Markets appear to have breathed a sigh of relief following the truce agreement between Washington and Beijing, which includes a reduction in tariffs on Chinese exports to the U.S. from 145% to 30% for a period of 90 days. “The news that China and the U.S. have rolled back policies that, in practice, amounted to a trade blockade between the two countries has been warmly welcomed by the markets. Investors are hopeful that this three-month window will be used to negotiate a lasting agreement that, while unlikely to remove all tensions stemming from strategic competition, at least provides a more predictable environment for companies,” says Sean Shepley, Senior Economist at Allianz Global Investors.

According to experts, markets gained ground, led by cyclical sectors. “In the U.S., inflation stability offered slight relief, though the rise in durable goods prices was not fully offset by the slowdown in service inflation. In Europe, cyclical sectors such as automotive rebounded, though sector rotation began to show signs of fatigue by the end of the period, with defensive sectors making a comeback. Investors are now waiting for a new catalyst, as the good news appears to be already priced in,” summarizes Edmond de Rothschild AM.

According to the firm’s analysis, U.S. economic data for April have yet to reflect the impact of the increased tariffs, either in prices or consumer spending. “The Consumer Price Index (CPI) for the month stood at 2.3%, so the anticipated acceleration has not yet materialized, not even in goods. Services continued to ease. Meanwhile, falling oil prices helped slow energy and food inflation. The Producer Price Index (PPI) showed imported goods prices rising slightly from 2.3% in March to 2.5%,” they note.

With PMI releases still pending this week, analysts at Banca March believe market attention in the U.S. will focus on negotiations over the tax reform promoted by President Trump. “According to House Speaker Mike Johnson, the proposal could go to a vote next Monday. The new law gains relevance after Moody’s downgraded the U.S. credit rating. Market attention will also be on Treasury auctions, particularly a $16 billion 20-year bond issue scheduled for Wednesday,” they explain.

The Truce Between Washington and Beijing

In the view of Paolo Zanghieri, Senior Economist at Generali AM (part of Generali Investments), the unexpected and swift agreement to temporarily de-escalate trade tensions between China and the U.S. shows there is a sort of “Trump option,” even if the exercise price is higher than expected. “Following the truce, we have revised our growth forecasts for the U.S. and the eurozone to 1.6% (from 1%) and 1% (from 0.9%), respectively, and reduced our forecast for Fed rate cuts from three to two by year-end. In terms of asset allocation, we have strengthened our preference for investment grade bonds while maintaining a slight overweight in equities. The peak of uncertainty has passed, and trade protectionists no longer seem to hold the upper hand in the U.S. administration—but caution is still warranted,” explains Zanghieri.

He first points out that the truce with China is temporary, with the suspension of punitive tariffs set to expire on July 8, though he expects it to be extended until the U.S. reaches agreements with key trading partners. “This extension, while welcome, would not fully resolve the uncertainty that continues to hinder corporate capex planning,” he adds.

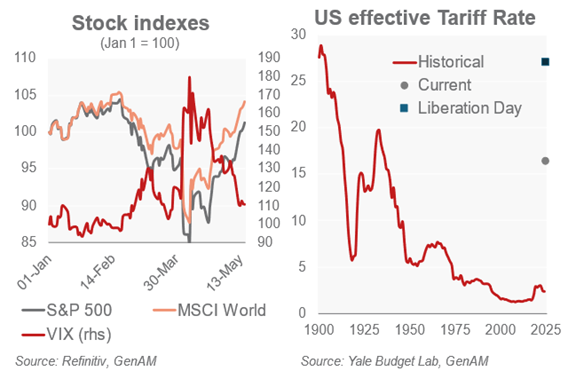

Second, he notes that the universal 10% tariff and the 25% tariffs on steel, aluminum, automobiles, and auto parts remain in effect, with few exemptions, which will impact both growth and inflation. “U.S. trade authorities are still assessing potential security threats from imports of semiconductors, pharmaceuticals, critical minerals, and commercial aircraft, among others, which could trigger new sector-specific tariffs,” he explains.

Lastly, Zanghieri highlights that the only near-finalized deal—with the UK—has very limited scope and includes provisions aimed at excluding China from British supply chains in strategic sectors. “Beijing would strongly oppose this becoming a standard feature of all trade agreements,” he concludes.

Navigating the 90-Day Pause

In the view of Andrew Lake, Chief Investment Officer and Head of Fixed Income at Mirabaud Asset Management, the rhetoric may sound familiar, but this latest chapter in the tariff saga comes with a notable shift: “The real negotiations are not between the United States and its trading partners, but between the White House and the U.S. bond markets.”

According to Lake’s analysis, a subtle yet significant change has emerged in recent weeks: Trump appears far less reactive to stock market volatility than during his first term, when he often measured his success by the performance of the S&P 500. “This time, the key indicator is U.S. funding costs. He wants lower Treasury yields, lower interest rates, and a weaker dollar. When Treasury yields started to break down in April, the tone changed. Now it is the bond market—not equities—that seems to be driving policy adjustments,” they explain. In Lake’s view, with most of the 90-day pause still ahead, markets remain optimistically positioned, buoyed by news of deals with the UK and China.

For Lake, the real question is whether financial markets, encouraged by optimism over tariffs, can look past current data and focus instead on the potentially better economic expectations now being priced in for the second half of the year.

“Clearly, we are in a worse position than at the start of the year, with 10% now seemingly the minimum tariff rate, but that is still much better than the situation just a few weeks ago. Doubts remain, but if this is now the ‘new normal,’ then we would expect agreements with other major trading partners to follow in the coming months. As we return to a ‘wait-and-see’ mode, our positioning remains cautious. Markets are rising on narrative, not fundamentals, and we have been reducing risk during these rallies. We prefer rotating into high-quality credit, where spreads have widened to levels we consider ‘recessionary.’ We are building exposure gradually at attractive entry points,” he concludes.