Do you remember what you were doing exactly a year ago? Most likely, you were glued to your Bloomberg terminal or responding to calls and emails from your clients while the S&P 500 index plunged by as much as 18.7% from its peak in February. Yes, it has already been a year since ‘Liberation Day,’ and the image that has gone down in history is that of Donald Trump holding an enormous board listing each of the tariffs that the U.S. was going to apply to countries with which it maintained a large trade deficit—though not exclusively.

For the markets, this staging had another meaning: the return of volatility and uncertainty that continue today, now driven by geopolitics and oil. As Mauro Valle, head of fixed income at Generali AM (part of Generali Investments), points out when taking stock of this first year of a new normal in U.S. trade policy, the most relevant aspect is the changes in the market that have occurred since Liberation Day.

“President Trump’s protectionist policy had two consequences in the months following the announcement of the tariffs. The first was in the bond market, where the yield on the 10-year U.S. Treasury rose sharply. The second, which still largely persists, was a weaker dollar against currencies such as the euro. In fact, the dollar has depreciated in recent months due to other factors such as twin deficits, geopolitics, and the fragmentation of global capital flows. However, in these recent phases of acute risk aversion, it can still strengthen tactically, reflecting its liquidity function. It remains to be seen whether, after this crisis, the dollar will continue to be perceived as a safe-haven asset or not,” explains Valle.

Market Performance

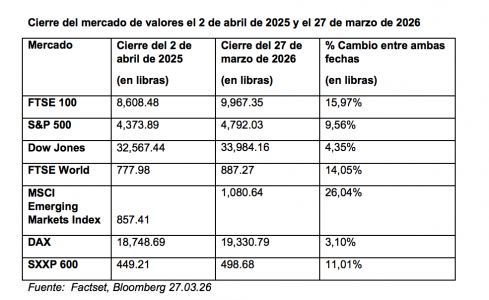

The surprise has been that, despite the initial impact, the balance of the past year shows a different message: emerging markets defied expectations and led the gains in global stock markets one year after the announcement of the Liberation Day tariffs. According to data analyzed by Aberdeen Investments, which focuses on comparing percentage changes to assess how markets have performed across six major global markets between the market close on April 2, 2025, and one year later, on March 27, 2026, overall, most major indices experienced positive dynamics, with emerging markets at the forefront.

According to the asset manager, global stock markets recorded strong gains over the period, but the MSCI Emerging Markets index had the best performance, with a rise of 26%, followed by the FTSE 100, with 16%, and the FTSE World, with 14.1%. Meanwhile, the S&P 500 posted an increase of 9.6%, while the Dow Jones and the DAX recorded more modest gains of 4.4% and 3.1%, respectively.

“During the past year, investors have had to make sense of a great deal of noise and uncertainty, in addition to the human impact of global events. Although we would never want to draw major conclusions from a single year of market data, our analysis is interesting, and this period has served to remind us that headlines do not always tell the whole story. Even at a time when markets and geopolitics seem more entangled than ever, the figures can sometimes point to something different. Our main recommendation has been to encourage investors to diversify their equity allocations and, in that sense, it is encouraging to see that markets outside the United States are leading the way at a time of great uncertainty,” notes Ben Ritchie, Head of Developed Markets Equities at Aberdeen Investments, in light of these conclusions.

Economic Resilience

In the opinion of Jon Butcher, Senior U.S. Economist at Aberdeen, one year after “Liberation Day,” the U.S. economy has demonstrated resilience despite a clear cooling of the labor market. “Hiring slowed sharply in the months following the announcement of the tariffs, as companies assessed rising costs and policy uncertainty. Even so, growth held up better than expected, as households continued to spend and business investment accelerated. Tariffs did boost inflation, but the impact has been slower and smaller than the market initially feared,” says Butcher.

In addition, it is noteworthy that trade in 2025 did not contract, despite gloomy forecasts. “Both U.S. imports and Chinese exports reached new highs. Southeast Asia deepened its role in global manufacturing, India gained ground in selected sectors, and Brazil expanded commodity exports to China. Overall, trade grew faster than the global economy, while advanced economies and China reoriented away from geopolitically distant trading partners,” notes the McKinsey Global Institute in its latest report.

However, according to the think tank of McKinsey & Company in its report, tariffs triggered a reshaping of trade, with trade between the U.S. and China falling by around 30%. “The United States replaced approximately two-thirds of that gap with imports from other suppliers, while Chinese exporters of consumer goods, from electric cars to toys, cut prices by an average of 8% to find buyers in new markets. ASEAN prospered, increasing trade with both economies, but the European Union faced a double pressure: more Chinese imports and higher U.S. tariffs,” they add.

Lessons Learned

This episode leaves several lessons learned. First, according to the McKinsey Global Institute, changes in trade point to some lasting trends and, consequently, to the need for resilience in the face of shocks. “AI, the growth of emerging markets, and the evolution of China’s manufacturing approach are not temporary phenomena, nor is the growing role of geopolitics in reshaping trade, a shift that has been evident in the data for nearly a decade. Short-term developments also require a response. Tariff changes in 2025 were abrupt, and 2026 has already brought its own shocks. Companies need a long-term vision combined with agility,” they note.

Second, the Aberdeen economist warns that the political landscape has become even more uncertain: “The Supreme Court ruling on the IEEPA has cast doubt on the future of the tariff regime, and efforts to rebuild parts of it through other policy tools have left companies unsure about what the long-term rules of the game will be. For markets, the greatest risk is the growing perception among global investors that the United States is becoming a less reliable destination for capital. Concerns have increased about political volatility, central bank independence, and fiscal pressure. And although attention has shifted toward the Iran crisis and energy prices, tariffs remain a critical unresolved factor shaping how international capital perceives the United States.”

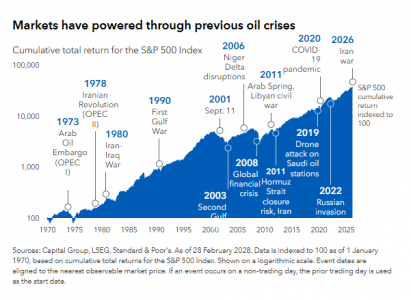

Finally, Capital Group reminds us that when markets are volatile, it is difficult to resist the temptation to do something, but they recommend staying the course. “What is the lesson of ‘Liberation Day’? Market downturns can be painful, but rather than trying to time when to enter or exit the market, the most sensible approach for investors is to stay the course. To weather market volatility, they should seek diversification across equities and bonds, while periodically assessing their risk tolerance in the face of elevated volatility. Although it may seem that this time is different, markets have proven resilient throughout history when faced with wars, pandemics, and other crises,” they insist.