UBS Florida International announced that Ana Sofía Dominguez and Eduardo Carrera have joined the UBS International Florida Market office in Coral Gables. Both come from Citi, where they each worked for over 10 years.

The welcome was extended by Jesús Valencia, Market Director of UBS Florida International Market.

Valencia shared a post on his personal LinkedIn profile, stating that “with Eduardo’s support, Ana Sofía will leverage her years of financial experience to provide tailored strategies to ultra-high-net-worth individuals in Latin America and the U.S., with a special focus on families with ties to the Southern Cone of Latin America.”

“As part of a leading global wealth manager, Ana Sofía and Eduardo will bring well-thought-out strategies and innovative solutions for every dimension of your financial life,” he added on the professional platform.

Ana Sofía Dominguez joins from Citi, where she spent over 18 years in various roles. Her most recent position at Citi was Director and Private Banker for Ultra High Net Worth clients. She previously worked at Lehman Brothers, MultiCredit Bank Panama, and Banco Santander. At Citi, she also served as Co-Chair of Women in Wealth Latam.

Eduardo Carrera served as an Associate Banker at Citi, where he worked for 14 years in multiple roles. He holds a degree in Industrial Engineering from the Pontificia Universidad Javeriana in Bogotá, Colombia, and a Bachelor’s in Business Administration from the University of South Florida. He also holds FINRA Series 7 and Series 66 licenses, according to his LinkedIn profile.

Uncertainty Over U.S. Trade Policy Has Given Rise to Three Scenarios for the Country’s Economic Outlook: Light Tariffs, Trade War, or a Broader Economic and Financial Crisis Including the Introduction of Capital Controls in the U.S., According to Scope Ratings.

“The recent announcement of U.S. trade tariffs marks a notable escalation in the protectionist policy adopted by the Trump Administration,” says Alvise Lennkh-Yunus, Head of Sovereign and Public Sector Ratings at Scope.

“If implemented, the tariffs would represent the largest peacetime trade disruption to the global economy in more than 100 years. If maintained, this policy will have significant credit implications not only for the U.S. (AA/Negative) but also for other countries around the world,” Lennkh-Yunus states. “Even a full reversal, though unlikely, would not fully restore trust in previous alliances and supply chains, indicating a degree of lasting economic loss.”

In the “light tariffs” scenario, tariffs serve as a starting point for negotiations, with most countries appeasing the U.S., resulting in a slightly more protectionist equilibrium. Key implications include short-term growth and inflation volatility. A technical recession in the U.S. may cause modest effects on global demand and supply chains; growth and credit risks remain mostly contained.

In the “trade war” scenario, tariffs are high and permanent, with significant escalation and retaliatory tariffs. According to Scope’s projection, this leads to sustained pressure on growth and inflation in the medium term, with the U.S. likely entering a recession during the year. The impact on growth and credit quality for trade partners would depend on the depth of trade ties and existing vulnerabilities.

In the most severe scenario, a “broader economic and financial crisis”, tariffs are permanent, tensions between the U.S. and China intensify, and the European Union imposes broad countermeasures. Scope Ratings’ scenario includes the U.S. introducing capital controls and rising doubts about the dollar as a global safe-haven asset. Under this outlook, the U.S. falls into a multi-year recession, and countries with significant economic and/or financial exposure to the U.S. are heavily affected.

The final impact on growth, inflation, public debt, external credit metrics, and hence sovereign credit ratings will ultimately depend on the macroeconomic environment shaped by U.S. policy decisions, the responses of trade partners, and countries’ underlying credit strengths and vulnerabilities prior to this trade conflict.

The possible responses from U.S. trade partners range from appeasement through negotiations to a combination of countermeasures, new free trade agreements among themselves, and deeper domestic economic reforms to at least partially offset the adverse effects of U.S. tariffs.

“In our ratings, we will assess both the magnitude of the trade-related disruptions and the adequacy and quality of regional and national monetary and fiscal policy responses, focusing on countries’ fiscal adjustment capacity and underlying economic resilience to absorb and reverse the long-term impact of the situation,” says Lennkh-Yunus.

One of the most exposed countries is the U.S. itself, as the epicenter of this unorthodox policy shift—especially under Scope’s more extreme scenarios.

“In a prolonged trade war and/or the introduction of U.S. capital controls, viable alternatives to the dollar could emerge. For example, China and the EU might decide to deepen their trade relationship, and/or China could further liberalize its capital account, and/or the EU might accelerate its Capital Markets Union. These developments are unlikely to happen quickly, but if doubts were to grow about the exceptional status of the dollar, this would be very credit-negative for the U.S.,” Lennkh-Yunus affirms.

Countries with large trade surpluses and/or financial exposure to the U.S. are also highly vulnerable to the adverse consequences of the shift in U.S. trade policy, although the impact in Europe is expected to be uneven.

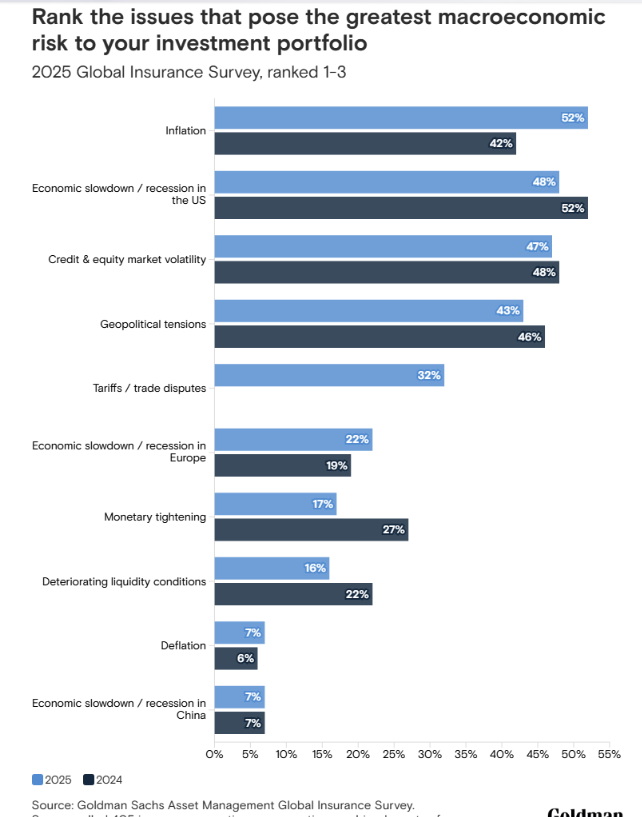

The global insurance industry is shifting toward more diversified and illiquid investment portfolios, according to findings from the 14th Global Insurance Survey by Goldman Sachs Asset Management.

The survey, which included 405 participants representing over $14 trillion in insurance assets, revealed that 62% of insurers plan to increase their allocations to private assets over the next year. Among these, private credit stands out, with 61% of respondents ranking it among the top five asset classes expected to deliver the highest total returns over the next 12 months.

This growing confidence in private assets comes as insurers increasingly believe that credit quality has stabilized. Nearly one-third of insurers are prepared to take on greater credit risk. “As the market expands, more financing opportunities could emerge, offering attractive returns to insurers while diversifying their direct lending portfolios,” says Stephanie Rader, Global Co-Head of Alternative Capital Formation at Goldman Sachs Asset Management.

Over the next two decades, $84 trillion in wealth is expected to change hands. Vanguard sees this as an opportunity for advisors to deepen client relationships and strengthen their businesses through wealth transfer planning. For this reason, the XI Investment Summit by Funds Society will be the ideal occasion for the global asset manager to present its Advisor’s Alpha approach, coinciding with the 25th anniversary of this service model.

The event, scheduled for May 15–16 at the PGA National Resort in Palm Beach, is aimed at professional investors covering the U.S. Offshore market in South Florida.

In a presentation titled “Connecting and Strengthening Client Relationships for the Future”, Colleen Jaconetti, Senior Manager at Vanguard’s Investment Advisory Research Center, will reflect on the origins of the Advisor’s Alpha approach, its impact on the advisory industry, and its role in improving outcomes for both advised clients and advisory practices.

Over the past 25 years, Vanguard and the investment advisory community have maintained a close collaboration, with advisors widely adopting the Advisor’s Alpha framework, the firm stated in a press release. This collaboration has led to a significant transformation in how advisors manage client portfolios.

Vanguard believes that advisory practices have shifted toward more transparent and value-added activities, resulting in significantly improved investment outcomes for advised clients and stronger performance for advisory businesses, while expanding the addressable market for advice. The widespread adoption of this approach has brought greater focus to asset allocation, fund selection, financial planning and wealth management, and behavioral coaching—leading to better results.

About Colleen Jaconetti

Colleen Jaconetti has more than 25 years of experience in the financial services industry and has spent nearly her entire professional career at Vanguard. She currently serves as Director of the Investment Advisory Research Center. Prior to this role, she was Director of Investment and Retirement Income Research within the Vanguard Institutional Investor Group, where she led the development and positioning of Vanguard’s holistic retirement income offering for defined contribution plans, including thought leadership, services, advice, and products.

She also led the global Retirement Income Research team within the Vanguard Investment Strategy Group, conducting research and providing thought leadership on retirement accumulation and decumulation. Earlier in her career, she worked as a financial planner in Vanguard’s Personal Financial Planning and Advice Services departments, creating comprehensive financial plans and supporting the development of Vanguard’s advisory products and services.

She holds a degree in Mathematics, an MBA from Lehigh University, and is both a CPA and a CFP®.

Founded in the U.S. in 1975, Vanguard is one of the largest investment management firms in the world, with a presence in Europe, Australia, Asia, and the Americas. Its mission is to champion all investors, treat them fairly, and give them the best chance for investment success.

Boreal Capital Management Miami announced in a statement on Monday, May 5, that during fiscal year 2024 it increased its business volume in Miami to $2.951 billion, representing a 40% increase since 2022.

“We have a very clear value proposition, focused on our highly personalized private banking and our expert wealth management,” said Joaquín Frances, CEO of Boreal Miami. “We are committed to providing our clients with personalized attention, tailoring our services to their needs. Our steady growth is the best proof that our clients trust us and value what we do.”

The Boreal professional team grew by 7% compared to 2023, and the combined number of clients—together with Boreal Capital Securities, a subsidiary of MoraBanc—increased by 3.4% year-over-year.

“Boreal’s successful year contributed to the global growth of its parent company, MoraBanc, which increased its assets under management by 67%, reaching €18 billion. MoraBanc’s profits rose by 12%, to €57.7 million, and it reported a CET1 fully loaded capital ratio of 19.47%, well above the European banking average of 16%. MoraBanc’s acquisition of the Spanish securities firm Tressis also contributed to its 2024 results,” the firm noted.

Boreal Capital Management Miami, a subsidiary of the MoraBanc Group, is an asset management and advisory firm based in Miami. It partners with Boreal Capital Securities, a registered broker-dealer and subsidiary of MoraBanc. Through its business platform, Boreal offers clients a transparent and flexible model that supports multiple custodians. Pershing, a Bank of New York Mellon company, is its preferred custodian.

During the first quarter of the year, Mexican Afores surpassed $350 billion in assets under management for the first time in history, according to final figures from the regulatory agency.

The Afores ended the first three months of the year with a total balance of MXN 7.194 trillion, equivalent to $359.7 billion, based on an average exchange rate of 20 pesos per dollar—the rate at which the Mexican currency was traded during the first quarter.

The accumulation phase for Mexican Afores is nearing its end, and according to industry representative Guillermo Zamarripa, it may have already concluded. Other analysts also point out that the era in which Afores received significantly more contributions than pension payments is drawing to a close.

However, the gradual increase in worker contributions—outlined in the major 2020 pension reform—has been a key factor in allowing Afores to continue capturing inflows and, to some extent, slow or delay the deaccumulation phase, which is nonetheless expected to arrive by the end of this decade.

In the meantime, Afores continue to attract growing assets, having increased by over MXN 1 trillion in the past year, driven primarily by capital gains.

According to Consar, by the end of March, Afores managed 68.682 million retirement savings accounts, with total assets of MXN 7.194 trillion, representing 17% annual growth—an increase of MXN 1.05 trillion (or $52.5 billion) over the previous year.

Experts clearly identify two key drivers behind the increase in Afore assets:

Capital gains, reflecting the growing pool of assets under management and resulting in higher benefits paid to workers.

The mandatory contribution increases introduced by the 2020 reform, which will remain in effect until 2030, when the total contribution rate is expected to reach 15% of workers’ income.

Thanks to the 2020 Retirement Savings System (SAR) reform, employer contributions to workers’ Afores are gradually increasing through 2030. Before the reform, employer contributions stood at 5.15% of the worker’s salary. Starting in 2022, they began to rise, reaching 8.42%, and for 2025, they have increased to 9.51%.

The reform’s goal is for employer contributions to reach 13.88% of the worker’s salary by 2030, raising total contributions to 15%, up from 6.5% prior to the reform.

Record Capital Gains

Capital gains have also reached unprecedented levels. In just the past 12 months, Afores posted a record MXN 770.631 billion in gains, equivalent to $38.531 billion.

During the January–March 2024 period, despite the risks posed by the arrival of President Trump in the U.S. and his aggressive tariff policy, Afores recorded gains of MXN 307.838 billion ($15.391 billion), marking a record for a first quarter.

In this context, Mexico’s pension system—with Afores as one of its core pillars—continues to deliver positive results for workers and is consolidating its role as the most important driver of national savings, alongside the banking system.

A new global analysis by Ortec Finance shows that clients are increasingly focused on the ESG credentials of their investment portfolios. However, many wealth managers and financial advisors lack the tools and systems needed to effectively track and manage ESG and climate risks, and the industry must invest heavily to improve.

Around 90% of respondents in the study—comprising wealth managers and financial advisors whose firms collectively manage approximately £1.207 trillion—said they are seeing more clients focused on the ESG credentials of their portfolios, with 12% reporting a drastic increase.

This trend is expected to intensify, with 85% agreeing that client focus on ESG factors in their portfolios will increase over the next 24 months. Only 14% believe this focus will remain the same during that period.

93% of respondents say they are seeing more clients looking to avoid funds and stocks that invest in companies or sectors that harm the environment or contribute to climate change. About 83% report increased client attention to the climate risk potentially affecting their investment portfolios, with 38% of those observing a drastic increase.

Despite this growing focus, only 1% of respondents say they have “very effective” systems and tools to review ESG or climate risk in clients’ funds, stocks, or portfolios. An additional 71% consider their tools and systems to be “fairly effective,” while over one in four (27%) rate their ESG and climate risk review and monitoring tools as only “average.”

Overwhelmingly, more than 94% of respondents agree that the wealth and portfolio management industry must make significant investments in new technologies and systems to improve their understanding of ESG and climate risk factors across client portfolios, as well as in funds and equities more broadly.

“Wealth managers and financial advisors need to be equipped with the right tools and systems to fully analyze and understand the degree to which their clients are exposed to ESG and climate-related risks—especially as this is an area clients intend to focus on more in the coming years. Our research shows that many in the sector feel they lack the proper tools, systems, and resources, so it’s vital that organizations invest in order to empower both themselves and their clients to make the most informed investment decisions,” concludes Tessa Kuijl, Head of Global Wealth Solutions at Ortec Finance.

Banco Santander has agreed to sell to Erste 49% of the capital of Santander Polska for approximately 6.8 billion euros and 50% of its asset management business in Poland (TFI) not controlled by Santander Polska for about 200 million euros, bringing the total amount to around 7 billion euros. The transaction is subject to customary conditions in this type of deal, including the corresponding regulatory approvals.

The transaction, entirely in cash, will be carried out at a price of 584 zlotys per share, which values the bank at 2.2 times its tangible book value per share as of the end of the first quarter of 2025, excluding the announced dividend of 46.37 zlotys per share, and at 11 times 2024 earnings. Additionally, it represents a 7.5% premium over Santander Polska’s May 2, 2025, market closing price, excluding the dividend, and a 14% premium over the volume-weighted average price of the past six months. Santander Polska shares will trade ex-dividend on May 12, 2025.

Following the transaction, Santander will hold approximately 13% of Santander Polska’s capital and intends to acquire the entirety of Santander Consumer Bank Polska before closing by purchasing the 60% currently held by Santander Polska.

The closing of these transactions, expected around the end of 2025, will generate an approximate net capital gain of 2 billion euros for Santander, representing an increase of about 100 basis points in the group’s CET1 capital ratio, equivalent to approximately 6.4 billion euros, and will place the pro forma CET1 capital ratio around 14%.

Strategic collaboration In addition to the acquisition, Santander and Erste announce a strategic collaboration to leverage both entities’ capabilities in Corporate & Investment Banking (CIB), and to allow Erste access to Santander’s global payment platforms, in line with the group’s strategy to become the world’s best open financial services platform.

In CIB, both Santander and Erste will leverage their respective regional strengths to offer local solutions and knowledge of their respective markets to corporate and institutional clients through a referral model that will facilitate client interactions and an agile service offering. In addition, Santander will connect Erste clients with its global product platforms in the United Kingdom, Europe, and the Americas. Both entities will collaborate as preferred partners with the aim of building long-term, mutually beneficial relationships that maximize joint business opportunities.

In payments, the entities will explore opportunities for Erste, including Santander Polska after the transaction closes, which will allow it to leverage Santander’s capabilities and infrastructure in this area, including its PagoNxt payments business.

Santander’s strategy is focused on generating sustainable value for clients and shareholders, through common platforms across each of its five global businesses, enabling the best client experience at the lowest service cost and taking advantage of the group’s network and economies of scale.

Since announcing a new phase of value creation in 2023, Santander has added 15 million new clients, improved its efficiency ratio from 46.6% to 41.8%, and increased its earnings per share by 62%.

Regarding this sale, Ana Botín, Executive Chair of Banco Santander, commented: “This transaction represents a key step in our shareholder value creation strategy, based both on accelerating platform development through ONE Transformation and on increasing the group’s scale in highly connected markets. Santander is achieving very attractive multiples for its bank in Poland, and Erste is acquiring an exceptional business with a first-rate team that will continue generating value for customers, employees, and other stakeholders of Santander Polska. We will allocate the capital generated by this transaction according to our capital allocation hierarchy, which prioritizes profitable organic growth. We plan to dedicate 50% of the amount (about 3.2 billion euros) to accelerate the execution of the extraordinary share buyback programs by early 2026, possibly exceeding the announced buyback target of up to 10 billion euros, given the attractiveness of these transactions at current prices, subject to regulatory approvals. I especially thank Michał and the entire team in Poland for their outstanding contribution to the group over all these years. It has been an honor and a pleasure to work with you.”

Financial impact Following the transaction’s closing, the group will temporarily operate with a CET1 ratio above the target range (12%-13%), with the intention of gradually returning to that range by reinvesting capital according to the guidelines set in its capital strategy, which prioritizes profitable organic growth and investment in its businesses to achieve cumulative growth in profits, profitability, book value, and shareholder remuneration.

Santander plans to distribute 50% of the capital released by this transaction through a share buyback of approximately 3.2 billion euros. This will accelerate the achievement of the up to 10 billion euros share buyback target from 2025 and 2026 results and projected excess capital. As such, the previously announced target could be exceeded, given the attractiveness of buybacks at current valuations, subject to regulatory approval.

The transaction is expected to have a positive impact on earnings per share starting in 2027/2028, thanks to the reinvestment of capital in a combination of organic growth, share buybacks, and potential complementary acquisitions that meet the group’s strategic and profitability criteria. The generated capital will allow Santander greater strategic flexibility to invest in other markets where it already operates in Europe and the Americas with the goal of accelerating growth, increasing income derived from network collaboration across its five global businesses, and maximizing benefits for clients and shareholders.

Europe, the U.S., and Latin America are strong regions in the asset management industry, but beyond these geographies, one market stands out for its rapid growth: Saudi Arabia. It is estimated that assets under management surpassed the 1 trillion Saudi riyal threshold—approximately USD 266 billion—in 2024, driven by 20% year-over-year growth.

According to Samira Farzad, Director of Business Development at HF Quarters, the industry is undergoing a significant expansion phase, consolidating its status as the largest and most dynamic market within the Gulf Cooperation Council (GCC) region. In fact, assets under management are projected to exceed 1.3 trillion Saudi riyals (USD 350 billion) by 2026. This growth trajectory is being substantially fueled by the Kingdom’s ambitious Vision 2030 economic diversification strategy, which seeks to reduce the country’s historical dependence on oil revenues by developing non-oil sectors, along with support from the Financial Sector Development Program.

According to Farzad, while the current landscape is dominated by domestic asset managers affiliated with banks—who control a significant share of industry fund assets and revenue—the competitive environment is expanding with the entry of renowned international firms such as BlackRock and Goldman Sachs, drawn by the Saudi market’s considerable potential.

“The Public Investment Fund (PIF), the country’s sovereign wealth fund with a target of USD 2 trillion in assets by 2030, acts both as a key capital allocator within the industry and as a powerful direct investor shaping the national economy through large-scale megaprojects like NEOM,” the expert notes.

On the investment front, several key trends are actively transforming strategies. “There is a clear shift beyond traditional investments toward alternative assets such as private equity, venture capital, and private credit, which are complementing the already well-established real estate and equity portfolios. Demand for Shariah-compliant products remains a core feature of the market, influencing product development and asset selection criteria,” adds Farzad.

Another major trend is the rise of ESG considerations, which are rapidly gaining relevance, driven both by global investor preferences and national strategic priorities embodied in initiatives like the Saudi Green Initiative.

“Looking ahead, proactive regulatory reforms and market infrastructure enhancements, led by the Capital Market Authority (CMA), aim to foster a more robust, efficient, and investor-friendly environment, which will support the sector’s continued growth,” concludes the Director of Business Development at HF Quarters.

Major asset owners (LAOs) remain confident that their portfolios are well-positioned to withstand a variety of shocks over the next year. However, according to the latest Large Asset Owner Barometer 2025 published by Mercer, they perceive greater vulnerability compared to the previous year regarding several key risks over the next 12 months, including geopolitical risks (35% vs. 31% in 2024), inflation (31% vs. 22%), and monetary tightening (30% vs. 23%). In fact, over a three- to five-year horizon, perceived vulnerability to most risks has shown a slight increase.

In particular, regulatory risks during this period were cited by 32% of LAOs, marking a significant rise from 20% in the previous survey. This reflects growing uncertainty among asset owners about the future direction of regulation after a year marked by major political shifts and their potential impact on portfolios.

“Equity, fixed income, and currency markets are experiencing extreme volatility due to trade tensions, but based on our data, we see that major asset owners are positioned for the long term and generally remain calm about short-term market movements. That said, in the coming year they plan to make strategic portfolio adjustments, as they did last year, to mitigate risks and seize identified opportunities,” says Eimear Walsh, European Director of Investments at Mercer.

Positioning and Asset Allocation

According to Mercer’s report, over the past year LAOs have taken various steps to protect their portfolios, including adjusting fixed income allocation duration (53%) and modifying geographic asset exposure (47%). Notably, nearly half (45%) of respondents increased their allocation to private markets, a trend expected to continue into 2025.

Looking ahead to the next 12 months, 47% expect to increase portfolio allocations to private debt/credit, while 46% plan to boost allocations to infrastructure. This trend is especially pronounced among the largest asset owners; 70% of those managing over $20 billion intend to increase private debt/credit allocations, and 63% plan to invest more in infrastructure.

“Only five percent—one in twenty—of surveyed asset owners manage their investments entirely in-house. In an increasingly complex investment environment, we see strong appetite among major asset owners to outsource investment management, with the more complex asset classes often being handled by external teams,” notes Rich Nuzum, Executive Director of Investments and Global Chief Investment Strategist at Mercer.

Optimism Toward Domestic Markets

While generally confident in their resilience, European asset owners show greater concern about risks than their U.S. counterparts: 43% of European LAOs believe their portfolios are vulnerable to geopolitical threats over the next 3–5 years, compared to 18% in the U.S.

Unlike major asset owners in the U.S. and the U.K., European asset owners appear more optimistic about investing in domestic equities. 34% of Europe-based LAOs expect to increase their allocations to European equities over the next 12 months. On average, LAOs in the U.S. and the U.K. are more likely to reduce their allocations to domestic equity markets.

There is also evidence that European LAOs, which may have previously had lower exposure to private markets than their U.S. peers, are now looking to close that gap. 48% of European LAOs allocated to private markets in the past 12 months, compared to 27% of those based in the U.S.

Focus on AI

More than two-fifths (43%) of major asset owners surveyed believe that artificial intelligence will be a highly influential factor shaping the macroeconomic environment over the next 5 to 10 years, ahead of geopolitics (34%) and energy transition/climate change (34%). Despite this view, more than two-thirds (69%) of LAOs say they have not yet implemented or started developing an AI/GenAI policy.

Another key trend is the increasing incorporation of sustainable investment objectives among asset owners, though climate transition goals are declining. Larger LAOs (with more than $20 billion in AUM) are more likely to integrate sustainability goals into their investment strategies, with 81% including such objectives in their policies, compared to 64% of smaller asset owners. Additionally, over the next 12 months, 24% plan to increase their allocation to ESG/sustainable funds, and 29% expect to increase exposure to impact strategies.

Despite this, the number of LAOs planning to set climate transition and net-zero targets is decreasing: 39% do not plan to establish net-zero emissions targets, up from 29% last year, and nearly 39% do not plan to set climate transition goals, compared to just 8% the year before.

Mercer, part of Marsh McLennan and a global leader in consulting and investment, publishes the Large Asset Owner Barometer 2025. In it, surveyed asset owners—collectively representing more than $2 trillion in assets—provide key insights into the investment decision-making of the world’s largest capital allocators.