Although global markets have been marked by turbulence this year, Colombian pension funds posted double-digit returns during the first quarter. That is the picture reflected in figures recently published by the pension fund managers’ trade association, Asofondos.

In a statement, the organization—which represents the AFPs Colfondos, Porvenir, Protección, and Skandia—reported that pension fund assets closed March 2025 with a total value of 467.7 trillion Colombian pesos (about USD 109.89 billion). This represents 11% growth compared to the 421.3 trillion pesos (USD 99 billion) reported in March 2024.

“This growth reflects not only returns (which totaled 38 trillion pesos over the past 12 months) but also that contributions exceeded withdrawals by 8 trillion pesos,” said Andrés Velasco, president of Asofondos, in the release.

The association also highlighted the performance of pension savings. Between January and March, returns reached 250 billion pesos (approximately USD 59 million).

“This means that, had there been no additional contributions or withdrawals, the fund would still have grown by 250 billion pesos,” the executive explained.

Velasco emphasized that these results come amid a backdrop of uncertainty.

“So far, 2025 has been—and will continue to be—a very volatile, uncertain, and challenging year for financial and capital markets,” he warned.

In this context, the economist stressed the importance of portfolio diversification in investment management.

“In the first quarter, we saw strong gains on the Colombian Stock Exchange, as well as in other Latin American and European markets, while U.S. stock indexes saw declines. Not putting all our eggs in one basket allowed for a consolidated positive result.”

Investment Placement Group (IPG) premieres new offices in Miami. They are located in Brickell City Tower, in the heart of Miami’s new financial center, across from Brickell City Center.

“We are very happy and excited to see our Miami group grow,” said Rocio Harb, director of the Miami office and branch manager at IPG. “Very grateful to the partners and the San Diego team for their support and generosity,” she added.

The company’s headquarters are located in that California city.

For his part, Adolfo Gonzalez-Rubio G, Head of Wealth Management at IPG, said that “our new office is a testament to the hard work of our team and our vision for the future. This space will allow us to scale operations and continue attracting top talent and advisors.” He then added: “we want to offer better value to our clients as we embark on the next chapter of growth.”

The Miami office of IPG currently has 5 of the firm’s 15 advisors, within a total team of 70 people.

The company, founded in 1983, grew from being a California broker-dealer to becoming a multigenerational and diversified wealth management firm with expert financial professionals serving both domestic and international clients.

A large part of Investment Placement Group’s portfolio is offshore and is composed of Latin American clients. One of the goals of its hiring campaign is to attract advisors to help diversify its client base.

IPG has offices in Arizona, California, and Florida, and also has an affiliated investment advisory company in Mexico to serve the local market. Additionally, it has an institutional commercial office in Argentina.

Currently, the group oversees more than $5 billion in assets and works with multiple renowned custodians for the U.S. offshore market.

Goldman Sachs Asset Management launches in Europe a range of actively managed equity exchange-traded funds (ETFs). The Goldman Sachs Alpha Enhanced US Equity Active UCITS ETF (GQUS) is the first of the five funds to be launched; moreover, the ETF is listed on the London Stock Exchange and the Deutsche Börse, with other European exchanges to follow, and will offer exposure to U.S. equities. The four following funds will offer access to global, European, Japanese, and emerging markets equity.

The funds are based on the capabilities of the Quantitative Investment Strategies (QIS) team of Goldman Sachs Asset Management, which represents more than 35 years of investment experience and includes more than 80 professionals worldwide, with over $125 billion in assets under supervision as of December 31, 2024. The QIS team combines various data sources to better understand the growth prospects of companies across different sectors and geographic areas.

The launch comes after the recent entry of Goldman Sachs Asset Management into active ETFs in EMEA with several fixed income funds, expanding the product range and underscoring the firm’s commitment to offering its investment capabilities through the ETF wrapper.

Regarding these launches, Hilary Lopez, Head of Third Party Wealth Business for EMEA at Goldman Sachs Asset Management, said: “Clients are increasingly seeking top-tier active capabilities, with the control and convenience of ETFs. Following the launch of our flagship active fixed income blocks, we are leveraging our proven quantitative investment strategies to expand the range into equities. Our goal is to offer transparency and flexibility while helping investors navigate market turbulence and the changing dynamics of markets.”

For her part, Hania Schmidt, Head of Quantitative Investment Strategies in EMEA at Goldman Sachs Asset Management, commented: “Our data-driven approach is based on the experience, infrastructure, and knowledge of Goldman Sachs, in search of an informational edge to generate differentiated returns and outperform the market.”

Goldman Sachs Asset Management currently manages 55 ETF strategies globally, representing more than $38.7 billion in assets as of March 31, 2025. The TER of the Goldman Sachs Alpha Enhanced US Equity Active UCITS ETF (GQUS) is 0.20%.

Capital Dynamics, independent global asset manager, has announced the appointment of Susan Giacin, current Senior Managing Director and Head of Sales for the Americas, as Global Head of Sales. In addition, she will join the company’s Executive Committee, where she will contribute to the strategic direction of the firm.

According to the firm, in her new role, she will lead the firm’s global fundraising efforts and drive growth across the full range of Capital Dynamics investment strategies, including private equity and clean energy. Giacin will report to Martin Hahn, Chief Executive Officer and Chairman of the Executive Committee, and will be based in the New York office.

Giacin brings more than 25 years of experience in creating, developing, and marketing investment solutions for institutional and wealth management clients. Since joining Capital Dynamics in 2017, she has played a key role in expanding the firm’s investor base in the United States and in strengthening client relationships, and she is recognized as an industry leader in creating accessible private market investment solutions.

“This appointment recognizes Susan’s extraordinary leadership and the impact she has had on the company. Her success in the U.S. market has been a key factor in the expansion of our firm, and we are confident that in her new role, she will help further advance Capital Dynamics’ investment solutions internationally. With her deep market knowledge, client-oriented approach, and ability to collaborate with our globally integrated team, she will bring great value to our already successful international fundraising team,” highlighted Martin Hahn, Chief Executive Officer of Capital Dynamics.

For her part, Susan Giacin, now as Global Head of Sales of Capital Dynamics, stated: “I am delighted to take on this role. Capital Dynamics enjoys a great reputation for delivering innovative, high-quality solutions to investors. As we intensify our global fundraising efforts, I look forward to working with my colleagues to further strengthen our relationships with existing and new limited partners (LPs), and to support our clients’ evolving needs in this rapidly changing investment landscape.”

In a week marked by the release of macro data—including the first-quarter GDP in the U.S.—and the completion of the first 100 days of the Trump Administration, the keyword is confidence. According to international firms in the sector, markets will look for signs and proof of long-term stabilization, such as trade agreements or the action of central banks, to regain confidence. On that path, investors must be prepared to identify opportunities, but also to seek safe-haven assets, as volatility is expected to remain high.

For Benoit Anne, Senior Managing Director of the Strategy and Insights Group at MFS Investment Management, the starting point of all this uncertainty and volatility has been a crisis of credibility in economic policies. “Policy credibility is important and no country is above this basic market law. Apparently, not even the United States. In our view, the most concerning signal seems to come from the U.S. bond market. Although the deterioration of macroeconomic fundamentals should, in principle, have pushed bond yields down, what is happening now is the opposite. In the face of increased risk aversion, U.S. bonds currently do not appear to offer the protection they once did, leading to upward pressure on yields. To be clear, it is still too early to know whether this confidence shock will persist for a long time. Given the extreme level of uncertainty, we believe the market backdrop may change radically in a relatively short time,” acknowledges Anne.

He explains that this “confidence shock” is quite rare and occurs due to a “triangular market correction,” meaning that massive sell-offs occur simultaneously in a country’s Treasury bond market, equity market, and currency market. He notes that historically, this unusual market phenomenon has been observed mainly in emerging markets, such as during episodic financial crises in Brazil or Turkey in the 1990s or 2000s. “However, it is not a phenomenon exclusive to emerging markets. We all probably remember the episode of the UK’s mini-financial crisis in October 2022,” he adds.

Implications for the Investor

In this context, Lombard Odier acknowledges that it has taken advantage of the market downturn to rebalance portfolios and restore strategic equity weightings in multi-asset portfolios. “We continue to overweight fixed income. We believe our base case of slower growth, but without a recession, with interest rate cuts from central banks supports this tactical positioning. We are ready to make further adjustments as the situation evolves, following the steps outlined below,” they explain.

Based on their experience, the question investors should ask is what the path is to restore confidence. In their view, confidence tends to be restored in the markets through the initial attempts to buy assets at low prices. “While equity markets rebounded, other parts of financial markets have remained volatile, preventing this behavior from taking hold. It would be encouraging to see more buying attempts by investors at these levels. That would support other segments of the markets,” they point out.

For Michaël Lok, Group CIO and Co-CEO of UBP, “it is likely that investors will have to continue relying on strategies focused on risk management until markets better absorb the new landscape of growth, inflation, and geopolitics that is taking shape. Tactical risk management has helped us endure one of the biggest market declines since 2020. Gold and cash remain reliable safe havens.”

When discussing more reliable assets, MFS IM adds that, leaving aside the U.S. bond market, the best fixed income results will likely be found in asset classes with low duration and low credit risk, along with low correlation to the U.S. “With this in mind, the Global Agg index was the best refuge, with a positive return of 0.83%. The EUR IG also showed great resilience, with a marginally negative return (-0.20%). On the other hand, it is worth noting that local emerging market debt performed well during this period, favored by the weakness of the dollar. The local EM debt index delivered a return of 0.72%. Beyond fixed income, some currencies benefited significantly from the widespread weakness of the dollar. The Swiss franc has risen nearly 8% since April 1, reaffirming its status as a defensive asset. And gold has gained nearly 3.5% during this time,” argues Anne.

Finally, Duncan Lamont, Head of Strategic Research at Schroders, does not believe that investors should close the door on equities. According to Lamont, the market downturn means that the cash you’re considering investing will go further. “Valuations have come down and, in the case of non-U.S. markets, are cheap compared to history. Not too much, but bargains can be found. Even the U.S., which for so long has been an outlier, is quickly converging toward more neutral valuations compared to history,” he notes.

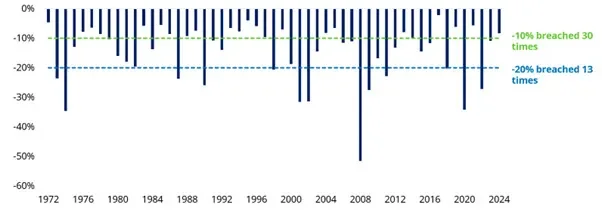

Calm: Declines Are Not Unusual

Lamont, Head of Strategic Research at Schroders, reminds us that downturns in equity markets are normal and part of the financial system’s mechanics. In fact, he points out that in global equity markets (represented by the MSCI World Index), 10% drops occurred in 30 of the 53 calendar years prior to 2025. In the past decade, this includes 2015, 2016, 2018, 2020, 2022, and 2023. Meanwhile, more significant declines of 20% occurred in 13 of the 52 years—once every four years on average. But if it happens this year, it would make it four times in the last eight years: in 2018, 2020, and 2022.

“That markets fall is nothing new, but that doesn’t prevent the feeling of panic from taking hold of investors. The stock market falls by 20% once every four years on average, and by 10% in most years. It’s easy to forget this. Even if you’re an experienced investor, how much comfort does that bring you when you’re in the thick of it? The simple reality is that the stock market has tremendous power to help grow wealth over the long term, but short-term volatility and the risk of drawdowns are the toll to pay,” points out Lamont.

The reading made by Union Bancaire Privée (UBP) is that markets appear to be focusing on weaker growth (the first impact) and a “transitory” rise in inflation, as described by Fed Chair Jerome Powell in his March press conference.

“In fact, 5-year inflation expectations are now at their lowest level in comparison with their 2-year counterparts since 1980 (outside of the initial deflationary shock of the 2020 global pandemic), which suggests that markets are not focusing on medium-term inflation concerns and instead, U.S. Treasury yields are closer to pricing in a recessionary environment—that is, weak growth and weak inflation in the medium term,” they point out in their April “House View” report, titled “Navigating Market Instability.”

In fact, UBP highlights that despite equity market declines, global equity valuations have returned to nearly historical averages.

“This suggests that markets are no longer discounting a repeat of the economic and corporate earnings boom centered in the U.S. in 2017, which occurred in the first year of Trump’s term. Instead, they reflect expectations of more moderate, though still favorable, economic and earnings growth. However, these more moderate expectations do not reach the recessionary scenario that bond markets are increasingly pricing in,” they indicate.

This is the question Amundi aimed to address in its latest global report, and the answer it obtained is clear: 77% of respondents invest at least part of their portfolio through a digital platform or app. However, what’s most relevant are the trends identified, ranging from holding investments on digital platforms to using digital sources of information and advice for decision-making.

According to the asset manager, that 77% demonstrates that digital investing is not just for younger investors, gaining ground across all age groups, as 68% of people over 50 globally make digital investments. This figure increases among younger investors, suggesting that the number of investors with digital holdings will grow as younger generations age. Furthermore, the document shows a disparity among countries; with Finnish (95%), Brazilian (89%), Swedish (89%), and South Korean (89%) investors adopting digital methods to a greater extent than their counterparts in Thailand (46%), Japan (64%), and France (65%).

For Fannie Wurtz, Head of the Distribution & Wealth and Passive Division, the Decoding Digital Investment report provides a highly valuable resource for those seeking to understand the changing expectations and behaviors of investors. “The study highlights the importance of professional investment advice: almost three times more investors who receive support—whether through people, meetings, or digital channels—have established a structured investment plan. While the use of digital channels continues to grow globally, promoting financial education and developing a hybrid advice model is more essential than ever to help investors achieve their long-term investment goals,” says Wurtz.

A Wide Variety of Digital Information Sources

Focusing on the report’s findings, it stands out that nearly three in four retail investors worldwide (73%) obtain investment information or advice through digital means, with this figure being lower in Europe (69%) and higher in Asia (76%). 38% of respondents favor influencers on television, radio, podcasts, blogs, and social media for investment guidance, while 31% prefer to go directly to the website of the investment service provider.

Regarding specific social media platforms, YouTube is the most influential among retail investors (72%), followed by Instagram (49%) and Facebook (46%). European investors are less likely to turn to digital influencers, especially those aged between 51 and 60. Although the use of digital information sources is high, the need for human advice remains important and continues to play a significant role in investors’ decision-making.

Professional Advice Through a Hybrid Model

The study shows that more than half of investors (55%) do not have a well-developed long-term financial plan, but those who do are four times more confident in achieving the goal of a financially comfortable retirement than those who don’t. It is also noted that those who receive professional advice (digital or in-person) are nearly three times more likely to have a plan than those who do not, indicating the vital role that advice plays in its various forms.

Exclusively digital investors (19%), however, are much less likely to access professional advice (whether in-person or digitally), meaning they have less confidence in their investment decisions (62% vs. 69%) and in reaching their investment goals.

The results also show that retail investors value human professional advice, especially when it comes to long-term financial planning. However, even analog investors are interested in improving their knowledge and exploring online investment options. This demonstrates the need to explore hybrid models to holistically meet investors’ needs.

Retirement: The Main Investment Goal

When asked what drives people to invest, the primary reason globally is a comfortable retirement (41%), followed by maximizing returns (39%). People generally seem confident in their investment decisions, but this does not translate into an expectation of achieving their retirement goals. Two-thirds (66%) of respondents believe they are making the right investment decisions, but only one in four (26%) feel they are on track to obtain the income needed for retirement. This may be due to more than half (54%) of global investors lacking a solid financial plan to support their decision-making.

The Particular Case of the Retail Investor in Spain

In Spain, overall, Spanish investors are slightly less likely than the European average to invest through digital platforms (72% vs. 78% in the EU). Notably in Spain, half of the investors have a well-developed long-term financial plan, compared to 39% of investors in the EU.

Specifically, men (40%) are more convinced than women (30%) to invest for a comfortable retirement, long-term financial security, or to retire early (32% vs. 16% of women). Likewise, 65% of Spanish investors are confident in making the right investment decisions, but only 22% feel very confident about achieving a financially secure retirement. By asset type, Spaniards are slightly more aware of ETF investments (53% vs. the 48% European average), but less likely to invest in them (21% vs. 27%).

Regarding influences, Spanish investors (38%) generally trust social media slightly more (compared to 30% of European investors). Specifically, nearly two-thirds (63%) of people aged 21 to 30 have made an investment decision based on information from an influencer (compared to 32% of investors aged 51 to 60). In this regard, Spanish investors agree that these decisions have proven successful (87% vs. 80% of European investors).

BECON Investment Management organized a breakfast for women in the financial industry in Miami at the Tiffany & Co location in the Design District. At the event, attendees were able to admire the store of the famous jewelry house, which was reopened a year ago after a renovation inspired by the connection that American artist and designer Louis Comfort Tiffany had with the city.

Alexia Young, International Sales Representative at BECON IM, was the host of the event and explained that the choice of location for the gathering was related to the desire to bring the firm’s clients together in a space that offers a “sensory experience” like no other.

As the group toured the location, guided by the jewelry store’s specialized staff, the women were able to admire the Bronze Venus Italica by Daniel Arsham, stunning hand-blown glass chandeliers by Venini, and captivating ceramic table lamps by artist Peter Lane.

On the second floor, they paused to view some of the store’s most exquisite jewels, such as a morganite ring, a gemstone from the beryl family—the same mineral family that includes other famous gems like emerald (green) and aquamarine (blue). Its characteristic color ranges from soft pink to peach, and it was given its name in 1911 in honor of the renowned banker J.P. Morgan, who was a gem collector and a major client of Tiffany & Co.

They also explained the story behind the brand’s famous blue box, the “Tiffany Blue Box”, one of the most recognizable symbols of luxury in the jewelry world and a marketing masterpiece. In 1845, the brand launched its first Blue Book, an annual catalog of fine jewelry, and chose a distinctive shade of blue for its cover. This catalog could not be requested; you were selected to receive it, and it became a symbol of social status in New York. Its color, which would later become known as Tiffany Blue, became synonymous with the brand. The catalog evolved into the box, and today it remains a coveted item and a symbol of exclusivity—to the extent that employees of the company are forbidden from giving away a box unless it accompanies a legitimate purchase.

The tour concluded with a breakfast in the “Comfort Lounge,” a speakeasy that pays tribute to Louis Comfort Tiffany, named after his estate, Comfort Lodge, which was located on the now-vanished Millionaire Row of Brickell Avenue in the 1930s.

Alexia Young wanted to remind attendees that, like the jewels of Tiffany & Co., the funds distributed by BECON Investments can also be considered gems within their respective asset classes.

Morgan Stanley launched a new digital platform aimed at the most active traders. It is called Power E*Trade Pro and is currently in pilot phase. Its full launch is scheduled for June. The announcement appears on the E*Trade website, where a video explains some of its functionalities.

“Our sophisticated trader group is very important to us,” said Jed Finn, Head of Wealth Management at Morgan Stanley, to Bloomberg news agency. Finn explained that the firm asked the most sophisticated active traders in the industry what they needed “to take your game to the next level.”

The new E*Trade platform will allow traders to customize up to 120 tools across six screens in a desktop application separate from the company’s current web and mobile products. On the website, it is announced that it will have “near-unlimited customization and multi-monitor support,” as well as “advanced charting and technical analysis,” with over 145 technical studies and drawing tools. It will also include “simplified tools such as customizable options chains, and the ability to track and trade futures.”

The launch coincides with the high volatility currently affecting financial markets due to Donald Trump’s tariff policy, which unleashed a trade war but in turn drove up trading volumes on brokerage platforms. At E*Trade, April 4 and 7 were the two highest-volume days in over three years, according to Finn. The tariffs were announced by the U.S. President on April 2, called by Trump “Liberation Day.”

In October 2020, Morgan Stanley completed the acquisition of E*Trade for 13 billion dollars, marking the largest acquisition by a major U.S. bank since the 2008 financial crisis. This move significantly expanded Morgan Stanley‘s wealth management capabilities, adding more than 5 million retail client accounts and approximately 360 billion dollars in assets.

With this new platform, Morgan Stanley will compete directly with Thinkorswim, from Charles Schwab, and Legend, from Robinhood Markets.

BBVA opens its third International Private Banking hub in Spain, after the U.S. and Switzerland

Latin American clients have around half of their wealth outside their country of origin, and Spain is in their sights: it has become an attractive destination, not only in terms of financial and real estate investments, but also due to factors such as language, quality of life, and security. This has led BBVA to create a specialized International Private Banking unit in the country, with the goal of serving global clients who wish to invest in Spain. This new unit joins the platforms already existing in Switzerland and the United States, reinforcing BBVA’s international model and consolidating Spain as a strategic hub in its global offering of high-value-added services.

The entity, which already has 583 international clients in this unit in Spain, with 440 million euros in volume and a growth of 43 clients so far in 2025, had been working over the past three years with Latin American clients through its local private banking; now, the business achieved has provided the incentive to give it this new international structure, with slightly different protocols. Although no specific growth objectives have been set, they are ambitious about what can be achieved in international private banking and believe this is just “the tip of the iceberg,” explained Fernando Ruíz, Head of Private Banking at BBVA in Spain, in a meeting with journalists.

Because the creation of a specialized private banking unit that only serves international clients allows for better adaptation to those clients (who have their particularities, such as, in the case of Latin Americans, the appetite for real estate or investments in dollars), expanding the group’s international offering to a third market and becoming a reference in Spain in international private banking, taking advantage of the group’s positions and synergies in Latin America. “Having a specialized team will allow us to better understand the client, analyze how they invest, and adapt,” he said, with a relationship model that is in-person (through the dedicated office in Madrid and trips to the countries of origin) and digital communication and operational capabilities.

To this office, located at Goya 31, which represents a first step, more centers could soon be added in potential areas such as the Mediterranean coast, cities like Barcelona, or the Northwest area (Galicia especially), leveraging the 218 locations where BBVA’s local private banking is present in Spain. “In the U.S. we started with centers in Miami and then expanded to Houston (Texas) and California. In Spain, we could follow the model, as long as we see that it is convenient for international clients,” stated Jaime Lázaro, Head of Asset Management & Global Wealth.

Colombia, Mexico, and Peru

The new unit is born with the aim of offering an exclusive service adapted to the particular needs of international clients, especially those from countries like Mexico, Colombia, and Peru, who seek to diversify their wealth outside their places of origin. The Goya office has a team of five professionals dedicated to those clients, composed of Javier Domínguez Freijo, as director, and four bankers: Alejandro Valverde Carranza (for clients from Mexico), Silvia Díaz Henao (Colombia), Gonzalo Martín Soria (Peru), and María López Moral (other geographies). All of them—highly specialized bankers with exclusive dedication, capable of understanding the wealth, tax, and legal particularities of each country—were already working in BBVA‘s private banking. The team will also grow with the business, with a preference for internal talent although external hires are not ruled out.

“Latin American clients have 50% of their wealth outside their country of origin. In some cases, they want to diversify and we help them come to Spain; in other cases, the clients are already here and we serve them with the support of the LatAm franchises. In the end, they are usually clients with investments in some Latin American country, who asked us about BBVA’s offering in international private banking and now, as a third path in addition to the U.S. and Switzerland, we can offer them Spain,” added Ruíz. “With this new unit, our goal is to elevate and differentiate international private banking in Spain, replicating the model of excellence we already offer from our offices in Switzerland and the United States. We have created an exclusive, highly specialized team, capable of meeting the specific needs of international clients, in many cases different from those of national private banking. We want to offer a unique service in the Spanish market, both to those who reside in the country and to those who have interests here from other geographies,” he added.

Clients can access the international private banking offering starting from 500,000 euros, under the same conditions as local private banking, and with the same service standards, in which BBVA Patrimonios and the ultra-high-net-worth unit come into play. Currently, the average volume of international clients is around 800,000 euros. Of these clients, about half are from Colombia, 30% from Mexico, and 20% from Peru. According to the firm, the end of the Golden Visa in Spain will not be a determining factor for the arrival or withdrawal of investments, just as it has not been a significant attraction lever in recent years.

Under the umbrella of the international platform

The value proposition of this specialized unit is based on BBVA’s international platform, Global Wealth, which connects all the Group’s local banks and enables global and consistent service in any geography. In this way, the personalized attention provided by the team of the new Madrid office is complemented by close coordination with the bank’s local teams in the clients’ countries of origin, ensuring comprehensive wealth management at the international level, the firm explains.

“Private Banking is one of the strengths of the BBVA Group, and therefore our global private banking unit, Global Wealth, has as a priority objective to provide a unique and consistent experience to clients with interests in different geographies, becoming their best financial ally through a relationship and advisory model that is transparent, complete, and consistent in all our processes and wealth solutions,” stated Lázaro.

The person responsible for these units recalled the strength of their service, between local and global, and the strategic priority represented by the development of private banking for the group, already present in nine markets, in Europe (Spain, Switzerland, and Turkey) and the Americas (Uruguay, Argentina, Peru, Colombia, Mexico, and the U.S.), with 200 billion euros in assets. “We want clients to perceive that they are working with a single bank, even if they have accounts in more than one country,” he said, assuring that the bank’s communication circuits will enable holistic and global advisory and reporting.

BBVA offers these clients not only specialized bankers but also expert teams in wealth planning and strategic analysis. Notably, the Global Wealth Planning area, present in Spain, Mexico, and Switzerland, enables efficient and personalized wealth structuring. The bank also collaborates with prestigious international firms, as well as with local firms in each country, to provide complete coverage on legal and tax aspects.

A tailored value offering

Specifically, the value proposition for international private banking clients—coordinated between the experts of the international unit and the locals in each geography—is focused on wealth planning, as well as services in high demand such as real estate (with BBVA’s agreements with Intrum and CBRE), alternatives (in which the bank has recently launched proposals), financing facilitation, arrival and residency support in Spain (with agreements with leading entities), assistance to companies and families to transfer wealth from generation to generation, and the same products available to local private banking clients.

In terms of investment solutions, BBVA’s international clients have access to discretionary management portfolios or advisory services tailored to their risk profile and currency, proprietary and third-party funds (via Quality Funds), private market opportunities, customized financing, real estate services with specialized brokers, international payments solutions, and premium cards with global benefits, as well as advice on business investments. Thanks to the international network of the BBVA Group and the global capabilities of its various areas such as BBVA Research, BBVA Asset Management, Quality Funds, or Corporate & Investment Banking (CIB), the entity can offer a comprehensive, flexible, and dynamic approach to wealth management, adapted to the circumstances and objectives of each client.

“It’s about giving them the same as in Spain, but with adaptations to their peculiarities—for example, adjusting their investments in dollars. We also remind that in all countries BBVA facilitates product offerings through open architecture via BBVA Quality Funds. We don’t want the client’s preference to be conditioned by the product offering, which is available in the three international private banking centers,” added Lázaro. The offering also includes services beyond traditional financial ones, such as educational, sports, or cultural topics.

Growth in local private banking in Spain

In this context, BBVA’s private banking in Spain continues to grow strongly. The entity manages nearly 140 billion euros in assets under management and has 158,000 clients and 722 bankers. The objective is to reach 200,000 clients in three years and manage 150,000 investment portfolios in the next two years, thus consolidating its personalized advisory model based on the combination of the banker’s knowledge and technological support.

Vontobel has announced the appointment of Ana Claver to the firm as the new Head of International Clients. According to the firm, in her new role she will be responsible for leading Vontobel’s distribution business in EMEA (excluding DACH), US Intermediary, US Offshore, and Latin America.

The firm highlights that Claver brings extensive experience in senior leadership roles at a global level and a proven track record in developing client-oriented solutions and partnerships across a wide range of markets. She joins Vontobel from Robeco, where she recently served as Head of Wholesale Sales in Europe. Previously, she was Managing Director of Robeco Iberia, U.S.Offshore, and Latin America. Her professional experience also includes senior roles at Morgan Stanley, Venture Consulting, and UBS. She holds a degree in Economics and Business Administration from ICADE in Madrid and is a CFA Charterholder.

Following the appointment, Christoph von Reiche, Head of Institutional Clients, stated: “We are pleased to welcome Ana to Vontobel. Her experience and strategic vision will help accelerate our expansion and deepen our commitment to clients in key markets. This appointment reflects our dedication to partnering with our clients and delivering innovative investment solutions that meet their evolving needs.”