According to Detlef Glow, Head of EMEA research at Lipper, assets under management in the European mutual fund industry enjoyed net inflows of €2.3 billion into long-term mutual funds for November.

While Ireland (+€20.4 bn), France (+€5.2 bn), Luxembourg (+€3.8 bn), Germany (+€2.1 bn), and the United Kingdom (+€1.3 bn) were the single fund markets with the highest net inflows for November, Switzerland (-€2.2 bn), Norway (-€2.2 bn), and Spain (-€1.5 bn) stood on the other side.

In terms of asset classes, Equity funds with €5.2 billion enjoyed the highest net inflows for the month, followed by alternative UCITS products with €2.8 billion and mixed-asset funds with €2 billion. Meanwhile, bond Funds, which in October had the highest net inflows, suffered during November from the highest net outflows, loosing €7.8 billion.

Money market products enjoyed net inflows of €23 billion for November.

The best selling sectors within the segment of long-term mutual funds in November where:

· Equity Europe with €2.1 billion

· Absolute Return EUR Medium Term with €1.9 billion

· Bond EUR Corporates with €1.8 billion

Amongst ETF promoters, Blackrock’s iShares with €5.46 billion, Goldman Sachs with €5.42 billion and Aviva €4.81 billion, were the best selling ones.

The best selling ETF for November was the SLI Global SICAV Global Absolute Return Strategies A EUR, which accounted for net inflows of €966.26 million

Federal Street Advisors, an independent investment consultant and wealth management firm for individuals, families and nonprofit organizations, and Pathstone Family Office, a Multi Family Office offering in house expertise in investments, tax planning and compliance, estate planning, family education, and philanthropy jointly announced today that Federal Street has merged with Pathstone to create Pathstone Federal Street, a wealth advisory firm with enhanced capabilities to provide truly independent advice and services to both high-net-worth and institutional clients.

“This marks an exciting new chapter for us – it expands our capabilities and offerings in wealth management,” said Steve Braverman Co-CEO of Pathstone Family Office and the new Pathstone Federal Street. “We feel this combination of talents, founded on a strong mutual heritage of multigenerational stewardship and independent advice, will offer broader perspective, deeper services and a robust organization built for the long-term.”

“Pathstone Federal Street integrates and leverages each organization’s strengths and expertise,” John LaPann, Founder of Federal Street Advisors and Chairman of the new organization. “Pathstone combines its solid legacy in providing integrated family office services, state-of-the-art technology and operating efficiencies with Federal Street’s long-respected internal manager research, due diligence process, and leadership in sustainable and impact investing.”

“The combination of the two firms will allow many more opportunities for all our clients as it will leverage the talents of our now 65 employees across our 4 offices serving 190 clients representing in excess of $6.5 Billion in total advisory assets,” said Allan Zachariah, Co-CEO of Pathstone Family Office and the new Pathstone Federal Street. “Our partnership and expanded services provide significant opportunities for our employees to grow and uniquely contribute to the individual outcome of each client.”

Matthew Fleissig of Pathstone Family Office will become President of the new organization, joined by Eric Godes and Jennifer Murtie of Federal Street Advisors who will share the Chief Operating Officer title at Pathstone Federal Street. Jennifer will also serve as the firm’s Chief Marketing Officer. Kristin Fafard of Federal Street will continue as Chief Investment Officer for the combined organization. Matthew Sher will serve as the new firm’s Chief Compliance Officer and Chief Technology Officer. In addition, Pathstone Federal Street is proud to name new Managing Directors: Daniel Gross, Kelly Maregni, Janet Mertz, Mark Peters, and Charles Walsh.

CC-BY-SA-2.0, FlickrPhoto: AlfonsoBenayas, Flickr, Creative Commons and I will treat emerging markets as emerging (yet again), among them. UBS AM: Market Resolutions for 2016

The latest edition of UBS Asset Management’s Economist Insights, authored by Joshua McCallum and Gianluca Moretti, speaks about market resolutions for 2016. Joshua has been Senior Economist with UBS Asset Management’s Fixed Income area since 2005, and prior to this he was a macroeconomist at the UK Treasury. Gianluca joined the firm in 2010 from the central bank of Italy.

Based on the experiences of 2015, they once again suggest some New Year’s resolutions for the market. Among others:

I must behave like an adult if I want central banks to treat me like an adult;

I must acknowledge that lower potential growth mean searlier rate hikes;

I will start the year with more humble expectations of growth;

I will treat emerging markets as emerging (yet again);

I will think of Greece as a holiday destination, rather than as destroyer of the Euro;

I will recognize that the global economy is diverging.

You can download the full document in the following link.

Foto: Rachel Gardner. Cerrada la compra de Arden Asset Management por parte de Aberdeen

Aberdeen Asset Management acquired hedge fund solutions provider Arden Asset Management on December 31, 2015.

The combined hedge fund solutions team located in London and New York specializes in creating and managing multi-manager portfolios with expertise in hedge fund manager research, selection, monitoring/oversight and portfolio management. With $10.3 billion in assets under management, the team provides commingled funds, customized portfolios, mutual funds and advisory services to a global, blue-chip client base of individual and institutional investors.

This acquisition grows Aberdeen’s global alternatives platform, which encompasses multi-manager research, selection and portfolio management for hedge-fund strategies, private equity and debt, property and other real asset investments, along with direct investments in infrastructure projects. Aberdeen can now offer its clients access and exposure to a universe of high-quality alternative investments, covering liquid strategies, private markets and real assets.

Andrew McCaffery, Global Head of Alternatives at Aberdeen Asset Management, comments:”We are very pleased to have closed on the acquisition of Arden Asset Management LLC. Our excitement about the potential of the combined, integrated platform continues to grow, enhanced by the very encouraging feedback we have received from clients since signing the agreement. We continue to focus upon the opportunity presented by investors’ increasing demand for high-quality research, combined with effective portfolio construction and management, in an effort to generate sustainable returns for their hedge fund portfolios. The development of liquid-alternative portfolios and products, built off our broader hedge fund solutions platform, is an area that we are increasingly confident will grow in 2016 and beyond.”

It is anticipated that during the first quarter of 2016, Arden’s Alternative Strategies Fund and Arden’s Alternative Strategies II will be reorganized into newly created series of Aberdeen Funds, Aberdeen Multi-Manager Alternative Strategies Fund and Aberdeen Multi-Manager Alternative Strategies Fund II, using investment strategies that are substantially similar to those of the Arden Funds.

Aberdeen’s alternatives division has more than $21 billion of assets under management as of September 30, 2015. This coupled with Arden will bring the group’s alternatives assets to more than $31 billion. Aberdeen manages more than $429.7 billion on behalf of institutional and private investors.

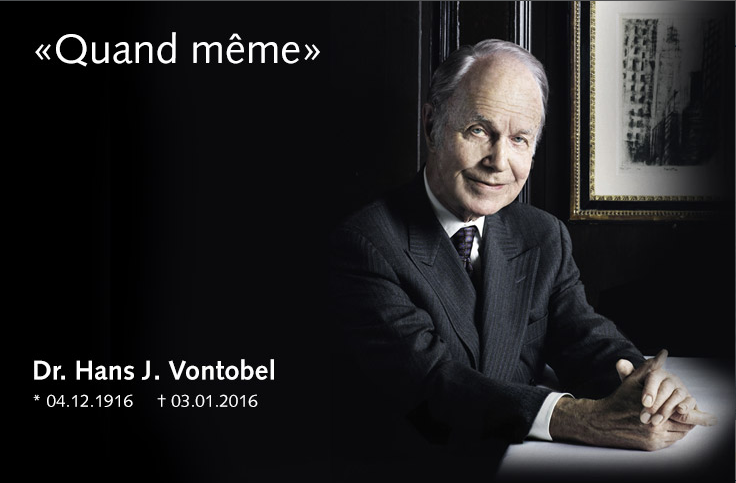

CC-BY-SA-2.0, Flickr. Hans Vontobel muere con 100 años

Dr. Hans Vontobel, Honorary Chairman of Vontobel Holding AG, died on January 3rd 2016 at the age of 100. According to Vontobel’s statement “The employees of Vontobel are mourning an exceptional man, with whom they all felt a special bond.”

Hans Vontobel joined the then J. Vontobel & Co. in 1943, and under his leadership it became one of the leading internationally active investment advisory firms. He took over as Chairman of the Board of Directors in 1981, and had served as Honorary Chairman since 1991. For many years, he was the Chairman of the Zurich Stock Exchange, a member of the Board of Directors of the Swiss Bankers Association and the Neue Zürcher Zeitung, and Chairman of the German-Swiss Chamber of Commerce.

A father of two daughters and a son, he was not only a passionate banker, he was also an author and publicist. His credo “quand même” was immortalized in his his last Blog entry, He had an acute sense of civic awareness, and was a keen observer of his time. Hislife was greatly influenced by his love of nature, and by his commitment to a wide range of charitable causes. As a philanthropist he will be remembered, among other things, for having set up the Vontobel Foundation, the Kreatives Alter Foundation, and the Lyra Foundation, which supports highly gifted young musicians.

As a prudent and far-sighted entrepreneur, he soon put his stamp on the house and also addressed his own transience with the transfer of significant stakes to the Vontobel Foundation and the family-controlled Vontrust AG. “Ensuring that the company would remain independent after his death was a matter of great importance to him,” stated Vontobel.

Herbert J. Scheidt, Chairman of the Board of Directors of Vontobel Holding AG said: “Hans Vontobel was one of the most important bankers in our country, but beyond that he was a convinced humanist, who put people at the heart of everything he did. He will remain an example to us all, as a source of considered, far-sighted advice, and with his cosmopolitan outlook and thirst for knowledge. The Board of Directors, Group Executive Management and the employees will carry on his work and his values with a due sense of responsibility, resolve and commitment. All the employees send their heartfelt condolences to the family.”

WIN/Gallup International, the world’s leading association in market research and polling, has published its 39th End of Year Survey exploring the outlook, expectations, views and beliefs of 66,040 people from 68 countries across the globe. Below some of the most revealing findings:

66% of the world say that they feel happy about their lives, down from 70% in 2014; 23% are neither happy nor unhappy, and 10% feel unhappy about their lives

Net happiness (happy minus unhappy) globally is 56%

Colombia is the happiest country in the world (85% net happiness), followed by Fiji, Saudi Arabia, Azerbaijan and Vietnam while Iraq is the least happy for the second year in a row (-12% net happiness)

45% of the world is optimistic about the economic outlook for 2016; 22% are pessimistic and 28% believe the economy will remain the same

The most optimistic country about economic prosperity in 2016 is Nigeria (61% net optimistic), followed by Bangladesh, China and Vietnam. In contrast, Greece is the most pessimistic (-65% net optimistic) country

A little over 1 person out of 2 (54%) believes 2016 will be better than 2015, 16% think it will be worse and 24% believe 2016 will be the same as 2015

Bangladesh, China, Nigeria, Fiji and Morocco are the most hopeful nations, while Italy is the least hopeful

A happy world in 2015

As 2015 comes to an end, 66% of respondents to the WIN/Gallup International survey say that they are happy, down slightly from 70% in 2014. Of the 66,040 people surveyed, 10% said that they were unhappy, up 4% from 2014. Overall that means that the world is 56% net happy (happiness minus unhappiness). In 2015 the net happiest country in the world is Colombia (85%), in stark contrast the world’s unhappiest country is Iraq at -12% net happiness.

Economic Optimism high across the world

The study shows that 45% of the world is optimistic for the economic outlook in 2016 over double (22%) of those who are pessimistic. It’s perhaps unsurprising that Greece is the most pessimistic (-65% net optimistic) country given their current perilous financial position. The most optimistic nation when it comes to the economy is Nigeria (61% net optimism). When it comes to a demographic breakdown young people prove to be considerably more optimistic than older generations with 31% net optimistic for the under 34s compared to just 13% for the over 55s.

Hope high amongst aspiring nations

As part of their analysis WIN/Gallup International has grouped the world into three tiers: Prosperous (the G7); Emerging (G20 excluding the original G7) and Aspiring (all others) nations. Whilst there is huge disparity in income levels across these three tiers, the level of net happiness across all three (Prosperous 42%, Emerging 59% and Aspiring 54%) is notably high. However, the findings on hope and economic optimism vary markedly across the tiers. According to the global poll, Prosperous nations display the least hope and economic optimism with 6% and -16% respectively; to the contrary Emerging nations are very hopeful about the future and far more optimistic about the economic outlook at 50% and 36% meanwhile the Aspiring nations sit between the two on hope (29%) and economic optimism (16%).

CC-BY-SA-2.0, FlickrFoto: nathanmac87

. Beechwood Acquires Old Mutual Bermuda

Beechwood Bermudaannounced the completion of its acquisition of Old Mutual (Bermuda), a Bermuda based provider of insurance and investment products with over $1 billion in assets, which closed for new business in 2009. Beechwood, one of the largest providers of international investment plans, now has over $2 billion in total assets and is featured on the platforms of over 100 banks and brokerage firms around the world.

The transaction, which closed on December 31, 2015, provides for the continuation of service support by Old Mutual for the OMB products over the next three years, supplemented by additional support from Beechwood’s growing wealth management business. As part of the arrangement, Old Mutual will reinsure certain policy guarantees until they mature in 2017 and 2018. Given the continuity of resources, no disruption to client service is anticipated.

“This transaction offers a unique opportunity to strengthen our position as a global leader and demonstrates our dedication to providing innovative financial solutions for international investors,” said Mark Feuer, Chief Executive Officer of Beechwood. “Our scale and resources will allow us to continue to meet and further develop client demand for our products for years to come.”

Over the next several weeks, Beechwood will be contacting OMB’s distribution partners to discuss the transition and introduce Beechwood’s Accumulator Plus and Escalator Plus investment plans, which offer attractive rates and unique investment features such as principal protection guarantees. David Lessing, Executive Vice President of Products and Services at Beechwood, noted, “The growing client demand for the Beechwood products reinforces our decision to make a significant commitment to this business in support of our distribution partners and their financial advisors.”

Financial terms of the transaction were not disclosed. Certain regulatory approvals for the transfer of future policy administration arrangements are expected by the end of Q1 2016.

CC-BY-SA-2.0, FlickrEmmanuel Bourdeix, director general de Seeyond y co director de inversiones de Natixis AM. Foto cedida. "Solo una cosa es segura a corto plazo: la incertidumbre está aquí para quedarse… hasta que los datos económicos arrojen luz sobre los fundamentales"

Emmanuel Bourdeix, General Director at Seeyond and Co-CIO at Natixis AM, explains in this interview with Funds Society his view about volatility and the trends we will see in the next months.

Does the volatility has come back to stay? Will it increase in the coming months?

Over 2015 and late 2014, we have observed a period of heightened volatility spikes. Now that the Fed starts normalising its rates after several years of accommodative monetary policy, the beginning of 2016 should probably look very much like the end of 2015, in the sense that market participants will keep on taking a close look at economic data releases to convince themselves that the Fed’s decision was the good one… or not.

More precisely, should strong economic data be published, investors might finally wonder whether the Fed is not behind the curve. Due to this market psychology of “good news is bad news”, we might witness volatility spikes in an environment of robust and favourable fundamentals. Indeed, higher US interest rates as well as an expensive U.S. Dollar could weaken certain market segments, such as emerging markets and U.S. high yield which, in turn, would be a source of contagion and potential increased market volatility.

Conversely, should weak data be released in the coming months on the back of a sustained deterioration of the manufacturing sector in the US, it would mean that the U.S. economy might find itself at the end of an economic cycle with a risk of a recession and that the Fed’s action was inappropriate. To that extent, volatility spikes would occur, with the risk that they become so frequent that it leads over the medium term to a structural adjustment of volatility to the upside.In a nutshell, we believe only one thing is sure over the short term, uncertainty is here to stay… until economic data shed some light on the underlying fundamentals.

Would volatility management be an investment key theme for 2016?

Definitely, volatility will remain a key driver in 2016 in such an uncertain environment. Specialised in extracting value from risk, Seeyond has developed different strategies that can make the most of the current period of low visibility and beyond.For instance, Seeyond’s Minimum Variance strategy offers investors a full exposure to equities with an average risk reduction of 30%. By investing in stocks that display not only low volatilities but also low correlations between each other, we strive to build portfolios that reduces volatility to the lowest, however not at the expense of long term performance: as a matter of fact, academic research, but also empirical observations, suggest that low volatility stocks tend to outperform their peers over long time horizons. This strategy typically fits uncertain environments, like the one we forecast for the coming months.

Beyond, once the economic background gets clearer, be it on the upside or the downside, Seeyond’s multi-asset conservative growth strategy is able to drastically adapt its asset allocation, avoiding markets that would be negatively impacted by the economic environment. Investing in each market independently, the investment process has no structural bias to any asset class in order to provide investors with a robust total return strategy. It combines volatility metrics with fundamentals and momentum indicators, adjusting market views to the underlying risk. To that extent, Seeyond’s multi-asset allocation and minimum variance strategies are complementary and are expected to be a good fit to next year’s environment.

Which are the investment opportunities in the current scenario? Is it more efficient to seek for protection against volatility or to try to take advantage from it?

The arbitrage between seeking protection and exploiting volatility depends on client needs. Intuitively, the cost of holding protection, that is to say the cost of carrying volatility, tends to be expensive in a normalized environment. Investors have to ask themselves if they are not better off selling an overpriced asset. However as structural market crises materialize, investors are potentially compensated for carrying volatility as the crisis unfolds. Volatility has therefore the potential to generate alpha which sets it apart from risk off assets such as cash. This duality is really the corner stone of Seeyond’s investment philosophy around volatility: by looking at the effective cost of carry of volatility instead of its facial level, our strategy is by construction long volatility during a systemic crisis, striving to generate significant value when risk assets are out of favour ; it is short volatility the remainder of the time, striving to provide an additional alpha stream to the overall portfolio.

2016 feels like we are in front of an heightened uncertainty and the outcome from the scenarios we have identified are miles apart. In that context, our firm belief is that allocating to volatility actively has the potential to present investors with the ability to adapt to a favourable scenario while maintaining the ability to generate value should a storm set in.

In this environment how do Seeyond funds help the investors to balance the risk/return equation in their portfolios?

Depending on client needs, balancing risk/return profiles of portfolios can be done on different levels:

– Downside risk protection though structured products (full or partial): investors have a formal protection of their capital whilst being able to participate partially in financial markets’ potential.

– Equity volatility reduction through minimum variance strategies which offer full long-only equity exposure, whilst reducing volatility considerably.

– Risk/return optimisation through total return strategies offering multi asset exposure (equities, fixed income, currencies) based on risk-adjusted allocation

– Active volatility management by investing in equity volatility, an asset class which generates uncorrelated returns to equity markets and thus, significantly enhances the diversification profile of an asset allocation.

It is the 5th anniversary of the Europe Min Variance fund. How has the performance been since the launching?

Since inception and as of end of Sept 2015, Seeyond Europe Minvariance has outperformed its benchmark by more than 15% and reduced volatility by around 30% vs the MSCI Europe NR EUR over the period. Despite varying market configurations, and strong performance shifts encountered over the last 5 years due to various events (among which eurozone debt crisis, FED tapering and European QE, China’s “Black Monday”, etc.), the strategy succeeded in generating consistent returns proving the relevance of its core foundation: focusing on managing the overall level of portfolio volatility does indeed benefit from superior long term risk-adjusted returns. The fund also demonstrated its ability to adapt over different market environments through its reactive allocation from a geographic or industry point of view.

How does the other fund, which invests in derivatives, work? What kind of investors profile and portfolios is it recommended for?

Seeyond’s equity volatility strategy provides investors with a diversification tool that can be used as part of their allocation. It invests in equity volatility actively through listed and liquid instruments, and aims to provide diversification during structural crises. During normalised market conditions, we strive to harvest the equity volatility risk premium in order to generate a moderate total return.

Though this strategy hasn’t had so far the opportunity to experiment a strategic bear market (comparable to 2008 or 2011) in order to demonstrate its ability to generate a decent crisis alpha, it hasn’t exhibited any significant cost of opportunity in comparison with money market investments since its inception in 2012. Therefore, we would recommend this strategy to investors who still hold large portions of cash in their asset allocation: they could arbitrage part of this cash into Seeyond’s equity volatility strategy without any substantial cost while integrating a source of active diversification, should equities enter an undesired bear market.

Global asset manager Legg Mason Inc is in exclusive talks to buy a majority stake in real estate investment manager Clarion Partners LLC in a deal valuing the company at about US$ 850 million, according to Bloomberg. Clarion, which is based in New York and invests in office and retail related real estate, has about US$ 38 billion in assets under management, according to its website.

Under the terms being discussed, the asset manager would buy 80% of the firm from Lightyear Capital, while New York-based Clarion’s current management, headed by Chairman and Chief Executive Officer Stephen Furnary, will retain 20%. Back in November, Reuters reported in that private equity firm Lightyear Capital was looking to sell its majority stake in Clarion Partners LLC for around US$ 800 million. A deal could be announced as early as this month.

Lightyear helped Clarion’s management buy the firm from its previous partner, Dutch financial services company ING Groep NV in 2011. When that deal was struck, the price and ownership structure were not disclosed. Neither Legg Mason, Lightyear or Clarion have made any comments on this matter.

CC-BY-SA-2.0, FlickrPhoto: Chuck Coker

. House Prices Continue a Slow Recovery, IMF Says

Globally, house prices continue a slow recovery, according to The Global House Price Index, released by IMF in December. The Index, an equally weighted average of real house prices in nearly 60 countries, inched up slowly during the past two years but has not yet returned to pre-crisis levels.

If prices went up in The United States, Colombia and Spain, in Brazil, Chile, Mexico, and Peru they decreased. The areas with the biggest growth were Qatar, Ireland and Hong Kong while the biggest decreases took place in Ucraine, Russia and Latvia.

As noted in previous quarterly reports, the overall index conceals divergent patterns: over the past year, house prices rose in two-thirds of the countries included in the index and fell in the other one-third.

Credit growth has been strong in many countries. As noted in July’s quarterly report, house prices and credit growth have gone hand-in-hand over the past five years. However, credit growth is not the only predictor for the extent of house price growth; several other factors appear to be at play. While in Brazil credit and prices went down, and in Colombia and The United States both grew, in Spain prices grew while credit decreased, and in Mexico priced did not while credit did.

For OECD countries, house prices have grown faster than incomes and rents in almost half of the countries.House price-to income and house price-to-rent ratios are highly correlated, as documented in the previous quarterly report.