmarks, according to the Morningstar study.

“For a conservative portfolio that uses bonds as a counterbalance, these sharp swings are likely too risky to justify their potential returns,” Morningstar notes, adding that investors can use a “well-constructed” active portfolio to achieve “greater benefits in these categories, but they must understand that these returns come with additional risk.” Therefore, active bond ETFs require “more frequent reviews and more thorough due diligence compared with many passive bond ETFs.”

The Advantage of Manager Selection

The firm notes that some segments of the bond market are better suited to active management: high-yield bonds and emerging markets bonds are two of them, “given their relatively lower liquidity and higher credit risk.”

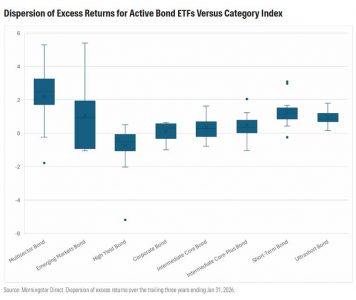

However, choosing an active ETF in any of these categories does not guarantee success. The greater margin for error also makes it harder for active managers to avoid pitfalls. The chart shows the dispersion of excess returns of active bond ETFs relative to their respective category index over the past three years. “The range is narrow for relatively safer categories, such as ultrashort- or short-term bonds, but widens dramatically for emerging markets or multisector bond ETFs,” the firm notes.

The outperformance of active bond ETFs often comes with higher risk. A good active manager can ensure that investors are adequately compensated for it. Choosing an experienced management team with a consistent track record, especially during periods of market stress, should be beneficial for investors.